Bitcoin's current correction: Amid the end of the "four-year cycle," a government shutdown intensifies liquidity shocks

TechFlow Selected TechFlow Selected

Bitcoin's current correction: Amid the end of the "four-year cycle," a government shutdown intensifies liquidity shocks

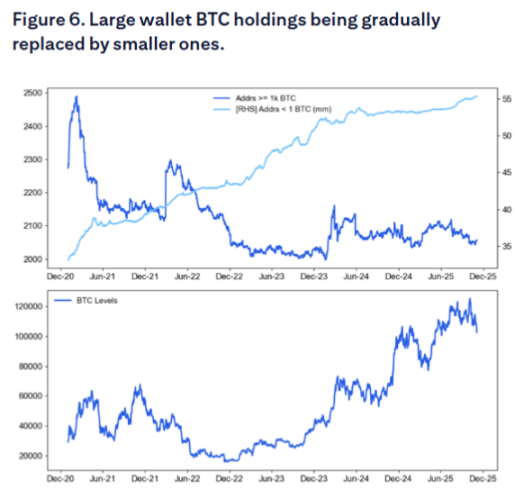

On-chain metrics indicate that Bitcoin whales are gradually decreasing, while the holdings of smaller retail wallets are increasing.

Author: He Hao

Source: Wall Street Insights

The crypto market is undergoing a deep adjustment. Bitcoin has fallen approximately 20% from its all-time high in early October. This correction is occurring at the tail end of Bitcoin's "four-year cycle." A liquidity crisis triggered by the ongoing U.S. government shutdown is exacerbating both the depth and duration of this downturn.

Historical Trajectory of Bitcoin’s Four-Year Cycle

Bitcoin’s four-year cycle theory is built upon its halving mechanism. Every 210,000 blocks mined—approximately every four years—the block reward for miners is cut in half, reducing the supply of new bitcoins. This mechanism creates predictable supply shocks that have historically triggered cyclical price increases.

Looking back, Bitcoin’s four-year cycle has shown remarkable consistency:

-

After the first halving in November 2012, Bitcoin’s price surged from $12 to around $1,100.

-

Following the second halving in July 2016, the price rose from about $650 to nearly $20,000.

-

After the third halving in May 2020, the price climbed from around $8,700 to over $67,000.

-

In April 2024, Bitcoin completed its fourth halving, reducing the block reward from 6.25 BTC to 3.125 BTC.

About a dozen months after each halving, Bitcoin reaches a cyclical peak before entering a bear market. It has now been 18 months since the April 2024 halving event.

However, some research institutions suggest that the Bitcoin market may be gradually moving away from the traditional four-year cycle centered on halvings. Bitwise noted in its long-term Bitcoin research report that as institutional investors continue to enter the market and spot ETFs provide new demand channels, the market structure is maturing, and price volatility may no longer strictly follow the traditional four-year rhythm.

Meanwhile, the impact of the 2024 halving on the supply side has significantly weakened compared to earlier cycles. According to data from Glassnode and Galaxy Research, this halving reduced Bitcoin’s annualized issuance rate from about 1.7% to 0.85%. However, with approximately 19.7 million bitcoins already mined out of a total cap of 21 million, newly issued coins represent a diminishing share of the overall supply, reducing their marginal market impact. This means pricing will increasingly depend on capital inflow structures—particularly institutions and long-term holders—rather than primarily being driven by changes in new supply.

“Whale” Selling: A Classic Sign of Cycle’s End

Citi’s latest report reveals a key driver behind the current correction: on-chain data shows that Bitcoin “whales” (large holders) are gradually decreasing their holdings, while small “retail” wallets are accumulating. This phenomenon aligns closely with the four-year cycle theory—that is, toward the end of a cycle, smart money typically sells Bitcoin to new entrants.

On-chain data indicates that since August, whales have collectively sold 147,000 bitcoins, worth approximately $16 billion.

Citi’s report highlights that the number of addresses holding more than 1,000 bitcoins is declining, while the number of “retail” investors holding less than one bitcoin is increasing. Glassnode’s holder-tier analysis shows entities holding over 10,000 bitcoins are in a clear “distribution” phase, while those holding 1,000–10,000 BTC remain largely neutral. Net buying is mainly coming from smaller holders who tend to adopt long-term positions.

There is deep logic behind this selling pattern. Nearly all long-term holders are currently in profit and are engaging in large-scale profit-taking. André Dragosch, Bitwise’s European Research Head, pointed out that these whales “believe in the four-year halving cycle and therefore expect Bitcoin has already reached the peak of this cycle.”

Ki Young Ju, CEO of CryptoQuant, noted that unlike previous cycles where whales sold directly to retail, the current market structure is evolving into a transfer of holdings from old whales to new long-term holders—such as institutions, ETFs, and strategic buyers. This implies that although selling pressure persists, the nature of buyers is changing, potentially leading to a milder but more prolonged price correction.

Government Shutdown as a Liquidity “Vacuum”

A more immediate catalyst for Bitcoin’s current correction stems from the liquidity crisis caused by the U.S. government shutdown. The rapid expansion of the Treasury General Account (TGA) balance is draining significant liquidity from financial markets, with Bitcoin—as a risk asset—being hit first and hardest.

By late October 2025, the TGA balance surpassed $1 trillion for the first time, reaching its highest level in nearly five years since April 2021. Over recent months, the balance surged from around $300 billion to $1 trillion, withdrawing over $700 billion in liquidity from the market.

It should be clarified that the rise in TGA balance is not solely due to the government shutdown but results from two overlapping factors:

-

First, the shutdown itself: Since the U.S. government shut down on October 1, 2025, the Treasury continues collecting tax revenue and issuing bonds, but with Congress failing to pass a budget, most federal agencies are closed, preventing planned expenditures. As a result, the TGA account becomes “inflow-only.”

-

Second, the ongoing effect of large-scale U.S. debt issuance. Even during normal operations, the U.S. Treasury issues bonds to replenish the TGA, which also drains market liquidity.

The impact of this “dual vacuum” mechanism is substantial:

According to Federal Reserve reports and financial institution data, foreign commercial bank cash assets have dropped to about $1.176 trillion, a sharp decline from July’s peak. Total reserves at the Fed have fallen to $2.8 trillion, the lowest level since early 2021.

The ballooning TGA balance has triggered broad stress in money markets. The upper end of overnight repo rates reached 4.27%, far exceeding the Fed’s 3.9% interest on excess reserves and the 3.75%-4.00% federal funds target range. The SOFR rate also rose significantly, indicating clear tightening in market liquidity.

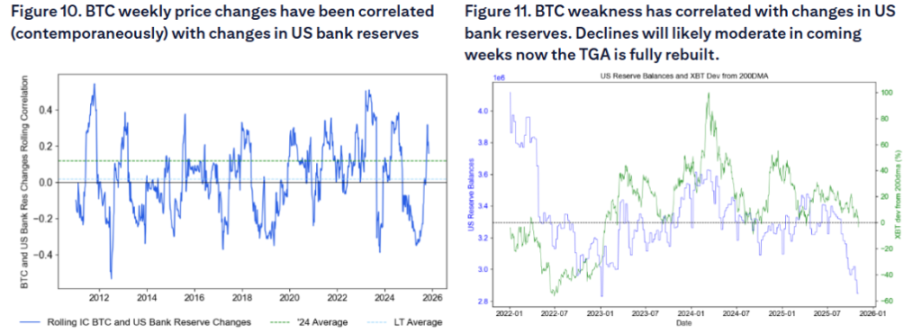

Citi’s report particularly emphasizes that cryptocurrencies are “highly sensitive” to banking system liquidity. Studies show that Bitcoin’s weekly price movements correlate synchronously with changes in U.S. bank reserves—declines in reserves often coincide with Bitcoin weakness. This sensitivity makes Bitcoin one of the earliest and most vulnerable victims of liquidity tightening.

From a policy standpoint, the government shutdown is effectively equivalent to multiple rounds of de facto rate hikes. Analysts estimate that the $700 billion in liquidity withdrawn by the Treasury has a contractionary effect comparable to a significant monetary tightening.

The Fed announced the end of quantitative tightening (QT) in its October meeting. Analysis suggests the Fed might not have made this decision had it not been for the severe liquidity strain. However, this policy shift won’t take effect until December.

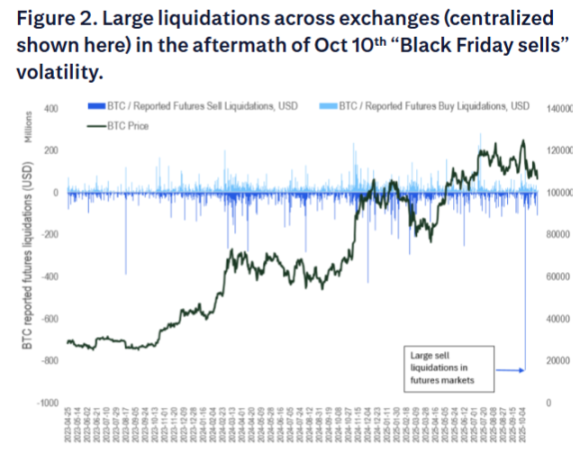

October 10 “Black Friday” Liquidation Event

Citi’s report notes that the “Black Friday” liquidation event on October 10 further damaged market risk appetite. While futures markets are typically zero-sum games, this round of liquidations likely impaired crypto-native participants’ willingness to take risks and suppressed risk appetite among potential new ETF investors.

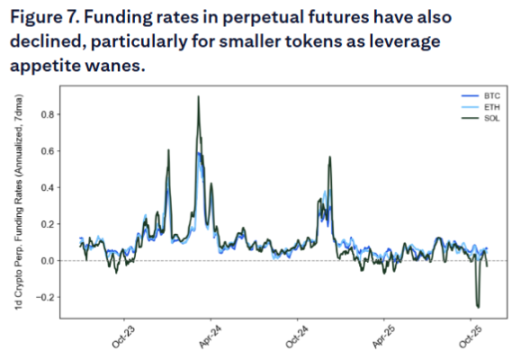

Falling funding rates also reflect weak leveraged demand, signaling overall softness in market sentiment.

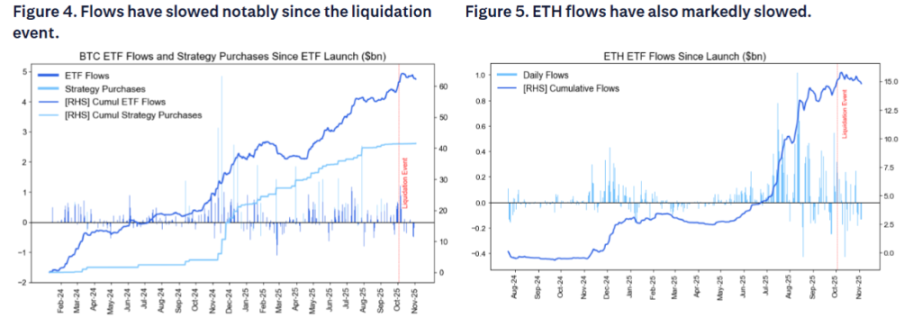

In addition, inflows into U.S. spot Bitcoin ETFs have declined significantly in recent weeks—contrary to market expectations, as ETF flows were previously considered relatively immune to the October 10 “Black Friday” liquidations in futures and decentralized exchanges. Inflows into Ethereum ETFs have also slowed markedly.

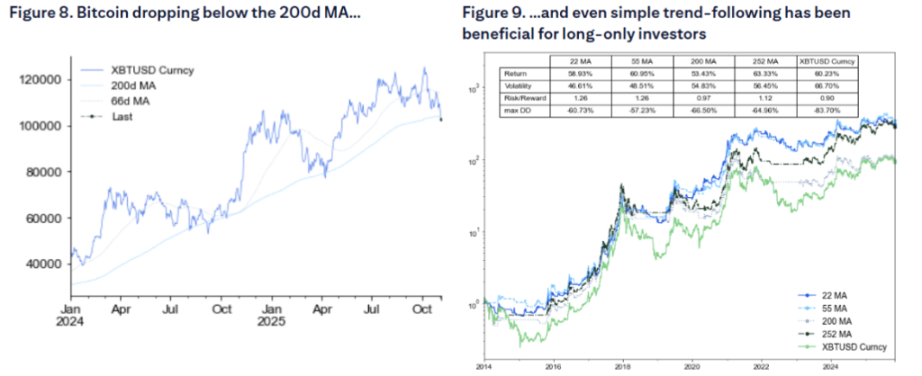

Citi’s report also points out that Bitcoin is now trading below its 200-day moving average, which typically further dampens demand. Technical analysis shows that even simple moving average rules have helped manage Bitcoin investments over the past decade, underscoring the importance of technical indicators in investment strategies.

Turning Point Amid Crisis: Liquidity Release Upon Government Reopening

Despite the current grim outlook, the root cause of the crisis also holds the key to a potential market turnaround. Since the government shutdown is the primary driver of liquidity tightening, once it ends, the U.S. Treasury will begin spending down its massive TGA cash balance, injecting hundreds of billions of dollars back into the economy.

Goldman Sachs previously projected that the shutdown would most likely end around the second week of November, with critical pressure points including payroll deadlines for air traffic controllers and airport security personnel on October 28 and November 10—similar disruptions in 2019 ultimately led to the end of that shutdown. Prediction markets indicate roughly a 50% chance of reopening by mid-November, with less than a 20% probability of extending beyond Thanksgiving.

Once the U.S. government resumes operations, the release of pent-up liquidity could trigger a broad rush into risk assets. This liquidity injection could act like “stealth quantitative easing,” similar to what occurred in early 2021, when the accelerated drawdown of Treasury cash balances fueled a strong stock market rally. If the government reopens, the timing of this liquidity release—coinciding with year-end—could propel explosive rallies in liquidity-sensitive assets such as Bitcoin, small-cap stocks, and nearly all non-AI-related assets.

The worse the near-term situation, the greater the pent-up liquidity available for release. With the TGA balance nearing $1 trillion, its eventual drawdown could unleash an unprecedented wave of liquidity. This sudden return of liquidity could serve as a powerful catalyst for a strong rebound in Bitcoin and other risk assets.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News