Interview with VanEck Portfolio Manager: From an institutional perspective, should you buy BTC now?

TechFlow Selected TechFlow Selected

Interview with VanEck Portfolio Manager: From an institutional perspective, should you buy BTC now?

"A support level near $78,000 and $70,000 is a good entry opportunity."

Compiled & Translated: TechFlow

Guest: Matthew Sigel, Portfolio Manager of VanEck Onchain Economy ETF ($NODE)

Host: Anthony Pompliano

Podcast Source: Anthony Pompliano

Original Title: Is It Time To Buy Bitcoin Now?

Air Date: November 25, 2025

Key Takeaways

Matthew Sigel is the portfolio manager of VanEck Onchain Economy ETF ($NODE), a fund widely regarded as one of the most forward-thinking institutional products in the crypto ecosystem. In this interview, we explore how institutions evaluate Bitcoin, covering market structure, investor sentiment, and recent price drivers. Matthew shares three key metrics he uses to assess Bitcoin’s future trajectory, his investment strategy during volatile periods, and his focus areas within publicly traded crypto-related equities. The discussion also extends to the broader digital asset landscape, including smart contract platforms, stablecoins, and sectors with long-term potential.

Below is a concise visual summary of the podcast for a quick overview.

Highlights Summary

-

Bitcoin miners are transforming into AI companies.

-

Volatility remains one of the biggest challenges in the crypto space.

-

Matthew Sigel typically evaluates Bitcoin from three perspectives. First, global liquidity—Bitcoin has consistently shown a negative correlation with the U.S. Dollar Index (DXY). Second, leverage levels within the crypto ecosystem—currently, leverage has declined significantly and funding rates have dropped sharply. Third, on-chain activity—which currently appears weak and not optimistic.

-

The support levels around $78,000 and $70,000 present attractive entry opportunities.

-

I usually adopt dollar-cost averaging, investing fixed amounts at specific price levels or every few days.

-

My investment style involves small positions, high diversification, and applying a "buy low, sell high" approach across the market. So far, this strategy has worked well.

-

Once deciding to buy, there's no need to deploy all capital at once—gradual accumulation allows for more rational responses to market volatility.

-

The market is oversaturated, and altcoin inflation remains high. Beyond speculation, they haven't yet achieved true product-market fit.

-

Solana excels in building cross-industry ecosystems.

-

Trump’s deregulation policies have negatively impacted altcoins by weakening the advantage of decentralization under new regulatory conditions.

How Institutions View Bitcoin Today

Anthony Pompliano: Today we’re joined by Matthew Sigel, portfolio manager of VanEck’s Onchain Economy ETF ($NODE).

I think we can start with an important question: How do institutions view Bitcoin today? Market signals are mixed—there are positive data points alongside negative ones, price performance has been poor, and investor sentiment is low. How do VanEck and other institutions generally view Bitcoin and its role in asset allocation?

Matthew Sigel:

In terms of investor interest, I believe institutional attention toward Bitcoin remains strong. We continue to receive significant demand for educational content, portfolio construction advice, and small allocations. However, Bitcoin prices have corrected over 30%, and trading volumes in some of our listed products have declined. This suggests that while research interest is high, actual trading activity shows hesitation.

Anthony Pompliano: If we analyze these data points, how would you differentiate between positive and negative indicators?

Matthew Sigel:

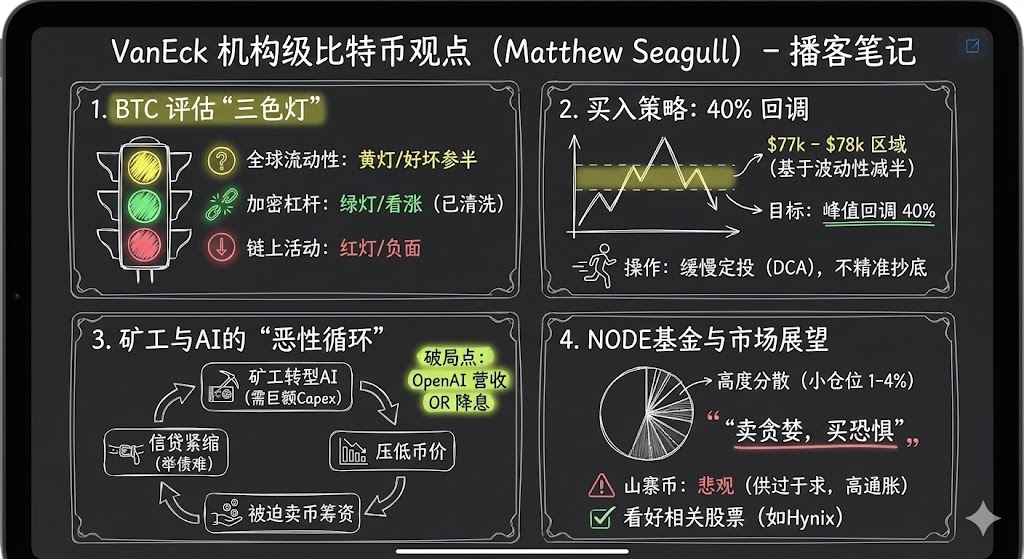

We typically assess Bitcoin’s market performance through three lenses.

The first is global liquidity. Bitcoin has maintained a consistent negative correlation with the U.S. Dollar Index (DXY), so global risk appetite, leverage, and deleveraging have had a major impact on Bitcoin—especially since the COVID pandemic. This macro trend has influenced Bitcoin far more than in previous phases. Unfortunately, Bitcoin miners sit at the center of this process. Recently, tightening credit conditions and massive debt raises by tech giants (like Oracle) to fuel AI development have forced miners to adjust operations. This requires substantial capital expenditures, often funded via debt, equity, or selling Bitcoin. Until October, miners were actively selling Bitcoin to finance these projects. This created a vicious cycle: tighter credit not only hurt miner financing but further pressured Bitcoin prices. Therefore, from a global liquidity perspective, evidence is mixed—some support exists, but market outlooks are increasingly uncertain.

The second lens is leverage within the crypto ecosystem. This is a positive signal. We saw a market-wide liquidation in mid-October, reducing overall leverage and causing funding rates to drop sharply. Within a 12-hour window, approximately $1.7 billion in positions were liquidated. This indicates a meaningful reduction in leveraged sentiment, which I view as bullish.

The third lens is on-chain activity. We monitor transaction fees, active addresses, and transaction frequency. From these metrics, on-chain activity currently appears weak and not encouraging.

Evaluating Real-Time Metrics and Key Bitcoin Price Levels

Anthony Pompliano: So how do you assess the Bitcoin market? We’ve covered global liquidity as a “yellow light,” leverage as a “green light,” and on-chain activity as a “red light.” These signals are clearly mixed. How do you weigh them? Among these three, which carries the most weight? And how do you adjust your strategy when signals conflict?

Matthew Sigel:

It largely depends on individual investment styles. As mentioned earlier, current trading volumes suggest investor hesitation. With my Onchain Economy ETF, about two or three weeks ago, I sold 15% of our Bitcoin mining exposure. We noticed optimism fading and credit conditions tightening. Miners contribute significantly to returns, so modest de-risking ahead of year-end makes sense. We haven’t redeployed that capital yet, but I’m watching several key Bitcoin price levels.

One key level is $78,000, representing a 40% decline from the peak. In the last cycle, Bitcoin fell 80%. Since then, volatility has roughly halved. If volatility is halved, the drawdown could also be halved—making a 40% correction a reasonable risk-reward opportunity. Additionally, $78,000 breaks above the post-election support at $69,000. We experienced volatility around $70,000 on election day, and tested it again in April. This forms a solid technical floor.

If prices fall further, another critical level is $55,000—the 200-week moving average. In an extreme scenario—say, another 80% drop—Bitcoin could reach ~$27,000, coinciding with the price when BlackRock filed for its Bitcoin ETF. That would erase all ETF gains, but I consider it unlikely. Overall, a 40% drop and support near $70,000 offer a solid entry point.

Anthony Pompliano: I understand your point. Individual investors can flexibly target levels like $77,000 or $80,000—the difference may not matter much personally. But institutions face constraints: risk management, rebalancing, etc.—and access data tools and experience individuals lack.

How do you differentiate investing between $77,500 and $80,000? Should you act decisively near your target rather than wait for lower prices? Given current emotional volatility, how do you execute? For example, when markets swing between extreme greed and fear, equity volatility is low, but the VIX hits 28—do you jump in decisively, or maintain discipline using limit orders and price targets?

Matthew Sigel:

My personal style favors gradual entry. I usually opt for dollar-cost averaging—investing fixed amounts at set price levels or every few days. As a professional investor, we have dedicated traders who help locate liquidity and execute efficiently. This is one institutional advantage—enabling disciplined, systematic execution.

But there’s no single right way. The key is making intelligent, logical decisions aligned with your framework and client needs. For me, slow deployment fits best.

Why $NODE Outperforms: Crypto-Linked Equities Strategy

Anthony Pompliano: Let’s discuss public equities tied to Bitcoin and crypto. Your ETF, $NODE, has performed exceptionally since launch—I understand it’s up 28%–32%, outperforming Bitcoin itself.

Generally, many assume Bitcoin or crypto assets should outperform related stocks, but we’ve seen the opposite over the past year. Can you explain $NODE’s public equity strategy and your allocation philosophy?

Matthew Sigel:

Indeed. From an investor standpoint, both institutions and retail prefer indirect exposure via equities. Financial disclosures are standardized, and equities integrate easily into brokerage accounts. Since the election, a major shift has been investment banks willing to underwrite crypto-linked assets—explaining the surge in IPOs, SPACs, and follow-ons. At VanEck, we were fortunate to pivot post-election toward crypto-linked equities. The results speak for themselves: since $NODE launched, Bitcoin is down 16%, while related equities rose sharply. We identified AI’s deep impact on miners and built a relatively low-volatility portfolio.

Of course, we’ve seen drawdowns, but compared to peers, strict position sizing reduced downside risk. In this early-stage industry, small, highly leveraged firms face execution and operational risks. I see no need to take excessive bets—like 10% in a single name. Instead, I cap exposures between 1%–4%, leveraging volatility for advantage.

Additionally, our definition of crypto-linked equities is broad—not limited to core crypto businesses, but including firms entering the Bitcoin value chain via tokenization or sales. These companies cut costs and generate revenue, significantly impacting P/E ratios. Thus, my style emphasizes small positions, high diversification, and “buy low, sell high” tactics. So far, it’s working well.

Anthony Pompliano: You mentioned companies not primarily focused on crypto. Could you give an example—firms selling to or using crypto tech without being traditional crypto companies?

Matthew Sigel:

A good example is Hynix, a Korean memory manufacturer supplying semiconductors. They compete with Micron and SanDisk in an oligopolistic market. When Bitcoin miners sell well, Hynix’s DRAM used in mining represents low-to-mid single-digit percentage of their business. Marginally impactful, but not dominant. However, when factoring in AI’s supply chain effects, supply-demand dynamics shift. Hynix now trades at ~5x earnings—a compelling valuation. We hold ~1%. It benefits from both digital assets and other structural growth themes. A great case study.

What Could Turn Around Bitcoin Miners’ Downturn?

Anthony Pompliano: Bitcoin miners have faced sharp drawdowns recently, especially after price peaks. What factors could reverse their slump?

We recently discussed a thought-provoking idea from Howard Marks in a 2018 Wharton interview. He criticized the metaphor of “catching a falling knife.” His strategy isn’t precise timing, but gradually accumulating near perceived lows—even if prices keep falling—and adding more during recovery. So, what would shift the trend for miners?

Matthew Sigel:

I fully agree with Howard Marks—that’s exactly my approach. Once committed, there’s no need to deploy all capital at once. Gradual accumulation offers a more rational response to volatility.

From my analysis, two key factors could help miners recover. First, revenue visibility from AI. There’s debate on whether AI investments yield real returns. I believe AI’s gains are more about cost optimization than direct revenue. By cutting operating costs, companies boost EPS meaningfully—a positive signal. For instance, OpenAI recently partnered with Target, integrating AI into retail apps and checkout systems. The deal could be nine figures. While disclosure is limited now, more such deals could rebuild market confidence in AI.

Second, Federal Reserve policy. Rate cuts would improve liquidity significantly—critical for miners. Markets are divided on a December cut, but improved liquidity would ease miner financing pressure.

Overall, AI revenue trends and Fed policy could be pivotal in reversing miners’ downturn.

Anthony Pompliano: When discussing crypto-linked public companies, miners are key. Then there are stablecoin issuers like Circle, Gemini, Coinbase, plus infrastructure and other themes. How do you view these?

Matthew Sigel:

Circle is a classic case—once overvalued due to market euphoria, now undergoing valuation reset. Yet, their market share is quietly growing. We may increase exposure in the future. Regarding miners, recent dynamics highlight the importance of capital costs. Over the past three months, nearly all miners raised funds for AI infrastructure. This is capital-intensive, and we’re seeing divergence in capital access. Cipher recently partnered with Fluid Stack (backed by Google), securing debt financing. Bitdeer relied on convertible debt; Clean Spark used dilutive financing. This gap will intensify winner-take-all dynamics—investors should favor large miners with capital advantages.

Anthony Pompliano: Economies of scale are becoming crucial. Earlier, size didn’t matter due to small market size. But as the industry matures—across private markets, liquid crypto assets, and early public firms—scale matters more. Coinbase has become a real giant; several miners have crossed scale thresholds. In traditional industries, economies of scale are vital. Same in crypto now—scale or get marginalized.

Matthew Sigel:

I completely agree. Early mining strategies focused on finding the cheapest power, profiting from regional advantages. But limited Wall Street funding made scaling hard. Now, that’s changing—especially at the intersection of AI and mining. Companies like Tera Wulf and Cipher now use debt to scale. Though ratings are low, this marks a turning point for minority shareholders.

Still, Bitcoin mining remains regionally concentrated. Cipher operates in Texas, Tera Wulf in New York, Bitfarms in PJM (the largest U.S. grid operator, covering 13 states and D.C.). Direct competition isn’t intense yet, but expansion signs exist. Tera Wulf recently said it plans to enter Texas to serve more clients. As the industry grows, economies of scale will emerge—but like utilities, regional factors will remain important.

Evaluating Corporate Balance Sheets Holding Bitcoin

Anthony Pompliano: MicroStrategy has demonstrated massive scale in holding Bitcoin on its balance sheet. Now, many companies are adding Bitcoin or other crypto assets—some via traditional listings, others through reverse mergers or SPACs. How do you view the broader digital asset market and how these assets might accrue value over time?

Matthew Sigel:

We’re relatively cautious here. Many small-cap digital asset firms may struggle to sustain high valuations. Not impossible, but no reason to expect so many small players to maintain premiums. Early in my career, I covered Asian markets—many NAV-type firms traded at 50% discounts, especially without clear control transitions or minority shareholder exit paths. So we avoid such structures, though exceptions exist. As valuations reset, some small firms are selling Bitcoin to buy back stock—activist involvement could create opportunities.

I’m watching whether Strive’s deal closes. If it does, Strive’s risk-reward may become more attractive—its preferred share structure is clearer, allowing fixed-income investors to better assess risk. For example, Strive’s preferred shares have a redemption price of $110, issued at $75, par value $100. Interest rate management keeps target pricing between $95–$105. This design improves upside/downside clarity.

In contrast, MicroStrategy’s preferred structure is more complex. Though closely tied to convertible bond arbitrageurs and able to trade at premiums cyclically, creditors face uncertainty—since the company retains call rights. This complicates risk assessment and may be less investor-friendly.

Similar issues arise with Meta Planet. They recently announced a new preferred structure resembling Strive’s—but this may not be favorable. Such designs increase bondholder power, prioritizing cash flows to debt, weakening equity upside. Better sustainability for bondholders, but potentially negative for shareholders—especially firms relying on equity gains. This could become a burden.

Anthony Pompliano: There’s skepticism about these firms’ ability to repay preferred debt. Saylor noted that even with just 2% annual Bitcoin appreciation, they can operate indefinitely. With zero growth, selling stock could fund operations for 70 years. How do you assess their repayment capacity?

Matthew Sigel:

It depends on balance sheet structure. Firms like MicroStrategy rely on rising Bitcoin prices and unrealized gains. They can borrow against these gains to sustain operations. Smaller firms tend to sell Bitcoin directly to repay debt. This may boost investor confidence, but raises concerns: if multiple firms sell Bitcoin during bear markets, what happens? This could amplify downward pressure—especially amid weak sentiment.

Anthony Pompliano: If these firms begin集中 selling Bitcoin, what would happen? Could forced selling occur? For example, might Michael Saylor be forced to liquidate?

Matthew Sigel:

This would likely worsen Bitcoin’s downside risk, especially in weak sentiment environments. Saylor’s case is unique—even if Bitcoin drops 50% from highs, he doesn’t need to sell. He can refinance through creditor negotiations. But smaller firms face tougher situations. If their stock trades at a 50% discount to NAV, activists may seek board seats and pursue legal actions for governance changes or even liquidation to return assets to shareholders. This process is typically long—taking one to two years.

Anthony Pompliano: For non-crypto firms holding Bitcoin—like Tesla or Block—will this trend grow, or will the market differentiate?

Matthew Sigel:

This is worth watching. We’ve observed similar cases managing the Node ETF. Tesla and Allied Resources (ARLP) hold Bitcoin, but the market hasn’t rewarded these minor holdings. Still, this could reverse. Recently, MSCI considered removing MicroStrategy from certain indices—prompting firms to keep Bitcoin below 49% of total assets to stay index-eligible. This lets them benefit from Bitcoin gains while maintaining index inclusion. Markets evolve—adjusting rules may lead to higher valuations for firms with small Bitcoin stakes.

Matthew’s Outlook on Altcoins and Bitcoin Dominance

Anthony Pompliano: Your team spends considerable time researching crypto assets and related public companies. What’s your current view on cryptocurrencies beyond Bitcoin?

Matthew Sigel:

Honestly, we haven’t been as aggressive as some ETF competitors in launching single-token products. We’ve filed for BNB and Avalanche (AVAX) ETFs. But objectively, the market is oversaturated, and altcoin inflation remains high. Beyond speculation, they haven’t achieved real product-market fit.

Thus, we’re not bullish. Clearly, the market has pulled back sharply. I attended the MultiCoin Summit yesterday and found that Solana excels in building cross-industry ecosystems. Many sectors are adopting its blockchain architecture. Yet, compared to corporate chains (like Tempo or Circle), decentralized blockchains lack sales teams. Corporate chains use sales forces to onboard merchants and stock incentives to drive adoption, while decentralized chains rely solely on community momentum and monetization potential—less direct in driving merchant adoption like Visa, Mastercard, Square, or Solana.

Anthony Pompliano: What about performance relative to Bitcoin? Historically, altcoins outperformed Bitcoin in bull markets. But this time, Bitcoin has beaten most altcoins—surprising many. Why?

Matthew Sigel:

From a fiat perspective, Bitcoin has indeed outperformed. I believe Trump’s deregulation policies negatively impacted altcoins by weakening the advantage of decentralization under new regulations. Previously, Ethereum held a clear edge as a decentralized alternative. Now, that edge is erased—every project competes on a level playing field. This partly explains why corporate chains are rising. They aren’t fully decentralized, lack explicit decentralization goals, but can use tokens to run businesses once deemed illegal. This erodes differentiation for truly decentralized projects like Ethereum and Solana.

Inside $NODE: Structure, Allocation, and Strategy

Anthony Pompliano: Could you briefly introduce NODE and your investment strategy?

Matthew Sigel:

NODE is an actively managed ETF. We can allocate up to 25% of assets to cryptocurrencies via ETFs. Currently, we hold 11% in Bitcoin ETFs, ~1% each in Ethereum and Solana.

The rest consists of related equities—any company demonstrating a clear strategy to save or earn money through Bitcoin, blockchain, or digital assets. I firmly believe Bitcoin miners are transitioning into AI companies. Miners represent our largest exposure—about one-third. The remainder is allocated across fintech, e-commerce, energy infrastructure, etc. This diversification aims to smooth portfolio volatility.

If we only invested in pure-play crypto firms like MicroStrategy and Coinbase, volatility from these leveraged names could exceed 10%. Based on institutional feedback, volatility is one of the biggest challenges in crypto. Therefore, our strategy reduces overall volatility through diversification, while still capturing growth from digital asset adoption. That’s NODE’s core mission.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News