AI, Healthcare, VC… 10 Charts Capturing Global Change

TechFlow Selected TechFlow Selected

AI, Healthcare, VC… 10 Charts Capturing Global Change

84% of humans have never used AI, and only 0.3% pay for it.

Author: Rex Woodbury

Compiled by TechFlow

TechFlow Intro: Rex Woodbury of Daybreak Ventures outlines key trends for early 2026 through 10 charts.

Key Findings:

(1) Newspaper stocks crashed five years before earnings declined—SaaS stocks are now repeating this pattern;

(2) 84% of humanity has never used AI; only 0.3% pays for it;

(3) Time spent on AI applications is surging, competing with Netflix and TikTok for user attention;

(4) Healthcare accounts for 15% of U.S. employment and drives nearly 100% of employment growth;

(5) Secondary markets are now on par with IPOs and M&A as exit channels;

(6) Gen Z’s “financial nihilism”: first-time homebuyers now average age 40—better to gamble instead;

(7) Retatrutide (Eli Lilly’s new drug) could become a trillion-dollar peptide;

(8) The gaming market is $200 billion; Roblox’s user engagement exceeds Steam + PlayStation + Fortnite combined;

(9) 50% of Anthropic agent calls occur in software engineering;

(10) A Citrini research report triggered market panic selling—we live in a meme economy.

Full text below:

It’s that time again: time for another installment of the “10 Charts” series.

I aim to publish one each quarter—and we’re overdue: the last one was in October. This is our 11th edition (!), and you know the rules: I’m a visual learner, and charts help me process information. Charts also happen to be an effective way to illustrate how the world is changing.

We’ll cover 10 charts spanning a wide range of topics:

- Newspaper stocks vs. earnings

- Still Game One

- AI app usage time

- Healthcare-driven employment

- Secondary markets reshaping VC + employee returns

- Gen Z: the last generation in the alphabet

- Peptides and Reta

- The state of gaming

- Calling for more agent usage

- The Citrini sell-off

Without further ado…

Newspaper Stocks vs. Earnings

This chart compares newspaper stock prices with earnings. You can see that stocks plungedabout five years before earnings declined—meaning the market saw the writing on the wall before it appeared on the income statement.

Source: Twitter; thanks to Emily Man for sharing

Of course, there’s some timing lag—the decline in forward-looking earnings coincided with the Great Recession. But directionally, this appears accurate: the market anticipated internet disruption of newspapers. We’re seeing it again today—last month, SaaS stocks plunged ahead of AI disruption.

As we wrote last week, the “SaaSpocalypse” will take time to unfold. At a panel I attended this week, one participant quipped, “Campbell Soup Company won’t vibe-code their own CRM”—a clever turn of phrase. Yet the market is pricing in an eventual reality: compressed software margins, where the “new normal” is 70% gross margin—not 90%.

On the theme that AI adoption takes a long time to unfold…

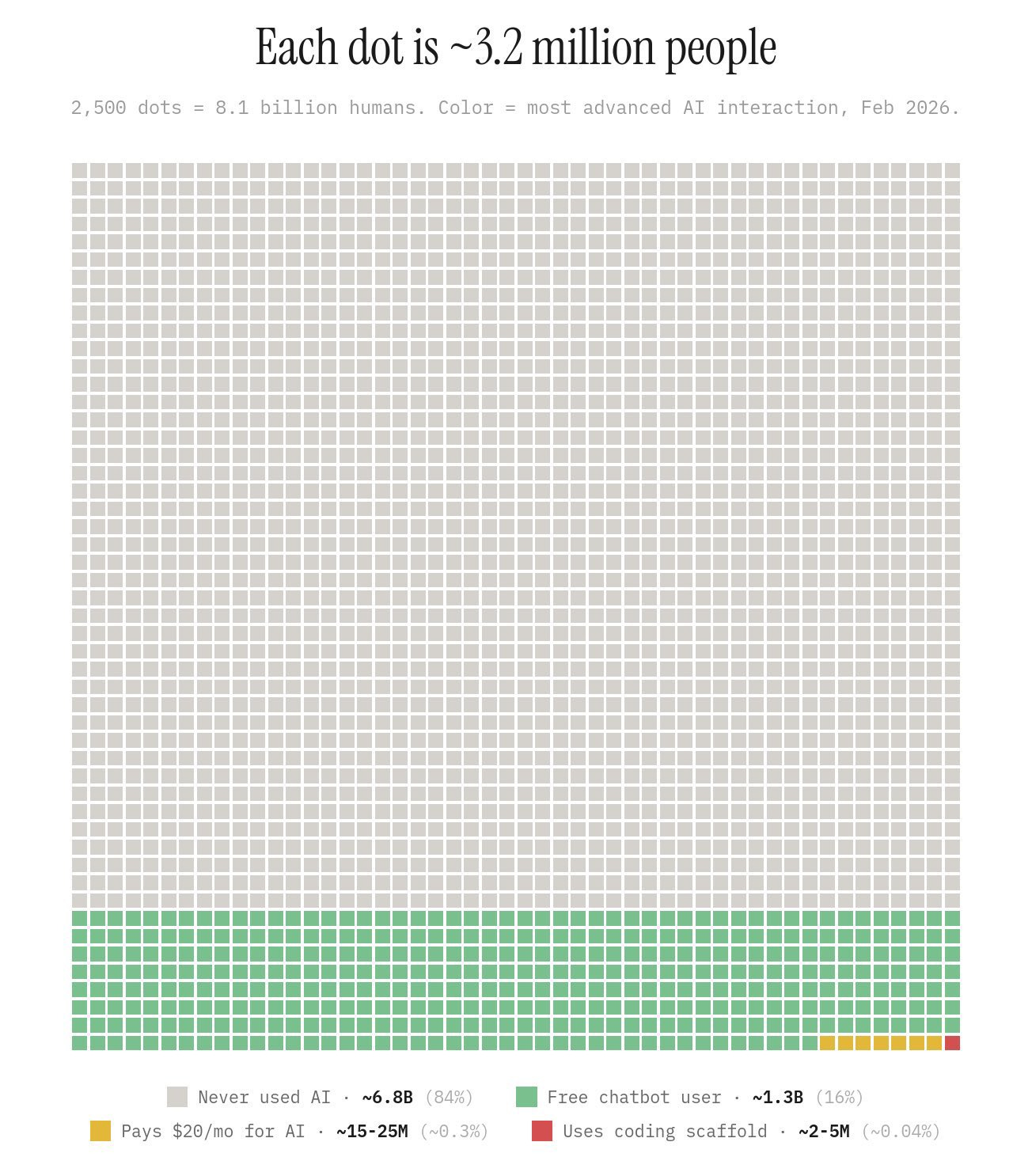

Still Game One

This is a cool visualization of where we are in the AI adoption cycle. Each dot below represents 3.2 million people. There are 2,500 dots total—8.1 billion people.

- Gray = 6.8 billion people who have never used AI

- Green = 1.3 billion free users

- Yellow = 15–35 million paying users

- Red = 2–5 million coders

Source: Noah Epstein on Twitter

Approximately 84% of the world has never used AI, and only 0.3% (!) pay for AI products. This is the best visualization I’ve seen of “we’re still very early.”

AI App Usage Time

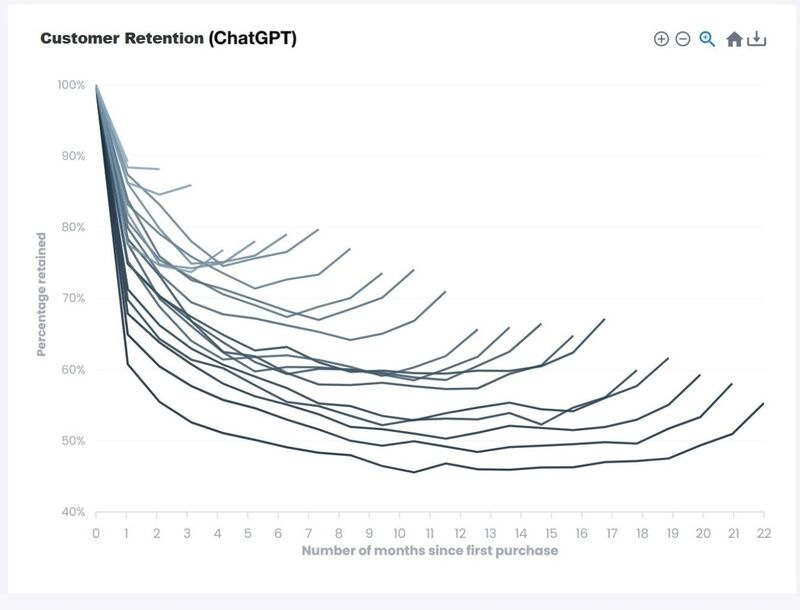

In the previous edition of “10 Charts”, we looked at ChatGPT’s “smile curve”:

From that article:

This chart commits what I call the “y-axis crime”—meaning the y-axis misleadingly does not start at zero. But in this case, the y-axis crime actually hurts ChatGPT! The curve looks even better once you realize the worst-performing cohort asymptotes in their mid-40s (and then “smiles”).

Such curves are typically reserved for markets or social products with network effects—i.e., they improve as more users join the platform (e.g., Uber improves with higher rider/driver density, or Instagram improves as more of your friends join the app). For a solo product without social features, achieving such retention is impressive.

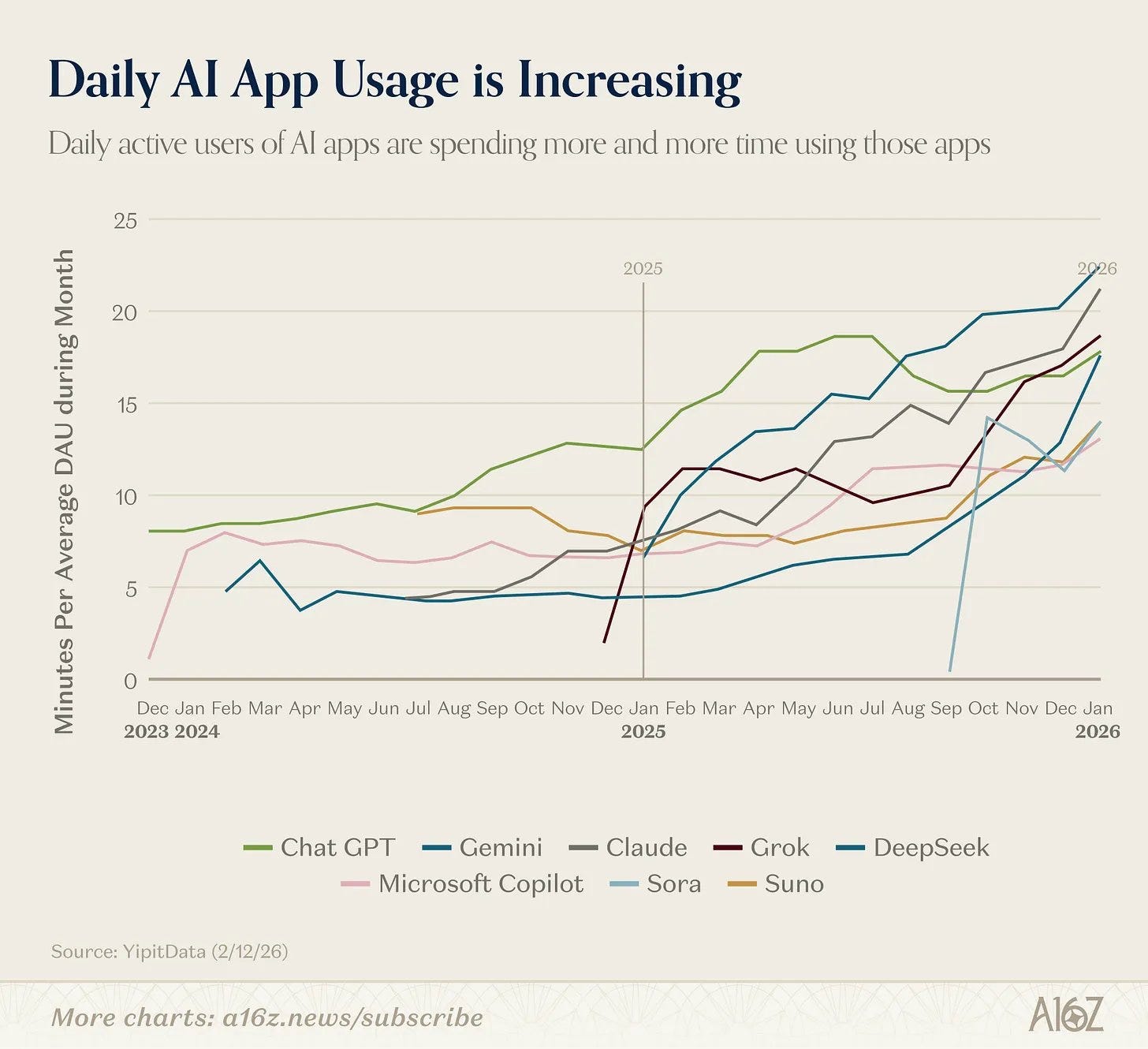

Beyond improved retention, AI apps are also seeing improved engagement. Here’s a visualization showing that trendline:

Overall, this represents a very impressive growth in usage volume.

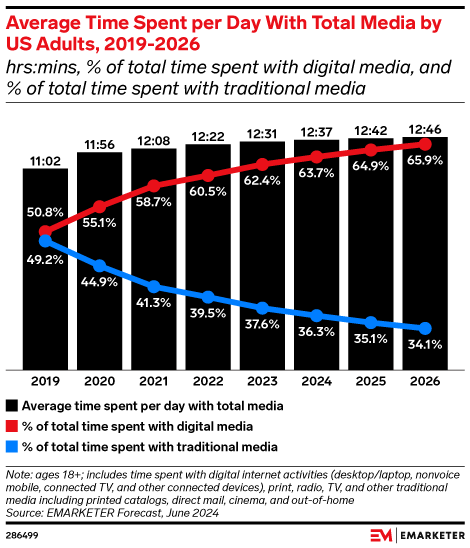

In 2017, Netflix’s Reed Hastings famously said Netflix’s biggest competitor is sleep. Netflix’s business model depends on absorbing more and more viewing time (more viewing time = better subscriber retention + willingness to pay), so naturally, sleep directly conflicts with its business model.

We’re now seeing media consumption plateau at roughly 12.75 hours per day:

The rise in AI usage must come at the expense of time spent elsewhere. Perhaps Claude’s biggest competitor is sleep? I also imagine Netflix, YouTube, TikTok, etc., are watching the AI usage chart above warily. Half an hour on Gemini is half an hour not spent watching short-form video. AI tools are clearly more than just Google replacements—they’re also social + content products. Just wait until generative media truly takes off; we’ll see large incumbent companies’ engagement metrics face immense pressure.

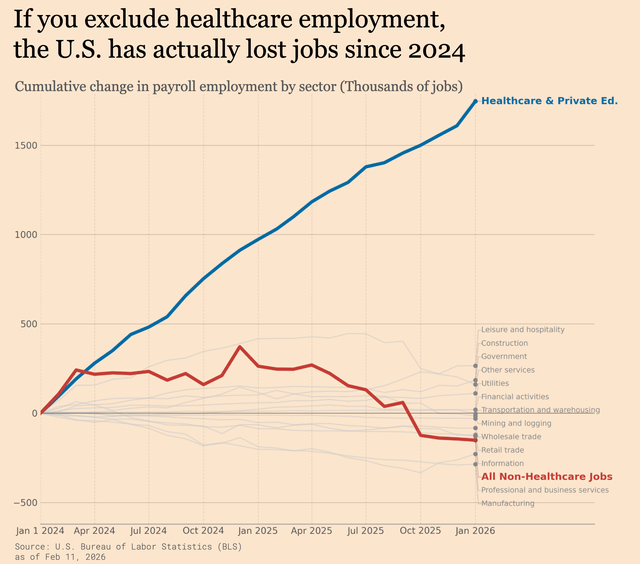

Healthcare-Driven Employment

Healthcare is the largest U.S. employment category, accounting for ~15% of jobs. It’s the engine behind nearly all employment growth. Consider this chart:

Overall, healthcare will drive ~40% of new jobs over the next decade. Meanwhile, the fastest-growing single job in the U.S. is “home health aide,” driven by rapid population aging (10,000 Americans turn 65 every day).

Healthcare benefits from several major tailwinds:

- LLMs are exceptionally well-suited to healthcare administration—a trillion-dollar market, since healthcare runs on language.

- Consumers are increasingly willing to measure, personalize, and spend on their health.

- Telehealth is expanding access to care, aided by new post-pandemic regulations broadening coverage.

- Our population is aging and becoming sicker—the “silver tsunami,” etc.

Many healthcare jobs are also “AI-proof,” which I believe means we’ll see more young people entering the field.

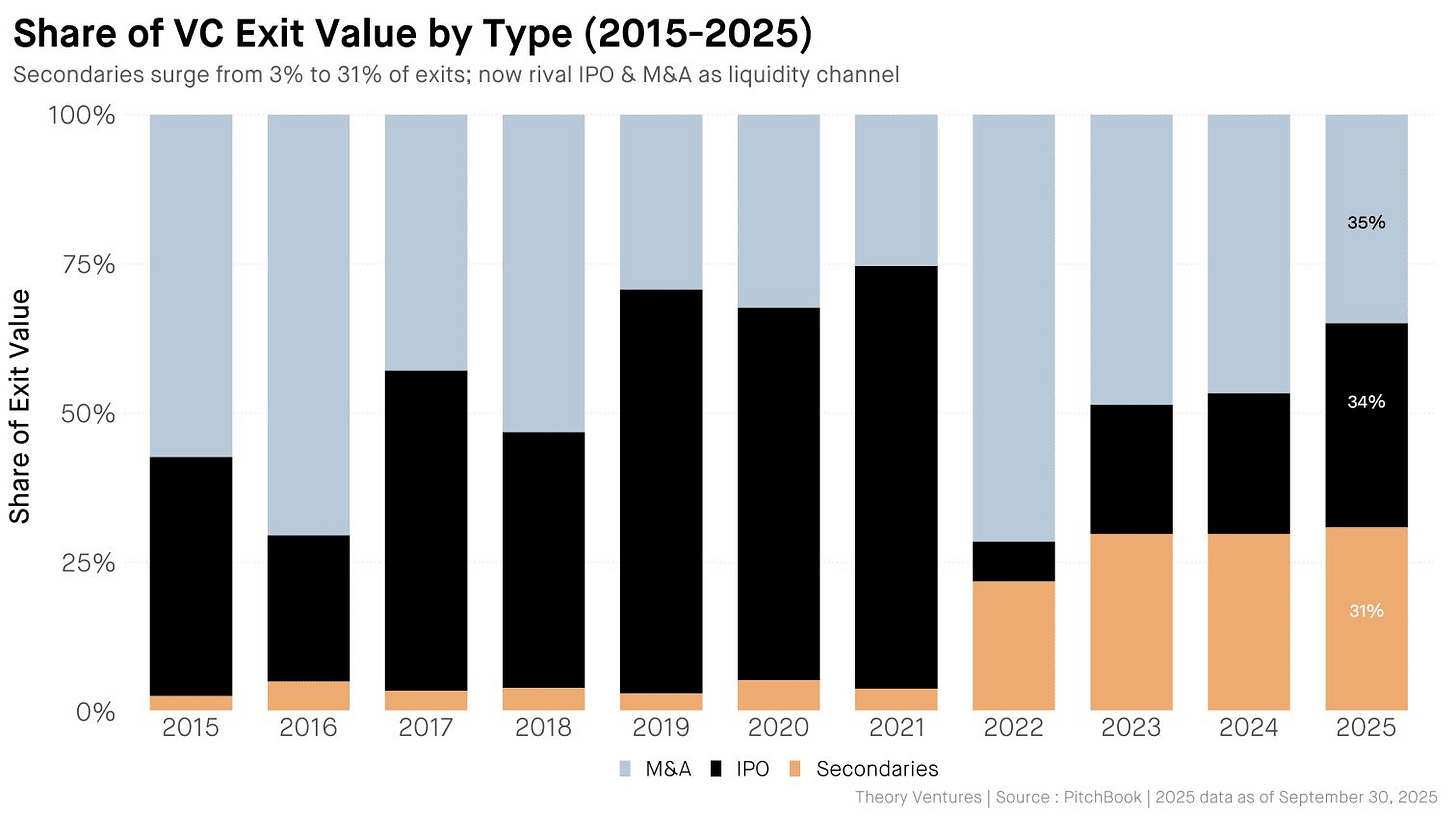

Secondary Markets Reshaping VC + Employee Returns

This is an underappreciated shift in venture capital. Secondary markets now rival IPOs and M&A as exit channels:

Source: Tomasz Tunguz on Twitter

This changes the game for early-stage funds like Daybreak—and for startup employees. Liquidity timelines are compressing. I wouldn’t be surprised if we return multiples to funds by selling shares during growth-stage financing rounds. This isn’t new—IA Ventures’ Roger Ehrenberg publicly discussed selling ~2.5 million of ~6.6 million shares of The Trade Desk in a secondary sale to return capital to LPs—but it’s becoming more common.

For employees, liquidity no longer requires waiting over a decade. Clay and ElevenLabs each completed two tender offers within the past 12 months, while Anthropic is currently conducting a $6 billion (!) tender offer. The latter will undoubtedly send shockwaves through the San Francisco real estate market.

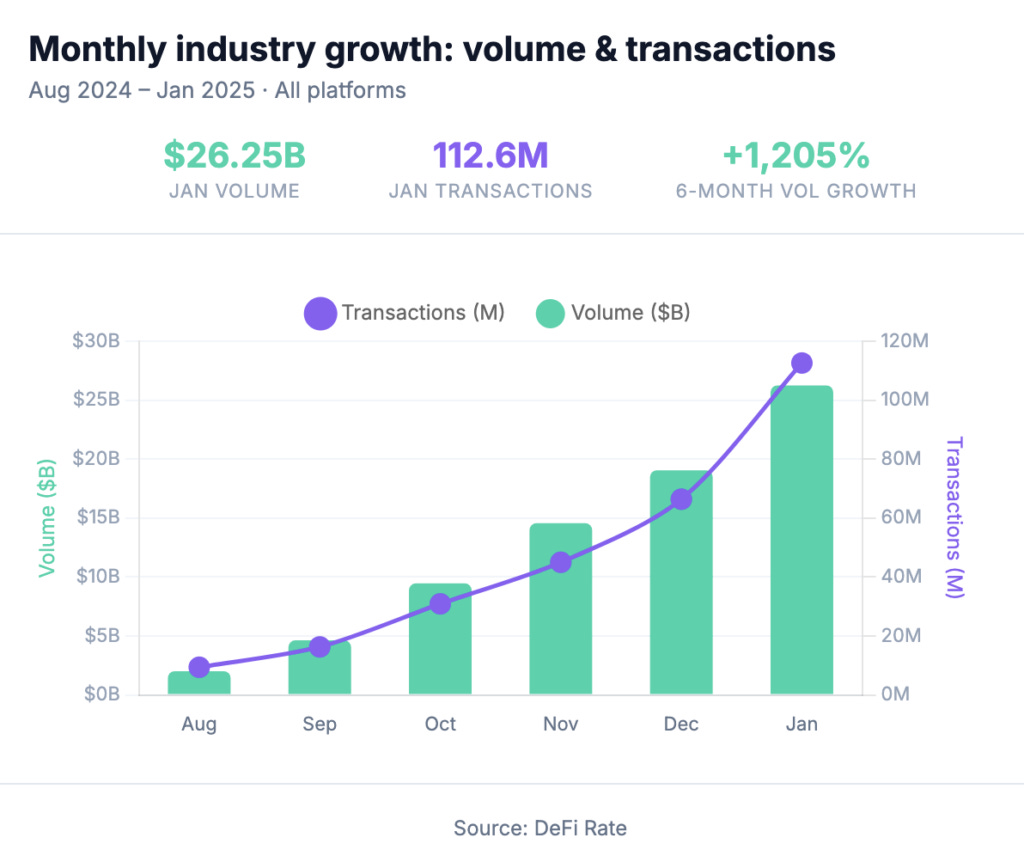

Gen Z: The Last Generation in the Alphabet

Kalshi reported over $1 billion in Super Bowl Sunday betting volume, up 2700% (!) year-over-year. Here’s a chart showing prediction market trading volume before the Super Bowl, with a 1205% increase over six months:

These markets are new—and controversial. White House Press Secretary Karoline Leavitt abruptly ended a briefing in early January amid insider trading concerns:

During the Super Bowl, my partner placed a small bet on Cardi B performing with Bad Bunny after she appeared onstage. He lost—the bet, because Kalshi defined “performance” as requiring singing. That led at least one person to file a complaint with the CFTC. It’s the Wild West!

Yet despite controversy, I believe prediction markets are here to stay. Last fall, we wrote about the forces driving the rise of prediction markets in Speculation Nation. That piece focused on enabling technologies colliding with Gen Z behavior—including the rise of FAFOnomics (FAFO = Fuck Around and Find Out).

My friend Jackson Denka wrote an interesting piece this week titled “Financial Nihilism, or: How I Learned to Stop Worrying and Love the Market”. He calls Gen Z “the last generation in the alphabet,” which struck me. Some stats he cites:

- Unemployment among 2025 U.S. college graduates stands at 9.3%, higher than during the Global Financial Crisis

- The top 1% of households owns nearly 30% of national wealth

- The average age of first-time homebuyers is now 40

No wonder we’re becoming a speculative economy? If upward economic mobility feels Sisyphean, why not bet everything for a shot at getting rich? Note: This isn’t good—but I think it’s one of the defining undercurrents of the next generation.

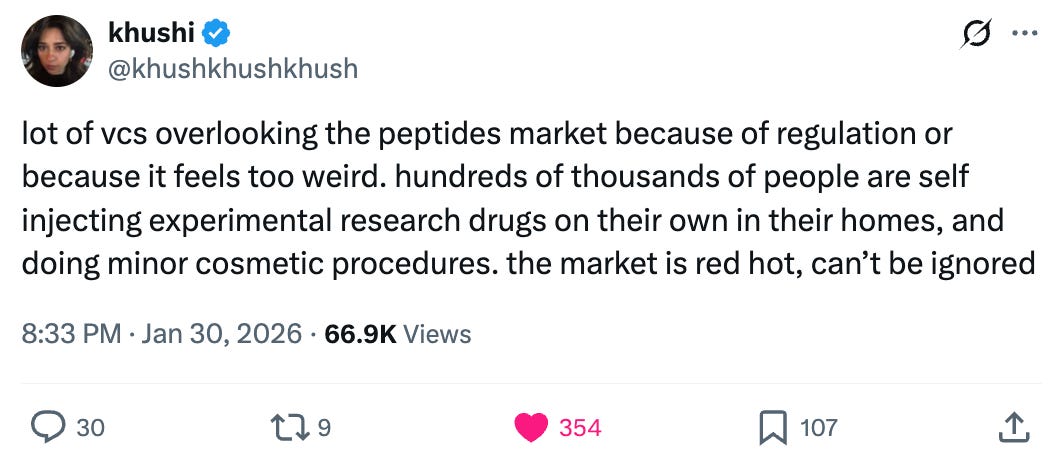

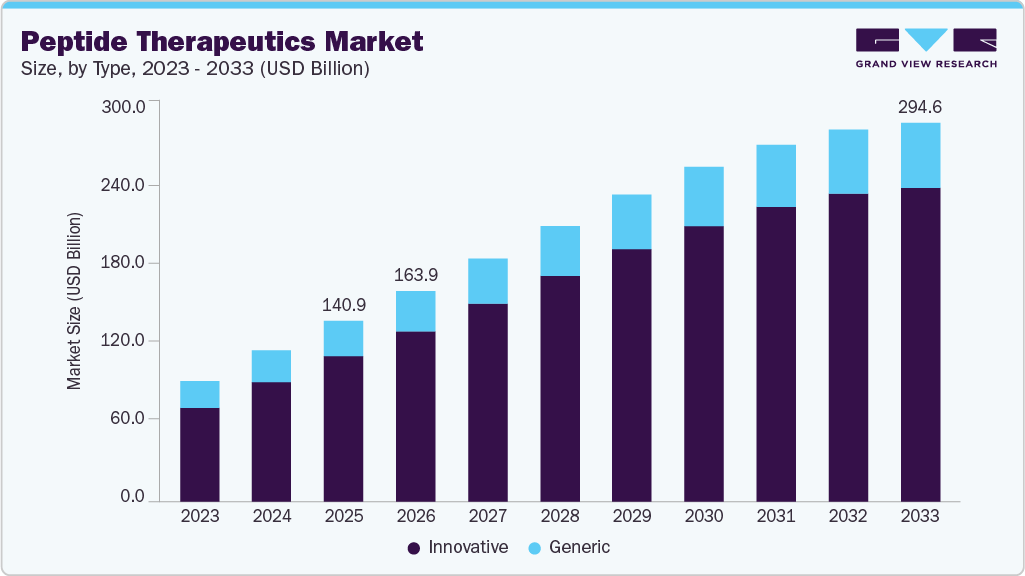

Peptides and Reta

Amid the AI noise, it’s easy to overlook other seismic shifts. One area I’ve spent significant time on: peptides—which are beginning to gain mainstream attention.

Peptides are chains of amino acids that act as signaling molecules in your body. The most famous peptides are Ozempic and Wegovy—the brand names for the peptide semaglutide. The peptide market is booming, as consumers demonstrate genuine interest and willingness to pay. My friend Khushi captured this well in this tweet:

Our first investment of 2026 is a peptide company, System Labs, which launched last week. There’s a big opportunity to demystify peptides for everyday consumers and become a trusted, U.S.-based, safe source for peptides.

You can see market expectations for growth here:

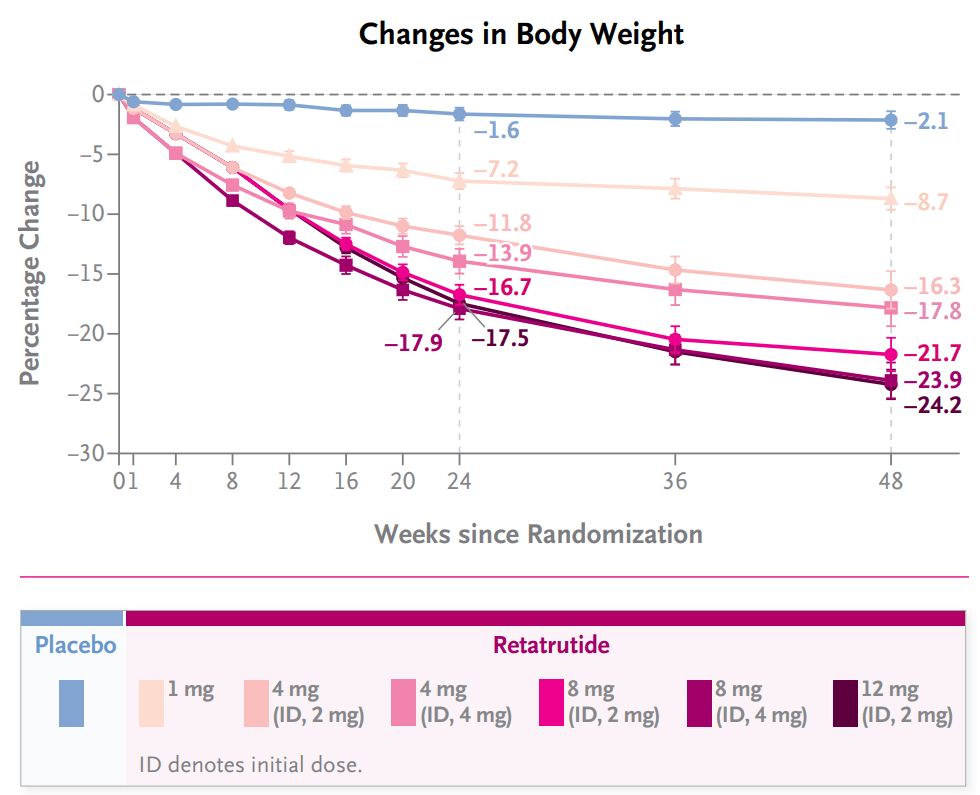

The most underestimated drug right now is Retatrutide, or Reta. Eli Lilly’s Reta is a triple agonist, whereas Ozempic is a single agonist—a fancy way of saying Reta targets three receptors: GLP-1, GIP, and glucagon. This means the drug enhances satiety, improves insulin sensitivity, and boosts metabolic rate (fat burning). Ozempic targets only GLP-1, focusing primarily on appetite suppression.

Reta is a potential trillion-dollar drug. Here’s a chart showing Reta’s weight-loss results:

Source: CTCD

Expect to hear much more about Reta soon.

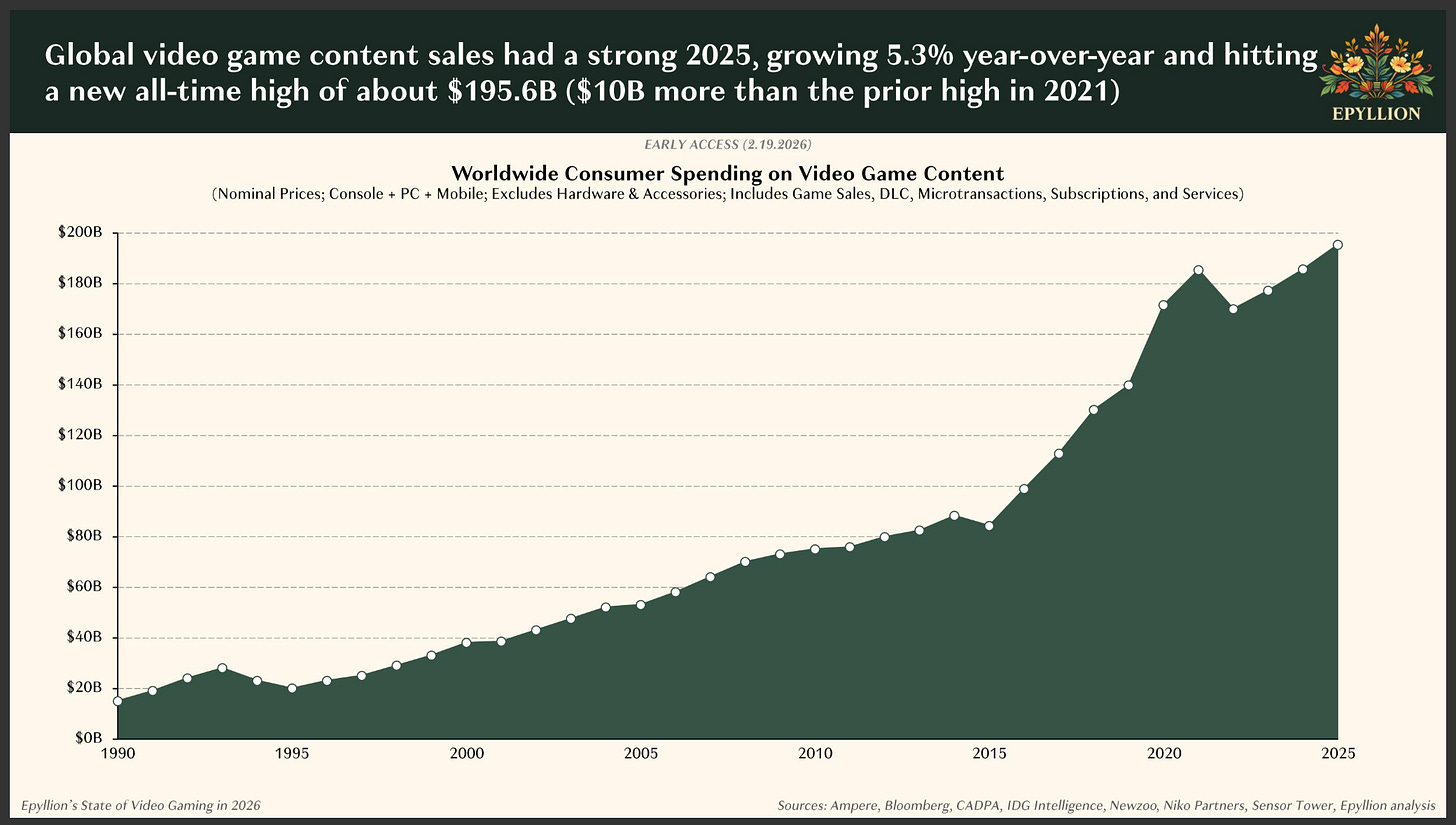

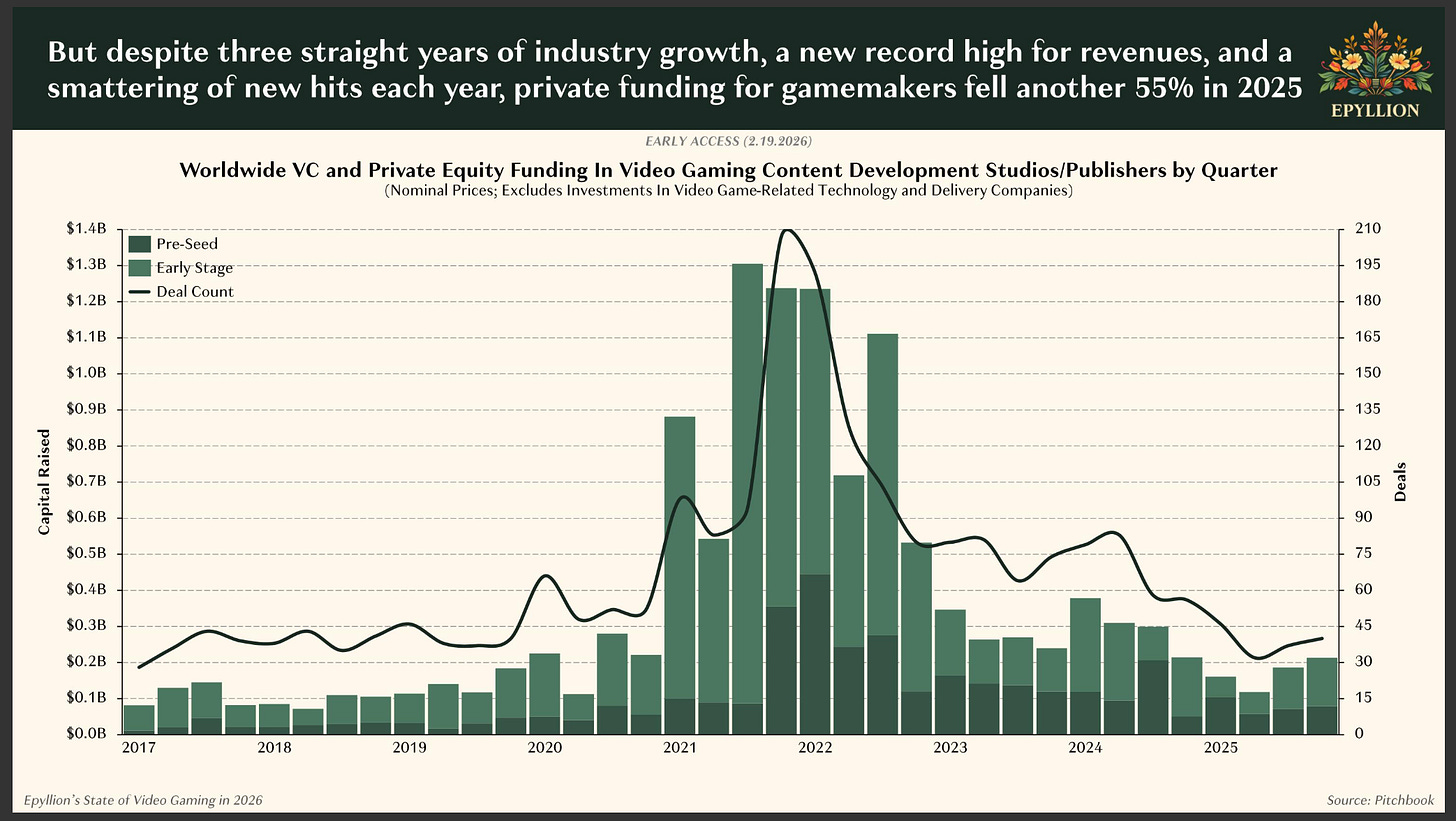

The State of Gaming

Last week, Matthew Ball released a comprehensive report on the state of gaming. Highlights include:

Gaming remains the largest media category, with annual spending at $200 billion—greater than film + TV + music combined. After a brief post-pandemic dip, growth has resumed:

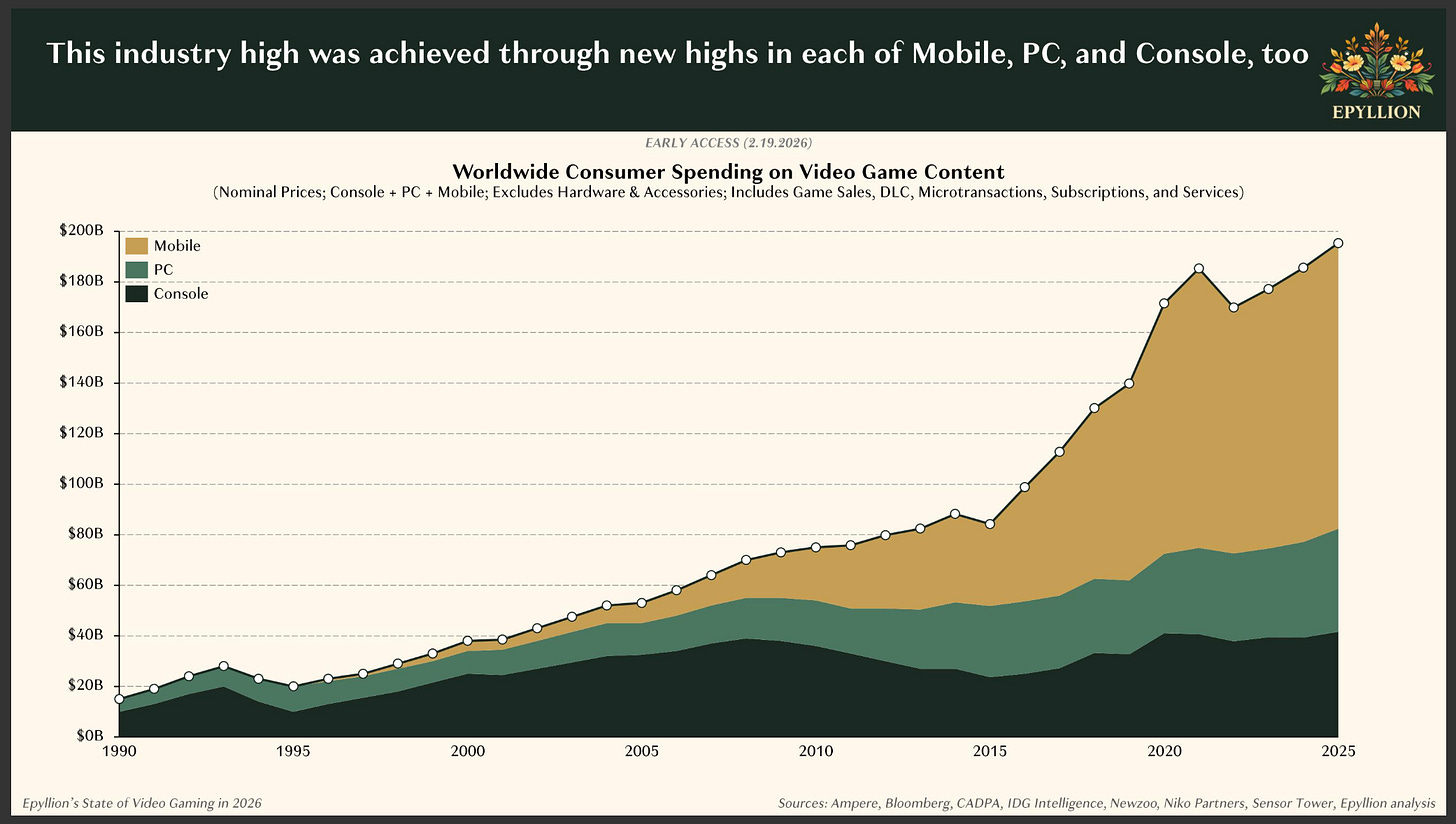

Mobile is driving most of gaming’s growth:

Despite market growth, venture capital funding has declined sharply from pandemic-era highs:

AI will reshape gaming—though this hasn’t meaningfully happened yet (we’re still mostly in AI’s text phase). Soon, game generation—not rendering—will become standard, unlocking new possibilities for narrative + world-building.

Returning to our earlier point about AI apps competing with sleep and Netflix: we may also see AI apps encroaching on gaming time. This tweet resonated with me:

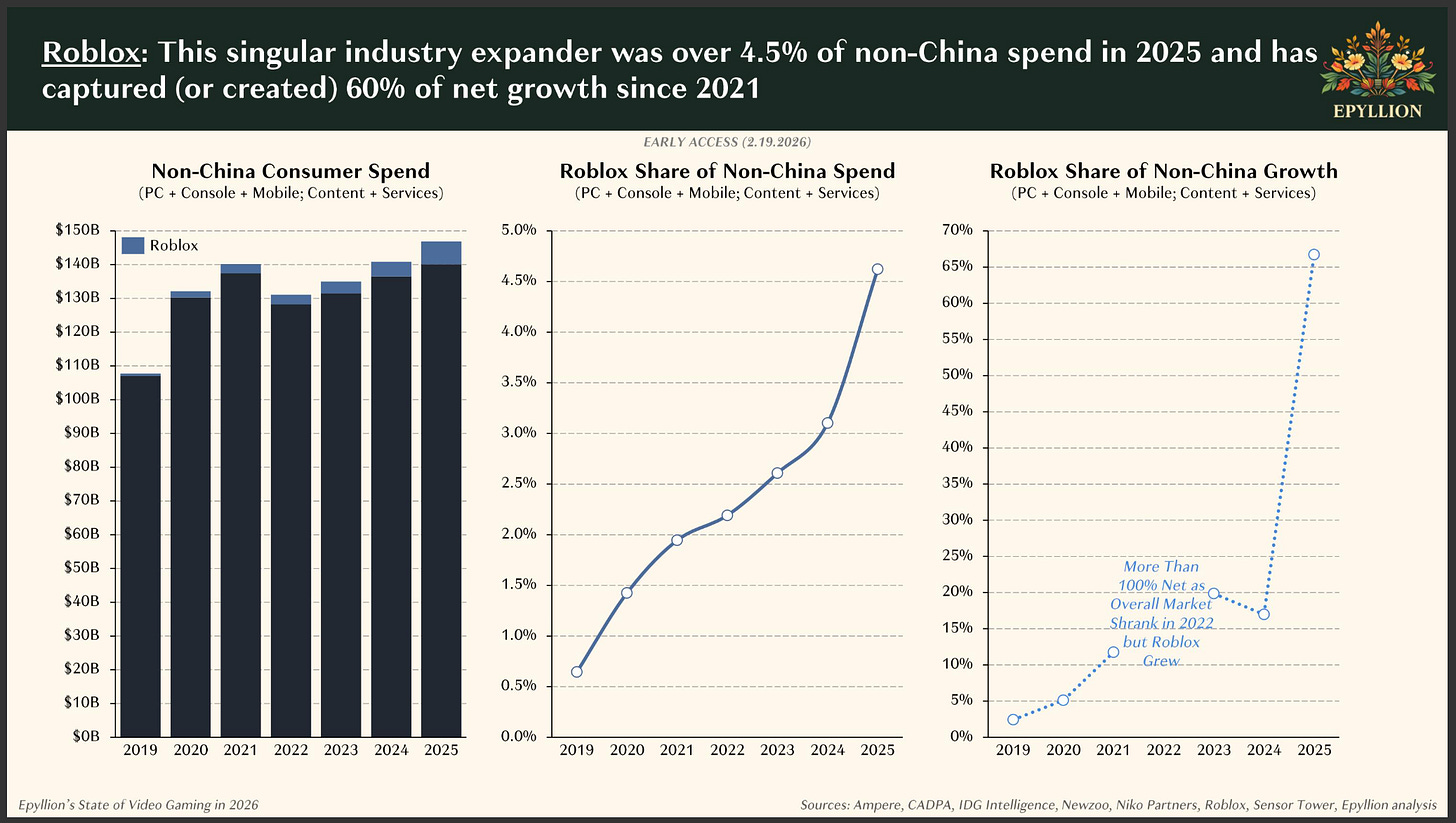

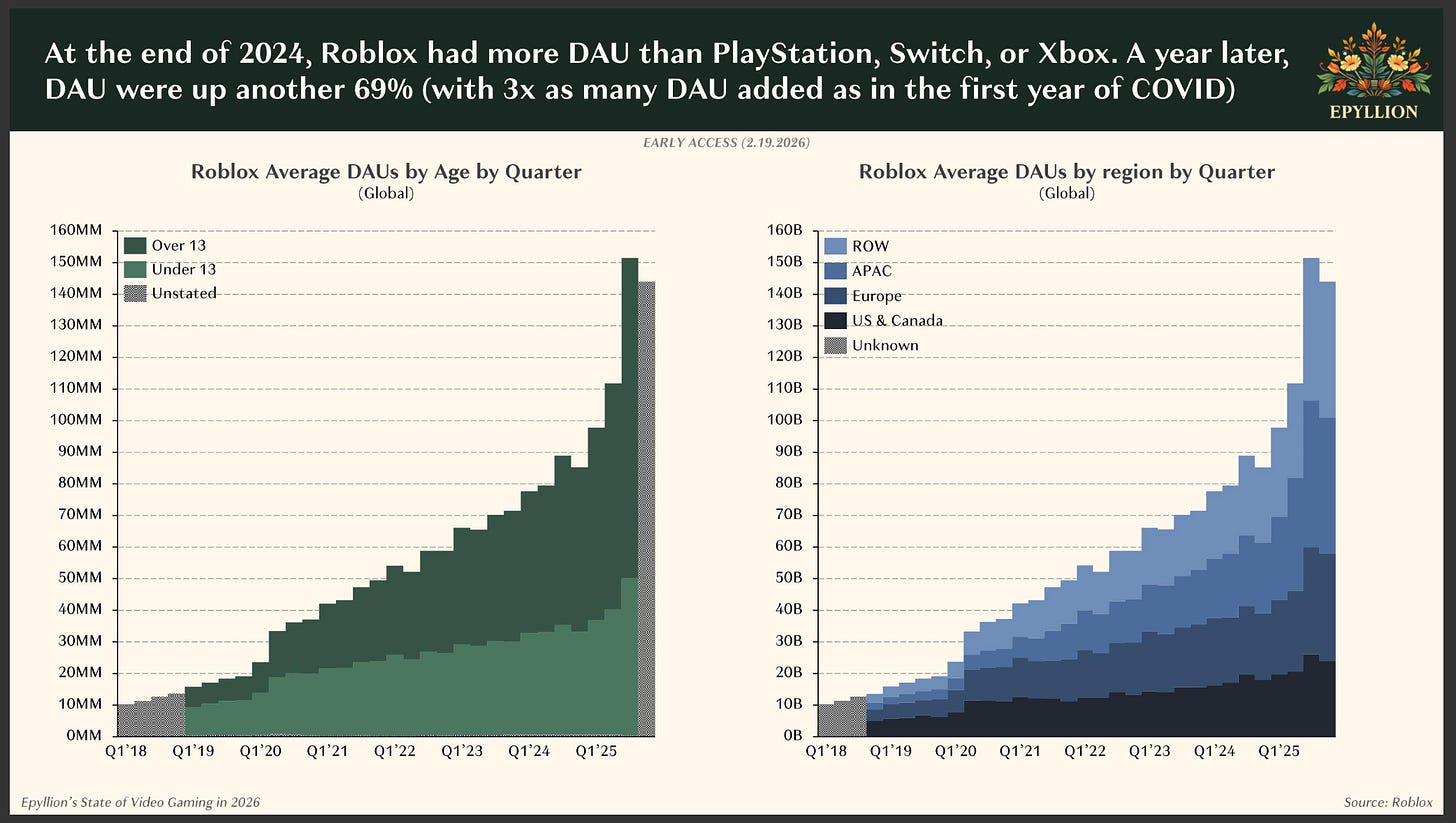

The most impressive gaming company remains Roblox, which drives a large share of gaming growth:

Roblox now boasts 150 million daily active users—and you can see the proportion of users aged 13+ growing especially fast:

Roblox’s average engagement now exceeds the combined total of Steam + PlayStation + Fortnite.

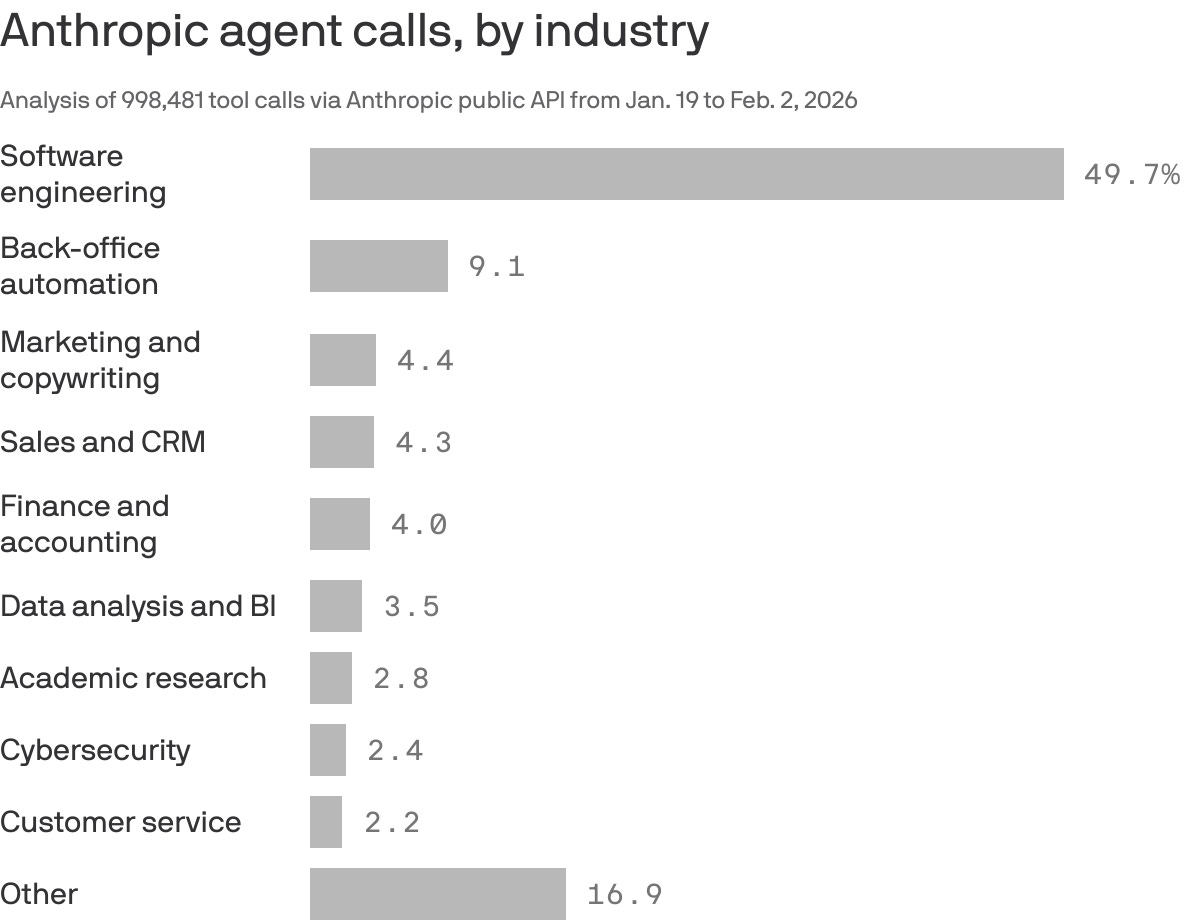

Calling for More Agent Usage

This is an interesting chart showing Anthropic agent usage across industries:

Clearly, there’s massive opportunity for agents beyond software engineering. Or as Garry Tan put it:

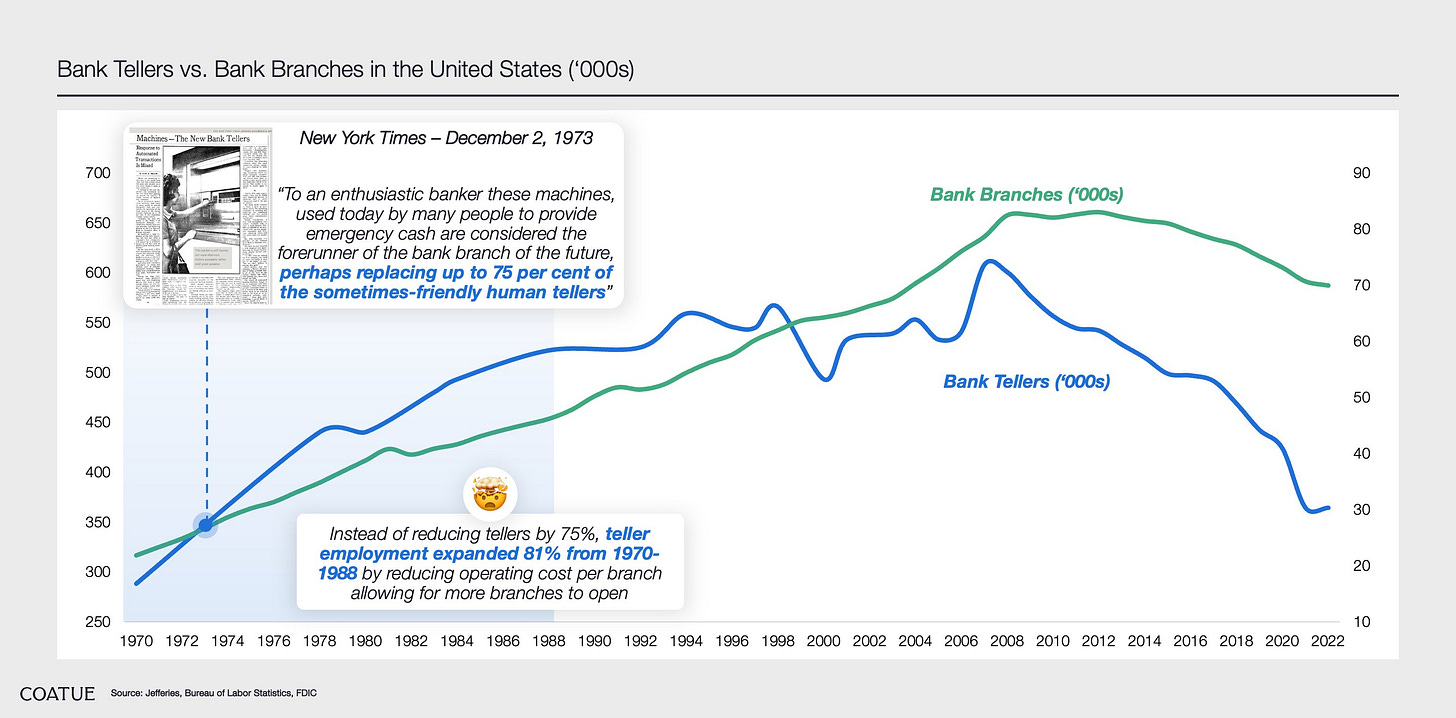

As for what happens to jobs in these categories: I expect labor displacement to unfold more slowly. We’ve written extensively here about Jevons’ paradox. Another example: Coatue’s excellent visualization of ATMs:

People assumed ATMs would destroy bank teller jobs. Instead, from 1970 to 1988, the number of bank tellers increased by 81%, enjoying four decades of steady growth.

The Citrini Sell-Off

Another week, another viral blog post. This week’s is a Substack article from Citrini, which triggered a market sell-off:

What’s wild to me is that a casual, future-oriented article—with no factual or data foundation—could spark such widespread market panic. To me, this signals (1) an overheated market seeking justification for a correction, and (2) our formal entry into a meme economy.

I find the article quite naive. Fintech and market infrastructure companies are harder to disrupt than the Citrini article suggests. DoorDash’s Tony Xu offered a strong rebuttal.

The real takeaway from the Citrini sell-off: nobody knows exactly what will happen.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News