Liquidity Dries Up: Where Do Crypto Project Returns Actually Come From?

TechFlow Selected TechFlow Selected

Liquidity Dries Up: Where Do Crypto Project Returns Actually Come From?

Money rules everything.

Author: Joel John

Translation: TechFlow

You know things are looking grim when people start talking about "fundamentals" again. Today's piece explores a simple yet critical question: Should tokens generate revenue? And if so, should teams buy back their own tokens? As with most complex issues, there’s no clear-cut answer—progress here is paved more by honest conversation.

If you're a founder or part of a DAO considering a token buyback program, we’d love to chat. Just hit reply or DM me on Twitter.

Alright, let’s dive in…

Life is just a capitalist game.

This article was inspired by a series of conversations I had with Covalent's Ganesh, covering seasonality of revenue, evolution of business models, and whether token buybacks are the best use of protocol capital. It also complements my Tuesday post on the “stagnation” in crypto.

Hello everyone!

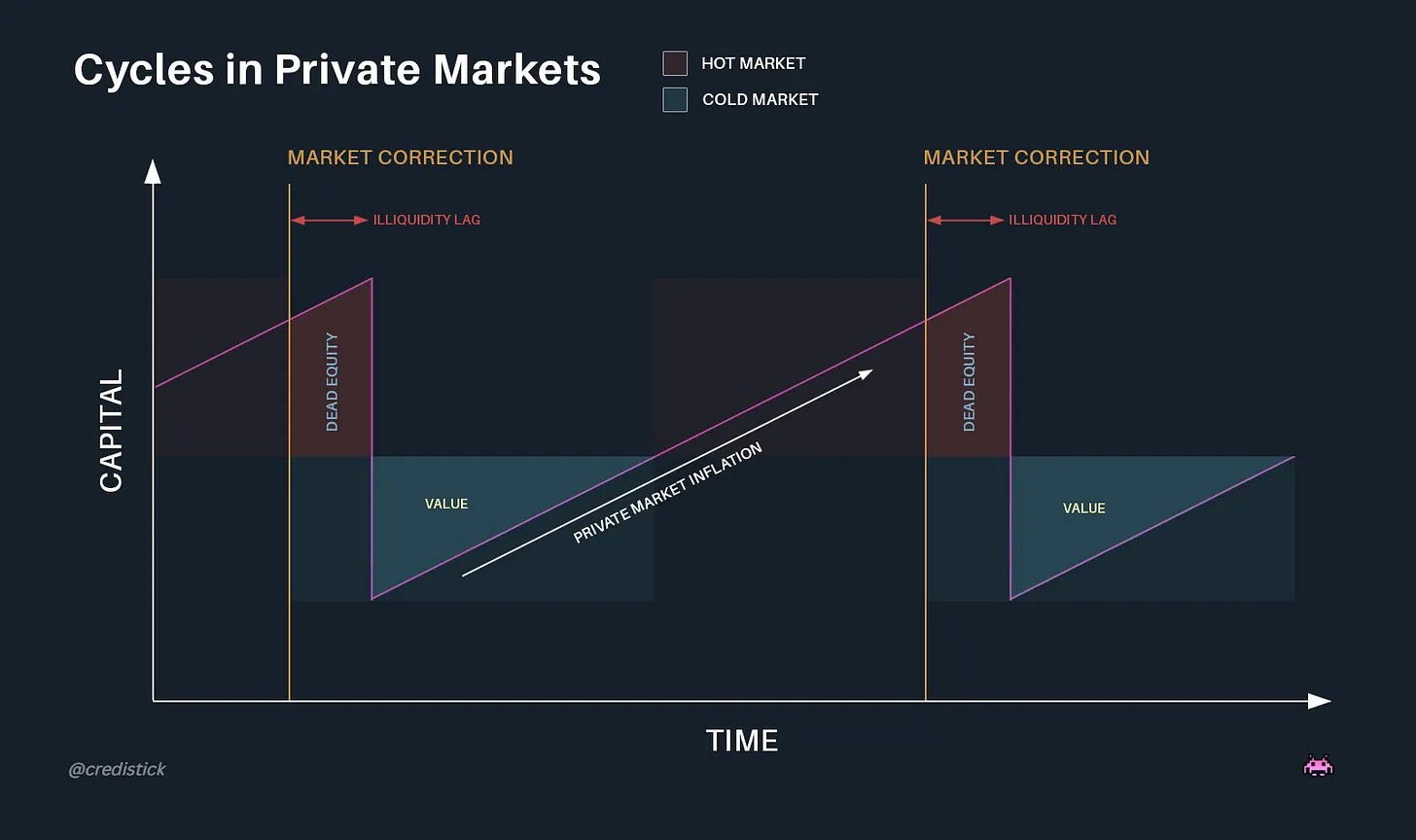

Private capital markets—like venture capital—oscillate between periods of liquidity surplus and scarcity. When these assets become liquid and outside capital floods in, euphoria drives up prices. Think newly listed IPOs or token launches. This newfound liquidity encourages investors to take on more risk, fueling a new generation of startups. As asset prices rise, investors shift capital toward earlier-stage applications, seeking returns beyond benchmark assets like Ethereum (ETH) or Solana (SOL).

This isn’t a bug—it’s a feature of the market.

Crypto market liquidity typically follows Bitcoin halving cycles. Historically, markets tend to rally within six months after each halving. In 2024, inflows from Bitcoin ETFs and Michael Saylor’s massive purchases—$22.1 billion last year—acted as supply "sinks" for Bitcoin. Yet, despite rising BTC prices, smaller altcoins haven’t seen broad-based recovery.

We’re now in a period where capital allocators face tight liquidity, attention is fragmented across thousands of assets, and founders who’ve spent years building tokens struggle to give them real utility. When launching meme assets is more financially rewarding than building actual products, who bothers shipping real applications? In previous cycles, Layer 2 (L2) tokens enjoyed premiums due to perceived value, driven largely by exchange listings and VC backing. But as market participants grow savvier, that perception—and its valuation premium—is fading.

The result? Declining L2 token values, limiting their ability to support small projects via subsidies or token revenues. Shrinking valuations force founders to revisit an old question: Where does revenue actually come from?

Such Transaction

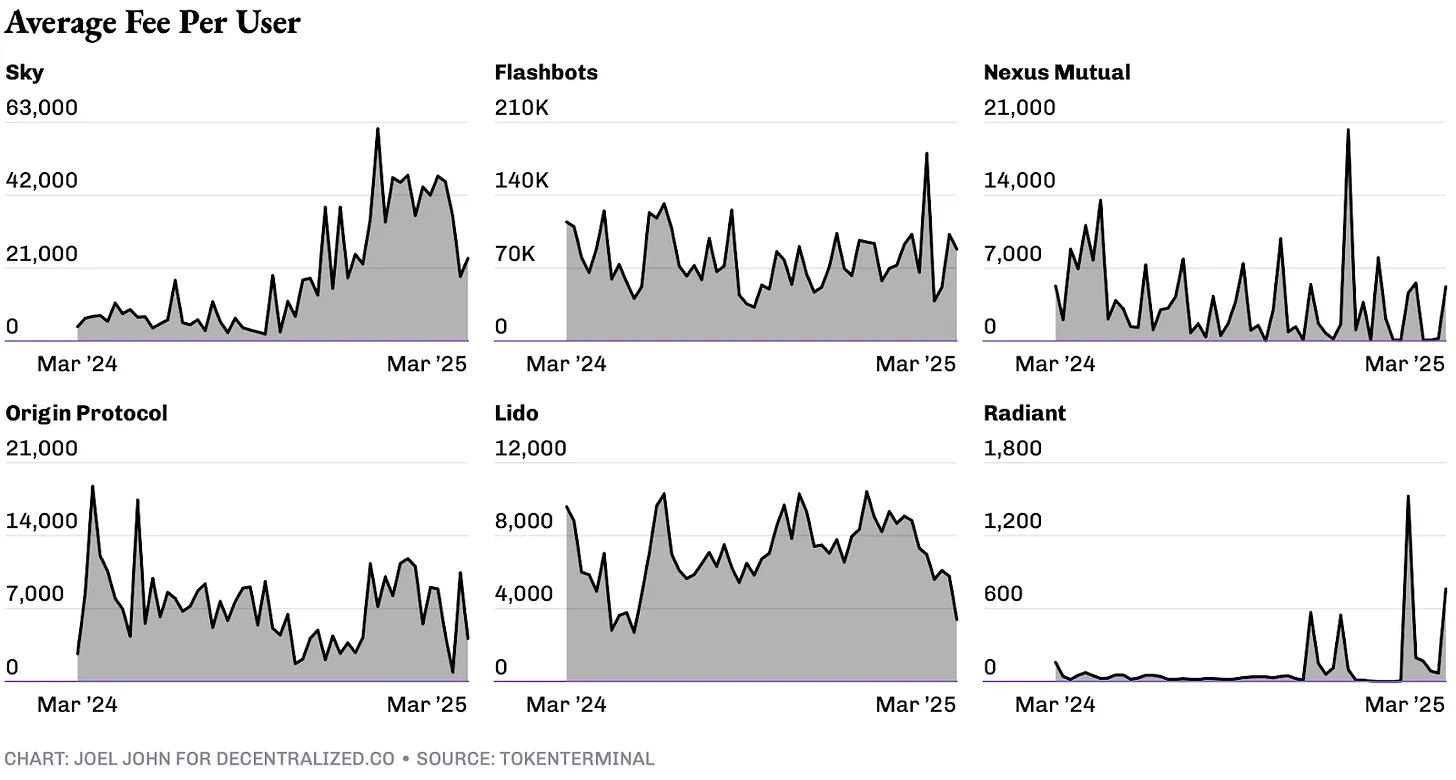

The chart above neatly illustrates how revenue typically works in crypto. From a revenue structure standpoint, most ideal crypto products resemble Aave and Uniswap. These have maintained steady fee income over years thanks to early market entry and the “Lindy effect.” Uniswap can even increase front-end fees to generate more revenue, showing deeply entrenched consumer preferences. Uniswap’s dominance in decentralized exchanges mirrors Google’s in search engines.

In contrast, FriendTech and OpenSea exhibit highly seasonal revenue. The NFT craze lasted two quarters; Social-Fi speculation burned out in just two months. For certain products, speculative revenue makes sense—provided it’s large enough and aligns with product intent. Many meme trading platforms have already joined the “over $100 million in fees” club, a scale most founders only dream of achieving through token sales or acquisitions. But such success remains rare.

Most founders aren't focused on consumer apps—they're building infrastructure, which has entirely different revenue dynamics.

Between 2018 and 2021, VCs heavily funded developer tools, betting developers would attract users. By 2024, two major shifts have occurred:

-

Unlimited scalability of smart contracts: Smart contracts enable infinite scaling with minimal human intervention. For example, Uniswap or OpenSea don’t need to proportionally grow their teams as transaction volume increases.

-

Advancements in AI: Progress in LLMs and AI reduces demand for crypto-specific developer tools. This category is at a pivotal turning point.

In Web2, API-based subscription models succeeded because of massive online user bases. In Web3, it’s a niche market—only a few apps reach millions of users. However, Web3 excels in “revenue per user.” Crypto users transact frequently and at high value because blockchains are inherently financial “rails.” Over the next 18 months, most businesses will likely pivot to directly capturing revenue from users via transaction fees.

This model isn’t new. Stripe initially charged per API call; Shopify used fixed subscriptions—but both eventually shifted to taking a cut of revenue. For Web3 infrastructure providers, this could mean lowering API barriers or offering free access until a certain transaction threshold is reached, then negotiating revenue shares. That’s the ideal scenario.

What might this look like in practice? Take Polymarket. Currently, UMA protocol tokens are used for dispute resolution, locked against cases. More markets mean higher dispute probability, directly increasing demand for UMA tokens. In a transaction-based model, required collateral could be a small percentage—say **0.10%**—of total wagers. If the presidential election market hits $1 billion in bets, that generates $1 million in revenue for UMA. Hypothetically, UMA could use this to buy back and burn its tokens. This approach has benefits—and challenges—we’ll explore shortly.

Another example is MetaMask. Its in-wallet swap feature has processed over $36 billion in volume, generating over $300 million in revenue. The same logic applies to staking providers like Luganode, which earn fees based on the size of user-staked assets.

Yet in a market where API costs keep dropping, why would developers choose one infrastructure provider over another? Why opt for a data oracle that requires revenue sharing? The answer lies in network effects. A provider supporting multiple chains, offering unmatched data granularity, and faster indexing of new chains becomes the go-to choice for new products. The same applies to transaction-based services like intents or gasless swaps. The more chains supported, the lower the cost and faster execution—the greater the likelihood new products will adopt it. Marginal efficiency gains not only attract but retain users.

Burn It All

Tying token value to protocol revenue isn’t new. In recent weeks, several teams have announced mechanisms to buy back or burn their own tokens using generated revenue. Notable examples include Sky, Ronin, Jito, Kaito, and Gearbox.

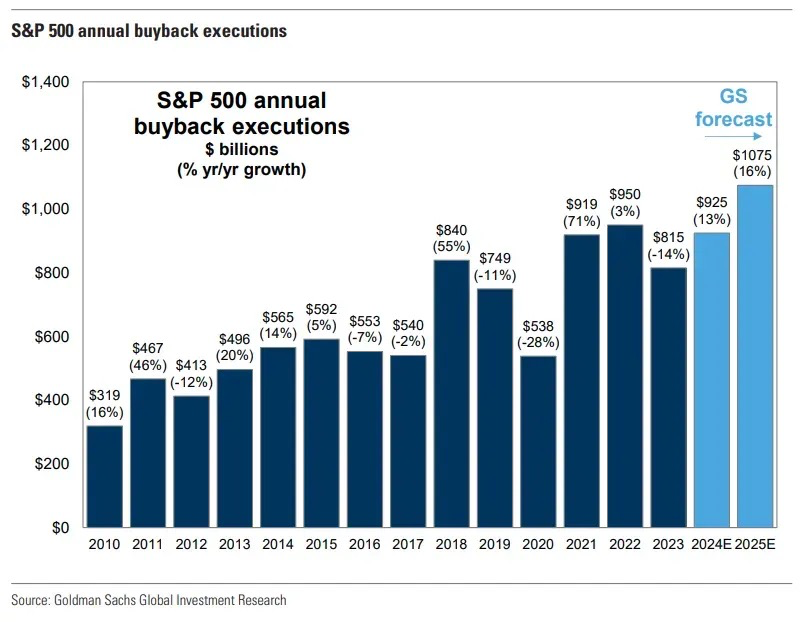

Token buybacks mirror stock buybacks in U.S. equities—a way to return value to shareholders (here, token holders) without violating securities laws.

In 2024 alone, U.S. stock buybacks totaled $790 billion, up from $170 billion in 2000. Before 1982, stock buybacks were effectively illegal. Apple has spent over $800 billion buying back its shares in the past decade. Whether this trend continues remains to be seen, but one thing is clear: the market is polarizing—some tokens have cash flows and reinvest in their value; others have neither.

For most early-stage protocols or dApps, using revenue to buy back their own tokens may not be the optimal capital allocation. One viable approach is allocating enough funds to offset dilution from new token emissions. This is how Kaito’s founder recently described their buyback strategy. Kaito is a centralized company using token incentives, earning centralized cash flow from enterprise clients, and using part of it to execute buybacks via market makers. The number of tokens bought back is double the amount newly issued, effectively putting the network into deflation.

Another model comes from Ronin. The blockchain dynamically adjusts fees based on transactions per block. During peak usage, part of the network fees flows into Ronin’s treasury. This controls supply without directly buying back tokens. In both cases, founders designed mechanisms linking value to economic activity.

In future posts, we’ll dive deeper into how these operations affect token prices and on-chain behavior. But for now, it’s evident: as valuations drop and less VC money flows into crypto, more teams must compete for marginal capital entering ecosystems.

Since blockchains are financial infrastructure, most teams will likely shift to revenue models based on a percentage of transaction volume. When that happens, tokenized teams will have strong incentives to implement “buyback and burn” mechanisms. Those who execute well will stand out in liquid markets—or they may end up buying back their tokens at extremely high valuations. The real outcomes will only be visible in hindsight.

Of course, one day all talk about price, yield, and revenue may become irrelevant again. Maybe we’ll return to throwing money at dog pictures or monkey NFTs. But for now, many founders worried about survival are having deep conversations around revenue and token burning.

Creating shareholder-like value,

Disclaimer:

1. Not investment advice.

2. Individuals associated with Decentralised.co may hold investments in CXT.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News