Jane Street’s Three Sins: Insider Trading, Index Manipulation, and the “Morning Massacre” of Bitcoin

TechFlow Selected TechFlow Selected

Jane Street’s Three Sins: Insider Trading, Index Manipulation, and the “Morning Massacre” of Bitcoin

The Most Powerful Trading Firm You’ve Never Heard Of Has Been Accused of Market Manipulation Across Two Continents—Bitcoin Could Break Free As a Result.

Author: Roberto Rios (@peruvian_bull)

Translated and edited by TechFlow

TechFlow Intro: Jane Street is Wall Street’s most profitable quantitative trading firm—and one of its least known—until this week, when it was accused of insider trading that triggered the Terra Luna collapse, while simultaneously facing a $560 million market manipulation lawsuit in India. This article weaves together Jane Street’s alleged manipulation of Terra Luna, its alleged manipulation of Indian markets, and Bitcoin’s daily 10 a.m. (ET) “10-Point Strike” into a single, rigorously timed investigative thread—complete with verifiable timestamps and data. Bitcoin’s rally today may well be rooted in this story.

Full text below:

The most powerful trading firm you’ve never heard of has just been caught reaching into the cookie jar. Twice. On two different continents.

And Bitcoin has finally been set free.

Come with me:

Jane Street Group is a New York–based quantitative trading firm. It has no CEO.

By its own description, the firm operates like an “anarchist commune.” In just the first nine months of 2025, it recorded $24 billion in net trading revenue—surpassing its full-year 2024 total of $20.5 billion. In Q2 2025 alone, it generated $10.1 billion—the highest quarterly trading revenue ever recorded by any firm on Wall Street.

By any metric, Jane Street is the world’s most profitable trading institution.

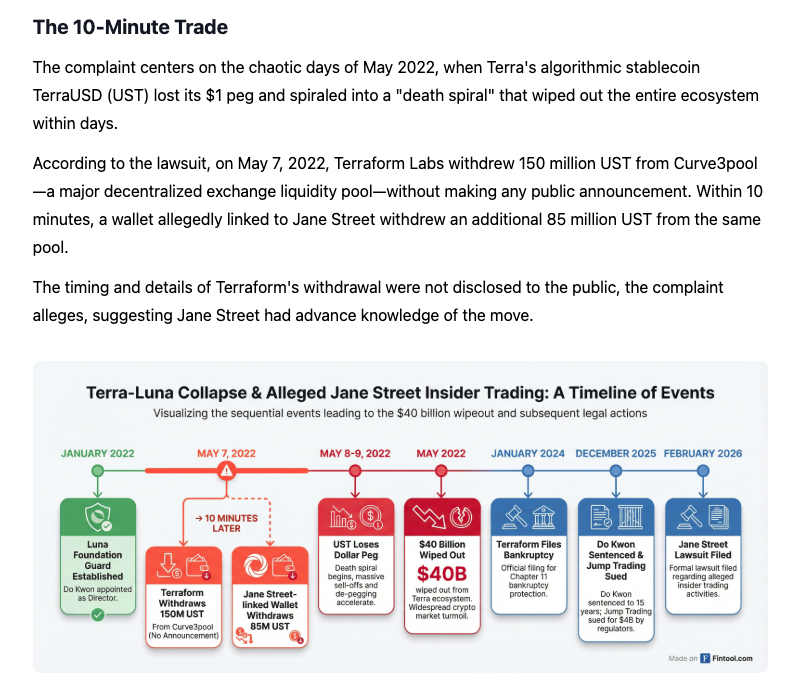

And this week, the Terraform Labs bankruptcy trustee filed suit in Manhattan federal court, accusing Jane Street of using material nonpublic information to front-run and profit from the May 2022 Terra Luna collapse—a crash that erased $40 billion in value and triggered a chain reaction ultimately toppling Celsius, Three Arrows Capital, and FTX.

The logic behind the allegations is shockingly simple.

On May 7, 2022, Terraform Labs quietly withdrew $150 million in UST from Curve’s 3pool—a major decentralized liquidity pool—with no public announcement, only a silent liquidity drain.

Ten minutes later, a wallet linked to Jane Street withdrew $85 million from that same pool.

Exactly ten minutes.

The complaint alleges that Bryce Pratt, a former Terraform intern who joined Jane Street as a full-time employee in September 2021, established a secret communication channel with his former Terraform colleagues—and allegedly passed material, nonpublic information about Terraform’s liquidity operations directly to Jane Street’s trading desk.

The complaint names four defendants: Jane Street Group LLC, co-founder Robert Granieri, and employees Bryce Pratt and Michael Huang.

The bankruptcy trustee’s statement cuts straight to the heart of the matter: the trades executed by Jane Street “could not have occurred absent access to its exclusive possession of material nonpublic information.”

It gets worse. The complaint alleges that Jane Street’s withdrawal helped trigger UST’s depegging, pushing the entire Terraform ecosystem into a death spiral. LUNA crashed from over $80 to near zero. $40 billion vanished. Ordinary people lost everything—retirement savings, college funds, lifetimes of accumulated wealth—gone in days.

Jane Street’s response? It called the suit a “desperate, last-ditch effort” and “baseless allegations.”

But here’s the problem: This isn’t their first time.

In July 2025, the Securities and Exchange Board of India (SEBI) brought one of the largest market manipulation charges in Indian history against Jane Street. SEBI’s investigation found that, across 18 derivatives expiry dates between January 2023 and March 2025, Jane Street executed textbook “ramp-and-dump” manipulation on the Bank Nifty index.

The mechanics are chillingly mechanical:

Early session: Jane Street’s algorithms aggressively bought Bank Nifty constituent stocks and futures, lifting the index 1%–1.3%. SEBI found that on certain trading days, Jane Street alone accounted for the index’s entire positive price impact.

Simultaneously, it built massive short options positions—primarily selling calls and buying puts—with position sizes wildly disproportionate to its equity and futures holdings. SEBI calculated that, in delta-equivalent terms, its options positions were 7.3 times larger than its stock and futures positions. This wasn’t hedging. It wasn’t arbitrage. It was directional manipulation wrapped in unnecessary steps.

Afternoon session: It reversed course—selling all the stocks it had bought earlier. The index fell, short options profited, and the cycle repeated—every single expiry day.

SEBI’s ruling: illegal profits of ₹4.843 billion—approximately $580 million. It characterized Jane Street’s conduct as “a deliberately designed scheme to manipulate settlement prices.” SEBI further noted that Jane Street continued executing this strategy even after the National Stock Exchange of India issued an explicit warning in February 2025.

SEBI’s language was unusually harsh—rare for a regulator: “The fairness of the market, and the trust of millions of small and medium investors and traders, cannot continue to be held hostage by the machinations of such an untrustworthy participant.”

Jane Street was banned from the Indian securities market. It deposited over $560 million into an escrow account and immediately appealed. As of today, the case remains pending before the Securities Appellate Tribunal in India.

Now let’s talk about Bitcoin.

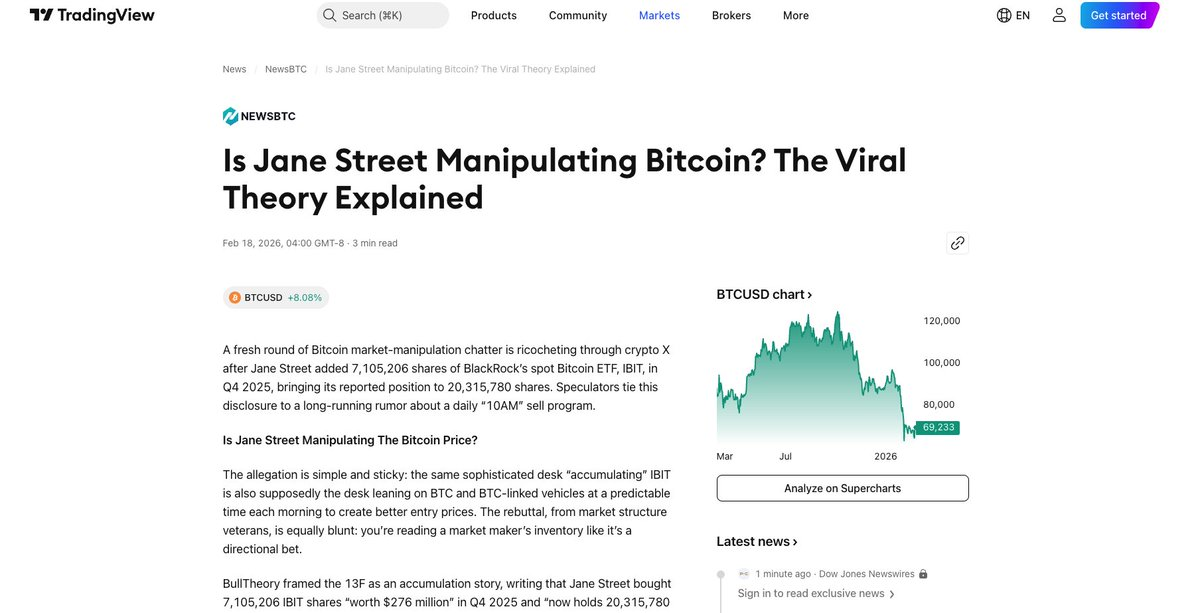

Since November 2025, Bitcoin traders have noticed a bizarre pattern: every morning around 10 a.m. ET—precisely when U.S. equities open—massive sell pressure hits BTC and related ETF shares.

The consistency is unnerving. Bitcoin rises during Asian and European trading hours—only to be suppressed the moment New York opens.

(See: https://www.tradingview.com/news/newsbtc:f65a83ede094b:0-is-jane-street-manipulating-bitcoin-the-viral-theory-explained/)

The numbers are staggering. A December 2025 chart shows BTC dropping from $89,700 to $87,700 within minutes on certain days—liquidating $171 million in leveraged long positions before recovering. This occurred on December 1, 5, 8, 10, 12, and 15—and recurred throughout January and February 2026.

Crypto Twitter dubbed it the “10-Point Strike.”

The finger points squarely at Jane Street—and for good reason. Jane Street is one of only four Authorized Participants (APs) for iShares Bitcoin Trust (IBIT)—the world’s largest spot Bitcoin ETF. The others are Virtu Americas, J.P. Morgan Securities, and Marex. As an AP, Jane Street holds the unique ability to create and redeem ETF shares—meaning it sits directly atop the pipeline through which Bitcoin flows into and out of institutional wrappers.

Its 13F filings confirm massive holdings: Jane Street held $5.7 billion in IBIT shares as of Q3 2025. In Q4, it added another $276 million—bringing its total position to over 20 million shares, worth ~$790 million at year-end prices. At its peak, it held nearly $2.5 billion in IBIT.

But something raises suspicion: While allegedly selling spot BTC every morning to suppress price, Jane Street increased its MSTR (Strategy, formerly MicroStrategy) position by 473% in Q4 2025—buying 951,187 shares worth ~$121 million. This occurred precisely as major funds like BlackRock and Vanguard were slashing billions of dollars in MSTR exposure.

Think about what that implies: Sell BTC at open to suppress price, liquidate leveraged longs, then buy back cheaply—while simultaneously loading up on the market’s most leveraged Bitcoin proxy, poised to benefit from the inevitable price rebound.

Jan Happel and Yann Allemann, co-founders of Glassnode, reignited this theory via their Negentropic account on X, linking algorithmic trading patterns to the filing of the Terraform lawsuit. Milk Road amplified the narrative, citing “persistent whispers” about institutional trading desks executing “very specific and conspiratorially detailed operating manuals.”

Then the lawsuit arrived. And then—something unexpected happened.

After the Terraform lawsuit against Jane Street was filed, the “10-Point Strike”… didn’t happen. For the first time in months, Bitcoin rose—not fell—at the U.S. market open.

Today, February 25, 2026, Bitcoin surged over 3%, broke multiple resistance levels, and traded above $68,000—just days after threatening to fall below $60,000. $323 million in short positions were liquidated. Random RSI hit 100. ETF net inflows reached $257.7 million—highest since early February.

https://x.com/peruvian_bull/status/2026730420168192432?s=20

The pattern has broken.

I want to tread carefully here. Correlation does not equal causation. Multiple forces are at play: Trump’s State of the Union address, oversold technicals, short covering. The Fear & Greed Index stood at 11—deep in the “Extreme Fear” zone, often a contrarian reversal signal. RSI had plunged to 15.80—the lowest reading since the 2020 pandemic crash, which preceded a 1400% rally. But the timing is hard to ignore.

Rumors are circulating on X that Jane Street “was forced to shut down its trading algorithms” following the lawsuit. Jane Street told Cointelegraph these are “baseless speculative allegations.” Whether it was forced to halt or voluntarily paused out of legal prudence, the outcome is identical:

Sell pressure disappeared.

What this truly means for Bitcoin.

Bitcoin spot ETFs were meant to be great equalizers: institutional access, regulated products, BlackRock’s stamp of approval. And they’ve indeed been hugely successful—IBIT alone has drawn over $20 billion in inflows since launch.

But the ETF structure introduced exactly what Bitcoin was designed to avoid: trusted intermediaries with privileged access to the plumbing.

When the U.S. Securities and Exchange Commission approved Bitcoin spot ETFs in January 2024, it mandated pure cash creation and redemption. Every time shares are created or redeemed, someone must actually buy or sell Bitcoin. And the firms plugged into that process—the Authorized Participants—hold structural advantages over every other market participant.

In September 2025, the SEC approved IBIT’s physical creation and redemption mechanism—meaning APs can now swap Bitcoin directly for ETF shares, bypassing fiat entirely. This grants Jane Street, Virtu, J.P. Morgan, and Marex even more direct control over Bitcoin’s inflows and outflows into the largest institutional wrapper.

The “10-Point Strike” is, at its core, the same pathology that has plagued gold markets for decades.

I wrote about this in “The Gold Endgame Begins”: paper-on-paper trading, where institutions with the most privileged pipeline access move prices before the rest of the market can react.

https://x.com/peruvian_bull/status/1778146092279861279?s=20

Gregg Smith and Michael Nowak, J.P. Morgan traders, were convicted of fraudulent order placement in precious metals futures—a scheme lasting eight years and involving thousands of illegal trades. J.P. Morgan paid $920 million to settle. Deutsche Bank paid $30 million for the same conduct. UBS, HSBC, and six individual traders face CFTC charges for anti-fraud violations.

Same script. Different asset.

Every time, these firms call it “market making,” “arbitrage,” “hedging.” Euphemisms abound—but the result is always the same: ordinary people get wiped out, while insiders capture the spread.

So where do we go from here?

The broader structural picture hasn’t changed. $4.5 billion in ETF net outflows over the first eight weeks of 2026 looks alarming—but Strategy (Saylor’s company) just bought $39 million in BTC, accounting for 99% of all corporate purchases during that period. Big players aren’t dumping—they’re waiting for the algorithms to finish their work.

And perhaps—right now—the algorithm has finished.

If Jane Street—whether due to legal exposure, regulatory scrutiny across multiple continents, or simple self-preservation—has indeed withdrawn from its alleged daily sell program, then a persistent, structural headwind suppressing Bitcoin for four months has been removed.

Bitcoin was born for this moment: a monetary system that doesn’t rely on trusted intermediaries, doesn’t need Authorized Participants, and cannot be front-run by messages passed from interns through secret channels to trading desks.

But don’t forget how we got here. The very firms entrusted to “make markets” and “provide liquidity” are the same ones accused of front-running collapses, manipulating national indices, and running algorithmic sell programs on the very assets their ETFs are supposed to track.

This is the system Bitcoin was designed to replace.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News