Liquidity crisis, are longs left only with "death queue"?

TechFlow Selected TechFlow Selected

Liquidity crisis, are longs left only with "death queue"?

The crypto market once again experienced a "bulls' death spiral" in mid-November.

By Murphy

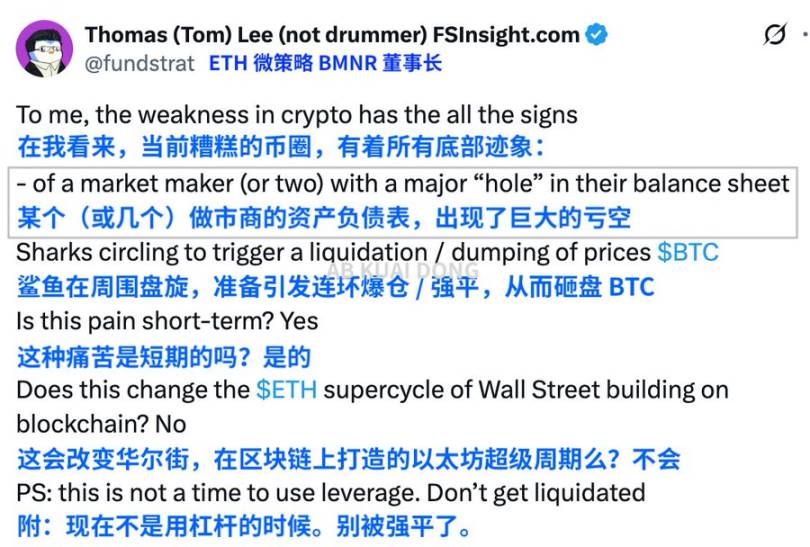

Bitcoin fell below $100,000 and Ethereum dropped 10% in a week, as the crypto market once again experienced a "bulls' death spiral" in mid-November. Tom Lee, Chairman of BitMine—the top institutional holder of Ethereum reserves—and Wall Street analyst, believes the real pressure stems from shrinking market maker liquidity and arbitrage-driven sell-offs by large traders.

Source: X

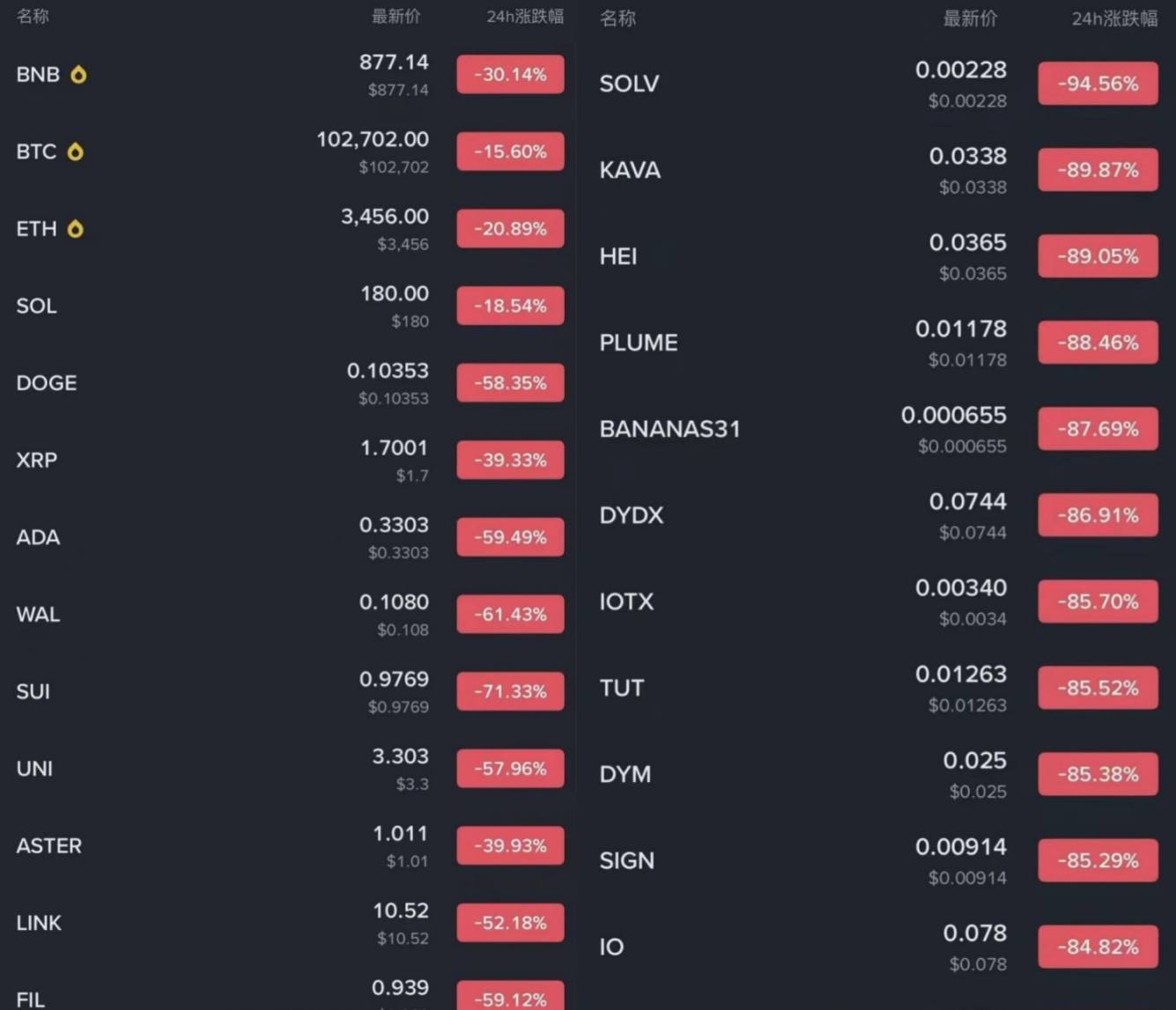

Bitcoin (BTC) has declined from its early October high of $126,000, losing the $100,000 mark within just three days. Bulls and market makers faced consecutive liquidations, briefly dipping to $97,000 with over a 5% weekly drop. After inflows of $524 million into Bitcoin spot ETFs on the 11th, outflows followed on the 12th and 13th at $278 million and $866.7 million respectively, accelerating selling pressure.

Some attribute this move to "whale selling," "Fed expectations reversal," or "market maker retreat." But focusing only on the present risks overlooking a deeper historical pattern: bull markets never end abruptly at peaks. Instead, they automatically digest themselves after the peak through a "liquidation chain."

And the sequence of this liquidation chain never changes.

The first to fall are the "bull faithful"

Source: Binance

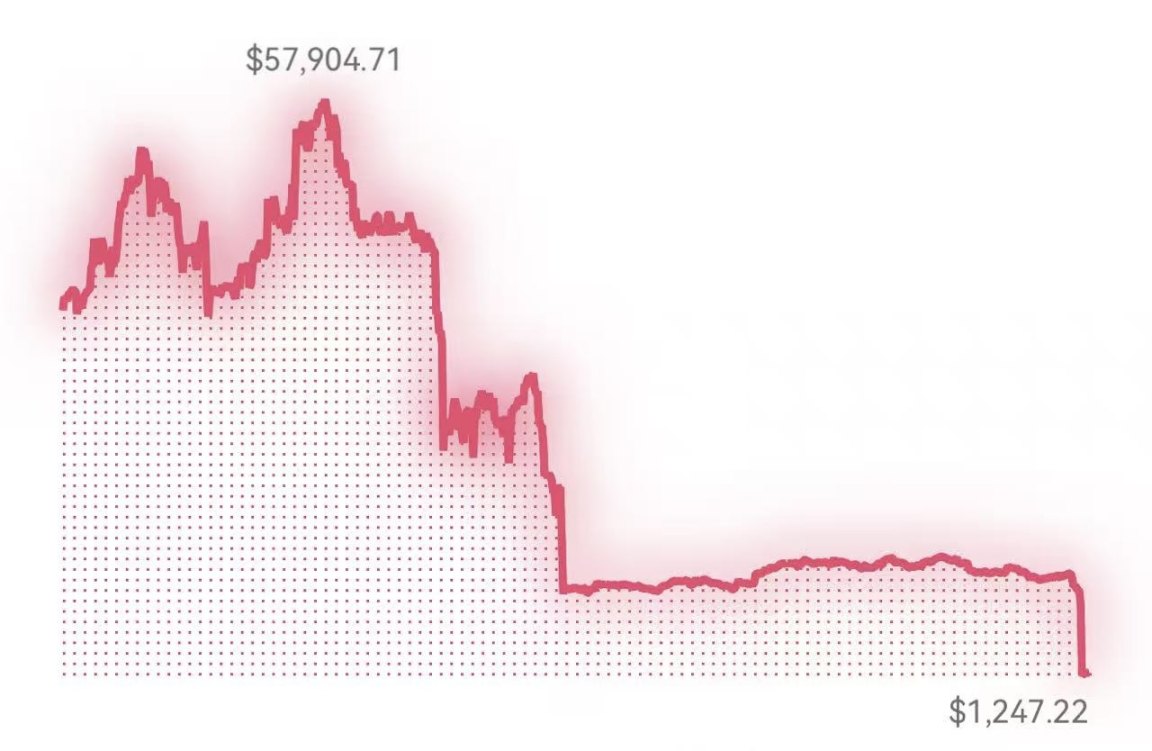

Those shouting "see $140,000 next" or "ETF bull market taking off" at $120,000 are the first to get buried. They added positions heavily at highs, often with high leverage. Even minor price movements trigger automatic cascading liquidations. Then come those who thought low leverage kept them safe. Just like during the flash crash of October 10–11, I myself was one of the low-leverage gamblers caught in this 1011 black swan event—"coin-based, 3X contract, isolated margin, instant liquidation upon entry." Across multiple accounts, my inbox was bombarded with liquidation alerts within minutes—once breached, it spread horizontally.

Hard-earned lesson: Low leverage isn't safety. Liquidation may be delayed, but it always comes.

Source: Author

The second wave: Market makers and quantitative firms

Do you think market makers are invincible? Remember March 12, 2020? Market makers pulled depth down to near-zero levels.

During the 2021 liquidation wave, even Alameda couldn’t hold on.

In 2022 during the LUNA collapse, crypto banks were taken out too.

Stablecoins sequentially unpegged, market makers, lending whales, and quant firms retreated in chains—sometimes becoming the very spark that accelerated the crash. "Market supporters" aren't "permanent backstops." When order book depth thins and hedging costs rise, their goal isn’t to stabilize prices—but to survive.

The third wave: DAT model institutions, token reserve entities, family offices

They act as accelerators in bull markets, but don’t forget—they have no faith, only spreadsheets. Once the logic for price growth stalls, they're the first to pull back. Over the past two weeks, on-chain data shows increasing selling and transfers from these actors—nearly identical to patterns seen in December 2021 and early 2022.

When you piece all this together, the current market resembles the aftershocks following the 2019 ICO bubble—or the prelude to the 2021 liquidation wave.

Combine these three phases and you see the market’s true state: the bull run isn’t dead—it’s just too heavy and needs to "unload cargo."

Bullish momentum is exhausted, market depth has been drained, institutional structured demand weakened, and upward momentum has temporarily dried up.

That said, we’re not yet at the chaotic end of a full-blown bear market. Extreme panic hasn’t emerged on-chain, capital hasn’t fully withdrawn, and whales aren’t dumping in fear. It’s more like a bull story halfway told—narrative intact, but main characters exiting stage left, leaving secondary players in disorganized combat.

Back to the key question: Is this a new bear market liquidation chain?

Judging from historical patterns, on-chain data, market maker behavior, and institutional posture, this does exhibit traits of "early-stage bear market liquidation"—not an obvious crash, but a "chronic blood loss" that gradually reveals the exhaustion of growth logic.

In the coming 1–2 months, if BTC continues testing the $90,000 support level with weak rebounds, then we can confirm:

The first half of the bull market is over. The market has entered a "structural reconstruction phase."

But if capital flows back in, depth recovers, and institutions resume buying (though difficult—most who wanted to buy already have), then this dip would merely be a "mid-bull market cleanse," similar to September 2017 or September 2020—a halftime break.

Everything now sits at a watershed moment.

No matter what, Bitcoin’s trend is always more complex than any chart. The market is now deciding who will be the next to take the hit: complete liquidation of market makers? DAT model institutions? Crypto banks? Reserve-holding small nations?

We can’t clearly predict the path ahead, but what we can do is ditch leverage and abandon侥幸.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News