레이어 1 위장술: 더 많은 암호화 애플리케이션이 공용 블록체인과 '부대끼기'를 시작할 때

저자: Alexandra Levis

번역: TechFlow

DeFi 및 RWA 프로토콜들은 인프라 수준의 밸류에이션을 얻기 위해 스스로를 레이어 1(Layer 1)로 재포지셔닝하고 있다. 그러나 Avtar Sehra는 대부분의 DeFi와 RWA 프로토콜들이 여전히 좁은 애플리케이션 영역에 국한되어 있으며 지속 가능한 경제성도 부족하다고 지적하며, 시장 역시 이러한 점을 점차 간파하고 있다고 말한다.

금융 시장에서 스타트업들은 투자자들이 테크 기업처럼 배수를 적용해 평가해주기를 바라며 오랫동안 자신들을 "테크 회사"로 포장하려는 노력을 해왔다. 그리고 이런 전략은 대개 통하기도 한다—적어도 단기적으로는 그렇다.

전통 기관들은 이를 통해 대가를 치렀다. 2010년대 내내 많은 기업들이 자신들을 테크 기업으로 재정의하려는 경쟁을 벌였다. 은행, 결제 처리업체, 소매업체들은 이제 금융기술(FinTech) 기업이나 데이터 기업이라고 자칭하기 시작했다. 하지만 이들 중 거의 아무도 진정한 테크 기업 수준의 밸류에이션 배수를 받지 못했으며, 그 이유는 기본적인 실적이 스토리에 미치지 못했기 때문이다.

WeWork은 가장 상징적인 사례 중 하나다. 테크 플랫폼인 척 위장한 부동산 회사였지만 결국 자신의 환상에 짓눌려 무너졌다. 금융 서비스 분야에서는 골드만삭스(Goldman Sachs)가 2016년 Marcus라는 디지털 우선 플랫폼을 출시하여 소비자 중심의 핀테크 기업들과 경쟁하려 했다. 초기에는 어느 정도 성과를 거두었으나 장기적인 수익성 문제로 인해 2023년 규모가 축소되었다.

JP모건은 자신들을 "은행 라이선스를 가진 테크 기업"이라 크게 선언했으며, BBVA와 웰스파고(Wells Fargo) 또한 디지털 전환에 막대한 투자를 했다. 그러나 이러한 노력들이 플랫폼 수준의 경제성을 실현한 경우는 극히 드물었다. 오늘날 이러한 기업들의 테크 환상은 폐허로 남아 있으며, 브랜드를 어떻게 포장하든 자본 집약적이거나 규제된 비즈니스 모델의 구조적 한계를 넘어서기 어렵다는 것을 명확히 일깨워 준다.

암호화 산업은 현재 유사한 정체성 위기를 겪고 있다. DeFi 프로토콜들은 레이어 1과 유사한 밸류에이션을 받고자 하며, RWA 탈중앙 앱(dApp)들은 주권 네트워크로 자리매김하려 하고 있다. 모두가 레이어 1의 "테크 프리미엄"을 추구하고 있는 것이다.

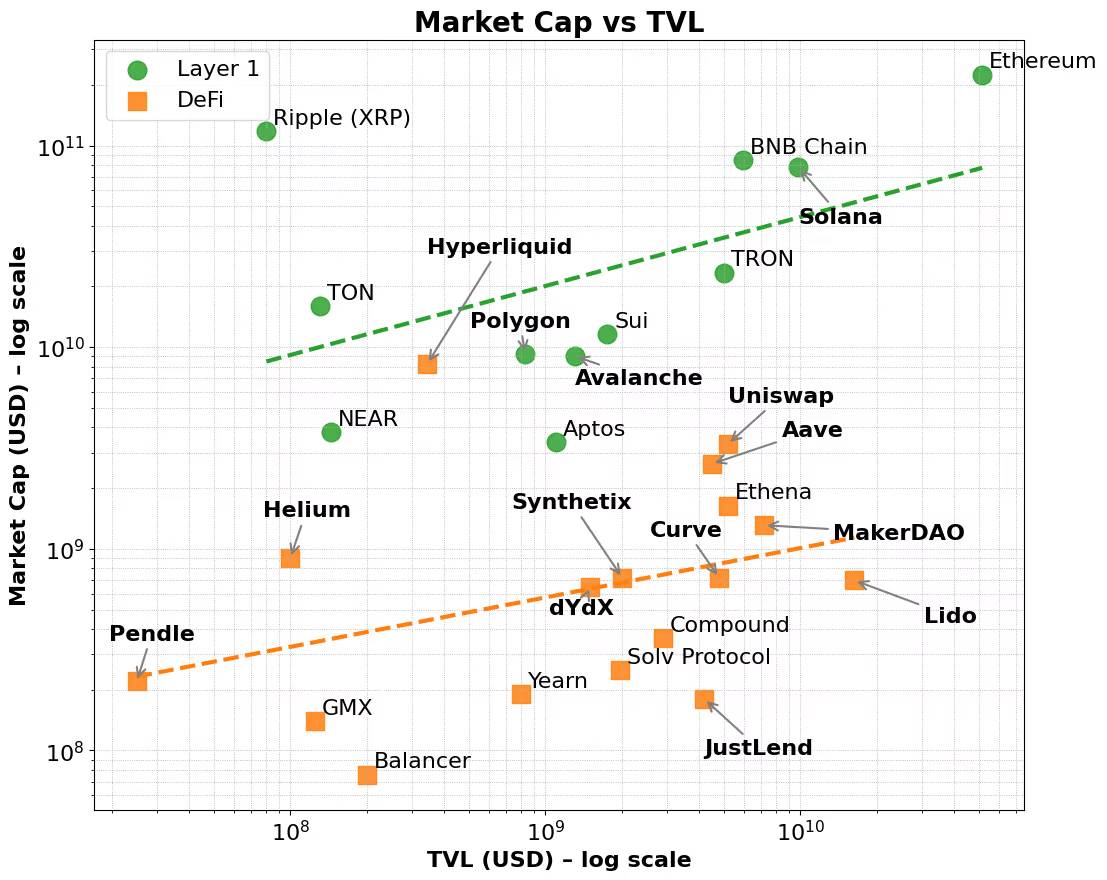

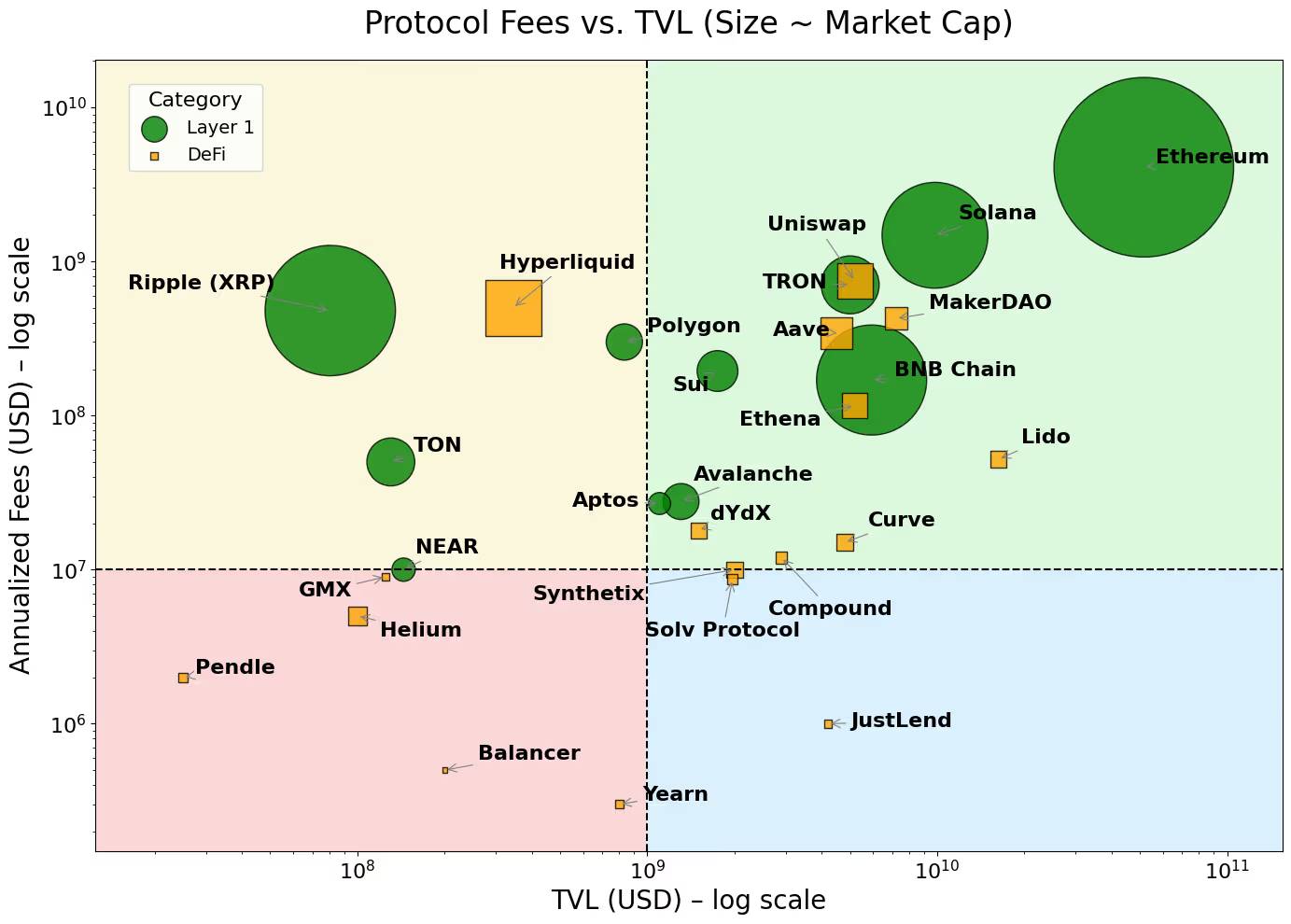

공평하게 말하면, 이 프리미엄은 실제로 존재한다. 이더리움, 솔라나, BNB 같은 레이어 1 네트워크는 총예치금액(TVL)이나 수수료 생성 등의 지표에 비해 항상 더 높은 밸류에이션 배수를 누려왔다. 이러한 네트워크는 인프라를 강조하고 애플리케이션이 아닌 플랫폼 중심의 서사를 통해 혜택을 받았다.

기본적인 요소들을 고려했음에도 불구하고 이 프리미엄은 여전히 유지된다. 많은 DeFi 프로토콜들이 강력한 TVL 또는 수수료 생성 능력을 보여주고 있음에도 불구하고, 여전히 레이어 1 수준의 시가총액에 도달하기 어려운 실정이다. 반면 레이어 1은 검증자 인센티브와 원생 토큰 경제를 통해 초기 사용자를 유치한 후 개발자 생태계와 조합 가능한 애플리케이션 분야로 확장된다.

결국 이 프리미엄은 레이어 1의 광범위한 원생 토큰 활용성, 생태계 조율 능력, 장기적 확장 가능성을 반영하는 것이다. 또한 수수료 규모가 증가함에 따라 이러한 네트워크의 시가총액은 비례하지 않는 수준으로 급격히 증가하는 경향이 있는데, 이는 투자자들이 현재의 이용 현황뿐 아니라 미래 가능성과 복합적인 네트워크 효과까지 고려하고 있음을 나타낸다.

인프라 채택에서 생태계 성장으로 이어지는 이러한 계층적 피드백 메커니즘은, 두 기술의 핵심 성능 지표가 유사해 보일지라도 왜 레이어 1의 밸류에이션이 항상 탈중앙 애플리케이션(dApp)보다 높은지를 잘 설명한다.

이는 주식 시장에서 플랫폼과 제품을 구분하는 방식과 매우 유사하다. AWS, 마이크로소프트 애저(Microsoft Azure), 애플 앱스토어(App Store), 메타(Meta)의 개발자 생태계와 같은 인프라 기업들은 단순한 서비스 제공자가 아니다. 그들은 생태계 그 자체다. 이러한 플랫폼은 수천 명의 개발자와 기업이 구축하고 확장하며 서로 협업할 수 있도록 지원한다. 투자자들은 이러한 기업들에게 더 높은 밸류에이션 배수를 부여하는데, 이는 현재의 수익뿐만 아니라 향후 새로운 사용 사례, 네트워크 효과, 규모의 경제 잠재력을 고려하기 때문이다. 반대로, 매우 수익성이 좋은 SaaS 도구나 틈새 서비스조차도 API 조합성과 제한된 활용성의 한계로 인해 동일한 밸류에이션 프리미엄을 얻기 어렵다.

현재 이와 같은 패턴은 대규모 언어 모델(LLM) 제공 업체들 사이에서도 반복되고 있다. 대부분의 공급업체들이 단순한 챗봇이 아닌 AI 애플리케이션의 인프라로서 자신을 포지셔닝하려고 경쟁하고 있다. 모두가 Mailchimp가 아니라 AWS가 되고 싶어 한다.

암호화 분야의 레이어 1도 유사한 논리를 따른다. 이들은 단순한 블록체인이 아니라 탈중앙 컴퓨팅과 상태 동기화의 조정 계층이다. 이들은 다양한 조합 가능한 애플리케이션과 자산을 지원하며, 원생 토큰은 가스 수수료, 스테이킹, MEV 등과 같은 기반 활동을 통해 가치를 축적한다. 더 중요한 것은, 이러한 토큰들이 개발자와 사용자의 인센티브 역할을 수행한다는 점이다. 레이어 1은 사용자, 개발자, 유동성, 토큰 수요 사이의 자기강화적 순환 덕분에 혜택을 받으며, 여러 산업 분야에서 수직적·수평적 확장을 지원한다.

반면 대부분의 프로토콜은 인프라가 아니라 단일 기능 제품이다. 따라서 검증자 집합(Validator Set)을 늘리는 것으로 레이어 1이 되는 것이 아니다—단지 더 높은 밸류에이션을 정당화하기 위해 제품에 인프라의 옷을 입히는 것일 뿐이다.

이것이 바로 앱체인(Appchain) 트렌드가 등장한 배경이다. 앱체인은 애플리케이션, 프로토콜 로직, 정산 계층을 하나의 수직 통합 기술 스택으로 통합하여 더 나은 수수료 포착, 우수한 사용자 경험, "주권성"을 약속한다. 일부 사례—예를 들어 Hyperliquid—에서는 이러한 약속이 실제로 실현되었다. 전체 기술 스택을 통제함으로써 Hyperliquid는 빠른 실행 속도, 뛰어난 사용자 경험, 상당한 수수료 수익을 logics, settlement layer into a vertically integrated tech stack, promising better fee capture, user experience, and "sovereignty." In a few cases—such as Hyperliquid—these promises have been fulfilled. By controlling the full tech stack, Hyperliquid has achieved fast execution, excellent user experience, and significant fee generation—without relying on token incentives. Developers can even deploy dApps on its underlying Layer 1, leveraging the infrastructure of its high-performance decentralized exchange. While its scope remains narrow, it demonstrates a certain degree of broader scalability potential.

However, most appchains are merely attempting to rebrand protocols by repackaging them, lacking real usage and deep ecosystem support. These projects often find themselves fighting on two fronts: trying to build both infrastructure and products, yet frequently lacking sufficient capital or team strength to excel at either. The end result is an ambiguous hybrid—neither a high-performance Layer 1 nor a category-defining dApp.

We've seen this situation before. A robo-advisor with a sleek UI is still essentially a wealth management service; a bank with open APIs remains fundamentally a balance-sheet-driven business; a co-working space company with a polished app is ultimately still leasing office space. Eventually, as market enthusiasm fades, capital will reassess the true value of these ventures.

RWA protocols today are falling into the same trap. Many are attempting to position themselves as infrastructure for tokenized finance, yet lack meaningful differentiation from existing Layer 1s and sustainable user adoption. At best, they are vertically integrated products without genuine need for an independent settlement layer. Worse, most have not yet achieved product-market fit within their core use cases. They simply bolt on infrastructure features and rely on inflated narratives, hoping this will support valuations that their economic models cannot sustain.

So what is the way forward?

The answer is not to pretend to be infrastructure, but to clearly define your role as a product or service—and execute it exceptionally well. If your protocol solves real problems and drives meaningful TVL growth, that’s a solid foundation. But TVL alone isn’t enough to make you a successful appchain.

What truly matters is real economic activity: TVL that enables sustainable fee generation, user retention, and clear value accrual for the native token. Moreover, if developers choose to build on your protocol because it is genuinely useful—not because it claims to be infrastructure—the market will naturally reward you. Platform status is earned through substance, not self-declaration.

Some DeFi protocols—such as Maker/Sky and Uniswap—are already moving along this path. They are evolving toward appchain-like models to improve scalability and cross-network access. But they do so from positions of strength: mature ecosystems, clear revenue models, and proven product-market fit.

In contrast, the emerging RWA space has yet to demonstrate lasting appeal. Nearly every RWA protocol or centralized service is rushing to launch an appchain—typically supported by fragile or unproven economic models. Like leading DeFi protocols transitioning to appchain models, the optimal path for RWA protocols is first to leverage existing Layer 1 ecosystems, accumulate user and developer traction, drive TVL growth, and demonstrate sustainable fee generation—before evolving into a purpose-built appchain infrastructure model.

Therefore, for appchains, the utility and economic model of the underlying application must be validated first. Only after these foundations are proven does a transition to an independent Layer 1 become viable. This stands in stark contrast to general-purpose Layer 1s, which can initially prioritize building validator and trader ecosystems. Early fee generation largely depends on native token trading, and over time, cross-market expansion draws in developers and end users, eventually driving TVL growth and diversified revenue streams.

As the crypto industry matures, the fog of narrative is lifting, and investors are becoming more discerning. Terms like “appchain” and “Layer 1” no longer attract attention by name alone. Without a clear value proposition, sustainable token economics, and a defined strategic roadmap, protocols lack the necessary foundation to transition into true infrastructure.

What the crypto industry—especially the RWA sector—needs is not more Layer 1s, but better products. Projects that focus on building high-quality offerings will be the ones truly rewarded by the market.

그림 1. DeFi와 레이어 1의 시가총액과 TVL

그림 2. 레이어 1은 수수료가 높은 곳에 집중되어 있고, dApp은 수수료가 낮은 곳에 집중되어 있다

참고: 이 칼럼에 표현된 의견은 저자의 개인적인 견해이며 CoinDesk, Inc. 또는 그 소유주 및 계열사의 입장과 일치하지 않을 수 있습니다.

TechFlow 공식 커뮤니티에 오신 것을 환영합니다

Telegram 구독 그룹:https://t.me/TechFlowDaily

트위터 공식 계정:https://x.com/TechFlowPost

트위터 영어 계정:https://x.com/BlockFlow_News