Friend.Tech Game Theory — WAGMI or Ponzi Scheme?

TechFlow Selected TechFlow Selected

Friend.Tech Game Theory — WAGMI or Ponzi Scheme?

This could be a great investment (if played right), but beyond speculation on Keys and airdrops, you might also genuinely derive significant value from it.

Written by: AYLO

Translated by: TechFlow

I believe you've all heard of Friend.Tech, a platform that combines social media with cryptocurrency:

-

Users can buy, sell, and trade "Keys," which are tied to specific X (Twitter) accounts—essentially purchasing shares in a user on the platform.

-

The price of Keys increases along a bonding curve. When a Key reaches 1 ETH, a room typically has around 100 people.

-

Owning a Key grants access to that user’s private chat room within the app.

-

Creators earn revenue from transaction taxes on each Key trade (5% goes to the platform, 5% to the creator).

-

The app is mobile-friendly and uses a unique “progressive web app” technology to bypass traditional app stores.

-

Built on Coinbase's BASE chain.

At first glance, this might seem like just another speculative app (remember BitClout?), but is it really? Over the past few weeks, as I’ve thoroughly tested the platform, I’ve been pondering this very question.

Today, I’d like to discuss my findings and share a unique perspective as an early user of the platform with a Twitter following. I developed my own strategy for FT and was among the first to aggressively push a completely new approach—I’ll get into that later.

My overall view: This could be a great investment (if played right), but beyond speculation on Keys and potential airdrops, there may also be real value to gain here.

Data Overview

Looking at Friend.Tech’s on-chain metrics tells a seemingly positive story.

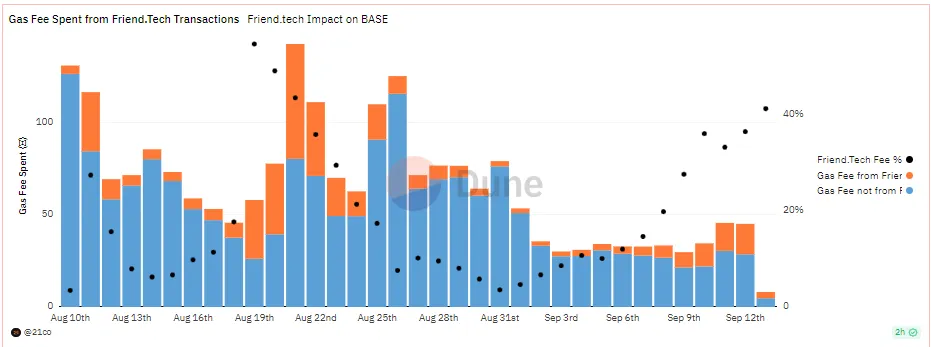

First, FT is unquestionably the leading app on BASE. This is evident from the percentage of fees it generates on the BASE chain—averaging around 20%. For a single application to generate 20% of total network fees is remarkable. Even more striking is that BASE is now the leading Optimistic rollup and ranks second among all Layer 2s, underscoring how dominant FT is in driving chain activity.

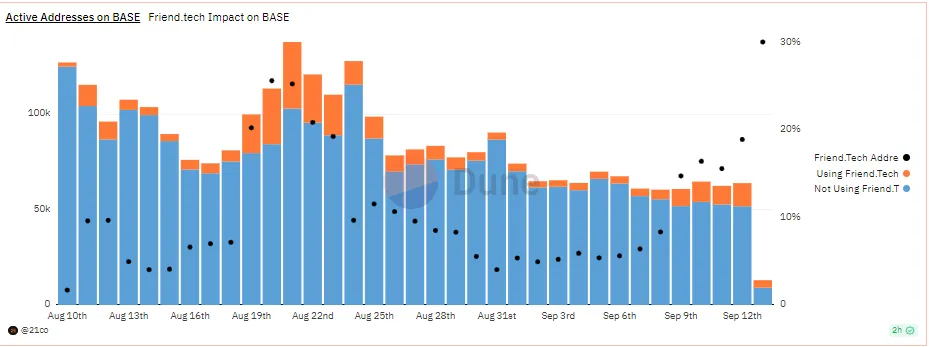

FT’s importance to the BASE chain is also reflected in its share of active users, currently averaging about 10%.

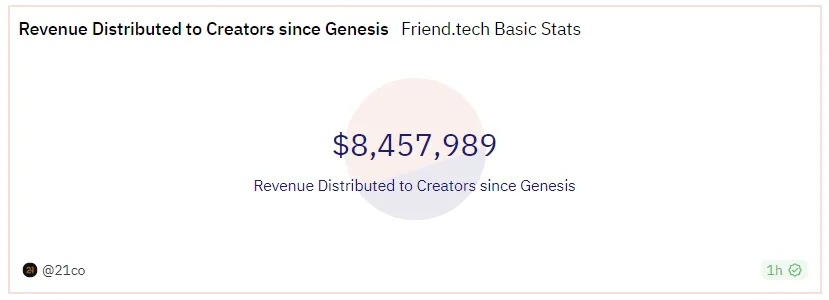

This level of engagement has led the platform to distribute over $8 million to users in just over a month—an impressive achievement for a beta application.

Coinbase launching its own chain is a major move not to be underestimated. As interest in crypto rises again, Coinbase will guide mainstream users into their new decentralized ecosystem. It’s easy to imagine that as BASE grows in popularity, its flagship application will grow with it.

Looking at daily active users, we see steady growth over the past two weeks. It should also be noted that this metric only tracks users who conduct transactions, excluding those who simply hold Keys or participate in chats—the actual number could be much higher.

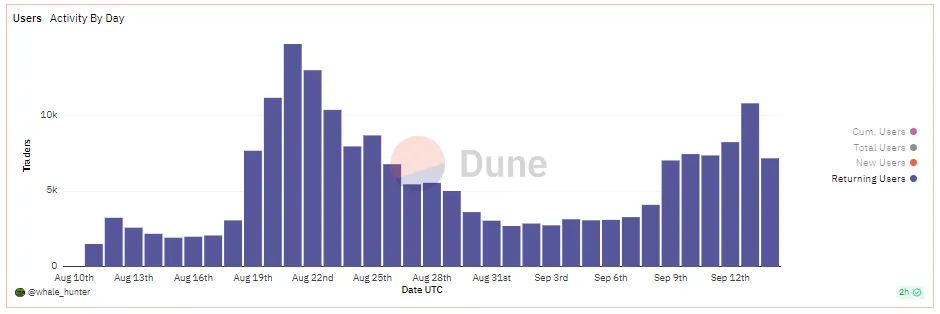

The user retention chart is also very bullish, showing repeated use of the platform.

Now looking at TVL, it has shown a consistent upward trend.

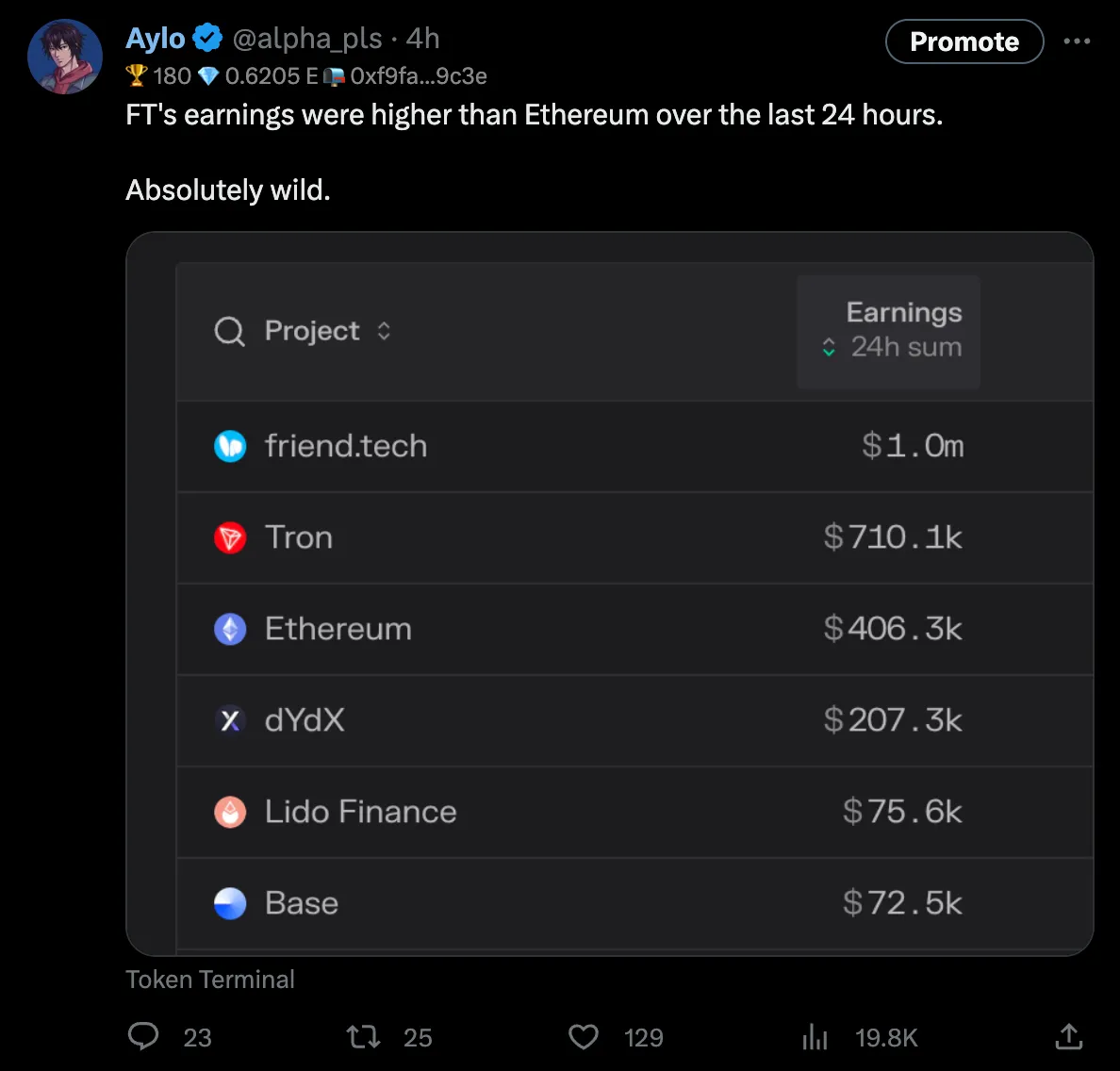

At the time of writing, its 24-hour revenue even surpassed Ethereum’s.

At the time of writing, its 24-hour revenue even surpassed Ethereum’s.

So what do these statistics tell us?

People are steadily returning to the app, staying longer, and keeping ETH deposited on the platform. For a new social app, these are excellent retention metrics and suggest strong momentum ahead.

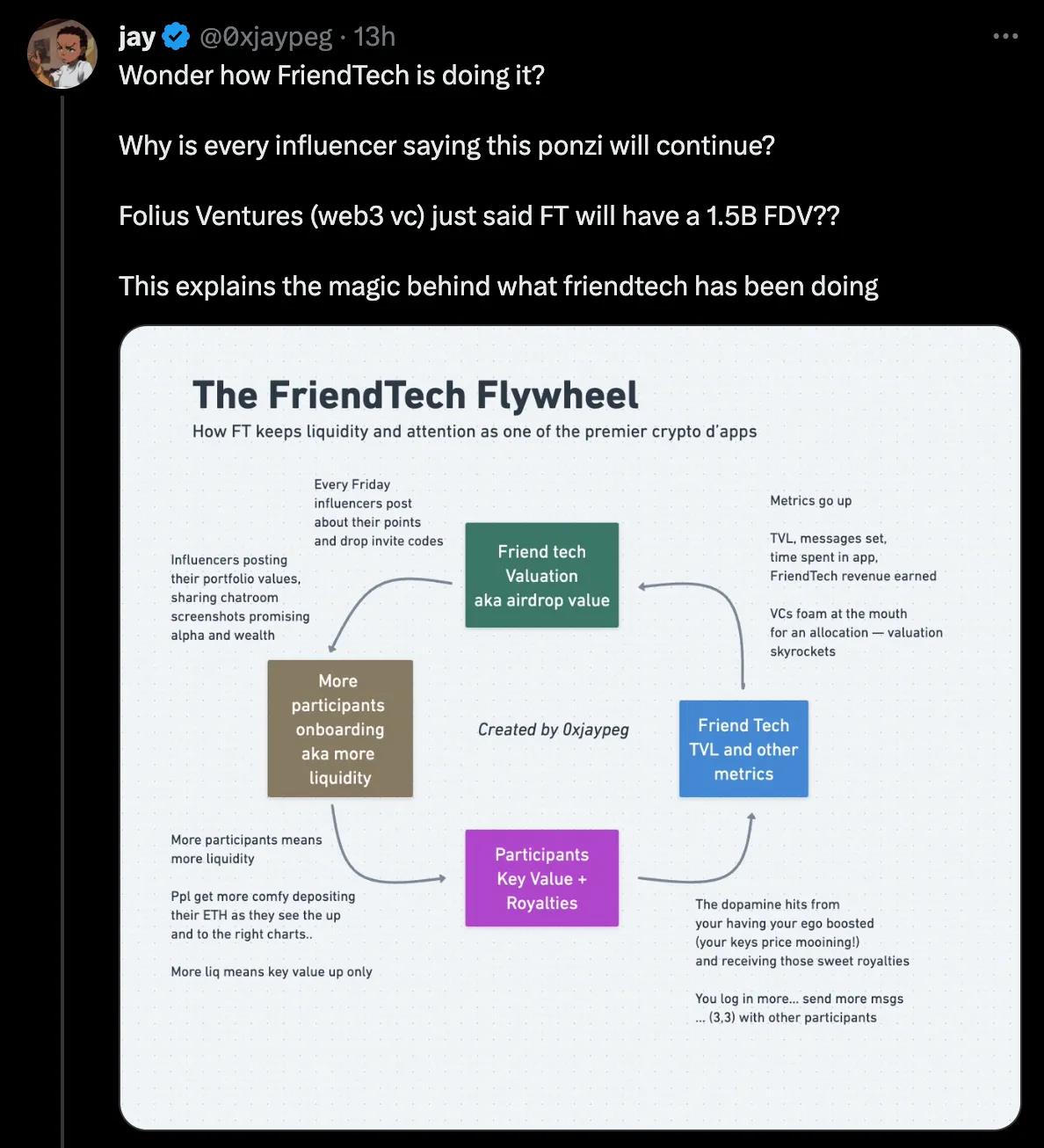

A key driver of this retention is a powerful flywheel effect.

We’ve seen similar patterns in DeFi apps before—yield farmers come in, collect rewards, then leave. But the high rate of returning users on FT suggests something different is happening.

If a platform lacks real utility, you’d expect its TVL to decline, triggering a death spiral. FT shows stickiness. It indicates that the platform may actually have enough utility to sustain itself for some time.

FT Analysis and Perspectives

One thing I appreciate about the app is that it doesn’t compete directly with mainstream social platforms like X, Instagram, or TikTok. It occupies its own niche: small, private, exclusive chat rooms. Anyone can create a community where membership is genuinely valued.

This is where people misunderstand the bonding curve. The total number of people in a room is inherently limited to a small group. This is a feature, not a bug.

For me personally, being able to share thoughts, trades, and information I wouldn’t post publicly means a lot. I’ve truly enjoyed the atmosphere in my and others’ chat rooms, and I’ve profited from insights unavailable elsewhere.

FT is composable—you’re already seeing many builders building on top of it. We’ll see many new products emerge in the ecosystem: full DeFi suites (perpetual contracts, lending, trading interfaces), analytics platforms, better tools to leverage FT, and more. Many projects are already emerging here, and they’ll only improve.

I don’t know how it will play out, but it certainly enhances FT’s network effects. It wouldn’t be surprising if FT launches a grant program to further incentivize development around the platform.

FT’s potential TAM (Total Addressable Market) is quite large. So far, the product seems positioned as a tokenized paid-group market—you can see all these groups within the app. Paid groups as a category have existed for a long time. They’ve captured this market and made it easy for anyone to launch their own group.

The app’s potential extends far beyond crypto users, traders, and enthusiasts. There are rumors that the music industry could be another major entry point for FT. Imagine having intimate access to top global artists—you can bet hundreds would pay for such exclusive access.

From a technical standpoint, FT is barebones today—but still attracting massive attention. As they add more features, more people will find creative ways to use the platform. Adding video support to chat rooms, for example, would attract an entirely different audience.

Using Ponzi-style economics to bootstrap adoption is the fastest way to get lots of people doing something, but it’s clearly unsustainable.

I do think FT will need to add alternative revenue streams for creators on the platform. Currently, you earn via trading fees on Keys—creators receive 5% of each transaction. However, if Key holders choose to hold long-term, creators won’t see additional income. Right now, they’re earning from airdrops and platform share, which is great, but long-term sustainability of valuable chat rooms will require clearer incentives.

Ideas could include charging non-Key holders a one-time fee to post in a room, offering time-limited passes, or enabling tipping on posts. There are many possible extensions.

Since I’ve been fairly positive about FT so far, let me balance my views by discussing what I’m uncertain about:

I believe 3,3 (people buying and holding each other’s Keys) is a Ponzi scheme—eventually people will lose ETH by buying others’ Keys at absurd prices, completely disproportionate to the value offered in their chat rooms.

If you join early, you might get lucky, but if you join late, when people start dumping each other’s Keys, it will end badly. That moment will come sooner or later.

People are buying each other’s Keys at ridiculous valuations, and at some point in the future, those Keys won’t justify their price. The sole aim of this strategy is to accumulate the most points and hope an airdrop makes the ETH investment worthwhile. Maybe it will work, but the risk is extremely high. Still, I can’t deny this behavior has greatly benefited the platform’s early growth.

Indexing mirrored chats is a big issue the app needs to solve—and I don’t have a good answer either.

Much of the alpha information from FT chats is being freely copied onto the internet.

This undermines the app’s value proposition. Not entirely, though—people still value direct interaction and ownership of a Key—but it definitely harms the value of Keys by weakening exclusivity.

As I’m editing this article, I’ve heard the FT team has taken steps to shut it down. How this evolves will be fascinating to watch.

I think some larger accounts may eventually stop sharing certain content in their chats if discussions are leaked online. For many, FT’s unique selling point is sharing things they wouldn’t normally disclose to a broader audience.

I believe eventual utility will become one of the most important aspects of Keys, because you can’t prevent chat leaks, nor rely solely on price appreciation.

Another issue is sniping. Bots are抢购 Keys, giving regular users no fair chance to buy. While there are solutions emerging, such as:

Manifold offering anti-snipe services for large accounts. Still, I believe FT itself needs to address this.

I’ve had a lot of fun on FT, but I want to make clear I’m not blind to its issues.

Clearly, FT will also have to navigate potential regulatory challenges. But we must remember the project is still in beta—that’s precisely why test versions exist: to identify and fix problems before wider release.

Earning Airdrops

Friend.Tech recently unveiled its points allocation system. People have discovered several ways to accumulate points:

-

Through referral links;

-

Increase in the value of your own Key;

-

Holdings;

-

Trading volume (to a lesser extent).

The platform appears to prioritize total Key holdings and in-app daily activity. You can’t just hold Keys and earn points—you must be active. It’s designed to drive user behavior, build habits, and increase retention.

Your total points will be published every Friday.

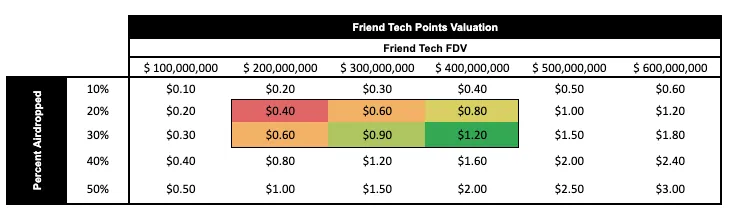

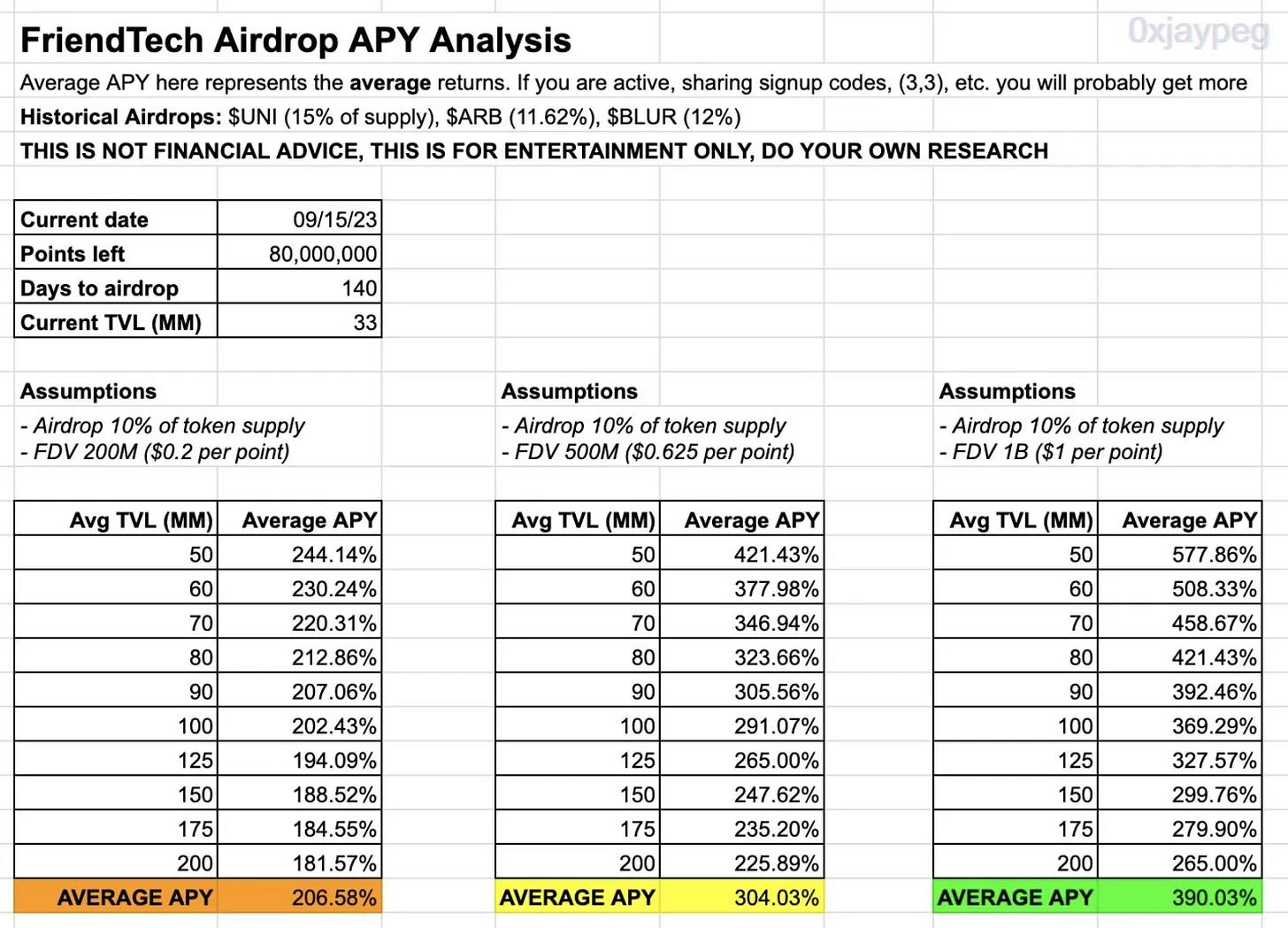

How much will these points be worth? Right now, it’s all speculation. We don’t know the point-to-token ratio, what portion of total supply will go to airdrops, or the market conditions at token launch—so assigning a precise monetary value is difficult.

Some have thrown out rough estimates and modeled various scenarios to guess at potential airdrop value:

As you can see, a conservative estimate values each token at approximately $0.50. If you invest in people whose group chats you enjoy and find useful, that’s not bad at all.

Ecosystem

Another major benefit of FT is the ecosystem of tools built to serve its community. Here are some I’ve handpicked to help you get started.

DeFi

PerpsTech

A perpetual contract Dex designed specifically for FT. Use perps to go long or short on KOLs.

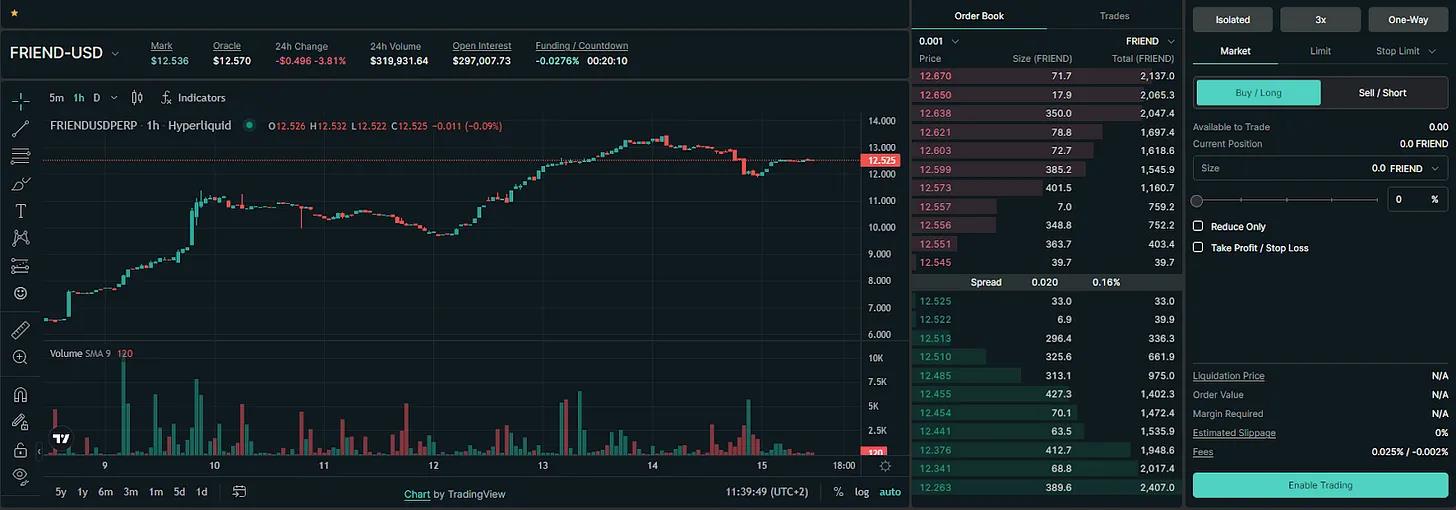

HyperLiquid

Hyperliquid offers a way to speculate on the FT ecosystem as a whole through perpetual contracts based on TVL. Before FT launches its own token, this is a good way to gain exposure.

DerpDEX ERC20 Wrapper

DerpDEX created a wrapper that converts FT Keys into ERC20 tokens, freely tradable outside the FT ecosystem, allowing you to use Keys however you wish beyond the app.

Tools

FriendTech Gems

A simple Chrome extension that overlays key FriendTech data directly into your X feed. Greatly helps track the market without extra effort—very convenient.

FriendTech.info

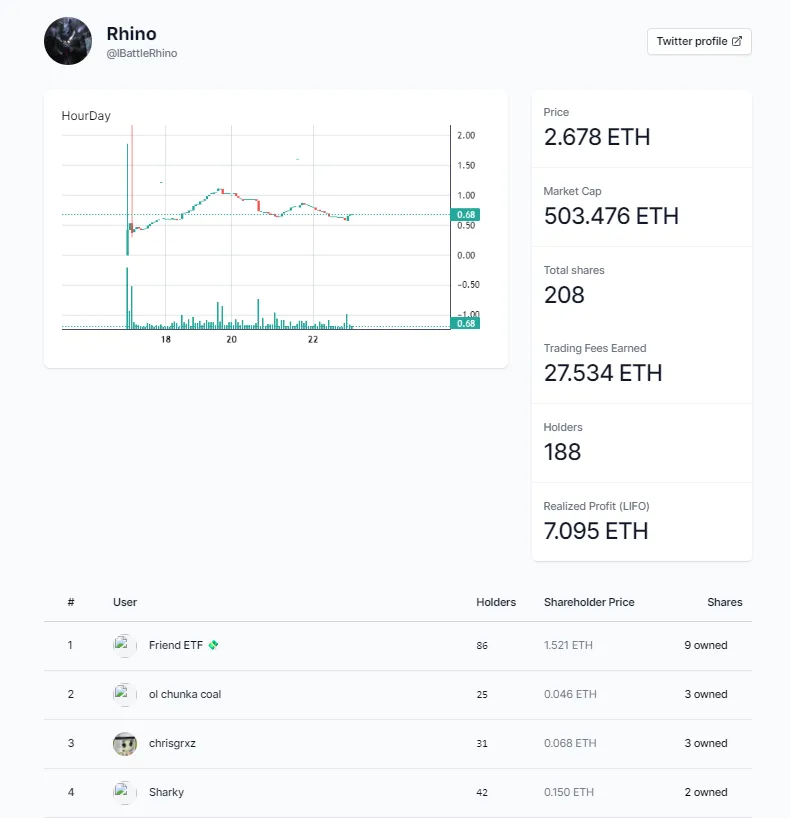

A great place to check top accounts. My favorite feature is the “Recently Joined” section, where you can try to spot rising stars before they blow up.

You can also access valuable info for each user and see who holds their Key.

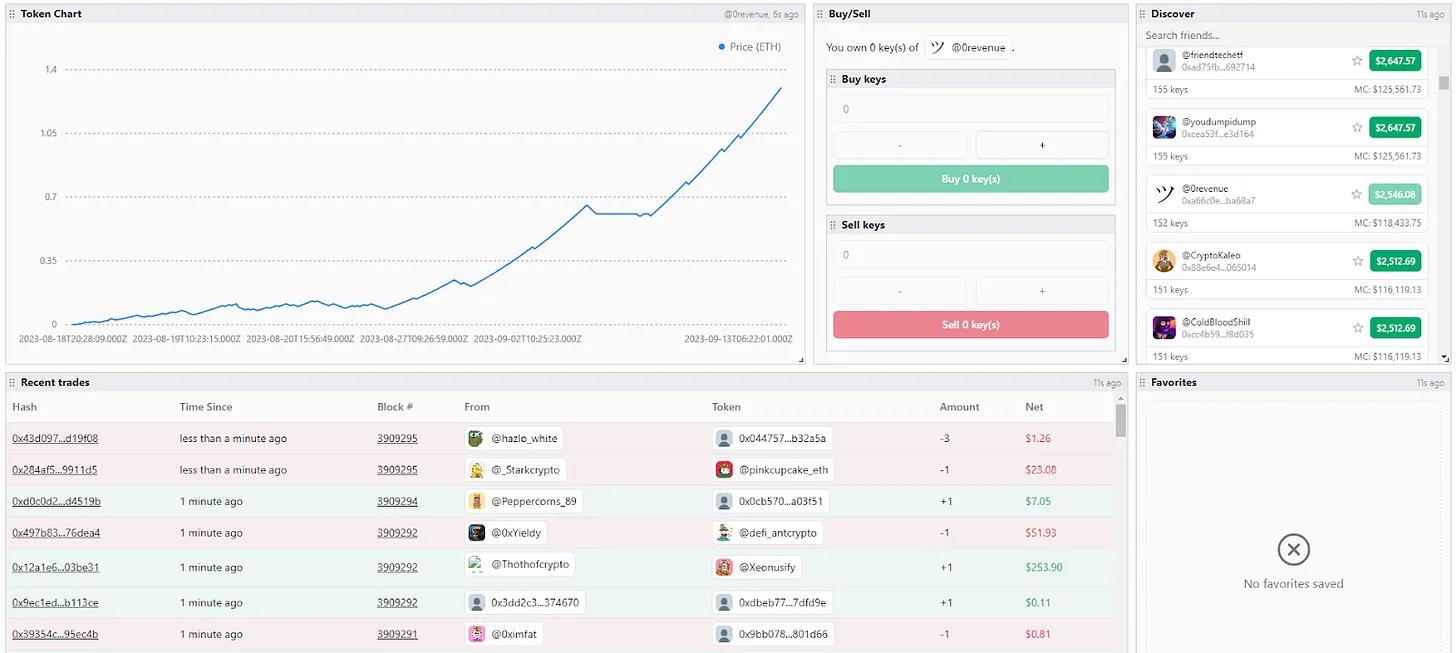

FriendMex

Your go-to front-end for all advanced users.

Friendex by Spotonchain

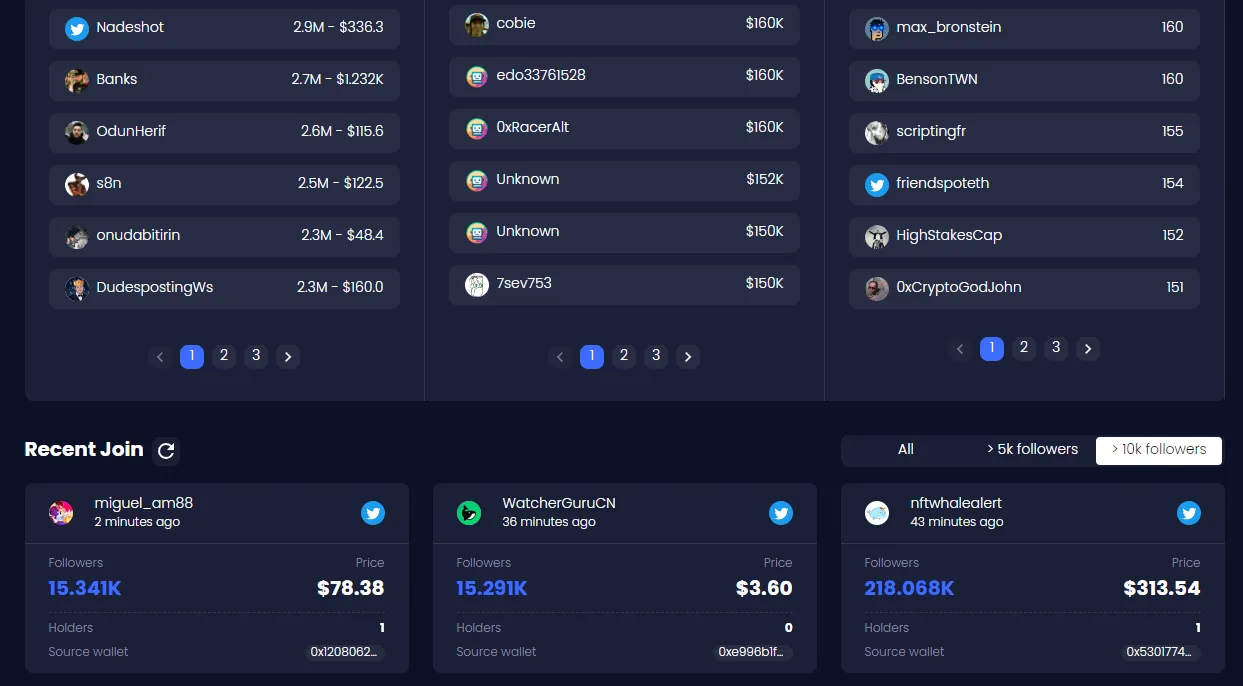

A clean, minimalist KOL aggregator that groups accounts by follower count. The best feature is being able to sort the “Recently Joined” section by follower count.

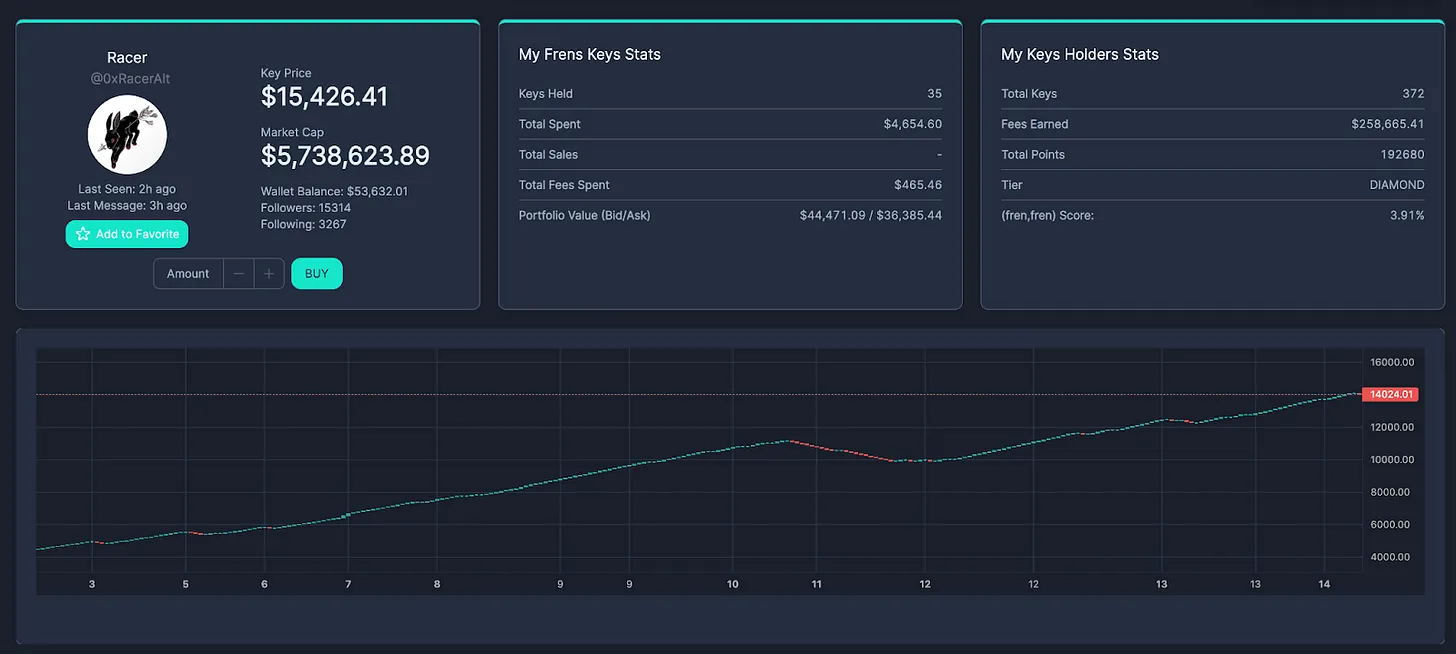

frentech.octav

Another excellent analytics platform displaying all stats related to any FT account. The FT founder’s market cap is now $5.7 million, and buying his Key costs $15,000.

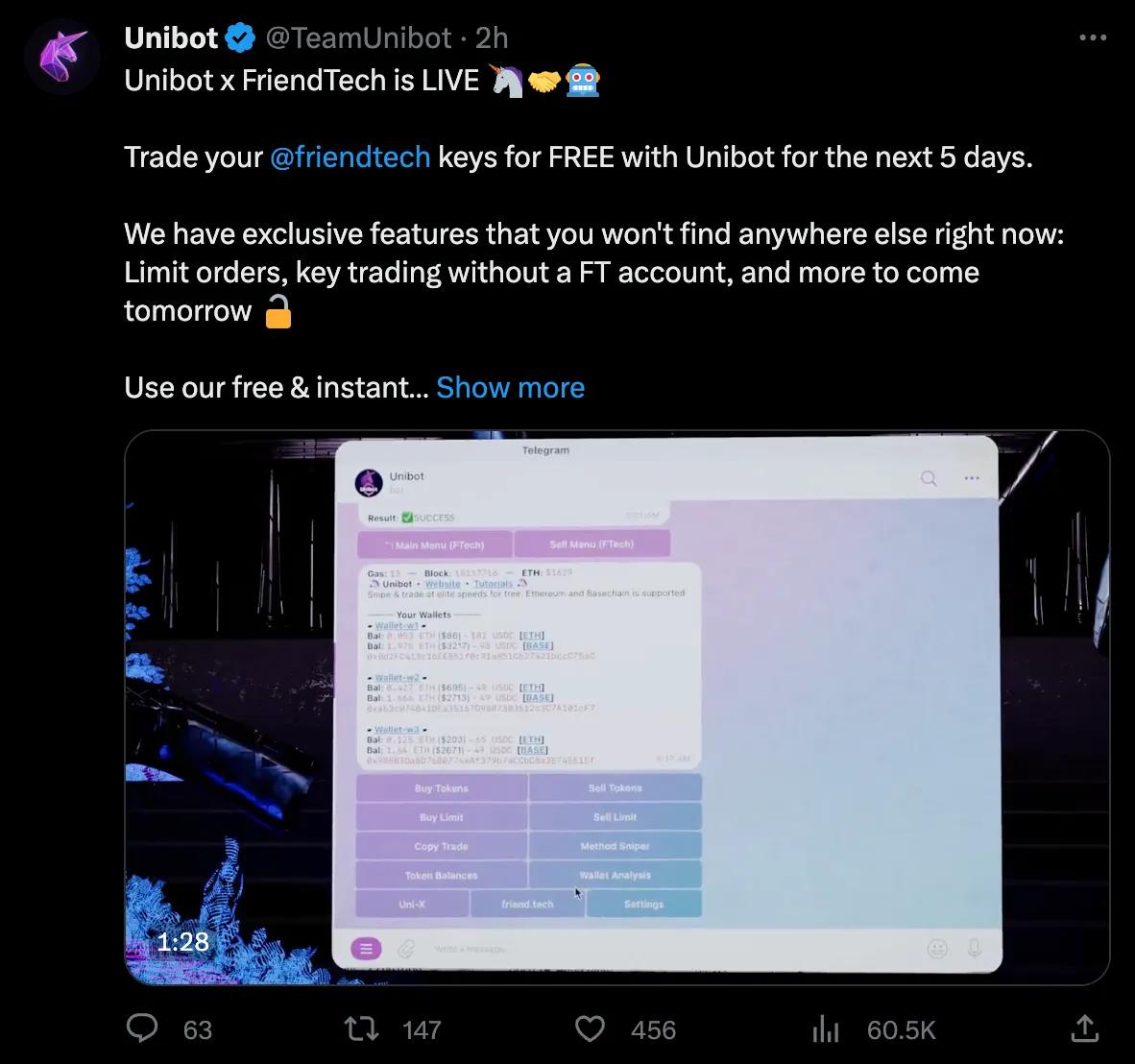

Unibot

Since sniping bots are already in the game, you might want to try one to stay competitive.

Meowl

If you dislike Telegram, Meowl recently added FT integration into their Discord bot.

I understand the current skepticism toward Friend.Tech, but you just need to use your imagination to envision what it could become. Most apps in this space lack long-term vision—FT might be no exception, but it has a strong chance of becoming a gateway for users who don’t care about crypto at all.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News