What Can We Learn from the Fall of friend.tech and Rise of Pump.fun?

TechFlow Selected TechFlow Selected

What Can We Learn from the Fall of friend.tech and Rise of Pump.fun?

Only time can reveal just how fleeting these games really are.

Author: Decentralised.Co

Translation: TechFlow

The Short-Lived Game

Earlier this week, friend.tech revoked the ability to change product fees or features. In plain terms—this product is unlikely to undergo any changes in the future. There might still be hope if the token holder network could influence product changes, but as of now, that’s no longer the case.

One appealing aspect of friend.tech was its ability to benefit users. As a wise person once said, the best way to rapidly grow a crypto community is to make your token holders rich. The friend.tech model allowed everyone to “be” a token and earn a share of revenue. To date, platform fees have generated nearly $98 million, half of which went to users. Sounds promising, doesn’t it?

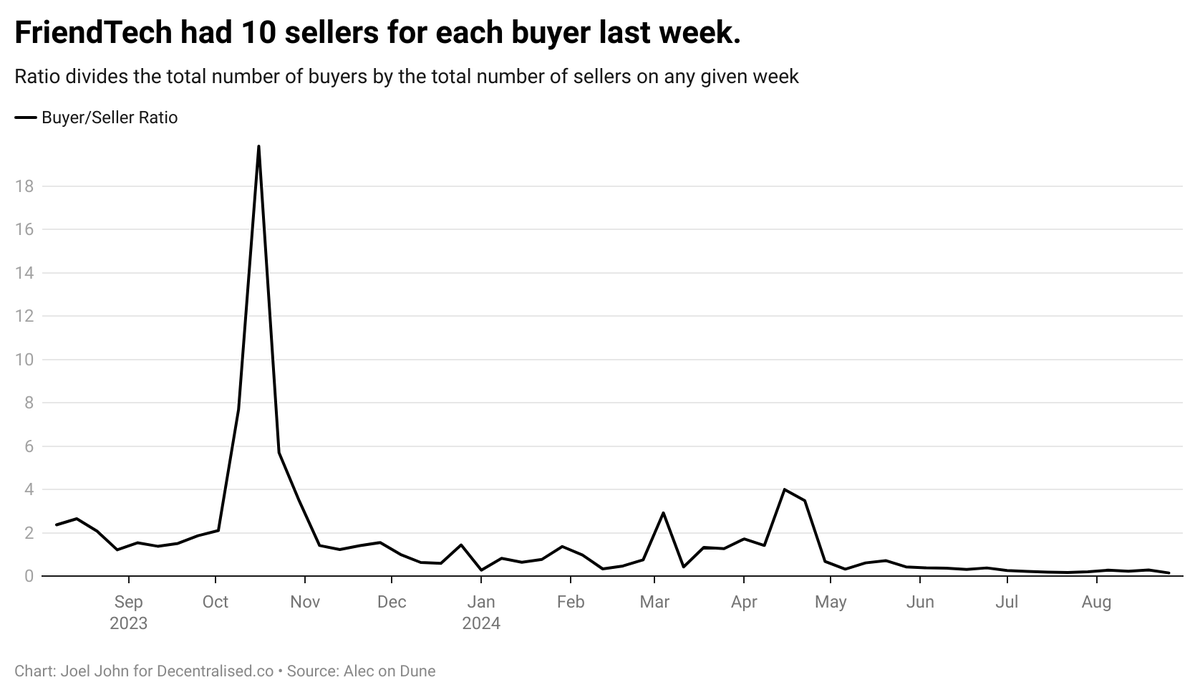

But not really. Problems with the friend.tech model were evident from the start. Before the token launch, data from DanielW_Kiwi on DuneAnalytics offered early clues as to why.

In October 2023, when friend.tech entered the mainstream, the product’s buy-to-sell ratio was 18:1. When there are 18 buyers for every seller, basic economics suggests prices will rise. By the time the token launched in May, this ratio had dropped to 0.32—one buyer for every three sellers. Last week, it fell further to 0.14.

Friend.tech can be classified as a short-lived game—a temporary system driven by financial incentives. For those hearing this term for the first time, a short-lived game refers to a short-term, financially motivated activity. Some products have even formed entire categories around this concept. Without a doubt, hashed_official comes to mind.

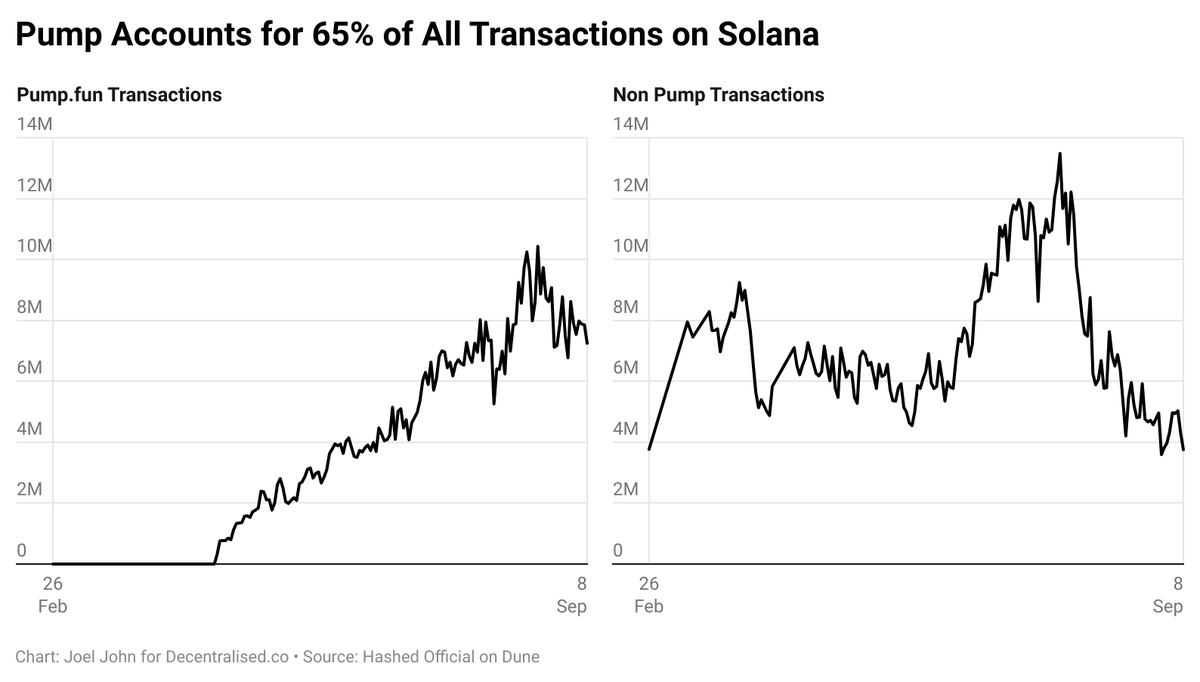

Pumpdotfun can be seen as the Costco of token launches—offering cheap, fast, and convenient access. According to data from hashed_official, the product launched in May and captured 65% of all DEX trading volume on Solana. Additionally, it has generated close to $100 million in revenue. To date, nearly 2 million tokens have been launched via pumpdotfun.

Pump has democratized token issuance. Previously, users had to go through centralized exchange listing processes; now Pump proves that leveraging DeFi infrastructure and on-chain liquidity works just as well.

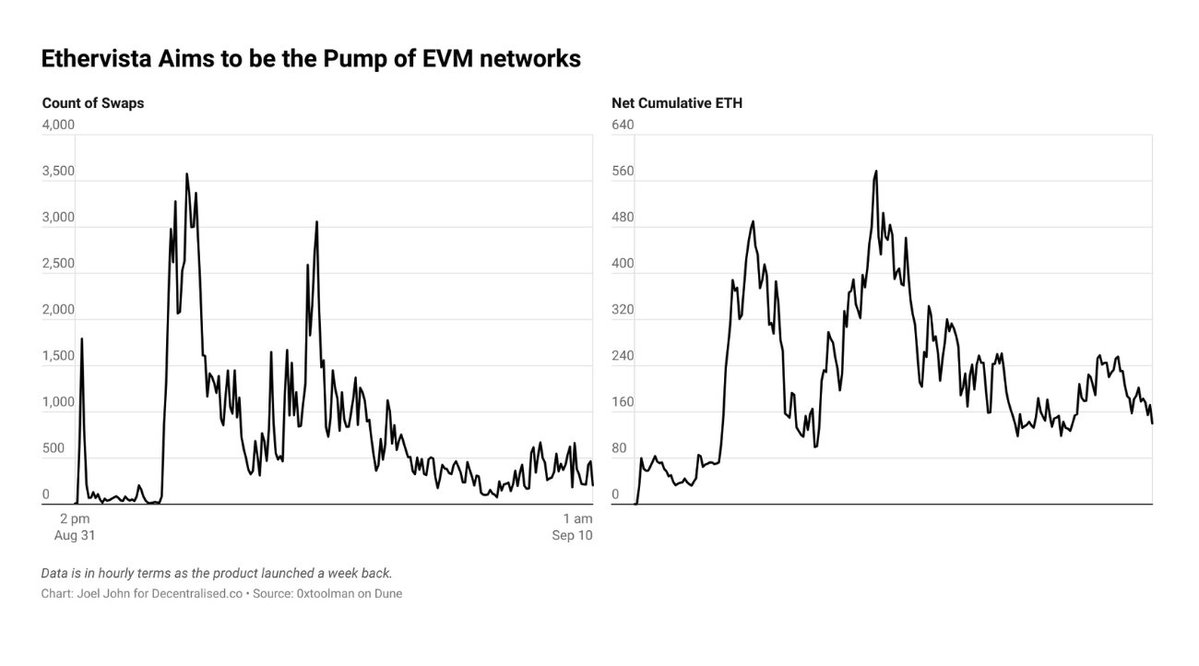

Clearly, this comes with risks. Token launches are often plagued by "rug pulls," where developers simply withdraw liquidity and dump the tokens held by users. Ethervista takes a different approach—it allows token issuers to earn a portion of trading fees in ETH, while liquidity providers (LPs) also receive ETH.

In 2023, LooksRare adopted a similar model with its platform fees, distributing LOOKS tokens to stakers. However, that story didn’t end well, as wash trading on the platform abruptly stopped. Ethervista also requires token issuers to lock their tokens for at least five days.

To date, activity on the platform has declined. According to Dune data provided by 0xToolman, transaction volume has dropped from 3,300 per hour to just over 160. The total ETH on the platform has fallen from 540 to 160 within a single week.

All of this raises the question: what are the rules of short-lived games? Are they merely short-lived, highly financialized Ponzi schemes that emerge and vanish quickly? Is a sustainable model even possible?

Essentially, these platforms share three characteristics:

-

Very high transaction frequency, clearly evident in Pump.

-

The "reason" for trading is often emotional. For example, you can't quantify why someone buys a meme coin on Pump. Volatility is the product.

-

They have a short half-life. By the time the token launched, the friend.tech community had already significantly shrunk.

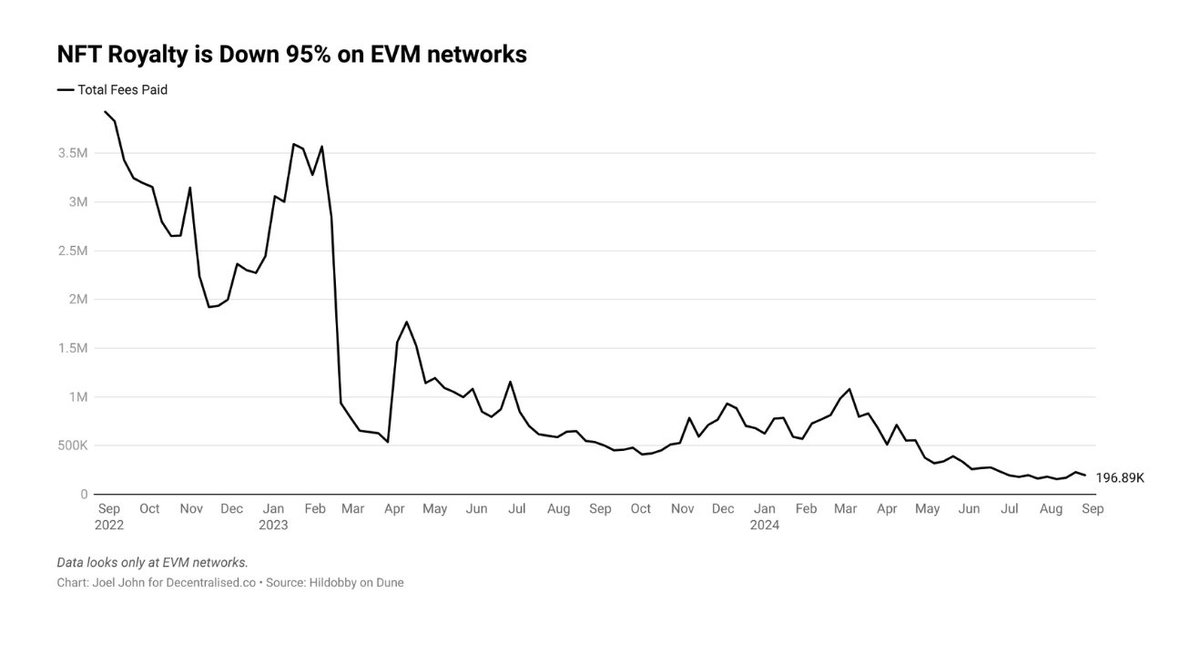

All of this reminds me of the golden age of NFTs. According to hildobby_'s Dune dashboard, average fees generated by NFTs (on EVM networks) dropped from over $3.2 million per day to $200,000—a decline of nearly 95%.

This model is interesting because it enables creators to continue earning royalties from their work and build meaningful communities. In contrast, the meme coin season of Q2 2024 was driven by celebrities promoting their own tokens, which often crashed 90% within weeks.

Products like Pump and Ethervista strip away the facade of traditional communities, building hyper-tradable products instead. In return, they pay creators.

Can such models scale? We remain uncertain about their sustainability. But if Pump and Ethervista point to a trend, it’s clear there’s market demand for volatility. As long as the market is willing to pay for these tokens and accept the associated risks, we’ll keep seeing them. Or, like ICOs and NFTs in previous cycles, they may gradually fade as market awareness of the risks grows. Only time will tell just how short-lived these games truly are.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News