Nine years ago he already understood Pop Mart and wanted to invest 100 million—why did he still miss it?

TechFlow Selected TechFlow Selected

Nine years ago he already understood Pop Mart and wanted to invest 100 million—why did he still miss it?

Everything is already destined, all fate, not a bit within human control.

Author: Jiangshan Johnson

Source: PR Ren and PRREN

Introduction: Wang Cen, a partner at Sequoia Capital, instantly understood Wang Ning back in 2016. He even gave Wang Ning a highly accurate piece of advice: acquire top-tier IP resources through buyouts whenever possible. This very suggestion almost became the core framework of Pop Mart's current strategic foundation. Wang Cen was also willing to invest 100 million RMB for a 15% stake—a move that would have multiplied nearly 500 times today—yet he still missed out… due to “it.”

(I)

As of June 11, Pop Mart’s stock price closed at HK$269.8 per share, with a total market capitalization of HK$362.3 billion. Founder Wang Ning holds a 48.73% equity stake, giving him a personal net worth of HK$176.5 billion. This makes the 38-year-old from Henan Province not only China’s newest richest person but also further widens his lead over second place.

First, let’s briefly outline Pop Mart’s timeline:

2010: Pop Mart was founded, opening its first store at Beijing’s OMALL shopping center. Positioned as a distributor of trendy toys, it sourced products from other brands and sold various fashion items. However, business was poor—almost unsustainable.

(Wang Ning’s parents ran a grocery store, so he had been familiar with the "grocery" and "retail" model since childhood. While studying at Zhengzhou University in 2008, he began entrepreneurial ventures—including running a popular "box shop." After graduating, unwilling to work as an employee, Wang opened Pop Mart’s first store in 2010.)

2014: Wang Ning visited Japan to scout potential hit products and discovered the blind box sales model of the Japanese doll "Sonny Angel," which was extremely popular among young people. He quickly contacted the brand and brought it to China, pioneering the "trendy toy + blind box" sales model domestically.

2015: Sales of "Sonny Angel" surged in China, generating over 30 million RMB in revenue that year—nearly one-third of the company's annual total. Yet, Pop Mart was still operating at a loss.

Nonetheless, this marked one of the two most critical years in Pop Mart’s history. From this point onward, the company essentially solidified its core strategy. By 2016, it secured investment and key IPs, launching into rapid growth.

The success of "Sonny Angel" proved the promising potential of the trendy toy market. Wang Ning then conducted a Weibo survey asking fans which other collectible toys they liked. In the comments, "Molly" was repeatedly mentioned.

Wang traveled to Hong Kong and met Kenny Wong (Wong Ming-shun), Molly’s designer. After three rounds of discussion, Pop Mart became the exclusive authorized distributor and manufacturer of Molly in mainland China. In July, they launched the first "Molly Zodiac" series, which sold out immediately.

From then on, fueled by the sales phenomenon surrounding Molly, Pop Mart entered a fast-growth phase. From 2017 to 2019, revenues from self-developed products based on the Molly character were 41 million, 214 million, and 456 million RMB respectively. In 2023, MOLLY generated 1.02 billion RMB in revenue, a 27.2% year-on-year increase. In 2024, MOLLY achieved sales of 2.5 billion RMB. Adding these figures together, Molly contributed approximately 4.231 billion RMB in total sales to Pop Mart between 2017 and 2024.

And thus began the now widely known, meteoric rise.

Therefore, 2015 and 2016 were pivotal years for Pop Mart. What exactly happened during those two years?

(II)

In 2015, although Wang Ning had gradually clarified Pop Mart’s direction, the company still incurred a loss of nearly 25 million RMB (with losses of 14.98 million in 2014 and 2.77 million in 2013).

Three consecutive years of losses meant Pop Mart was severely cash-strapped—Wang Ning’s most anxious period.

Luckily, he had begun to grasp the right path—agenting high-quality trendy toy IPs, ideally securing exclusive rights. The 2015 agency of Japan’s "Sonny Angel" clearly showed growth momentum, with a single IP generating 30 million RMB in revenue, validating the development strategy: “A blockbuster product is core competitiveness.”

But signing Molly would require one crucial thing—money.

In 2015, Wang Ning met Zhou Lixia, chairwoman of Jinhui Feng Investment.

(Image source: China Daily Chinese Edition)

In August 2015, Zhou invested several million RMB in Wang Ning (the exact amount has not been disclosed; “several million” is my personal estimate). Given that her venture firm was relatively small and funds limited—and considering that in 2016, when Wang Ning sought to fully buy out Molly, he still needed to raise funds elsewhere—it’s telling that after four failed financing attempts, Zhou had to rally her investment team to pool another 5 million RMB. If just five million could be scraped together this way, the initial investment must have indeed been in the range of several million.

With insufficient funds, raising money became Wang Ning’s top priority in 2016.

Zhou was truly a benefactor to Wang Ning, leveraging her network to help him secure funding. Public records indicate at least four such attempts:

1. Zhou took Wang Ning to pitch at Zhenghe Island. Attendees—investors and entrepreneurs alike—failed to understand the business model. No one expressed interest in investing.

2. Zhou brought Wang Ning to Qingdao for a golf tournament sponsored by Jinhui Feng, attended by many investors. Wang pitched again—still no takers.

3. She arranged a presentation at a large state-owned enterprise. Though the head of the investment department approved, corporate headquarters ultimately rejected the proposal, leading to another failed round.

4. She brought Wang Ning onto a TV show called *China Maker*, where entrepreneurs present projects to a panel of investors who may choose to fund them. This was Wang Ning’s closest brush with major funding in 2016.

(III)

Indeed, Wang Cen, a partner at Sequoia Capital—renowned in China’s VC circle as someone who deeply understands retail—had a pivotal encounter with Wang Ning. Watching the footage today, it’s clear Wang Cen truly understood retail, pinpointed key insights accurately, and delivered sharp, incisive feedback. Among all the investors present, he offered both the highest valuation and the largest investment commitment.

Let’s revisit that moment:

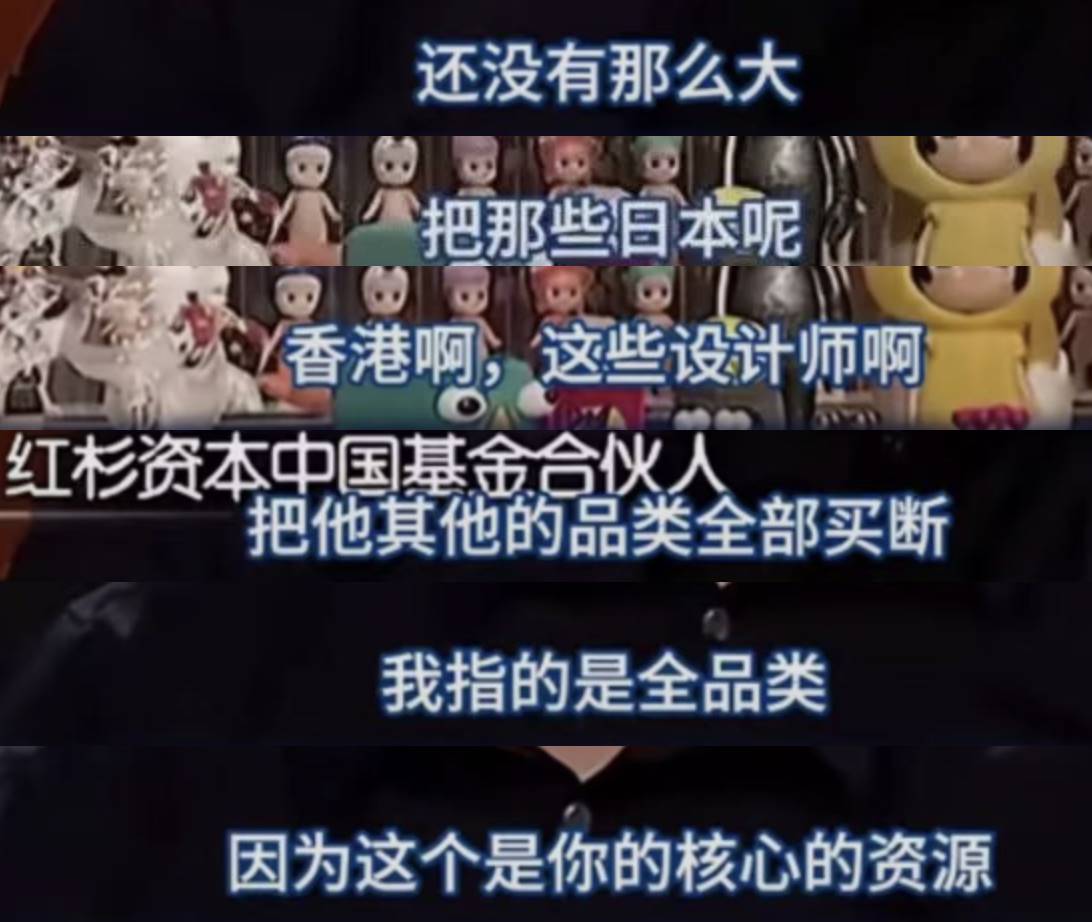

At first glance, Pop Mart seemed like just another retailer—low barriers to entry. So one judge cut straight to the chase: “What is your core competitive advantage?”

(Screenshots from "Dan Bin"'s Douyin account; same below)

Wang Ning responded: After more than five years of operation, their product and service systems had accumulated numerous SOPs (standard operating procedures). As a result, they earned dual certifications from premium malls and luxury brands, allowing them to open stores adjacent to flagship boutiques like Louis Vuitton.

This is indeed a rare competitive advantage.

It also explains why global stars like Rihanna and Lisa attach Labubu charms to their Hermès bags—because ten years ago, Wang Ning intentionally positioned Pop Mart stores next to luxury boutiques. This placement serves as powerful brand endorsement: trendy toys naturally complement luxury handbags. Buying a bag and adding a Pop Mart figurine allows owners to express both elegance and individuality.

Back to the dialogue: Wang Ning then highlighted his second core competitive advantage—the exclusive partnership with Kenny, an artist in the anime/IP creation space comparable to Jay Chou’s status in music: none other than Kenny Wong, the creator behind Molly, the IP that truly catapulted Pop Mart into the mainstream.

(Hand-drawn sketches by Kenny during Molly’s creation)

Wang Cen, true to his reputation for understanding retail, immediately picked up on the insight:

After receiving confirmation from Wang Ning,

Wang Cen instantly grasped his vision.

Then, Wang Cen made the most aggressive offer among all investors present—proposing an investment of 100 million RMB for a 15% stake.

When Wang Ning asked how he should use the 100 million if funded, Wang Cen doubled down with spot-on advice: continue hoarding top-tier IP resources—acquire them via full buyouts.

This is precisely Pop Mart’s current core strategy. To date, the company has signed over 200 world-class designer artists globally. Combining IP incubation, trendy toy commercialization, and Pop Mart’s superior distribution channels ensures access to the hottest IPs in the market—Molly in earlier years, Labubu more recently (see: Why Has Pop Mart’s Labubu Gone Global?)

(IV)

We all know the outcome today.

Yes,

Despite fully understanding the opportunity—and offering 100 million RMB for a 15% stake—

That investment would now be worth 49.6 billion RMB,

Nearly a 500x return,

A single deal that could have made Wang Cen legendary and allowed him to retire triumphantly.

But, but, but—

He didn’t invest.

In recent interviews, Wang Cen admitted candidly,

He only half-understood it,

And hadn’t spent enough time studying it thoroughly.

(Source: Screenshot from Phoenix Technology video)

I believe he hasn’t fully revealed his true thoughts.

The entire conversation between Wang Cen and Wang Ning in 2016 clearly shows:

1. Wang Cen deeply understood Pop Mart (both core competitive advantages—understood instantly)

2. His advice to Wang Ning was razor-sharp and essentially outlines Pop Mart’s core strategy today.

The real reason? He simply didn’t anticipate that the trendy toy business could scale so massively and grow so rapidly. Had he committed 100 million RMB on behalf of his fund, he would have borne significant risk, responsibility, and opportunity cost compared to other investments.

Wang Ning himself couldn’t have foreseen such explosive growth either. But for him, growing Pop Mart from 100 million to 1 billion, 10 billion, or even hundreds of billions—it was all part of his singular mission. He would keep going regardless. Thus, Wang Ning maximized his capture of the massive "trendy toy industry" boom.

But Wang Cen wasn’t in that position. That’s why he missed out.

2017: Pop Mart revenue reached 158 million RMB, net profit 1.56 million RMB.

2018: Revenue 514 million RMB, net profit 99.52 million RMB.

2019: Revenue 1.683 billion RMB, net profit 451 million RMB.

And then performance kept improving, profits rising steadily…

Reportedly, after 2017, Wang Ning stopped seeking investors altogether. The more profitable Pop Mart became post-2017, the more investors approached him—including top-tier firms and major financiers—but Wang Ning politely declined every single one.

Perhaps Wang Cen often sighs in regret late at night…

But everything was already destined.

It’s fate.

Not a shred can be forced.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News