Zhipu AI Through a Foreigner's Eyes: Free Models, Massive Losses, Why Did Its Market Cap Once Surpass Meituan's?

TechFlow Selected TechFlow Selected

Zhipu AI Through a Foreigner's Eyes: Free Models, Massive Losses, Why Did Its Market Cap Once Surpass Meituan's?

Tsinghua lineage, state-owned capital backing, 73.7% of revenue from private deployments for state-owned enterprises—this is what Zhipu is truly selling.

Author: Robonaissance

Compiled by: TechFlow

TechFlow Editor's Note: Zhipu AI listed on the Hong Kong stock market and rose 25 times in half a year, with a market cap once exceeding Meituan, but its 2025 revenue was 724 million renminbi, with a loss of 4.72 billion, and its strongest model GLM-5.2 is still free to download under the MIT open source license. This is not the market going crazy, but pricing scarcity, sovereignty, and a float small enough to be pushed. Tsinghua heritage, state-owned capital endorsement, 73.7% of revenue from on-premises deployment for state-owned enterprises—this is what Zhipu is truly selling.

On July 2, 2026, the stock price of the world's first listed AI laboratory plummeted nearly 17% in a single day. Six days later, on the morning of July 8, when the lock-up period expired and approximately 46 billion Hong Kong dollars worth of frozen shares were unlocked, the stock price instead rose 13%. Within 24 hours, the company issued 4 billion U.S. dollars in new shares amidst the rise.

Zhipu AI, named "Knowledge Graph Technology" in Hong Kong, was rated by Bloomberg as the most volatile stock in Asia. But volatility is not a side effect; volatility is the mechanism itself.

The underlying business is more magical than the K-line chart. In 2025, Zhipu's revenue was 724 million renminbi, approximately 105 million U.S. dollars. The loss was 4.72 billion renminbi, approximately 650 million U.S. dollars. R&D investment was 3.18 billion renminbi, 4.4 times the annual revenue. The flagship model GLM-5.2 uses the MIT open source license; anyone can download the weights, run inference themselves, fine-tune, and create commercial products without paying Zhipu a penny.

At the end of June, the market valued the company at 1 trillion Hong Kong dollars, approximately 128 billion U.S. dollars. Higher than Meituan—Meituan delivers food for hundreds of millions of people and actually makes money.

A simple interpretation is that the market has gone crazy. A more useful interpretation is that the market is pricing something real, and that something is not on the income statement. It is pricing scarcity, sovereignty, and a float small enough to be pushed. This is a story about these three, and also about when the world finally set a public price for a frontier AI laboratory and found that this price hardly reflects the laboratory itself.

Tsinghua Heritage

Zhipu did not start as a startup; it began as a university research group, and this difference explains most of the company's later form.

The Tsinghua University Knowledge Engineering Group, known internationally as THUDM, had been researching knowledge graphs and language models for years before they became popular. In 2019, two professors, Tang Jie and Li Juanzi, spun off this work to establish the company. The architecture they brought out is called GLM, General Language Model, which is both the company's technical identity and the source of its name.

This background brought two things, but only one is often written about.

The first is technology. In March 2023, when most Chinese AI companies had not yet released anything usable for developers, Zhipu released ChatGLM-6B, an open source dialogue model small enough to run inference on a single consumer-grade graphics card. It became one of the most downloaded models that year and was the first widely available Chinese instruction-tuned large language model. Enthusiasts fine-tuned it on laptops, university labs used it for courses, and enterprises took it apart to study the principles. The habit of releasing models for free existed from the beginning, for a reason that is not romantic at all: free release is how an academic spin-out gets noticed.

The second thing is trust, and trust later became the business itself. Zhipu became one of the "Six Little Dragons," that is, the batch of Chinese large model startups that emerged in the generative AI wave. Before listing, it assembled an unusually broad list of investors: Alibaba, Tencent, Ant Group, Meituan, Xiaomi, Hillhouse, Qiming Venture Partners, Chinese local government funds, and Saudi Aramco's Prosperity7 Ventures, totaling approximately 1.5 billion U.S. dollars. A Tsinghua spin-out with state-owned capital on the shareholder list means Chinese state-owned banks can procure with confidence, and no one on the procurement chain needs to defend this decision. This access is not a soft advantage. From the revenue structure, it is the entire commercial engine.

Zhipu has fewer than 900 people, about three-quarters of whom are researchers. The CEO is Zhang Peng, Tang Jie is the core scientist, and the Chairman is Liu Debing. For a company once valued by the market at more than Meituan, this is a very small building, full of scholars.

What Zhipu Actually Sells

In 2025, 534 million of Zhipu's 724 million revenue came from on-premises deployment, accounting for 73.7%.

This single number重构 the entire company.

On-premises deployment means Zhipu's engineers go to the customer's building, install the GLM model suite into the customer's own servers and intranet, and the data never leaves the local site. They fine-tune the model with customer data, integrate it with the customer's existing systems, and stay until it works. Then they go to the next customer and do it all over again.

Customers are Chinese state-owned enterprises, banks, and government agencies: these institutions cannot put sensitive data on someone else's cloud, nor will they buy foreign models at any price. For them, a model with Tsinghua heritage, state-owned investment, and domestic deployment is not one of several options, but the only option. This is what Tsinghua heritage exchanged for, converted into invoices.

The remaining 190 million renminbi, accounting for 26.3%, comes from cloud business: API, developer platforms, those parts that run like software. This block is growing rapidly, with revenue share rising from 15.5% in 2024, and gross margin climbing from 3.3% to 18.9%, because inference optimization and scale have pushed down the marginal cost per token.

But the shape of the company is determined by that 73.7%, and that shape has problems. Overall gross margin fell from 56.3% in 2024 to 41.0% in 2025. The gross margin for on-premises deployment itself fell from 66.0% to 48.8%. As this business grows, the gross margin is contracting, because growth means hiring more engineers to sit in more buildings. There is no version of on-premises deployment where serving the tenth customer is cheaper than the first. Labor has no cost curve, only headcount.

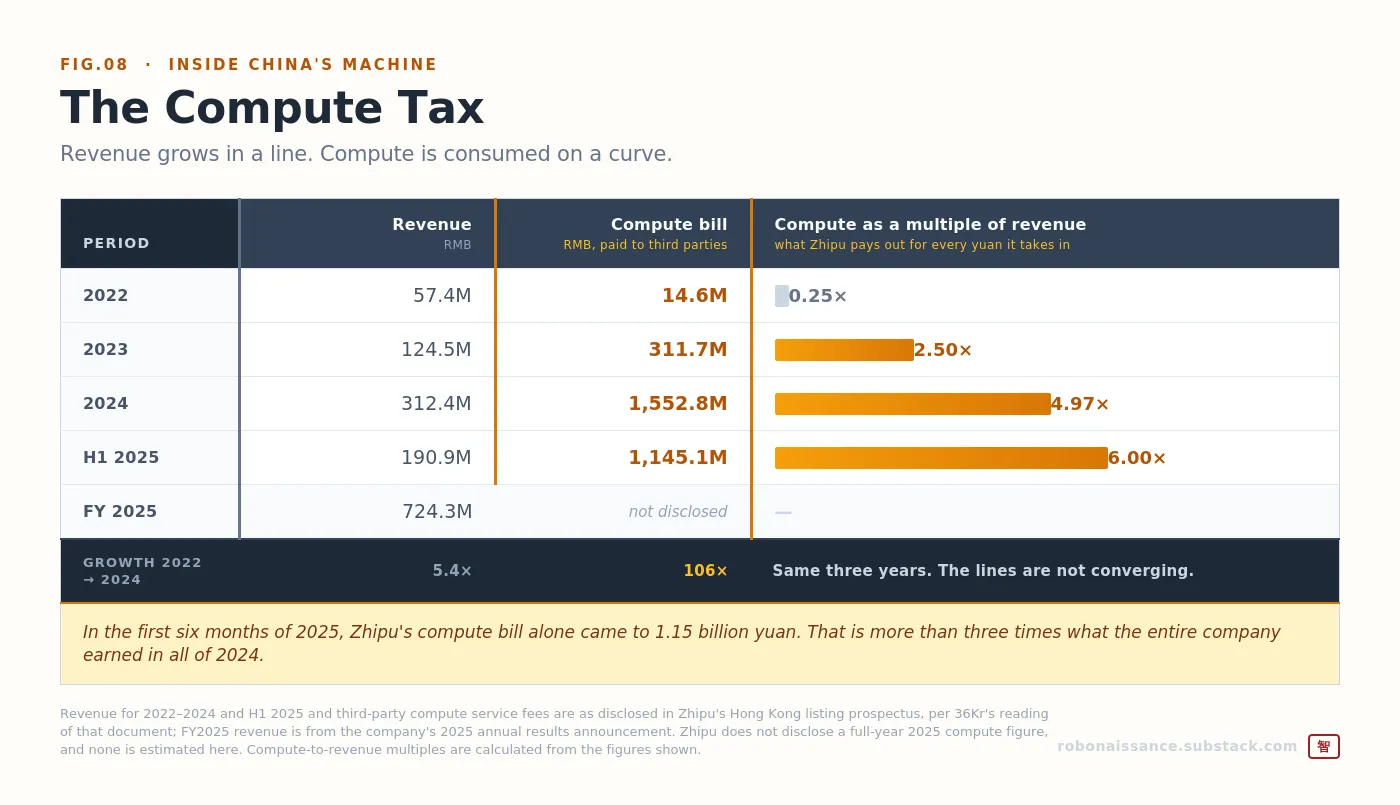

Growth is unquestionable. Zhipu's revenue was 57.4 million in 2022, 124.5 million in 2023, 312.4 million in 2024, and 724 million in 2025. This is a company that basically doubles every year; by revenue, Zhipu is China's largest independent large model developer. The trajectory is exactly what believers want to see.

The problem is the bill below, which decides everything. Zhipu's compute power fees paid to third parties were 14.6 million in 2022, 311.7 million in 2023, and 1.55 billion in 2024. In the first half of 2025 alone, according to prospectus figures, it was 1.15 billion.

Look at these two lines together. Between 2022 and 2024, Zhipu's revenue rose about 5 times. In those same three years, the compute bill rose more than 100 times. And in the first 6 months of 2025, compute alone cost more than the full year earnings of 2024.

These two lines are not converging.

Traditional software is written once and copied at zero cost, so software companies are the most profitable enterprises in history. Large models break this. It is written once, but every time someone uses it, you pay again. Revenue is linear growth, compute consumption is a curve, and as context windows lengthen and reasoning chains run longer, the curve is getting steeper. In 2025, for every 1 renminbi Zhipu earned, it had to pay chip manufacturers and cloud service providers far more than 1 renminbi.

Open Source Paradox

Zhipu's strongest model is free.

GLM-5.2, released in mid-June 2026, supports a context window of up to 1 million tokens and uses the MIT open source license. Download the weights, run on your own hardware, modify, make products, sell them, never pay Zhipu a penny. This is not a crippled community version; this is the flagship, the one the company uses to compete with American frontier models on the leaderboard.

The obvious question is, how can this become a business.

The answer is that open source is a distribution strategy Zhipu can afford precisely because its revenue does not come from selling model access. Revenue comes from selling deployment, integration, and services. Open source weights are marketing; on-premises contracts are the product. Free model release does not cannibalize revenue, because those paying customers did not intend to rent the model via API anyway. They intended to pay for someone to come to the building and install one.

What is exchanged for free is coverage. According to the company, over 4 million registered enterprise and developer users in 218 countries and regions have integrated its models, including nine of China's top ten internet companies. It exchanges for developer habits, and this is the raw material for API revenue. It also exchanges for a specific kind of credit: a model whose weights have been checked by the whole world, which a bank risk committee can approve without having to believe anyone's word.

The evidence that the strategy works is not download volume—download volume is easy to brush and cannot be monetized. The evidence is price. When Chinese peers were cutting prices to grab share, Zhipu raised API pricing by 83%, and demand still exceeded supply. The open platform's ARR reached 1.7 billion renminbi, approximately 240 million U.S. dollars, a 60-fold year-over-year increase, a number Zhang Peng gave at the company's first earnings call as a listed company.

A company that can raise prices in a price war shows it has something the price war cannot touch.

What changes the demand curve is the agent. The GLM-5 series is tuned for long-horizon software engineering; the model can work continuously for hundreds of iterations instead of stopping after answering one question. Zhipu's coding packages can be plugged into tools developers are already using. When a code agent runs autonomously for an hour, it consumes not the token amount of one query, but thousands of times that. Chairman Liu Debing's argument is that the resulting usage and price growth is persistent rather than peak, because it is driven by models becoming stronger and users making them do more work.

This is the one-sentence version of the bull case: agents are token furnaces, and Zhipu sells tokens.

Float Machine

But none of this explains a stock rising from 116.20 Hong Kong dollars in January to a盘中 high of 2,980 Hong Kong dollars on June 22, up 25 times in less than half a year. To explain this, you have to look at the pipeline.

Zhipu listed on January 8, 2026, with an issue price of 116.20 Hong Kong dollars, including over-allotment selling approximately 43 million shares, accounting for about 9.65% of share capital. Among them, 11 cornerstone investors took approximately 2.98 billion Hong Kong dollars, close to 70% of the issued shares. Cornerstone investors are large institutions pulled by Hong Kong issuers before listing: they promise to buy large blocks, guarantee allocation, and in exchange agree not to sell for 6 months. Retail investors oversubscribed the remaining portion by more than a thousand times.

Do some subtraction. The shares truly tradable on the first day were approximately 17.35 million shares. Less than 4% of the company.

A stock with a 4% float does not have the price of a normal stock. It has only a clearing level between a very small number of people willing to sell and any demand that appears, and the demand that appeared in the first half of 2026 was every investor on Earth who wanted exposure to Chinese frontier AI and had no listed pure-play target before January. Not DeepSeek, that is private. Not Moonshot AI, that is private. Not Huawei, that does not list nor sell models. Just Zhipu, and MiniMax listing one day later, that is the entire menu.

UBS put it bluntly: the valuation reflects a scarcity premium and the limited number of tradable shares. Bloomberg later observed that Zhipu stock is the most volatile in Asia, largely because the float is too small.

This machine ran for 6 months. Then July came, and the public ran it through once.

On July 2, as the cornerstone lock-up period approached, the stock fell nearly 17% in a single day; nothing happened, just the expectation that supply was coming. Closing at 1,754 Hong Kong dollars, market cap fell below 800 billion. Trading was too crowded, the float too thin; just 25.68 million shares about to unlock, accounting for 5.8% of the company, wiped out about one-sixth of the market cap in one day.

Then on July 7 the lock-up period expired, and cornerstone investors did not sell. Nearly 70% of them committed to continue holding. On July 8, the stock rose 13.35%, adding over 100 billion Hong Kong dollars in market cap in a single day, because not selling was interpreted as a vote of confidence.

Within 24 hours, Zhipu issued stock into this rise. It placed approximately 19.8 million new shares at 1,588 Hong Kong dollars per share, raising approximately 31.4 billion Hong Kong dollars, slightly over 4 billion U.S. dollars, one of the largest placements in Hong Kong this year, more than 6 times the size of Zhipu's own IPO. CICC BOCOM International acted as bookrunner. Shares were priced at a discount of about 13% to the previous close, the discount needed to let institutions take the plate at that level.

After the lock-up release, after the placement, only about 13.5% of Zhipu's issued shares were freely tradable.

The company did not fix the float; it monetized the float.

The control experiment ran the next day. MiniMax, another Chinese model developer listed in Hong Kong in January, faced its own lock-up expiration on July 9. The founder extended the lock-up period, strategic shareholders promised not to sell. It still fell more than 20% during the session.

The difference is not in the underlying architecture—the architecture is roughly the same. The difference is that MiniMax once tried to raise the price of its M3 model, but was rejected by the market and had to cut prices. While Zhipu raised prices 83%, and the market took it all. A thin float will amplify any existing market belief, but it will not create belief out of thin air. When belief exists, a thin float can turn a good quarter into a 25-fold rise. When belief does not exist, the same thin float will turn an unlock into a collapse.

Training Without Relying on NVIDIA

For anyone tracking the Chinese AI tech stack, the most important claim is one Zhipu made unobtrusively.

Reportedly, the open source flagship model GLM-5, released in February 2026, was trained and deployed on Chinese accelerators rather than NVIDIA hardware: Huawei's Ascend, and chips from Cambricon, Moore Threads, and Kunlun Xin. On the earnings call, Zhang Peng stated that since February, Zhipu has been accelerating the use of domestic chips to meet the sharp rise in compute demand. The R&D budget includes joint design work for domestic chip adaptation. The company built its own asynchronous reinforcement learning framework Slime, partly to allow the training pipeline to run on the hardware it is actually allowed to buy.

Zhipu chose this path less as an active choice than as being chosen. In January 2025, the U.S. Department of Commerce placed Beijing Zhipu Huazhang Technology and its subsidiaries on the Entity List, citing concerns that the company was helping advance China's military modernization through AI. Zhipu objected to this reasoning and stated it does not rely on American large model technology. However one views this determination, its practical effect is to limit access to American technology, turning domestic chips from a preference into a necessity.

The final product closes a loop running through this series. A frontier-level open source model, competitive in international programming benchmarks, trained to completion on Chinese chips.

Cambricon needs a customer with a large enough inference workload to make the domestic accelerator business a reality. Zhipu needs chips it is allowed to buy. Chips need models. Models need chips. Both need export controls to create a closed market where each is the other's best option. Tech stack forking is no longer a prediction, but a delivered product, complete with benchmark scores.

Sovereignty Trade

In mid-June 2026, Anthropic suspended access to its latest models Fable and Mythos to comply with U.S. Department of Commerce export control regulations. Access was restored on July 1.

During this window, Zhipu released GLM-5.2 and a message. The company stated on social media that frontier intelligence should not belong to only a few people, nor should it be withdrawn at any moment because of a few rules.

This statement is not entirely accurate. These models were suspended to comply with regulatory orders, not withdrawn on a whim by the company, and were restored within three weeks.

But this inaccuracy is not commercially important; understanding this is key. Buyers choosing on what basis to build their business will not go to evaluate the reasons why a model might be unavailable. Buyers evaluate the possibility itself. Zhipu never argued that American models are worse. GLM-5.2 ranked second on the Code Arena frontend leaderboard, second only to Anthropic's Claude Fable 5, and Zhipu did not pretend otherwise. The argument is narrower and harder to refute: American models can be turned off by someone who is not you, while a set of open source weights on your own server will not.

This is Cambricon's logic, moved up one layer on the tech stack.

Cambricon's chips are not the best chips. They are the chips Chinese buyers can actually get goods for; in a sanctioned market, availability is a form of performance. Zhipu's models are not the best models. They are models buyers can download, audit, deploy, and retain; in a market where frontier might be closed by foreign regulators, permanence is a form of performance.

In the chip field, good enough and available beats best but unavailable. In the weights field, models you can retain beat better models you might lose. The same trade happened twice at two different heights of the same tech stack.

Anthropic or Palantir

This leaves the valuation question, and valuation boils down to a classification problem.

The market prices Zhipu like pricing a frontier platform: a paradigm-setting company, with ecosystem premium and operating leverage that will eventually explode, today's losses are the entry fee for owning tomorrow's standard. This is the reason for a trillion Hong Kong dollar market cap, and also the reason Zhang Peng gave when saying Zhipu will continue along the path of becoming China's Anthropic.

Zhipu's income statement describes a different company. Nearly three-quarters of revenue comes from project-based delivery for enterprise and national clients, engineers on-site, custom fine-tuning, and margins thinning as work scale expands. Chinese analysts have made the comparison bluntly: the valuation speaks Anthropic, the business model speaks Palantir. Deep customer engagement, qualification thresholds, and delivery teams, not platform economics.

Both descriptions are partially correct, and the distance between them is where all the risk lies.

If there is a solution, it is visible in the revenue structure. The platform business is that 26.3%, the part that is compounding: cloud service revenue share is rising, cloud business gross margin rose from 3.3% to 18.9, platform recurring revenue grew 60 times, raising prices in a price war. The service business is that 73.7%, the part paying the bills today, while also limiting the company's future ceiling. Zhang Peng has stated the company is shifting from local deployment to the cloud, which is the correct direction, and an admission of what the current structure means.

A trillion Hong Kong dollar valuation is betting that 26.3% will become the company body, and 73.7% will become a legacy business line. This shift is possible. But it has not yet shown up in the audit results of a single full year.

Multiples measure this distance. At a trillion Hong Kong dollar market cap, Zhipu's price-to-sales ratio exceeded one thousand times, some estimates close to 1280 times. For rough comparison, OpenAI's approximately 730 billion U.S. dollar valuation against approximately 13 billion U.S. dollars revenue, price-to-sales ratio close to 56 times. Even calculating based on JPMorgan's aggressive forecast of 4.6 billion renminbi revenue in 2026 (growth over 500%), the forward multiple still exceeds 200 times. JPMorgan expects profitability in 2028. Soochow Securities models slower growth, smaller numbers.

As Zhipu grows to match the price, competitors have not stopped. Reportedly DeepSeek has completed a new round of financing exceeding 7 billion U.S. dollars. Moonshot AI is financing for its own listing. MiniMax listed in Hong Kong one day after Zhipu, halved the M3 model price, then watched about half its market cap disappear. In a market where model capabilities converge and price becomes the battlefield, pricing power is the only factor distinguishing platform from commodity, and pricing power is exactly what Zhipu has managed to maintain so far.

The company is also seeking more capital. On June 1, the company announced plans to list on the Shanghai STAR Market A-shares, targeting financing of approximately 15 billion renminbi, approximately 2.2 billion U.S. dollars. The application passed the acceptance stage on June 17. If completed, Zhipu will become the first AI company to complete a full dual listing on the mainland after listing in Hong Kong, facing domestic investors who have witnessed NVIDIA's surge from the outside and wish to own a local champion.

Compute Tax

This series now encounters three versions of the same problem.

Cambricon proved capability, not yet capture: a good enough chip running at real scale, priced by the market as if share has already been won. Star Engine has capture but not yet proved capability: four internet giants and a 2.8 billion U.S. dollar valuation, connected to a model that passed only 4 of its own benchmarks in 17 tasks.

Zhipu is the third variant, and the most enlightening, because it has both.

Capability is real. GLM-5.2 ranked second on a serious international programming leaderboard, behind an American model, ahead of all other open source models. Weights are public, benchmarks are independent, the model was trained on Chinese chips. Capture is also real. Nine of China's top ten internet companies have integrated its models. 4 million registered developers. Recurring platform revenue grew 60 times in a year. It raised prices 83% in a price war, and demand rose instead.

But it still loses about six renminbi for every one renminbi earned.

What Zhipu lacks is neither capability nor capture, but unit economics. The great trick of software has always been that you write once, and the cost to make the ten millionth copy is zero. Large models break this trick. Every copy has a cost. Every query has a cost. Every new customer comes with a compute bill, and the bill grows with context windows, inference length, and agent loops that the entire industry is competing to lengthen. Zhipu's R&D expenditure last year was 4.4 times revenue, not out of recklessness, but because this is the cost of standing at the frontier currently.

The world now has a public price for a frontier AI laboratory. This price was set by 4% float colliding with infinite demand; it says: scarcity, sovereignty, and the option value of becoming China's default option. What it has not yet stated is: this business works.

This is the experiment Zhipu is now conducting in the public market, on a stock ticker, with a filing calendar and quarterly disclosure obligations. It has proved a company can build frontier models on sanctioned chips, release weights for free, and still make the world pay. It has not yet proved a company can do all this and make money.

No one has proved it. Zhipu is just the first that must show its working process.

Models and Benchmarks: AI Wiki; The AI Rankings; BigGo Finance; Asia Tech Review. Information on GLM-4.7 (December 22, 2025; SWE-bench Verified score 73.8%, LiveCodeBench score 84.9%), GLM-5 (February 2026), GLM-5.1 (April 2026), and GLM-5.2 (mid-June 2026; context length up to one million tokens; uses MIT license) comes from company releases reported by these media outlets. Regarding the exact release date of GLM-5.2 in mid-June, different sources vary, so no specific date is given here. GLM-5.2 ranked second on the Code Arena frontend leaderboard, second only to Anthropic's Claude Fable 5; this information comes from Code Arena results reported by Asia Tech Review and Startup Fortune. Zhipu's own published benchmark data belongs to vendor-reported; treated separately from independent leaderboard results.

Domestic Chips: Reuters reposted via AOL, summarized by The AI Rankings; CNBC (earnings call). Reports on GLM-5 using Chinese accelerators (Huawei Ascend, Cambricon, Moore Threads, Kunlun Xin) rather than NVIDIA hardware for training and serving come from Reuters reports, presented here as reported content rather than company disclosure. Zhang Peng's statement on the company accelerating the use of domestic chips comes from CNBC's report on the earnings call. Slime asynchronous reinforcement learning framework and "joint design for domestic chip adaptation" R&D investment come from Soochow Securities annual report comments reposted via Futu.

Entity List: SCMP reposted via The AI Rankings. Listing Beijing Zhipu Huazhang Technology and its subsidiaries on the U.S. Entity List in January 2025, citations of reasons regarding military modernization, and Zhipu's objection to this reason are all based on reports from these sources.

Anthropic Model Suspension: Anthropic suspended access to Fable and Mythos models on June 12, 2026, to comply with U.S. Department of Commerce export controls, and restored access on July 1, 2026, after these controls were lifted (Anthropic Statement: https://www.anthropic.com/news/fable-mythos-access). Zhipu's public response characterizing frontier intelligence as something that should not be withdrawn comes from Zhipu social media reported by Asia Tech Review. This article explains the regulatory reasons for the suspension because the distinction between compliance-driven suspension and voluntary withdrawal is crucial to the argument, and Zhipu's statement sidestepped this.

Valuation, Forecasts, and Competitors: Caixin Global; South China Morning Post; Startup Fortune; BigGo Finance; KuCoin; Asia Tech Review. Price-to-sales ratio (peak over 1000 times trailing revenue, some estimates close to 1280 times; forward price-to-sales ratio over 200 times based on JPMorgan 2026 forecast) are analyst and media estimates, varying with stock price; presented here as reference rather than precise values. JPMorgan's revenue forecasts (4.6 billion renminbi in 2026, 11.4 billion renminbi in 2027, 30.9 billion renminbi in 2028, expected profitability in 2028) come from Caixin Global and SCMP. Soochow Securities' lower forecasts come from Futu. Comparison with OpenAI (approximately 730 billion U.S. dollar valuation against approximately 13 billion U.S. dollars revenue, according to Financial Times reports) is used only as a rough scale reference. DeepSeek receiving over 7 billion U.S. dollars financing, Moonshot AI pre-listing financing, MiniMax price cut and stock price fall, come from reports by Asia Tech Review, Caixin Global, and BigGo Finance. The Anthropic versus Palantir classification framework is an analyst comparison reported by BigGo Finance, citing Chinese market commentary, and is not this publication's original view.

STAR Market Listing: Startup Fortune citing Caixin Global. Announcement of A-share listing plan on June 1, targeting fundraising of approximately 15 billion renminbi (approximately 2.2 billion U.S. dollars), post-issuance share capital accounting for 2% to 8%, Guotai Haitong Securities acting as sponsor institution, passing acceptance stage on June 17, all come from these sources.

Classification Note

Financial performance, equity structure, IPO terms, lock-up mechanisms, and July placement information all come from company disclosures and multiple media reports, belonging to confirmed information. Stock prices and market caps are point-in-time data, dates are marked when cited. Domestic chip training, competitor financing rounds, and analyst forecasts belong to reported information, sources are marked. Valuation multiples are estimates varying with stock price. Zhipu's own benchmark data belongs to vendor-reported; here only rankings from independent leaderboards are cited as results.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News