Exposing Common "Labyrinthine" Tactics in Token Economic Models: Transparent Capital Structure Is the Right Solution

TechFlow Selected TechFlow Selected

Exposing Common "Labyrinthine" Tactics in Token Economic Models: Transparent Capital Structure Is the Right Solution

Prioritize transparency.

Author: 0xLouisT

Translation: TechFlow

Tokenomics Series

In mythology, the labyrinth was built to imprison the Minotaur—a terrifying creature with a human body and a bull's head. King Minos, fearing the beast, commissioned the genius craftsman Daedalus to design an intricate maze from which no one could escape. However, when the Athenian prince Theseus, aided by Daedalus, killed the Minotaur, Minos became furious. As punishment, he imprisoned Daedalus and his son Icarus within the very labyrinth Daedalus had designed.

While Icarus’s hubris led to his downfall, it was Daedalus who truly shaped their fate—without him, Icarus would never have been trapped. This myth closely mirrors the hidden token deals commonly seen in the current crypto cycle. In this article, I will expose these arrangements—labyrinthine structures meticulously crafted by insiders (like Daedalus)—that doom projects (like Icarus) to failure from the start.

What Are Backdoor Token Deals?

High FDV tokens have become a hot topic, sparking ongoing debates about sustainability and impact. Yet, one dark corner is often overlooked: backdoor token deals. These are agreements made off-chain among a select group of market participants through private contracts and side arrangements. They're typically hidden and nearly impossible to detect on-chain. If you're not an insider, you'd likely never know they exist.

In his recent piece, @cobie introduced the concept of "ghost pricing," highlighting how true price discovery now occurs in private markets. Building on that, I want to introduce the idea of ghost tokenomics—to illustrate how on-chain tokenomics may present a distorted and inaccurate picture of the real, off-chain token distribution. What you see on-chain might appear to be the token’s genuine “cap table,” but it’s misleading; the ghostly off-chain version is often the accurate one.

While there are many types of token deals, I’ve identified several recurring patterns:

-

Advisor Allocations: Investors receive extra tokens under the guise of advisory services, often categorized under team or advisor allocations. In reality, this is frequently just a way for investors to lower their cost basis without providing substantial additional advice. I’ve seen advisor allocations reach up to five times an investor’s initial investment, effectively reducing their actual cost by 80% compared to the official valuation.

-

Market Maker Allocations: A portion of the token supply is reserved for market-making operations on centralized exchanges (CEX), helping boost liquidity. But conflicts arise when the market maker is also an investor in the project. They can use these allocated tokens to hedge against their locked holdings.

-

CEX Listings: To get listed on top-tier CEXs like Binance or Bybit, projects must pay marketing and listing fees. If investors help secure these listings, they may receive additional performance-based incentives (up to 3% of total supply). @CryptoHayes recently published a detailed analysis showing such fees could amount to as much as 16% of the total token supply.

-

TVL Leasing: Whales or institutions providing liquidity often receive higher, exclusive yields. While regular users might settle for 20% APY, certain whales quietly secure 30% returns through private deals with the foundation. While this practice can be positive and necessary to ensure initial liquidity, these arrangements must be disclosed transparently within the tokenomics for the community.

-

OTC Rounds: While common and not inherently harmful, OTC rounds are often opaque due to undisclosed terms. The most impactful are so-called KOL rounds, which act as accelerants for token prices. Certain top-tier L1 projects (names withheld) have recently adopted this strategy. Major Twitter KOLs were offered highly attractive token deals with steep discounts (~50%) and short lock-up periods (linear vesting over six months) to incentivize them to promote the token as the next [insert L1] killer. If in doubt, here’s a handy KOL translation guide to help you see through the hype.

-

Selling Unlockable Staking Rewards: Since 2017, many PoS networks have allowed investors to stake vested tokens while collecting unvested rewards. If these rewards can be unlocked early, early investors gain faster exit opportunities. @gtx360ti and @0xSisyphus recently highlighted examples in Celestia and Eigen.

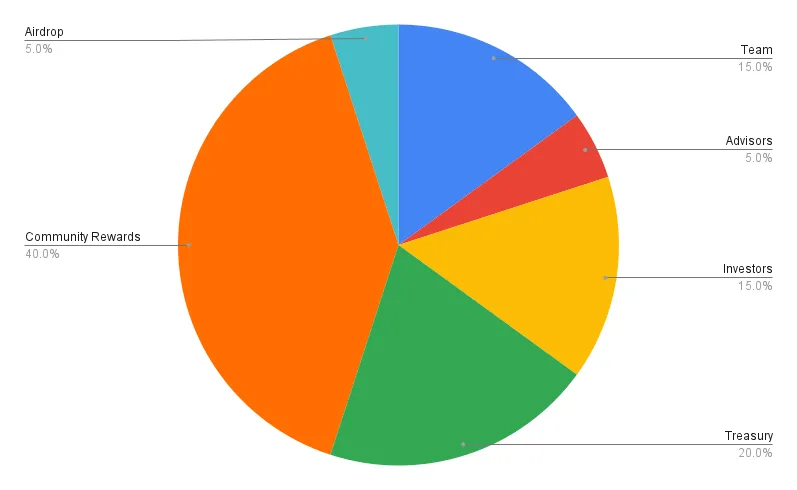

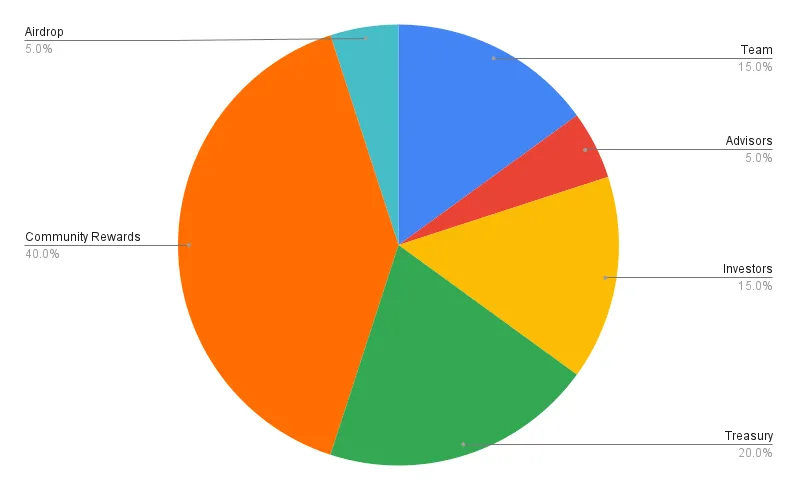

These token deals result in "ghost" tokenomics. As a community member, you might see a tokenomics chart like the one below and think it looks balanced and transparent (charts and data for illustrative purposes only).

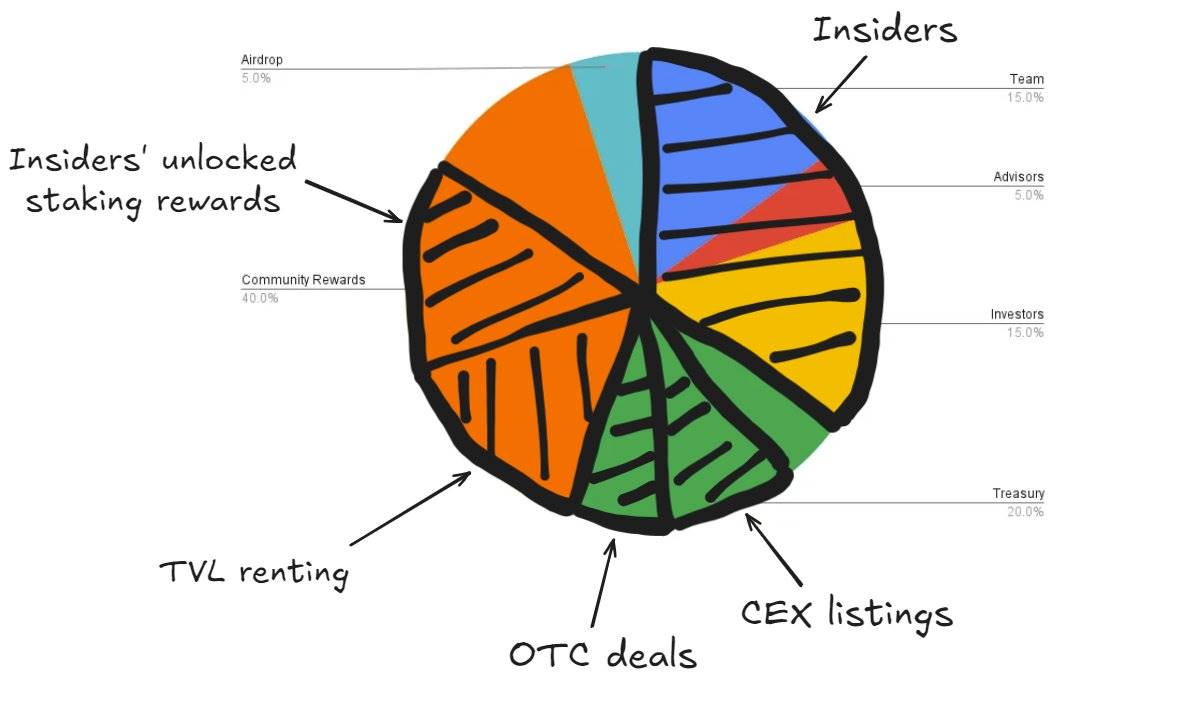

But if we peel back the surface and reveal the hidden ghost deals, the real tokenomics look more like this pie chart—leaving almost nothing for the community.

Just as Daedalus was the architect of his own prison, these arrangements seal the fate of many tokens. Insiders trap their projects in mazes of opaque deals, causing value to leak out from every direction.

How Did We Get Here?

Like most market inefficiencies, this issue stems from a severe imbalance between supply and demand.

The 2021–2022 venture capital boom flooded the market with projects. Many waited over three years to launch their tokens, and now they’re all rushing into a crowded, competitive environment—fighting for TVL and attention in a far colder market than before. It’s no longer 2021.

Demand cannot keep up with supply. There aren’t enough buyers to absorb the flood of new token launches. Likewise, not every protocol can attract deposits, making TVL a scarce and highly sought-after resource. Many projects fail to achieve natural product-market fit (PMF) and instead fall into the trap of overusing token incentives to artificially inflate KPIs, compensating for a lack of sustainable appeal.

Today, private markets remain the primary active arena. With retail participation declining, most VCs and funds struggle to generate meaningful returns. Shrinking profits force them to generate gains through token deals rather than asset selection.

Token distribution remains a core challenge. Due to regulatory barriers, distributing tokens directly to retail investors is nearly impossible. Teams have limited options, relying mostly on airdrops or liquidity incentives. If you're a team trying to solve token distribution via ICO or other means, feel free to reach out.

Summary

Using tokens to incentivize stakeholders and accelerate development isn't inherently problematic—it can be a powerful tool. The real issue lies in the complete lack of on-chain transparency in tokenomics.

Here are key recommendations for crypto founders to improve transparency:

-

Don’t offer VC advisor allocations: Investors should provide full value without needing extra token grants. If an investor requires additional tokens to commit capital, they likely lack confidence in your project. Do you really want such people on your cap table?

-

Market making is commoditized: Market making services are now standardized and should be available at fair prices. Avoid overpaying. To help founders better understand this space, I’ve written a guide.

-

Don’t mix fundraising with unrelated operational matters: During fundraising, focus on securing capital and investors who add strategic value. Avoid discussing market makers or airdrops at this stage—don’t sign agreements prematurely on such issues.

-

Enhance on-chain transparency: On-chain tokenomics should accurately reflect actual token distribution. At launch, transparently allocate tokens to distinct wallets representing each category (team, advisors, investors, etc.) as shown in your tokenomics chart. For example, ensure there are six main wallets clearly designated. Proactively contact the following teams:

-

@etherscan, @ArkhamIntel, and @nansen_ai: Label all relevant wallets.

-

@Tokenomist_ai: Provide vesting schedules.

-

@coingecko and @CoinMarketCap: Ensure accuracy in circulating supply and FDV.

-

If you're an L1/L2/appchain, ensure your native block explorer is intuitive and user-friendly.

-

Use on-chain vesting contracts: For team, investor, OTC, or any type of vesting, ensure it’s implemented transparently and automatically via smart contracts on-chain.

-

Lock staking rewards for insiders: If insiders are allowed to stake locked tokens, at minimum, ensure the staking rewards are also locked. See my take on this practice.

-

Focus on product, ignore CEX listings: Don’t obsess over getting listed on Binance—it won’t fix your fundamentals. Take @pendle_fi as an example: it traded on DEXs for years, achieved PMF, and then easily secured a Binance listing. Focus on building your product and growing your community. Once your fundamentals are strong, CEXs will come to you—with better terms.

-

Don’t hand out token incentives too easily: If you’re giving away tokens too freely, it may indicate flaws in your strategy or business model. Tokens are valuable resources—use them carefully and with specific goals in mind. They can be growth tools, but not long-term solutions. When planning token incentives, ask yourself:

-

What specific, measurable outcomes do I expect from these tokens?

-

What happens to this metric once incentives stop?

If you believe the metric will drop by 50% or more after incentives end, your token incentive plan likely has serious issues.

If there’s one key takeaway from this article, it’s this: Prioritize transparency above all.

I’m not here to point fingers. My goal is to spark genuine discussion, promote transparency, and reduce deceptive token deals. I truly believe this will strengthen the space over time.

Stay tuned for the next part of my tokenomics series, where I’ll dive into a comprehensive guide and rating framework for tokenomics.

Let’s make tokenomics transparent again—and escape the Daedalus labyrinth.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News