In-Depth Analysis of TrueUSD (TUSD)'s Key Role in the crvUSD Ecosystem and Risk Assessment

TechFlow Selected TechFlow Selected

In-Depth Analysis of TrueUSD (TUSD)'s Key Role in the crvUSD Ecosystem and Risk Assessment

The issuance of stablecoins requires a more transparent system to ensure security.

Author: LLAMARISK

Translation: Block unicorn

Relationship with Curve

TrueUSD (TUSD) plays a significant role in crvUSD as one of the Pegkeeper pools (crvUSD/TUSD), alongside USDC, USDT, and USDP. Pegkeepers algorithmically maintain crvUSD’s $1 peg by minting or burning crvUSD tokens based on market conditions, effectively backing the outstanding crvUSD supply with part of their paired Pegkeeper assets.

Pegkeepers enforce balance within each Pegkeeper pool, so if the pegged value of a Pegkeeper asset falls below $1, excessive crvUSD may enter circulation, causing crvUSD to de-peg. Curve intends to launch an improved version of Pegkeeper that will check token prices against a composite of other tokens. This would offer better protection by preventing crvUSD deposits into de-pegging Pegkeeper pools. Currently, crvUSD's stability relies heavily on strong confidence that its Pegkeeper pairs are robust and that the stablecoins involved are low-risk.

Within the context of serving as a crvUSD Pegkeeper asset, there are notable criticisms regarding TUSD’s transparency policies, which merit particular emphasis. TUSD lacks transparency in several areas, including custodial partners, reserve management, verification, on-chain operations, and ownership structure. This report will cover the most concerning issues—particularly those surrounding the status of TUSD’s reserves—that should inform DAO voters when determining whether action is needed to limit crvUSD’s exposure to TUSD.

Introduction to TUSD

Issuer and Custodian

At a high level, TUSD is a fiat-collateralized custodial stablecoin. Designed to maintain a 1:1 peg with the U.S. dollar, TUSD aims to provide stability amid volatile crypto markets. TUSD was initially issued by TrueCoin, LLC (a subsidiary of Archblock, Inc.), but ownership transferred to Techteryx on December 15, 2020.

According to TUSD representatives, Techteryx is described as an Asian holding company with operations in Hong Kong, Singapore, Guangzhou, Shenzhen, and Beijing, spanning traditional real estate, entertainment, environmental, and information technology sectors.

However, contrary to its self-description as an Asian holding company, Techteryx Ltd. appears on the British Virgin Islands (BVI) Financial Services Commission registry. Publicly available information about Techteryx is extremely limited, raising speculation about the ultimate beneficial ownership of both the company and TUSD.

As of July 13, 2023, Techteryx has fully assumed management of all offshore operations and services related to TUSD, including minting, redemption, customer registration, compliance, and oversight of banking and trust relationships.

TUSD has three custodial partners, described in audit reports as a Hong Kong custodian, a Swiss custodian, and a Bahamas custodian (audit reports can be downloaded from tusd.io).

The reserve composition is not specifically disclosed, but described as: U.S. dollar cash, cash equivalents, and short-term, highly liquid investments of sufficient credit quality that can be readily converted into known amounts of cash. The Hong Kong custodian also invests in other instruments to generate yield, with cash equivalents and other instruments recorded at cost in all cases.

TUSD’s primary revenue source is interest earned on the fiat reserves held as collateral. Income generated from these activities helps cover operational costs for maintaining the stablecoin infrastructure, regulatory compliance, and supporting TUSD’s growth and development.

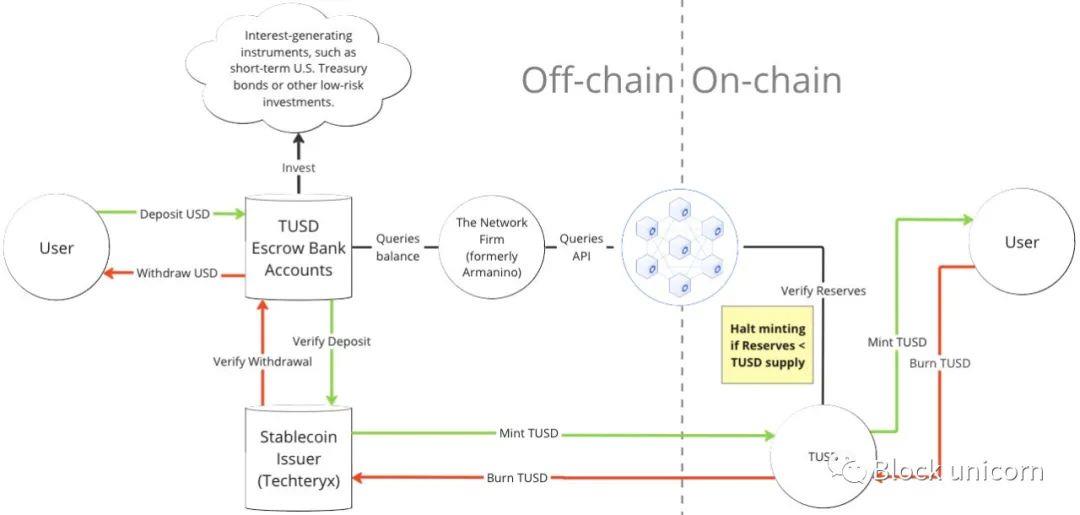

Minting / Redemption Process

TUSD’s system architecture is illustrated as follows:

Users wishing to mint TUSD must have an account at https://tusd.io/ and undergo KYC/AML checks. Then, users wire U.S. dollars to designated bank accounts managed by trusted partners. Techteryx emphasizes that fund management is entirely handled by its custodians, and the issuer never has access to user funds.

TUSD achieves real-time attestation through collaboration with The Network Firm LLP and Chainlink Proof of Reserve (PoR). TUSD can only be minted when the total TUSD supply plus newly minted TUSD is less than the reserves reported by Chainlink (provided by The Network Firm). Deposits confirmed via this minting check are then tokenized, and the corresponding amount of TUSD is delivered to the user’s designated receiving wallet.

Conversely, when users wish to redeem their TUSD for U.S. dollars, they first pass KYC/AML checks and specify their Ethereum and bank wire transfer addresses, initiating the redemption process with the stablecoin issuer. TUSD tokens are burned by sending them to the TUSD smart contract, and the corresponding U.S. dollar amount is transferred back to the user’s bank account.

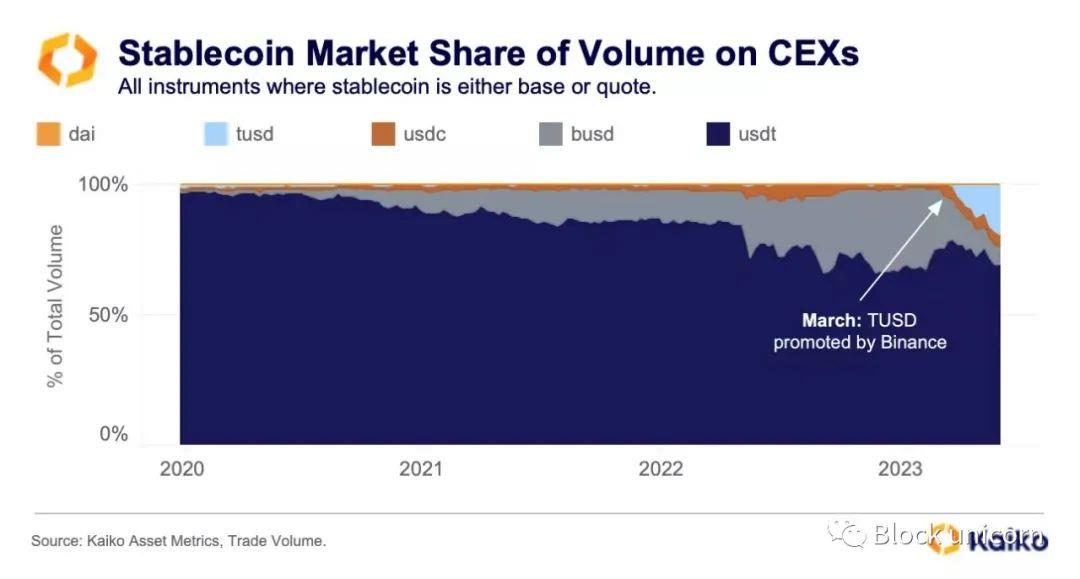

March 2023 Expansion of TUSD

Until March 2023, TUSD was a relatively small stablecoin with limited trading activity, accounting for less than 1% of the overall stablecoin market share. However, Binance decided to adopt TUSD as the successor to BUSD and subsequently promoted the BTC-TUSD trading pair with zero trading fees, significantly boosting its visibility and trading volume. Its market share rapidly expanded from under 1% to 19% within just a few months.

Two large transactions, each worth $1 billion, suddenly emerged from the same address and were sent directly to Binance exchange—these occurred on March 12 and June 16 (data date in chart below: June 27).

The rapid rise of TUSD may be linked to Binance’s zero-fee trading promotion and general platform-wide promotion of TUSD, announced by Binance on June 21. Observers may also note that TUSD’s unusual growth trend coincided with the period just before the closure of its Prime Trust custodial partner in mid-June.

Following the New York Department of Financial Services (NYDFS) order for Paxos to cease issuance of its BUSD stablecoin, Binance shifted support to TUSD. This move stemmed from unresolved regulatory issues between Paxos and Binance over BUSD issuance. Binance’s decision appears aimed at maintaining market share in the stablecoin space and reducing reliance on a single stablecoin. This push elevated Binance to become the largest holder of TUSD. Notably, the majority of TUSD’s trading volume currently centers around the BTC-TUSD trading pair on Binance.

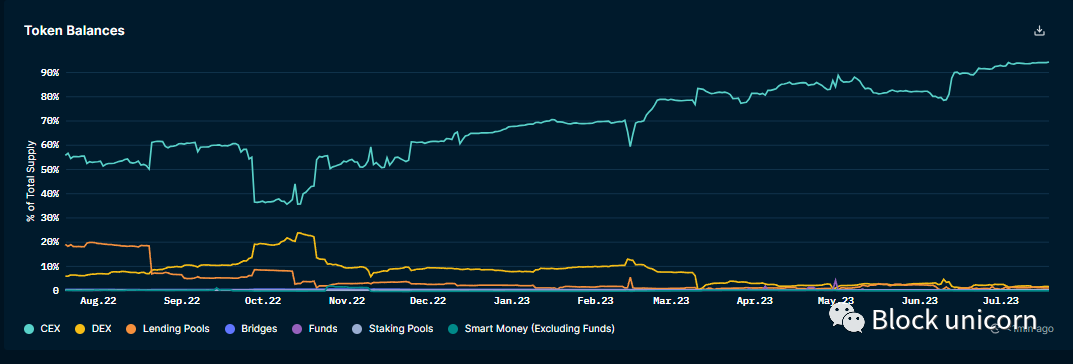

Token Distribution

According to Nansen data from July 19, the vast majority of TUSD supply is held on centralized exchanges (CEX), with 94% of token supply associated with CEX addresses. As shown below, the overwhelming majority of TUSD is actually held on Binance.

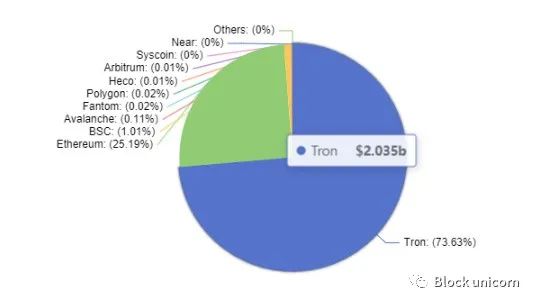

At the time of writing, the majority of TUSD token supply resides on TRON (73.56%), valued at approximately $2.035 billion. TUSD’s official website promotes its availability on TRON, Ethereum, Avalanche, Binance BNB Beacon Chain (BNB), and Binance BNB Smart Chain (BSC), incorporating token supplies across these chains into its attestation reports (chart below uses data from DeFiLlama dated July 19).

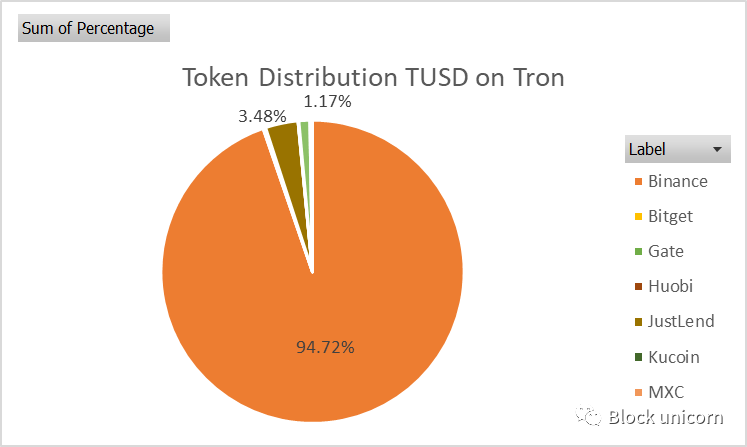

Distribution – TUSD on TRON

On TRON, the vast majority of TUSD is held by Binance (94.7%), with smaller portions on the DeFi lending platform JustLend (3.5%) and Gate.io (1.2%).

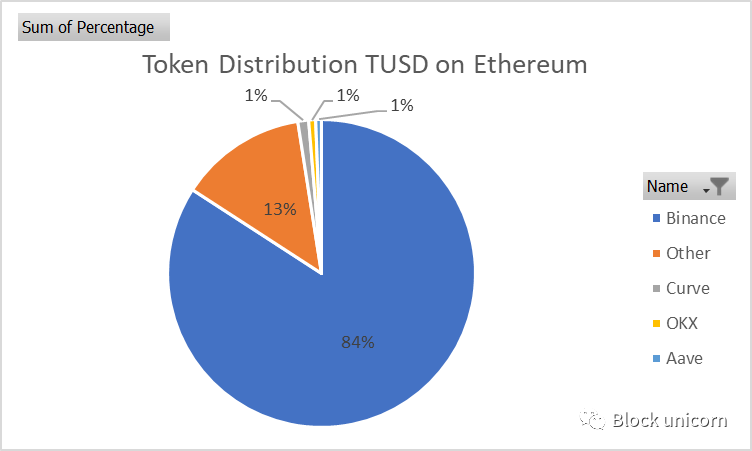

Distribution – TUSD on Ethereum

On Ethereum, TUSD token holdings are heavily skewed toward Binance, which holds 83.53% of the total supply. Smaller shares are held by Curve, OKX, and Aave at 1.12%, 0.73%, and 0.60%, respectively. The Curve crvUSD/TUSD Pegkeeper pool holds more TUSD tokens than any other contract on Ethereum.

crvUSD Pegkeeper and De-Peg Risk

-

TUSD/crvUSD Pool Contract

-

TUSD Pegkeeper Contract

-

AggregatorStablePrice Contract

Pegkeepers stabilize crvUSD’s peg by algorithmically supplying and withdrawing crvUSD to designated Pegkeeper pools. Currently, there are four pools: crvUSD/USDT, crvUSD/USDC, crvUSD/USDP, and crvUSD/TUSD. Each Pegkeeper is assigned a maximum debt it can supply to its respective pool. Currently, each Pegkeeper has a maximum debt of 25 million crvUSD, with a total maximum debt of 100 million crvUSD across all Pegkeepers.

The AggregatorStablePrice contract is critical to Pegkeepers, as it aggregates crvUSD’s price from at least three sources (currently the four Pegkeeper pools). Pegkeepers only supply crvUSD when the aggregated crvUSD price exceeds $1.

Using TUSD as an example, the following conditions must be met for Pegkeepers to supply crvUSD:

-

More than 15 minutes have passed since the last update.

-

The TUSD balance in the pool exceeds the crvUSD balance.

-

The crvUSD price referenced by the aggregator exceeds $1.

-

If conditions are met, an amount of crvUSD equal to 1/5 of the balance difference is supplied.

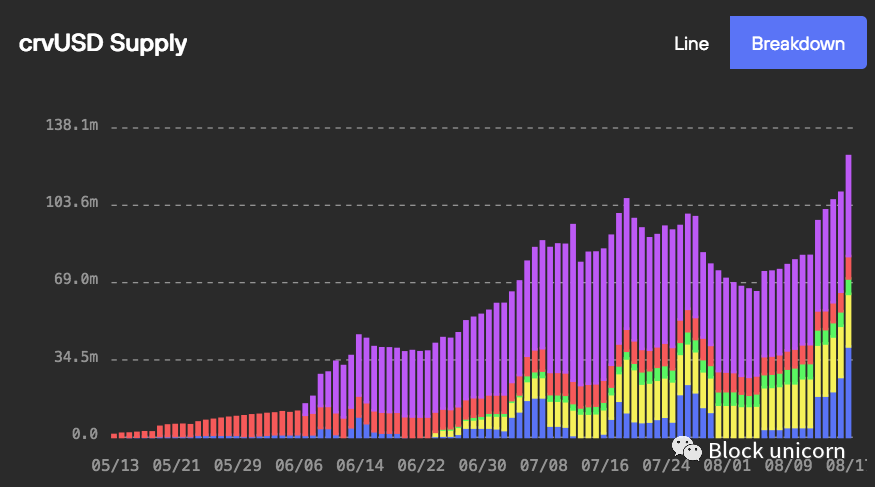

The chart below shows crvUSD supply over time by source. The blue bars represent crvUSD supplied by Pegkeepers, peaking at 40.6 million crvUSD (40.6% utilization) in mid-August. The recent increase in Pegkeeper utilization coincided with a sharp decline in crypto markets, increasing demand for crvUSD. As of August 18, total crvUSD supply was 125.5 million, with 85 million borrowed from collateral. This corresponds to 32.27% supplied by Pegkeepers and 67.73% borrowed from collateral.

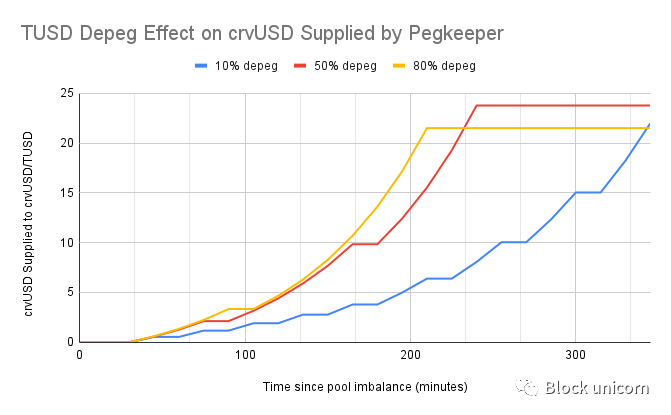

Any Pegkeeper asset (e.g., TUSD) losing its peg—either permanently or for an extended period—would have adverse consequences. Because the aggregator checks pool balances to determine crvUSD’s price, it could incorrectly quote crvUSD above $1 during a Pegkeeper asset de-peg. This would allow Pegkeepers to supply crvUSD up to their maximum debt limit. The chart below simulates how quickly Pegkeepers might supply crvUSD under varying degrees of de-peg severity:

These data were collected by simulating de-peg scenarios in Brownie using pool state data from August 8. Regardless of de-peg severity, nearly all available Pegkeeper debt would be introduced within a 4–5 hour de-peg event.

It should be noted that these figures are isolated; in reality, liquidity providers across other crvUSD pools would likely reduce their crvUSD exposure, leading to a de-peg proportional to the unsupported crvUSD entering circulation. This de-peg would lower the price quoted by AggregatorStablePrice, limiting additional Pegkeeper crvUSD inflows and allowing the DAO to take mitigating actions. The crvUSD supplied by the de-pegged Pegkeeper pool would become bad debt for the protocol (assuming the de-peg is permanent).

crvUSD depends not only on its Pegkeeper pools for stability but also for ensuring ongoing solvency. Therefore, it is crucial to assess the protocol’s exposure to potential Pegkeeper debt (i.e., maximum debt) relative to total crvUSD supply, while considering confidence in each Pegkeeper asset’s peg.

Criticisms regarding TUSD transparency issues:

1. Opaque reserve management: TUSD provides significantly less transparency regarding its custodial partners and reserve composition compared to competitors.

2. Opaque verification: TUSD provides relatively little detail in its attestations, calling into question the effectiveness of its proof-of-reserve system and potentially giving users a false sense of security.

Criticism 1: Opaque Reserve Management

Vague Handling of Reserve Accounts

TUSD’s attestations do not specifically name its reserve accounts, instead generally describing reserves as held at a Hong Kong custodian (previously disclosed as First Digital Trust), a Bahamas custodian (previously disclosed as Capital Union Bank), and a Swiss custodian.

As significant portions of TUSD’s reserves have moved to offshore entities, the custodial account structure has become increasingly opaque. TokenInsight reported on March 16, 2023, that Archblock, the former operator of TrueUSD, transferred $1 billion in the token’s reserves to Capital Union Bank in the Bahamas due to deteriorating banking conditions for U.S. crypto businesses. Located in Lyford Cay, Nassau, Capital Union Bank is an independent private banking institution regulated by the Central Bank of The Bahamas and the Securities Commission of The Bahamas.

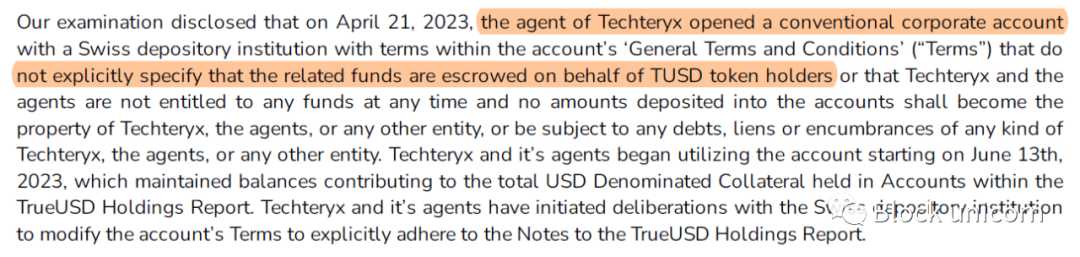

Additionally, a recent addition to the attestation indicates that Techteryx opened a corporate account at a Swiss custodian on April 21. The terms disclosed for this account do not clearly provide key protections for TUSD holders:

Funds in the account are held in trust for TUSD token holders.

The agent has no right to use funds in the account at any time.

Any amount deposited into the account does not become property of Techteryx, its agents, or any other entity.

Any amount deposited into the account is not subject to claims, liens, or encumbrances from debts owed by Techteryx, its agents, or any other entity.

Excerpt from the attestation:

This recently added account further highlights the lack of clarity regarding reserves held by Techteryx’s partners and the separation between issuer and user funds. Such a setup is highly susceptible to commingling customer deposits or misuse of corporate account funds.

Regarding assets held by unnamed custodians, the portfolio backing TUSD is disclosed in general terms as containing: U.S. dollar cash, cash equivalents, and short-term, highly liquid investments of sufficient credit quality that can be readily converted into known amounts of cash. The Hong Kong custodian also invests in other instruments to generate yield.

No further details are provided about portfolio asset balances or amounts held with each custodian beyond this general description. The Hong Kong account uses the vague phrase "other instruments." The risk profile of assets in this account is not clearly indicated, and because the attestation uses "cost" accounting, these investments may have experienced significant depreciation without being reflected in the attestation.

Readers are encouraged to compare TUSD’s attestation (available on TUSD’s website) with the latest attestations from major competitors USDC (June 2023), USDT (June 2023), and USDP (June 2023). In contrast, these issuers disclose significantly more information about custodians and reserve portfolios.

Market Panic in June 2023: Collapse of Prime Trust

Prime Trust was a Nevada-chartered trust company offering B2B custody, escrow, compliance, fiat processing, trading software, and other financial services. TUSD maintained a continuous partnership with Prime Trust starting in August 2019, when the collaboration was first announced. It used Prime Trust for 24/7 fiat transfers for its stablecoin products, including TrueUSD (TUSD), TrueGBP (TGBP), TrueAUD (TAUD), and TrueCAD (TCAD).

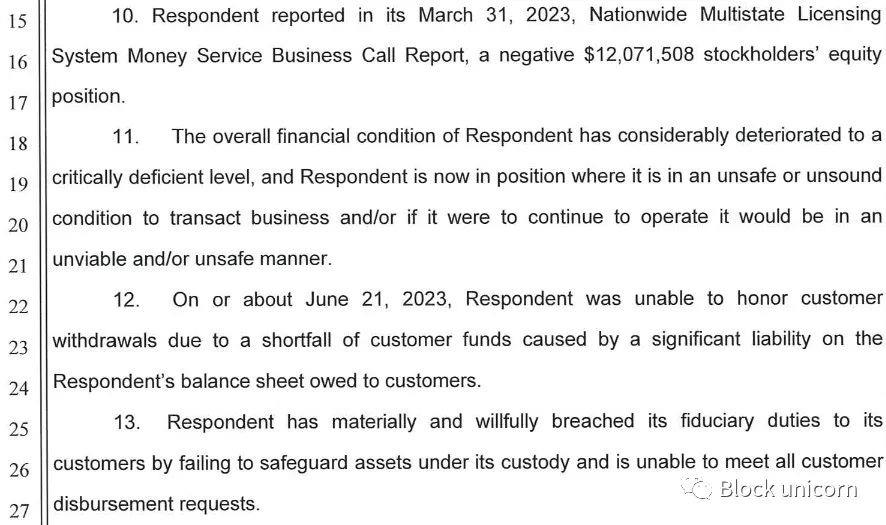

On June 21, 2023, the Nevada Department of Business and Industry, Financial Institutions Division (FID), ordered Prime Trust to cease all operations due to violations of state regulations. The company’s financial condition was found to be severely deficient, rendering it unable to fulfill customer withdrawals or protect assets under custody.

In 2020, an upgrade to its wallet management system reportedly caused issues, leading to a discovery in December 2021 that Prime Trust had rendered funds in its legacy wallets inaccessible. Allegedly, Prime Trust began using other users’ deposits to purchase cryptocurrency to meet withdrawal requests. The Nevada FID found that the custodian owed customers $85 million in fiat but had only $3 million on hand. It stated that Prime Trust had negative shareholder equity of $12 million and was effectively insolvent.

TUSD Exposure to Prime Trust Risk

Prior to the Nevada financial regulator’s shutdown order, rumors circulated about TUSD being undercollateralized. On June 9, TUSD announced it would suspend minting via Prime Trust until further notice (other minting/redemption services remained operational). This triggered a relatively brief market panic.

Subsequently, TUSD sharply de-pegged on Binance US, dropping to a low of $0.80. Notably, this was not a broad market de-peg event. Binance US faced its own challenges due to legal battles with the SEC, difficulties finding banking partners, and exposure to Prime Trust risks, threatening reliable deposits and withdrawals on the exchange.

After the shutdown order, TUSD initially claimed on June 22 that it had no exposure to Prime Trust. However, in its TUSD Funds Report on June 28, a $26,000 exposure to TUSD appeared. Although negligible, users continued reporting inability to mint/redeem TUSD, fueling ongoing market panic as participants remained wary of potential undisclosed exposures.

According to TUSD representatives, this $26,000 originated from random users’ funds held at Prime Trust, which auditors included on TUSD’s balance sheet, emphasizing that this amount was not actually related to TUSD.

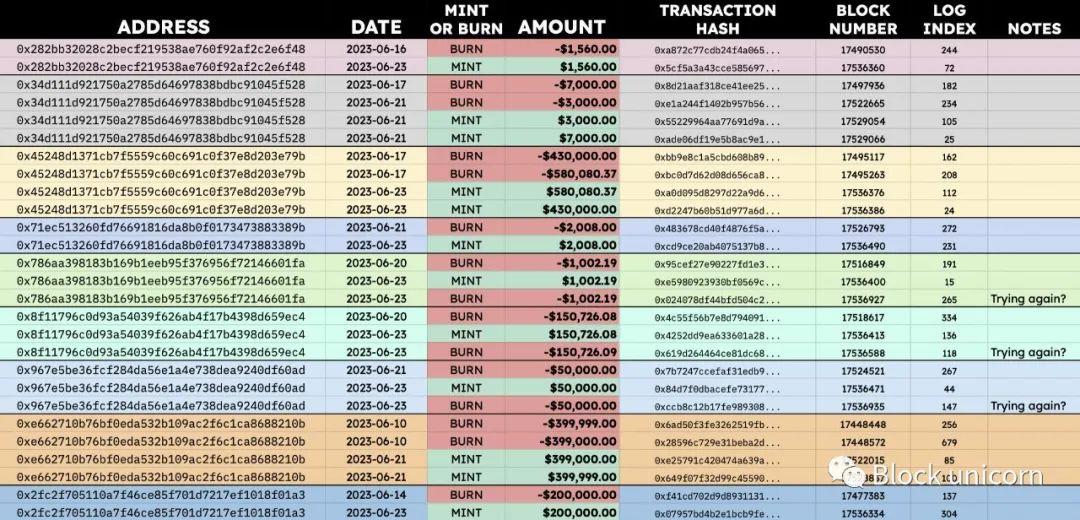

Reports of Failed Redemptions

Around mid-June, when issues with Prime Trust surfaced, reports began emerging that multiple users appeared unable to redeem TUSD, with their TUSD being returned to their wallets instead. This contradicted TUSD’s announcement on June 9, which claimed that despite the suspension of minting via Prime Trust, all other custodial partners remained intact and minting/redemption services were uninterrupted.

Prime Trust was shut down on June 21, aligning with the timing of redemption failure reports. Blockchain analytics firm @Chainargos and @willmorriss4, claiming to be a former TUSD employee, provided on-chain transaction records of failed redemption attempts between June 10 and June 23:

TUSD representatives responded that these transactions were user attempts to send funds to Prime Trust despite the public announcement that minting/redemption via Prime Trust had been suspended. They further emphasized that anyone could still redeem TUSD 24/7 without restriction through other custodial partners.

Criticism 2: Opaque Verification

LedgerLens System

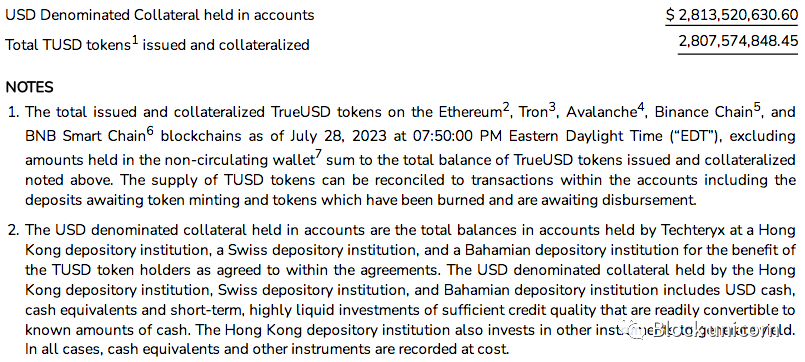

Real-time attestations are provided by The Network Firm LLP through their LedgerLens system, which delivers real-time reserve data. The service queries the total TUSD supply across all chains (ETH, AVAX, BNB, TRON, BSC) and the aggregate account balances of Techteryx’s custodial partners across multiple custodians. Below is an attestation report from July 28:

Ripcord is an alert system embedded within the attestation service that defines blocking conditions for automatic attestation updates. It detects system issues, as external APIs used for attestations may occasionally fail due to maintenance, downtime, or inaccuracies.

There are four types of Ripcord (emphasis on “Balance” Ripcord):

1. Management: During the previous reporting interval, management made unacknowledged statements, declarations, or failed to acknowledge participation in protocol terms.

2. Integration: During the previous reporting interval, a smart contract call returned an error, and excluding this error would trigger the Balance Ripcord (see below).

3. Pricing: Irrelevant for stablecoin attestations. Indicates API errors or non-responsiveness when applying USD (or other fiat-denominated) values from pricing sources to collateral assets.

4. Balance: During the previous reporting interval, third-party systems or accounts responded with errors or failed to respond, resulting in liabilities exceeding assets. This could stem from normal operations, such as customers opening bank accounts not yet integrated, or from actual imbalances between liabilities and assets.

As the situation with Prime Trust unfolded, the “Management” Ripcord was triggered on June 13, followed by the “Balance” Ripcord on June 20. TrueUSD clarified on June 22 that this trigger resulted from delays in API integration with a new banking partner (presumably the unnamed “Swiss custodian”), and attestations had since resumed normally. A TUSD representative also noted they are the only stablecoin with real-time attestation, though banks’ APIs cannot reflect amounts in real time.

Earlier criticism in March 2023 pointed out that attestations for other stablecoin products—including TrueAUD, TrueHKD, TrueCAD, and TrueGBP—had become increasingly outdated, raising transparency concerns. At the time of writing, these stablecoins’ attestations were last updated on June 22, and the “Management” Ripcord is currently triggered.

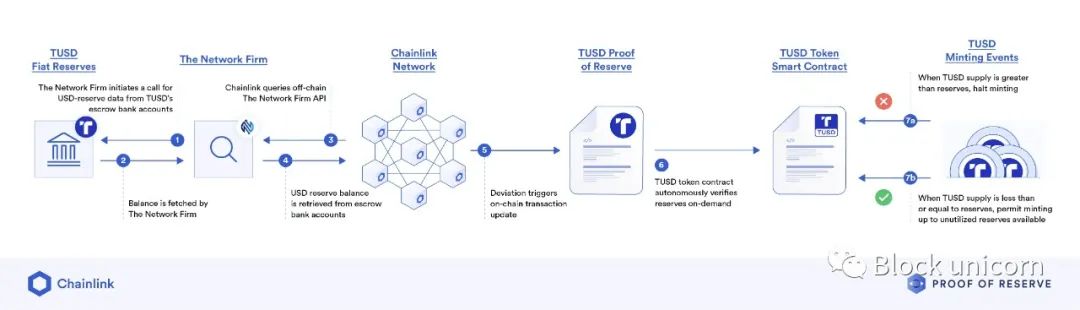

Introduction of Chainlink PoR Integration

TrueUSD uses Chainlink’s Proof of Reserve (PoR) technology to enhance TUSD’s transparency and reliability by regularly verifying full collateralization of the stablecoin.

As shown above, the minting and redemption processes depend on available reserves and involve the following steps:

1. Independent accounting firm The Network Firm uses its LedgerLens attestation service to request USD reserve data from TUSD’s custodial bank accounts.

2. Obtain USD reserve balance from custodial bank accounts.

3. Chainlink’s decentralized oracle network queries The Network Firm’s API off-chain.

4. Chainlink retrieves the USD reserve balance reported by The Network Firm’s API.

5. If discrepancies exist in account balances, on-chain transactions are executed to update the TUSD Proof of Reserve contract.

6. The TUSD token contract autonomously verifies reserves when needed.

7. TUSD minting availability depends on comparing reserves to TUSD supply:

-

If TUSD supply exceeds available reserves, minting of new TUSD tokens is halted to ensure the stablecoin remains fully collateralized.

-

If TUSD supply is less than or equal to reserves, minting is allowed up to the unused reserve amount, maintaining proper collateralization ratios.

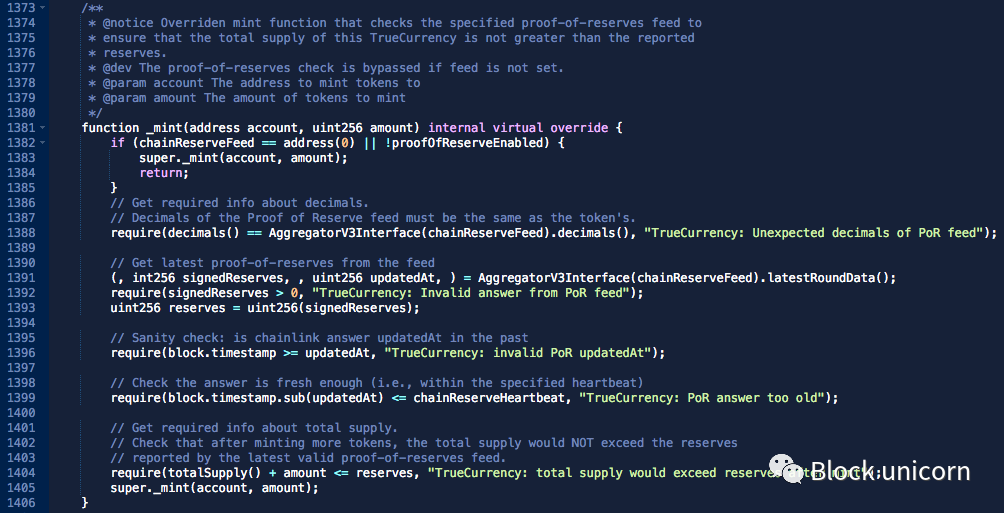

As shown below, TUSD’s _mint function checks whether the reserve value passed from chainReserveFeed is sufficient before allowing TUSD minting:

Integration with Chainlink is claimed to provide users with accurate and transparent information about the reserves backing TUSD, making it a more reliable form of collateral and payment method in DeFi.

Stablecoin Verification: Information Is Not Comprehensive Enough

TUSD’s reserve reports from The Network Firm via Chainlink’s PoR offer limited transparency and do not disclose specific details such as:

-

Full scope of corporate liabilities

-

Banking relationships

-

Composition of asset portfolio

-

Market value of reserves (reserves reported at “cost”)

This makes it difficult for users to fully assess the stability and legitimacy of the reserves.

The purpose of stablecoin verification is to prove that the entire stablecoin supply is fully redeemable. Proof of solvency can be achieved by ensuring both reserves and liabilities are fully accounted for.

Proof of Solvency = Proof of Reserves + Proof of Liabilities

While most of TUSD’s liabilities are visible on-chain (i.e., issued TUSD), there may be significant off-chain liabilities. Auditors of stablecoins, including The Network Firm (TNF), typically provide reserve snapshots that do not capture the full scope of corporate liabilities. Hidden or undisclosed liabilities could impact the availability and backing of the stablecoin, complicating definitive proof of solvency.

As previously mentioned, the custodians controlling TUSD’s reserves are only described in audits as the Hong Kong custodian, Bahamas custodian, and Swiss custodian. The portfolio backing TUSD is similarly vague, disclosed only as containing U.S. dollar cash, cash equivalents, and short-term, highly liquid investments of sufficient credit quality that can be easily converted into known amounts of cash (the Hong Kong custodian also invests in other yield-generating instruments).

Trust Assumptions Regarding The Network Firm LLP

According to disclosures in Chainlink’s PoR data source for TUSD, audit data is entirely dependent on The Network Firm LLP. The auditor’s credibility and independence have been questioned, particularly given The Network Firm’s association with Armanino, which faced scrutiny due to its prior business relationship with FTX US.

The Network Firm responded to questions about this association, calling it an “accidental or intentional misrepresentation,” and emphasized that The Network Firm is an independent accounting firm specializing in digital assets, distinct from Armanino. Many current team members were founding members of Armanino’s digital assets practice. After FTX’s collapse and controversy, Armanino decided to scale back audit services in the digital asset sector. The Network Firm LLP was established in October 2022, holds no equity in Armanino, and only one founding member worked on the 2021 financial statement audit of FTX US.

TUSD representatives responded that treating this association as malicious FUD is unfounded, as Armanino had a business relationship with FTX US, but the latter did not lose customer funds. Armanino also audits major crypto platforms like Kraken. Armanino expressed confidence in its work with FTX US, and aside from negative media coverage related to the association, there is no evidence that Armanino or The Network Firm failed in their duties or committed any wrongdoing.

A final note on PoR: While stablecoin attestations are far from perfect and require trust in auditors and issuers to provide accurate data and operate responsibly, they represent positive steps toward transparency and accountability. By voluntarily conducting and publishing attestations, TUSD demonstrates efforts to build trust among users and regulators, showing commitment to financial transparency and responsible practices.

On the other hand, some key information remains undisclosed—such as custodial partners, relative exposure to each institution, the asset portfolio backing TUSD, and corporate liabilities—all of which could impact TUSD’s backing. When such information is not public, users need to understand the trust assumptions involved, especially recognizing the limited utility of reserve proof systems like Chainlink PoR when much information remains undisclosed.

Risk Recommendations

TUSD has made significant efforts in building confidence in solvency through real-time attestations and on-chain proof of reserves. It stands out as the first dollar-backed stablecoin to programmatically implement minting restrictions based on off-chain reserves.

However, there are valid criticisms that Techteryx’s transparency policies are inadequate, as the issuer does not provide reasonable assurance regarding the stablecoin’s solvency. Compared to competitors, TUSD discloses very little about its reserve status. It does not disclose custodian names, balances per custodian, or detailed portfolio contents. TUSD is currently the only Pegkeeper that does not disclose such information (compare with latest attestations of USDC, USDT, and USDP).

The current Pegkeeper model could lead to crvUSD de-pegging or the protocol accumulating bad debt if a Pegkeeper asset de-pegges. Given the importance of Pegkeepers to crvUSD stability, these assets must undergo special scrutiny and meet minimum requirements. Generally, Pegkeeper candidates should satisfy the following conditions:

1. Sufficient confidence in the peg at technical, operational, and regulatory levels;

2. Candidates should complement the Pegkeeper asset basket by introducing diversity in issuers, custodians, and geographic jurisdictions.

To achieve this, candidates should be redeemable stablecoins with efficient arbitrage paths and compliant with regulations in their operating jurisdictions. Overall, the Pegkeeper asset basket should not be concentrated in a single jurisdiction or consist of white-labeled products from the same issuer and/or custodian (e.g., Paxos USDP and PYUSD).

We believe TUSD should not remain in the crvUSD Pegkeepers until upgrades are implemented and precautions taken to mitigate negative impacts from Pegkeeper asset de-pegging. Our reasoning is that, given Techteryx’s current transparency policies, we cannot have confidence in TUSD’s solvency or its peg. Reducing TUSD’s maximum debt as a Pegkeeper to zero would not significantly impact the overall situation (meaning other Pegkeepers could continue functioning and maintaining stability even if TUSD ceases to serve as one), as there are three other Pegkeepers with a combined maximum debt of $75 million. Historically, the highest Pegkeeper debt utilization for crvUSD since May has been $40.6 million (on August 18).

An argument for reducing—but not eliminating—maximum debt could be to preserve geographic diversity among Pegkeepers. Increasing the proportion of Pegkeeper assets based in the U.S. might increase exposure to U.S. stablecoin regulatory risks. If the DAO agrees with this reasoning, it is recommended to set TUSD Pegkeeper’s maximum debt at a conservative figure, such as $5 million.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News

![In-depth Analysis of Trade[XYZ]: How Were 92 Markets and 98% HIP-3 Trading Volume Established?](https://upload.techflowpost.com/upload/images/20260716/20260716061117965147.jpeg?x-oss-process=image/resize,p_50/quality,q_80)