Triple pressures on the crypto market: ETF outflows, leverage reset, and low liquidity

TechFlow Selected TechFlow Selected

Triple pressures on the crypto market: ETF outflows, leverage reset, and low liquidity

The spot liquidity of major cryptocurrencies and altcoins has not yet recovered, leaving the market in a fragile state and more susceptible to extreme price volatility.

Author: Tanay Ved

Translation: Luffy, Foresight News

TL;DR

-

Major capital absorption channels such as ETFs and DATs have recently seen weak demand, with the deleveraging process in October and a macro risk-averse backdrop continuing to pressure the crypto market.

-

Futures and DeFi lending markets have completed a full leverage reset, resulting in cleaner position structures and reduced systemic risks.

-

Spot liquidity for major and alt coins has not yet recovered, leaving the market in a fragile state more susceptible to extreme price volatility.

In early Uptober, Bitcoin surged to a new all-time high, but optimism quickly reversed as the flash crash on "10.11" severely damaged market confidence (Note: Uptober refers to the typical upward trend in cryptocurrency markets during October). Since then, Bitcoin's price has dropped by approximately $40,000 (over 33%), with altcoins suffering even greater losses, bringing the total market capitalization of the entire cryptocurrency market back to nearly $3 trillion. Despite multiple positive fundamental developments throughout 2025, price movements and market sentiment remain significantly divergent.

Currently, digital assets are at an intersection of multiple external and internal factors. On the macro front, uncertainty around December rate cut expectations and recent weakness in tech stocks have further intensified market risk aversion. Within the crypto market, previously stable funding channels such as ETFs and Digital Asset Treasuries (DATs) have experienced capital outflows. Meanwhile, the liquidation wave on "10.11" triggered one of the most intense deleveraging events in history, whose aftereffects continue to linger, with market liquidity remaining subdued.

This article will deeply analyze the core drivers behind the recent weakening of the digital asset market, focusing on ETF fund flows, leverage conditions in perpetual futures and DeFi markets, and order book liquidity, to explore what these changes reveal about the current market landscape.

Macro Shift Toward Risk Aversion

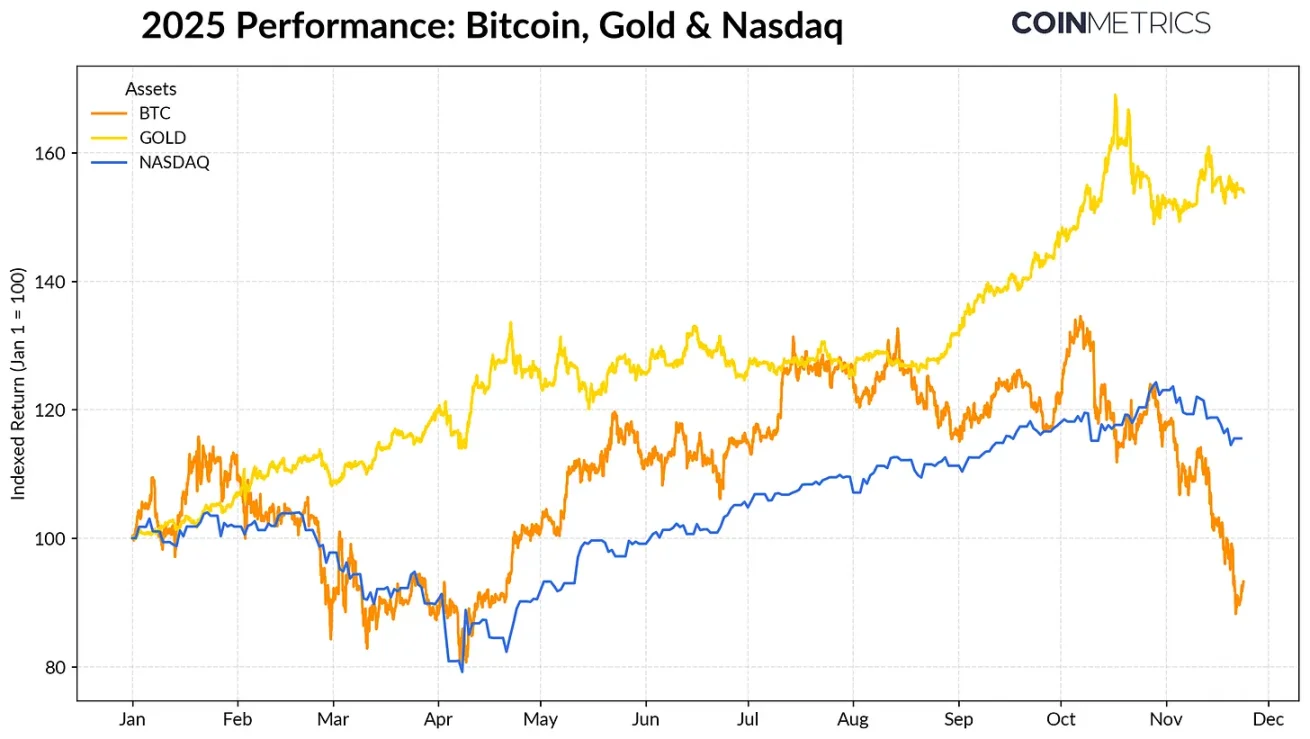

Bitcoin’s performance has increasingly diverged from major asset classes. Against the backdrop of central banks' record gold purchases and ongoing trade tensions, gold has delivered over 50% returns this year, surging steadily. Meanwhile, tech stocks (Nasdaq Index) lost momentum in Q4 as markets reassess the likelihood of upcoming Fed rate cuts and the sustainability of the AI-driven bull run.

As our previous research has shown, Bitcoin’s relationship with “risk-on” tech stocks and “safe-haven” gold fluctuates cyclically, adjusting according to shifts in the macro environment. This makes Bitcoin particularly sensitive to market shocks or catalytic events—such as the October flash crash and the recent risk-off sentiment.

Performance of Bitcoin, Gold, and Nasdaq Index in 2025, Data source: Coin Metrics and Google Finance

As the "anchor asset" for the entire cryptocurrency market, Bitcoin’s correction has spilled over into other assets. Although niche sectors like privacy coins briefly outperformed, most cryptocurrencies still maintain a high degree of correlation with Bitcoin.

Weakening Capital Absorption Capacity of ETFs and DATs

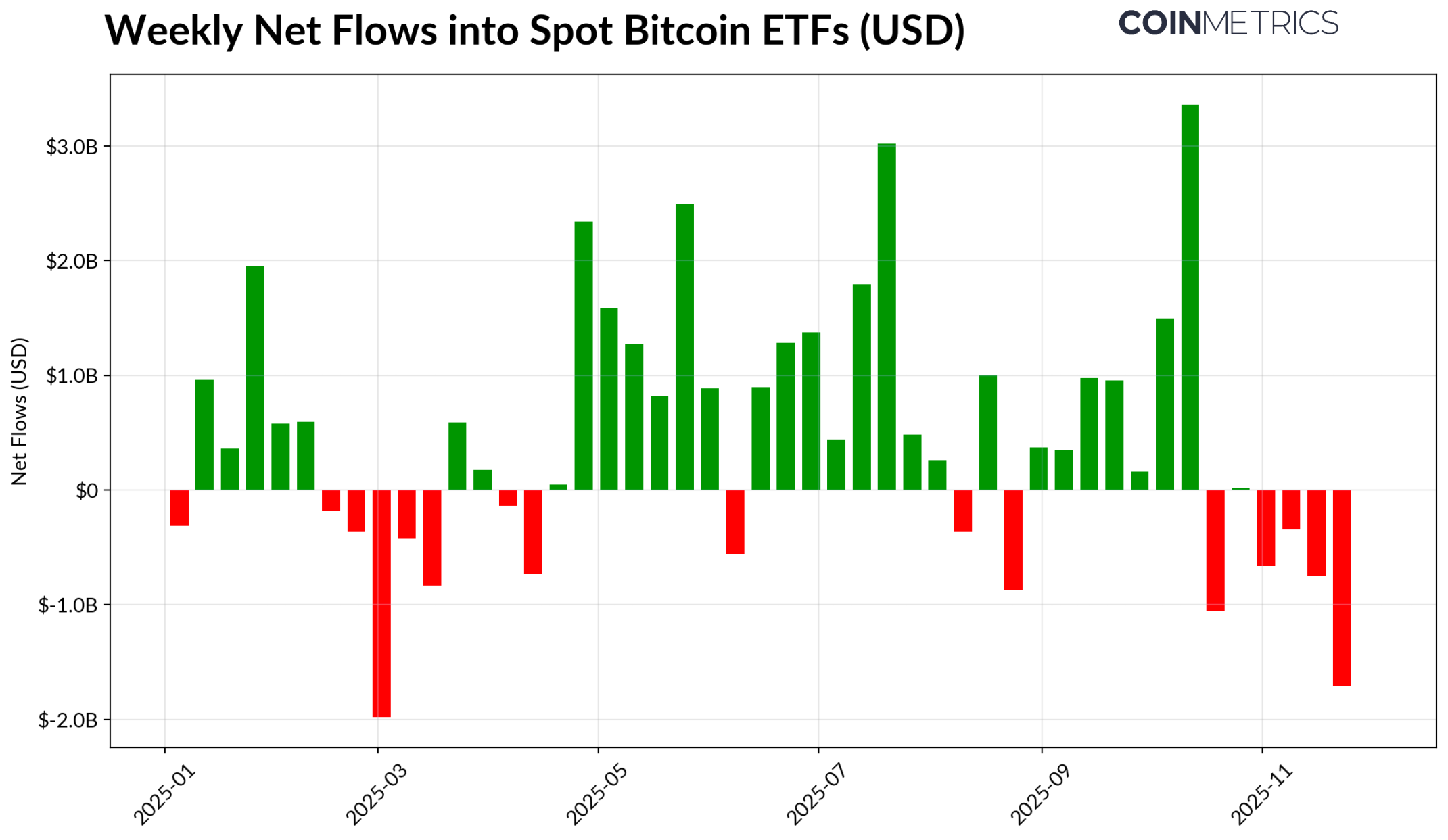

Bitcoin’s recent weakness partly stems from declining demand in core funding channels that supported its 2024–2025 rally. Since mid-October, ETFs have recorded net outflows for several consecutive weeks, accumulating $4.9 billion in outflows—the largest redemption wave since April 2025, when Bitcoin fell to $75,000 ahead of the “Liberation Day” tariff announcement.Despite short-term outflows, on-chain holdings continue to rise, with BlackRock’s IBIT ETF alone holding 780,000 BTC—approximately 60% of the current total holdings across spot Bitcoin ETFs.

If ETF inflows resume, it would signal stabilization in this channel. Historical data shows that during periods of renewed risk appetite, ETF demand was a key force absorbing Bitcoin supply.

Weekly Net Inflows into Bitcoin ETFs, Data source: Coin Metrics

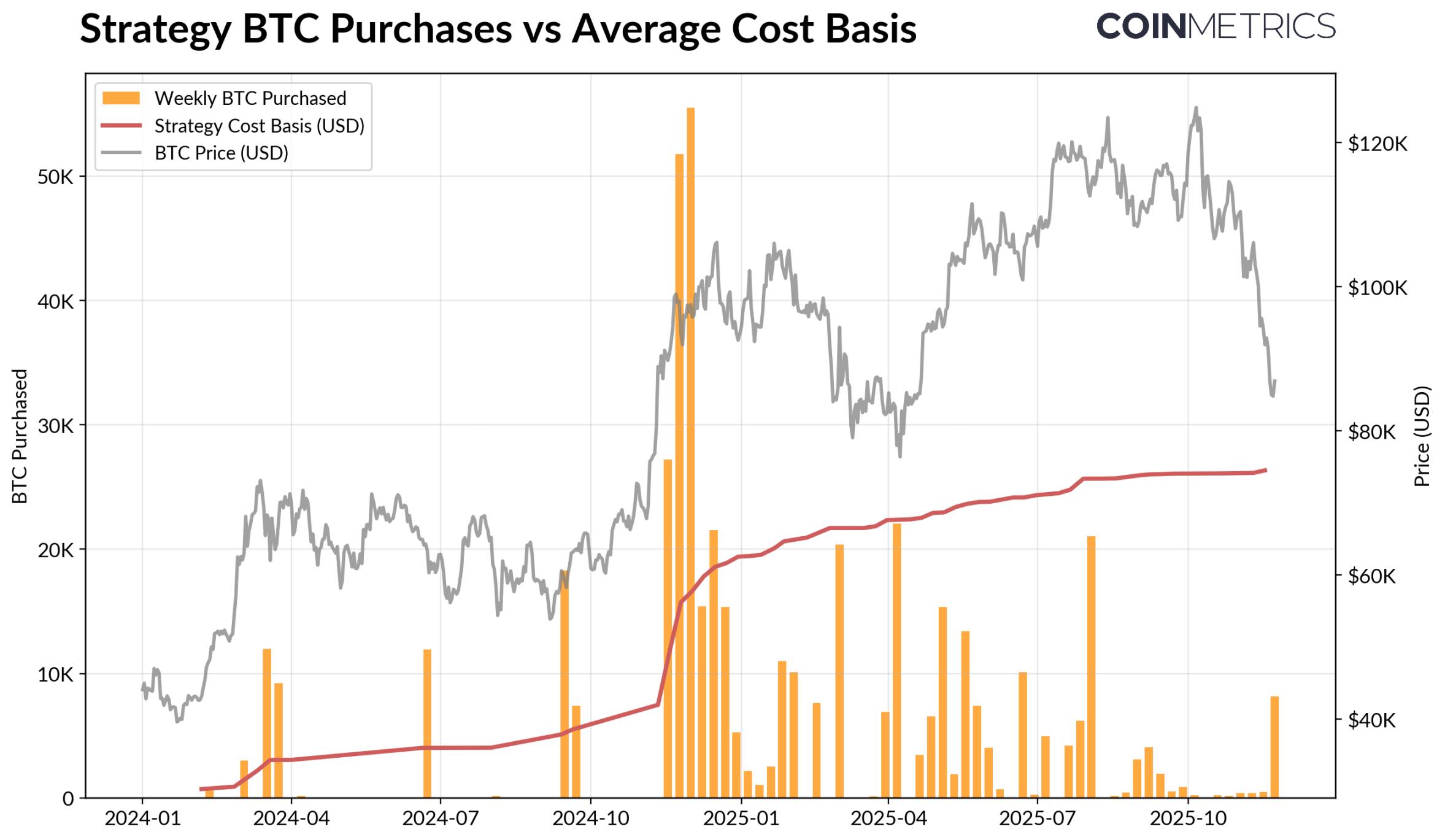

Digital Asset Treasuries (DATs) are also beginning to show signs of stress. As prices correct, the stock valuations and crypto holdings of DAT companies shrink, pressuring the net asset value premium that supports their growth flywheel. This weakens their ability to raise new capital through equity issuance or debt financing, thereby limiting growth in per-share crypto exposure. Smaller, emerging DATs are especially vulnerable, as changing market conditions may render cost bases and equity valuations unsuitable for further accumulation.

The largest DAT currently—Strategy—holds 649,870 BTC at an average cost of $74,333 (approximately 3.2% of Bitcoin’s current total supply). As shown in the chart below, Strategy accelerates its accumulation pace significantly when Bitcoin prices rise and equity valuations strengthen, while its buying pace has slowed recently. Nonetheless, Strategy remains in an unrealized profit position, with its cost basis below current market prices.

If prices fall further or if index delisting risks emerge, Strategy could face pressure. However, improved market conditions could enhance its balance sheet and valuation, recreating an environment conducive to DAT accumulation.

Strategy’s Bitcoin Purchases and Average Cost Basis, Data source: Strategy and Bitbo Treasuries

This trend aligns with on-chain profitability metrics. The spent output profit ratio (SOPR) for short-term holders (holding < 155 days) has fallen into a loss zone of approximately -23%, a level historically associated with capitulatory selling pressure from the most price-sensitive cohort. Long-term holders remain profitable on average, though SOPR data indicates slightly increased profit-taking. A recovery in short-term holder SOPR above 1.0, coupled with slowing long-term holder sell-offs, would suggest the market is gradually stabilizing.

Crypto Deleveraging: Perpetual Futures, DeFi Lending, and Liquidity

The liquidation wave on "10.11" initiated a multi-layered deleveraging cycle across futures, DeFi, and stablecoin-collateralized leverage, with ripple effects still reverberating through the crypto market.

Deleveraging Cleansing in Perpetual Futures Markets

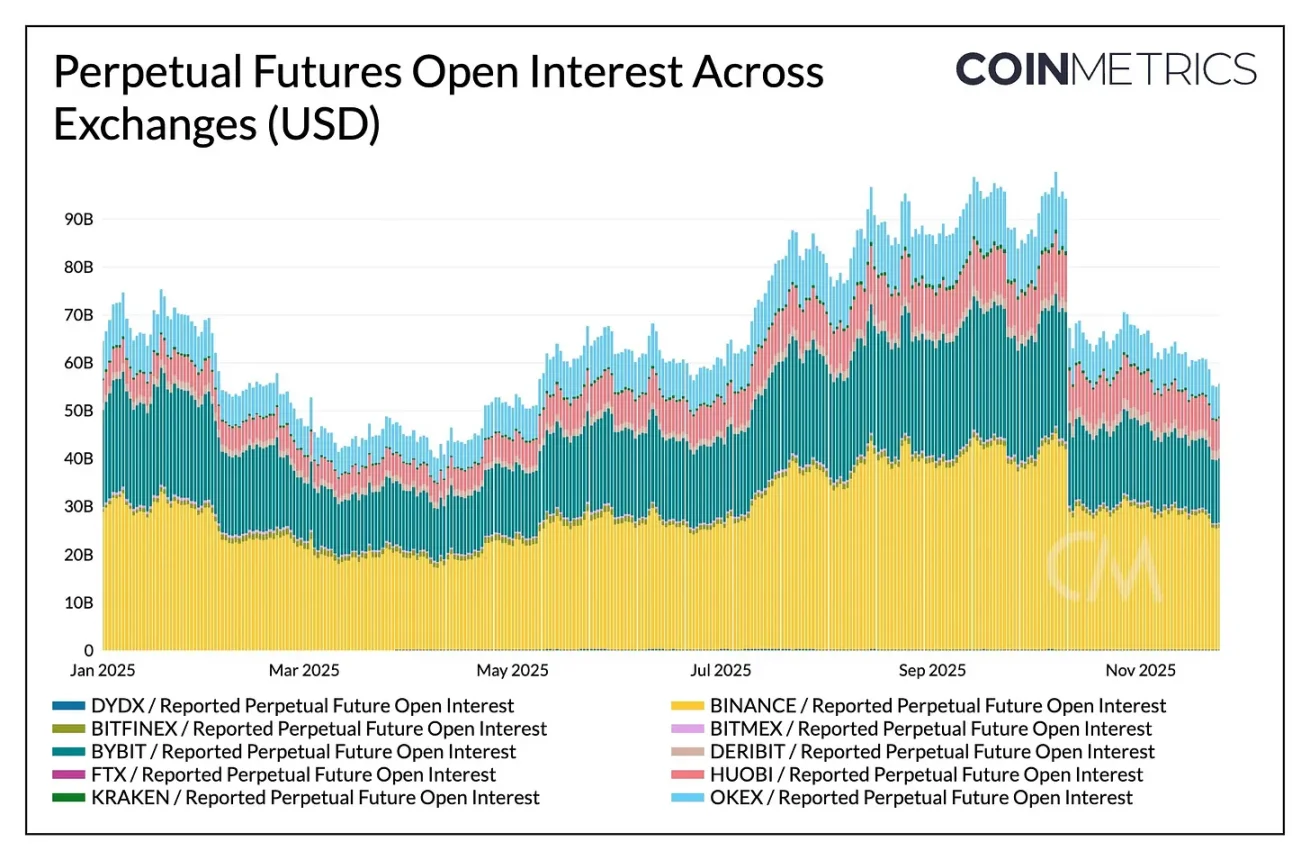

In just a few hours, the perpetual futures market saw the largest forced liquidations in history,reducing months of accumulated open interest (OI) by over 30%. Altcoins and exchanges popular among retail traders (such as Hyperliquid, Binance, and Bybit) experienced the steepest declines in OI—consistent with areas where leverage was concentrated pre-deleveraging. As shown in the chart below, current OI levels remain far below the pre-crash peak of over $90 billion and have continued to dip slightly, indicating effective cleanup of systemic leverage amid market stabilization and realignment.

Funding rates have also weakened during this period, reflecting a reset in long-side risk appetite.Bitcoin funding rates have recently hovered around neutral or slightly negative levels, consistent with the market’s lack of fully restored directional confidence.

Open Interest Changes Across Exchanges’ Perpetual Contracts, Data source: Coin Metrics

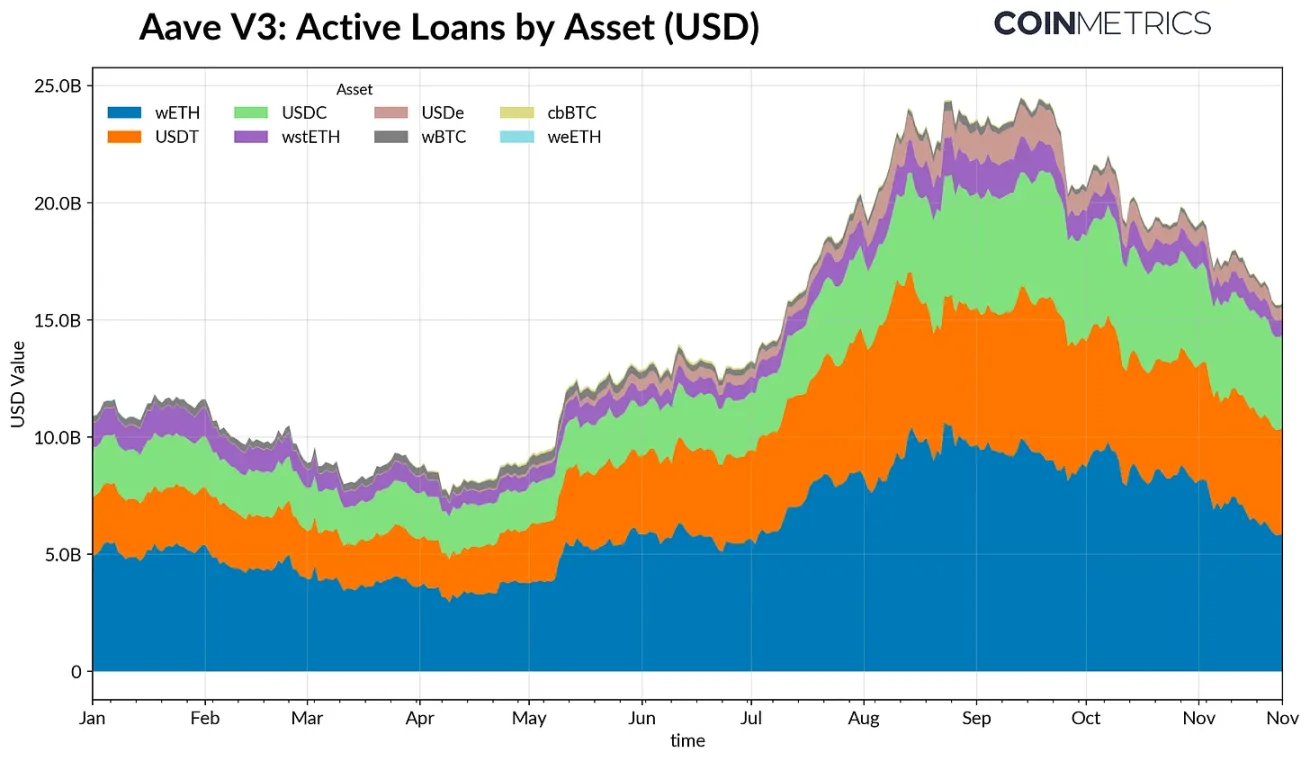

DeFi Deleveraging

The DeFi credit market has also undergone gradual deleveraging. Active loan volumes on Aave V3 have been steadily declining since peaking at the end of September. Amid weak risk appetite and collateral repricing, borrowers have been reducing leverage and repaying debts. Stablecoin-denominated borrowing contracted most sharply—USDe-related lending volume plummeted by 65% following the Ethena USDe depeg event, triggering widespread liquidations of synthetic dollar leverage.

Ethereum-related borrowing also declined: WETH and liquid staking token (LST) loans dropped by around 35%-40%, reflecting reduced circular borrowing strategies and contraction in yield-generating collateral approaches.

Active Loan Volume on Aave V3, Data source: Coin Metrics

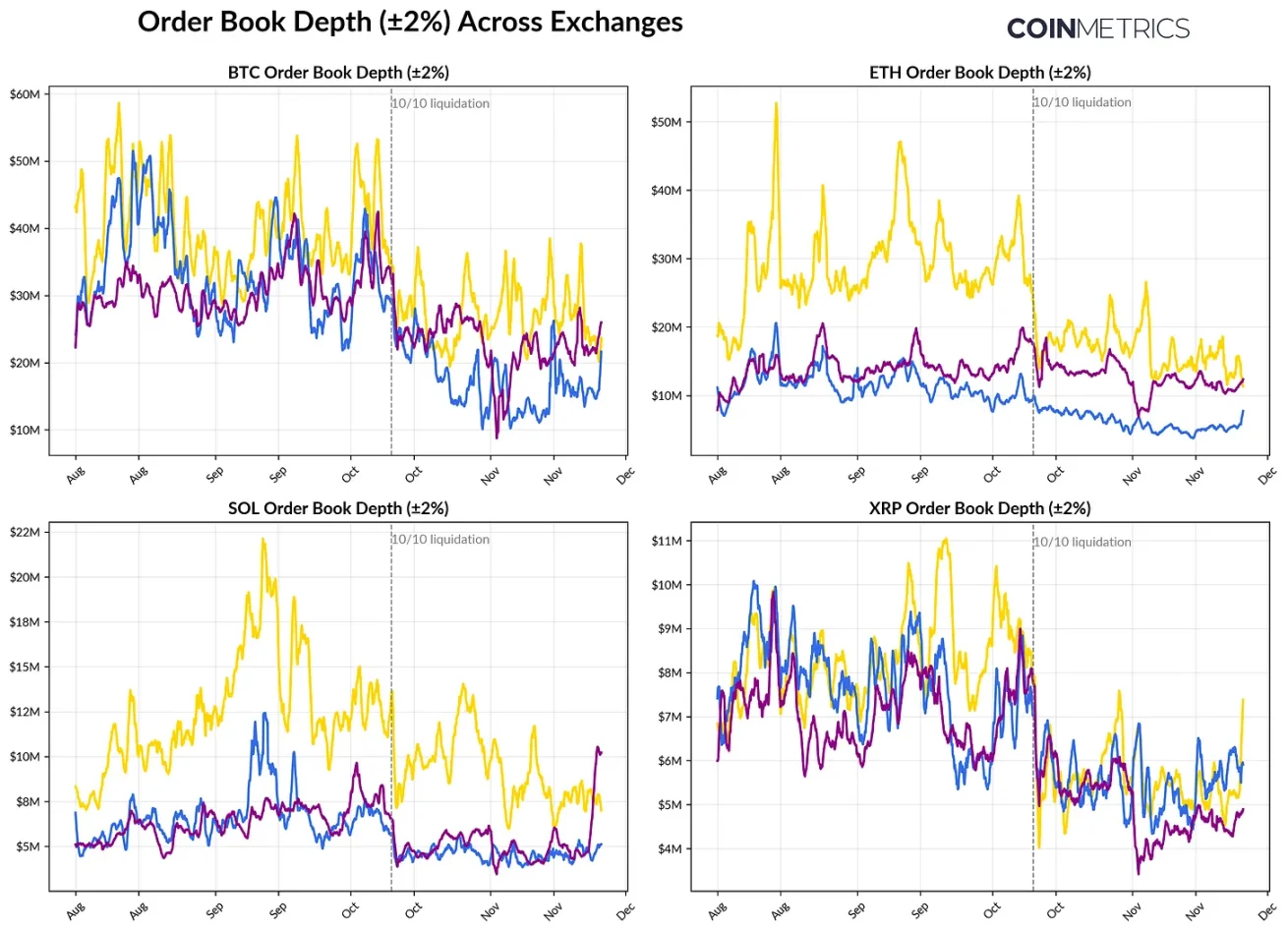

Weak Spot Liquidity

Following the "10.11" liquidation wave, spot market liquidity has remained tight. At major exchanges, volume depth (±2%) for Bitcoin, Ethereum, Solana, and other coins remains 30%-40% below early October levels, indicating that liquidity has not rebounded in tandem with price. With fewer limit orders, the market remains fragile—small trades can trigger disproportionate price swings, amplifying volatility and the impact of forced sell-offs.

Liquidity conditions for altcoins are worse.Order book depth beyond major coins has seen sharper and more persistent declines, reflecting sustained investor avoidance of risk assets and reduced market maker activity. A broad recovery in spot liquidity would help reduce price impact and stabilize the market, but so far, shallow depth remains one of the clearest signals that systemic stress has not fully eased.

Exchange Order Book Depth Changes, Data source: Coin Metrics

Conclusion

The digital asset market is undergoing a comprehensive adjustment driven by weak demand from ETFs and DATs, leverage resets in futures and DeFi markets, and persistently low spot liquidity. While these dynamics weigh on prices, they have also led to a healthier market structure—lower leverage, more neutral positioning, and a growing return to fundamentals-based pricing.

At the same time,the macro environment remains the primary headwind. Weakness in AI-related equities, shifting rate cut expectations, and an overall risk-off tone continue to suppress demand. If key funding channels (ETF inflows, DAT accumulation, stablecoin supply growth) recover and spot liquidity rebounds, the foundation will be laid for market stabilization and eventual reversal. Until then, the market will remain caught in a tug-of-war between macro risk aversion and evolving internal crypto market structures.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News