Analyzing GNS: Perhaps the Most Complex DeFi Derivatives Protocol in History

TechFlow Selected TechFlow Selected

Analyzing GNS: Perhaps the Most Complex DeFi Derivatives Protocol in History

This article will provide a detailed introduction to GNS's mechanism, development history, and competitive advantages.

By CapitalismLab

Both the new versions of GMX and SNX Perp have drawn inspiration from one project—GNS. Since the Luna crisis last year, GNS has risen over 10x, with trading volume and fee revenue repeatedly hitting new highs, thanks to its continuous innovation in mechanism design. This article will detail GNS’s mechanisms, development history, and competitive advantages. Understanding GNS allows you to instantly grasp the inner workings of many DEX Perps.

This article is relatively complex; I recommend focusing on the key points I’ve extracted while reading.

GNS Mechanism

If you're unfamiliar with GNS, simply put, it's a decentralized perpetual futures platform:

Priced via oracles; LPs and traders are counter-parties.

LPs provide pure stablecoins, supporting forex/stocks/crypto trading.

Two-way funding rate: similar to CEX Perps, one side pays the other.

Alternatively, you can read my previous Chinese-language GNS encyclopedia entry. Except for content about LP (DAI Vault), much remains relevant.

We previously discussed how GMX uses a fully collateralized model—each $1 ETH long position in GLP is backed by $1 worth of spot ETH—enabling GMX to survive volatile bull markets. But how does GNS, whose underlying assets consist only of stablecoins, manage risk? Reference link

GNS implements three layers of risk control on both the trading and LP sides. The core principles are:

On-chain liquidity determines trading slippage, preventing price manipulation.

Asset volatility and long/short ratio determine holding costs, managing one-sided market exposure.

Net asset value model combined with liquidity adjustments and cash flow recycling builds robustness into the LP system.

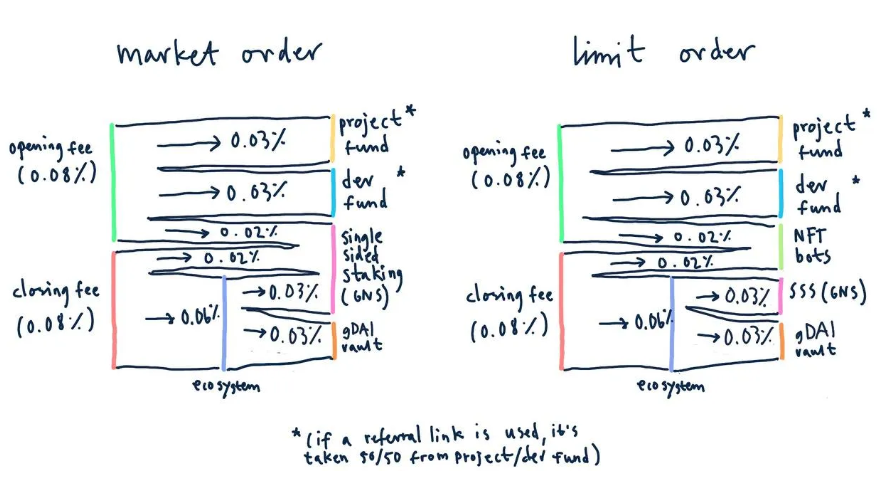

GNS employs three mechanisms—Spread, Rollover Fee, and Funding Fee—for trading-side risk management:

Spread: An additional opening fee. Larger positions and lower asset liquidity result in higher fees. Prevents price attacks and enables listing smaller-cap tokens.

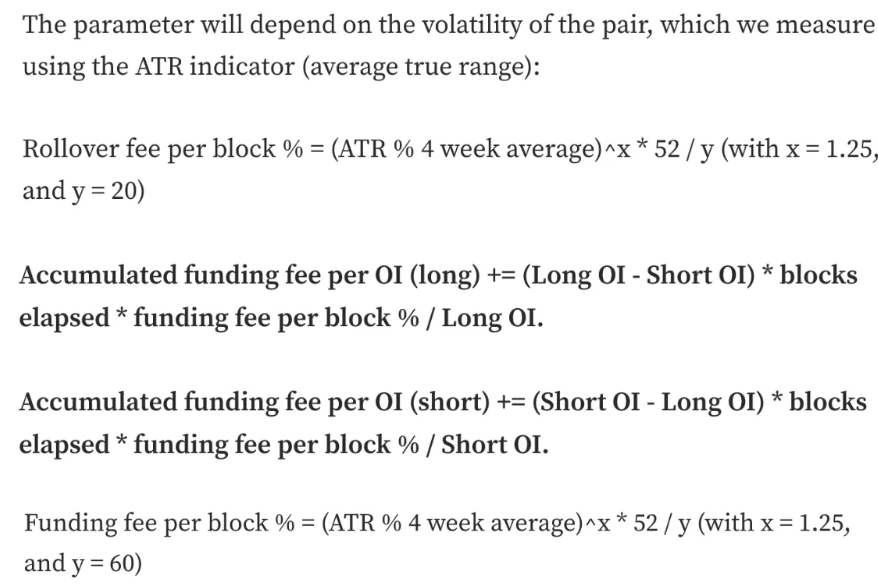

Rollover Fee: Priced based on spot volatility, controlling trader leverage and risk exposure.

Funding Fee: Based on the difference between long and short positions and spot volatility. When long/short > 1, longs pay shorts; otherwise vice versa. Balances long/short ratio and avoids excessive one-sided exposure.

See details: gTrade v6.1: In-depth

Spread refers to the extra slippage paid upon opening a position. For oracle-based pricing, this slippage should dynamically adjust according to the depth of the corresponding trading pair on external exchanges (CEX), ensuring that the cost of manipulating prices off-chain exceeds any potential profit on-chain. Thus, Spread is positively correlated with position size and on-chain open interest impact, and negatively correlated with off-chain spot liquidity depth. See formula below:

Rollover Fee and Funding Fee are calculated based on recent volatility. Both longs and shorts pay Rollover Fees, whereas Funding Fee is paid by one side to the other depending on the long/short ratio. Refer to the diagram below for exact formulas. During extreme bull runs, increased volatility and skewed long/short ratios cause longs to rapidly accumulate fees, compensating counterparty losses and rebalancing exposure. Of course, these also lead to non-trivial trading costs, which is why GNS lags behind GMX in terms of volume within crypto, where index asset LP models perform better.

Note that Rollover Fee applies only to collateral. For example, if you open a $10k position with $1k collateral, interest is charged only on the $1k. Meanwhile, Funding Fee applies to the full position size ($10k). Suppose the Funding Fee (s) = -0.0005% and Rollover Fee = 0.0043%. Then net fee = ($1k × 0.0043% − $10k × 0.0005%) / $10k = -0.00007%, meaning shorts actually earn interest at this moment.

On the LP side, gDAI operates under three mechanisms to ensure stability:

A NAV-based product similar to GLP, not principal-protected.

Fee revenue and trader PnL create a buffer layer for gDAI, protecting against price drops.

Incentivizes long-term staked capital, dynamically adjusts deposit/withdrawal timing to avoid liquidity crunches during extreme conditions.

The advantage of a NAV-based product is fair treatment for all stakers, sharing gains and losses equally under extreme scenarios. Older LP models claimed to be “principal-protected,” but when deficits occurred, the last ones out received nothing—exactly like FTX—and naturally triggered panic during crises.

The hardest concept to grasp here is the Buffer mechanism. Within GNS fee revenues, part is used to mint new GNS tokens paid to users, while the original DAI income flows into gDAI as an over-collateralization buffer. Trader profits and losses, under over-collateralized conditions, also feed into this buffer. As a result, although gDAI is nominally not principal-protected, its price rarely declines in practice—clearly demonstrating deep understanding of investor "loss aversion."

When over-collateralized, GNS also uses a portion of profits from trader losses to buy back GNS tokens, keeping the over-collateralization ratio fluctuating safely within bounds. Therefore, in the long run, GNS won't experience massive inflationary token issuance.

Long-term locked LPs receive discounts funded from this same buffer. The dynamic adjustment means withdrawals slow down as over-collateralization decreases, enhancing resilience. It might seem odd, but the rules are transparent and pre-disclosed.

Yes, you may not fully understand the paragraphs above—that’s normal. Otherwise, how could I call it the most sophisticated and complex protocol ever? If you really want to comprehend it, first read the original gDAI introduction: Introducing gToken Vaults, then revisit these sections. That should resolve much of your confusion.

Development History

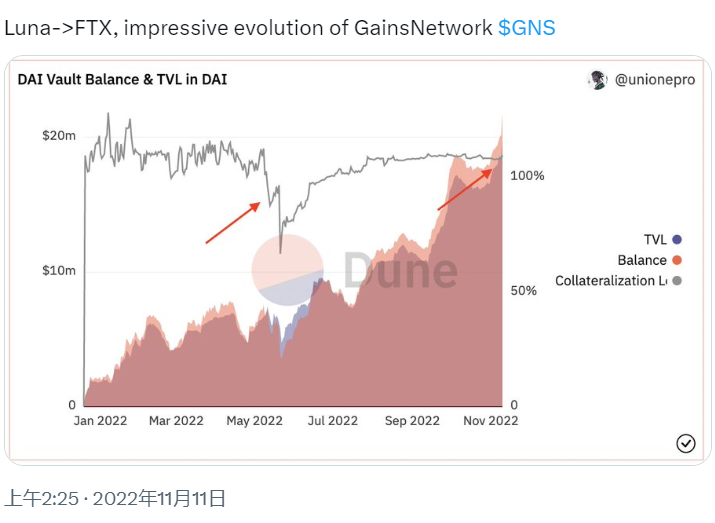

During the crash triggered by Luna, GNS’s LP fell into deficit, forcing them to sell GNS for DAI to cover the shortfall. Later, GNS implemented multiple improvements and performed well during the panic caused by FTX’s collapse.

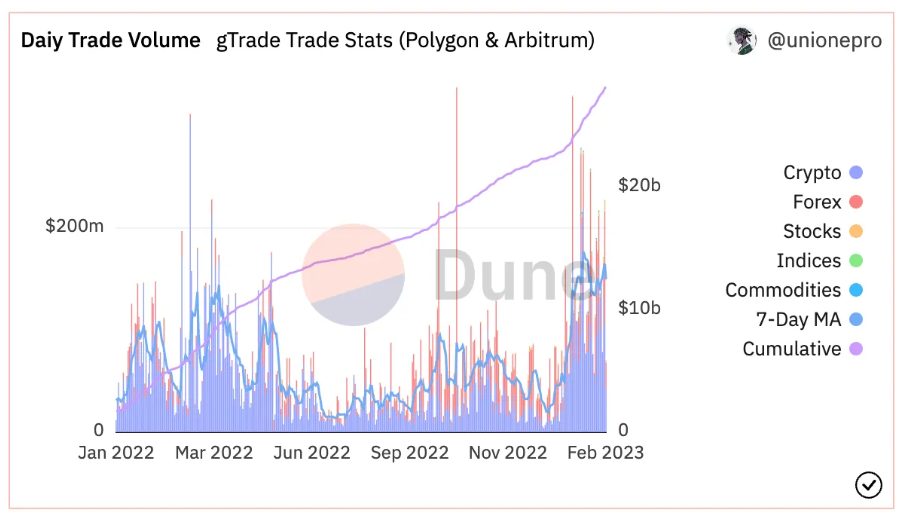

Just six months after the crisis, all three risk controls described earlier were fully implemented, restoring normal operations. By September, GNS began capturing attention due to surging demand for foreign exchange pairs amid sharp depreciation against the dollar, bringing it back into public view. In early December, gDAI limits were raised, and by month-end, deployment onto Arbitrum catalyzed explosive growth in both token price and business metrics at the start of this year. A highly efficient team enabled GNS’s continuous evolution, giving rise to this phoenix-like resurgence.

Competitive Advantages

Its core strength lies in providing a high-quality trading experience for forex and stock derivatives through intricate risk management mechanisms—unmatched in these asset classes—allowing its product to stand firm. Meanwhile, features like two-way funding rates differentiate it from GMX, enabling successful capture of some crypto traders as well. Achieving this wouldn’t have been possible without GNS’s excellent team—the most valuable asset of this growing project.

The detailed breakdown of GNS fee distribution is shown below. Given that market orders account for approximately 70%, GNS staking rewards amount to roughly 0.07/0.16×70% + 0.03/0.16×70% = 36.25%, while gDAI share is about 0.03/0.16 = 18.75%. The portion paid to NFT Bots (execution bots) in limit orders corresponds to the amount flowing into the gDAI buffer mentioned earlier.

Indeed, GNS allocates an unusually low proportion of fees to LPs. How does it sustain this?

To prevent forking, GNS has undergone audits but hasn’t fully open-sourced its codebase.

As previously noted, its mechanism is extremely complex and difficult to copy—poor imitation risks failure.

Non-fully collateralized LP model enables high capital efficiency.

While GNS appears to allocate a large share of revenue to the team, most current projects—including UNI, Maker, and Lido—either cannot or barely cover team expenses with treasury income, requiring ongoing token sales. In contrast, GNS sustaining itself purely through revenue-sharing is actually quite impressive. After all, you can't expect every team to operate like GMX, essentially functioning as a charity.

Conclusion

By now, you likely feel some awe. Indeed, DEX Perps are far more complex than the simplistic notion of traders and LPs being mere counterparties. Only when GMX introduced a low-risk, fully collateralized index asset model—combined with meticulous execution—did we finally see a usable product emerge. Yet, to trade off-chain assets like forex and stocks and expand the market further, synthetic asset models like GNS are essential. It’s only after such iterations that we finally see hope. Hats off to the builders.

GNS also has a referral program, e.g.: gains.trade/referred?by=pokemon. However, applicants must have at least 1,000 Twitter or YouTube followers and go through evaluation and approval. Contact me if interested.

More GNS updates and discussions:

GNS Chinese Twitter: twitter.com/gainsnetworkcn

Official GNS Chinese community: t.me/GNSChinese

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News