ABM Tokenomics Fitting Model: How Token Economics Affects Token Value and Its Stability?

TechFlow Selected TechFlow Selected

ABM Tokenomics Fitting Model: How Token Economics Affects Token Value and Its Stability?

The dynamics of token economies are extremely complex. Using ABM models, we can get closer to understanding the intricacies of token economies by starting with the analysis of interactions among individuals and how tokens influence their behavior.

Written by: MUSTAFA, CARL

Compiled by: TechFlow

TLDR

6MV has developed several agent-based models to help research tokens and advise portfolio companies on token generation, launch, and mechanism design. We have modeled “infrastructure” economies that use utility tokens to reward service providers and are funded by user payments for services. These economies include Filecoin, Chainlink, The Graph, and Helium.

In this article, we introduce our methodology and share four early findings:

- Our research indicates that while macroeconomic shifts are the strongest driver of token price performance, token design decisions can help mitigate downside price pressure during bear markets.

- All else being equal, incentivizing supply-side participants is more effective than incentivizing demand-side participants. Adding service providers to the network increases stability and overall token prices.

- In our model, adjusting token issuance rates (e.g., deflation) did not materially affect protocol performance. Instead, we recommend protocols prioritize value drivers over using deflation to push token prices.

- For networks with staking, increasing staking rewards boosts retail investor participation and overall token market cap but also increases volatility.

When market conditions are favorable, many token prices are heavily influenced by speculation, making it difficult to assess whether a token’s economic design is effective. However, in adverse market conditions, uncovering deep, evidence-based insights becomes increasingly important to help protocols stabilize prices and enhance utility.

Because a comprehensive framework for token economics has yet to be established, our research team is building agent-based simulations of token economies to better understand and respond to different market conditions.

Introduction

The challenge in understanding token economics lies in grasping mechanism design. In economics, game theory studies the strategies and incentives present within a given game. Mechanism design, conversely, examines the inverse problem—how desired incentives and behaviors should shape the design of the game itself. Using this mathematical framework, we can view token economic design as designing a game where tokens serve as the primary tool to incentivize behavior.

However, unlike games, token economics operates as an open system susceptible to external influences, making it difficult to predict behaviors and outcomes within the ecosystem. Therefore, we need computational methods to better understand these complex relationships.

Our approach uses agent-based modeling (ABM), simulating individual agents with distinct characteristics. These agents are rational and dynamically respond to market conditions, enabling us to gain deeper insight into how token economies function.

Agent-Based Models vs. Other Methods

Machine Learning (ML) is currently the industry standard for predictive modeling. In simple terms, ML consists of correlation-based models trained on multiple data inputs. When applying ML to predict token economics, we can forecast token prices based on historical metrics such as user adoption rate, token price, token supply, Bitcoin price, and other real-world indicators.

By aggregating these input data points, the model uses weighted regression to predict token prices over time. These models are typically used for short-term applications such as social media analytics and short-horizon trading decisions. At timescales of seconds or milliseconds, user preferences or market trends are highly correlated with prior patterns. However, over longer periods, inherent biases in input data make predictions relatively unreliable. The randomness of macroeconomic trends, external shocks, and other factors are often difficult or impossible to quantify, creating gaps in ML's predictive power.

Using agent-based models (ABM), we can incorporate randomness and allow agents to act independently, without reliance on historical input data. This enables us to run and analyze hundreds of simulations and derive meaningful insights. Most importantly, ABM allows us to understand why certain outcomes occur. Through detailed output logs, we can investigate the causal relationships between agent behavior and market trends. In contrast, machine learning models only produce predictions without explaining the underlying reasons.

In summary, ABM offers the ability to assign diverse behaviors to different participants, enables longer-term forecasting, does not require collecting, storing, and labeling millions of data points, and allows inference of causality through analysis of output logs.

Model Design

Overview

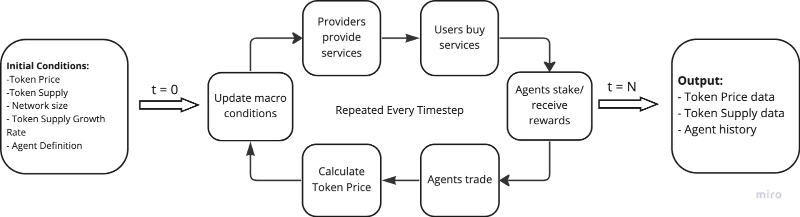

Our ABM is designed for “infrastructure economies,” where providers deliver services to users, such as Helium, Filecoin, and Chainlink. This structure easily translates into distinct categories of incentivized agents. Users pay service fees, while providers receive token rewards to cover costs and maximize profit. All agents also speculate according to market trends to maximize returns. We include two types of investor agents—institutional and retail investors—who do not directly participate in the network but buy/hold/stake/sell tokens for profit.

To initialize our simulation, we set a series of "initial conditions," including token price, token supply, and network size. The simulation then enters a loop phase where events unfold and agents transact. Each cycle represents one day, repeating until the specified total number of days is reached. The model outputs daily simulation data, including agent behavior, token price and supply changes, and market conditions.

Users

In the simulation, user parameters are defined as probability distributions, including capital amount and risk tolerance. This reflects their behavioral traits in the market—some agents prefer high-risk, high-return actions, while others adopt more conservative strategies. At each time step, users pay service fees, evaluate the market, and decide whether to buy or sell tokens based on current price, personal risk tolerance, recent token trends, and past actions.

Providers

Providers also act as agents, entering the simulation with risk tolerance, capital, and a percentage of total network computing power—representing the “service volume” they provide. Their incentives differ from users, as they are more likely to sell tokens at any time step to cover operational costs. Providers assess the same market and macro trends as users and are influenced by similar input factors.

Investors

Investor agents consist of two types: retail and institutional investors. Retail investors do not participate in the protocol as intended but instead speculate on tokens for profit. They use similar indicators when determining trading strategies, including macro trends, token price, past behavior, and profit/loss records. Institutional investors may face token lock-up periods and have investment goals differing from retail investors. Their decisions are influenced by various factors, including purchase price, selling propensity, lock-up duration, and required return rates.

Network Growth

Agents continuously enter and exit the economic system based on changing probability distributions and token price trends. We assume sustained price growth encourages more providers and users to join, and vice versa. The exact network growth parameters vary by protocol, and we tailor our model using real-world data.

Model Calibration

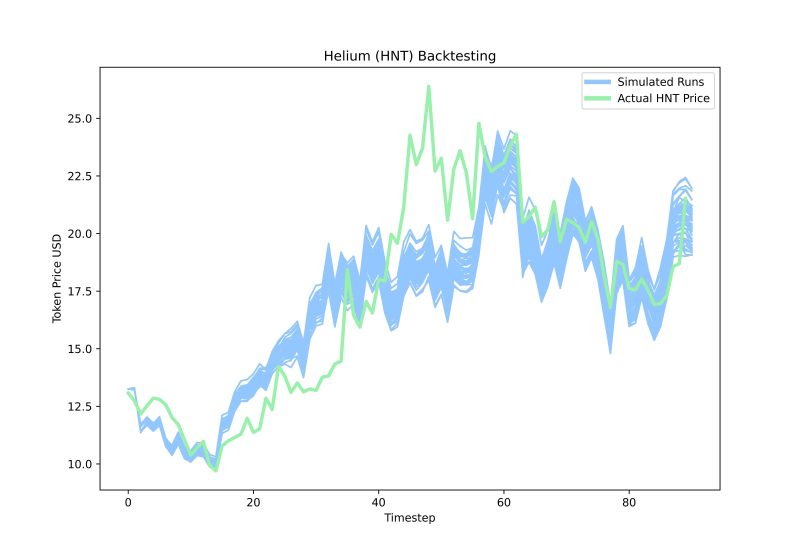

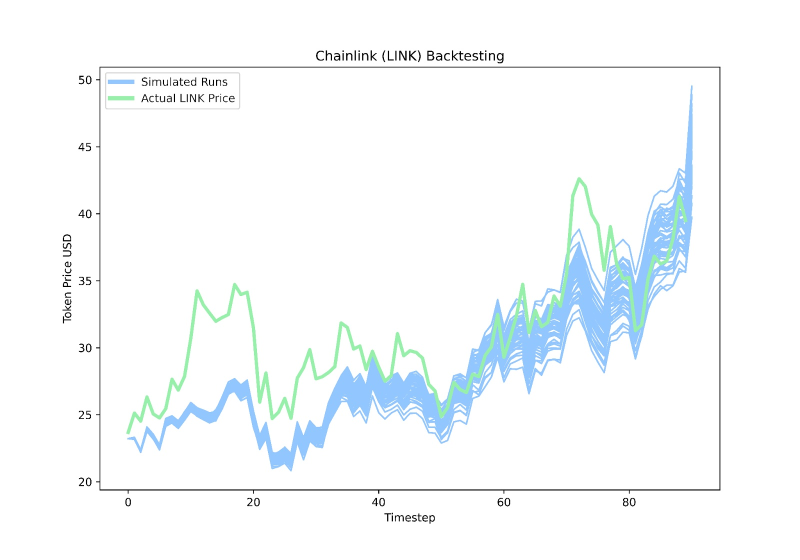

We calibrated the model through backtesting over the past 90 days. This iterative process involves setting initial conditions, running simulations, and comparing results with actual data. Our goal is to build a model that minimizes overfitting while accurately describing various real-world infrastructure protocols. We backtested against three major infrastructure economies: Helium (HNT), Filecoin (FIL), and Chainlink (LINK).

We use two metrics to evaluate model performance: token price correlation and relative price movement pattern match. Our model demonstrates broad accuracy across these metrics, giving us confidence in the defined mathematical relationships. This confirms the model’s ability to simulate real token price fluctuations in response to macro market conditions and network adoption.

Case Studies

Our initial model includes several configurable parameters: market trend, token issuance rate, network growth, and staking rewards. A natural starting point is experimenting with these parameters.

The strength of ABM lies in its ability to model complex parameter interactions. For this preliminary work, we isolated each parameter to understand its impact on the overall economy, yielding insights into different tokenomic design choices.

The Control Case is an inflationary economy with an initial supply of 15 million tokens and approximately 100,000 tokens minted monthly, equivalent to an 8% annual inflation rate. Given the inflation rates of other infrastructure-type economies and popular tokens, we consider this a reasonable baseline. We initialized 10,000 active users and 1,000 providers at a 10:1 ratio, based on Filecoin’s approximate 35,000 active users and 4,000 providers. For each run, we also initialized 1,000–2,000 investors. We used ETH as a proxy for crypto market sentiment, as both ETH and BTC closely track macro movements.

Each experiment was run 25 times, simulating 90 days per run. The shorter timeframe captures finer details of the simulated economy and focuses on immediate experimental outcomes. For each experiment, we altered one key parameter and analyzed the results.

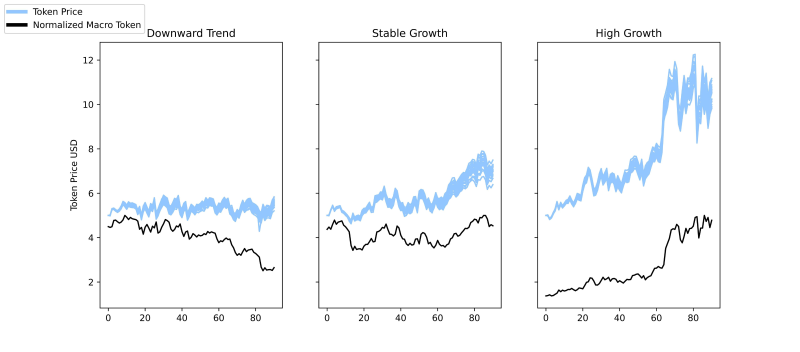

Case Study 1: Impact of Crypto Market Trends

Over the past year, cryptocurrency markets have been largely correlated with macroeconomic trends. With ABM, we can dive deeper to understand the extent and intensity of this influence under various market conditions.

We varied only the “crypto market trend” parameter:

In other case studies, we used the same set of real ETH price data for each run. In this study, we varied these subsets, selecting three different 90-day historical ETH price periods: downtrend, stable growth, and high growth. We found that macro trends are highly correlated with the price movements of our simulated token.

Even in extreme scenarios—such as strong deflation or very high staking rewards—with identical initial conditions and parameters except for macro trends, we still observed a high correlation between L1 token movements and our token price. Reviewing other case studies, the impact of market movements remains evident even under extremes. We clearly observe agents strongly influenced by overall market sentiment and trading accordingly.

This influence might suggest token design has little effect on actual outcomes. However, we believe the reality is more nuanced. While macro trends cannot be fully mitigated, poor token design accelerates bear market collapses, whereas smart token design enhances stability and price performance—even in volatile markets. The benefits of good token design make this discipline worthwhile, empowering protocol designers with greater control over their networks across varying macro environments.

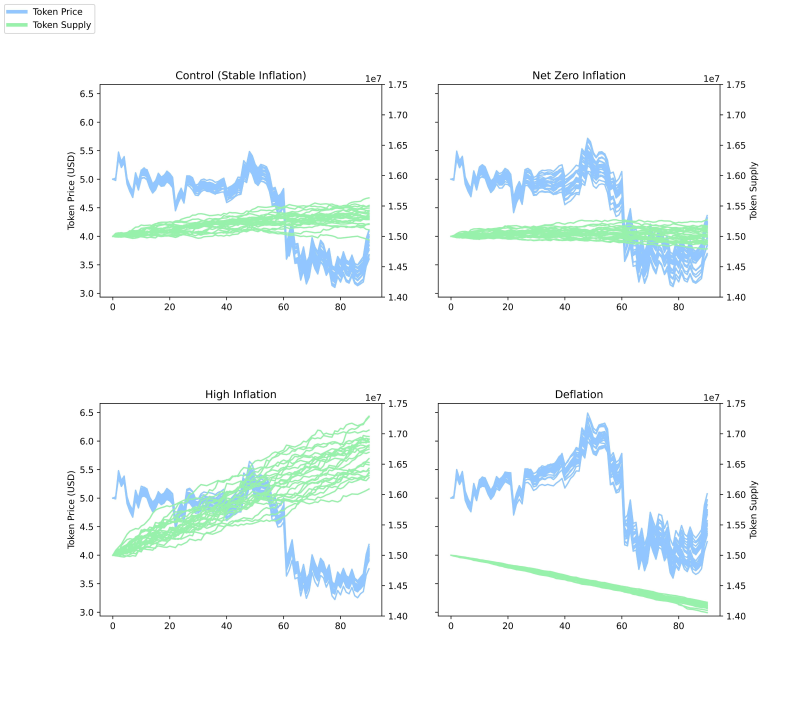

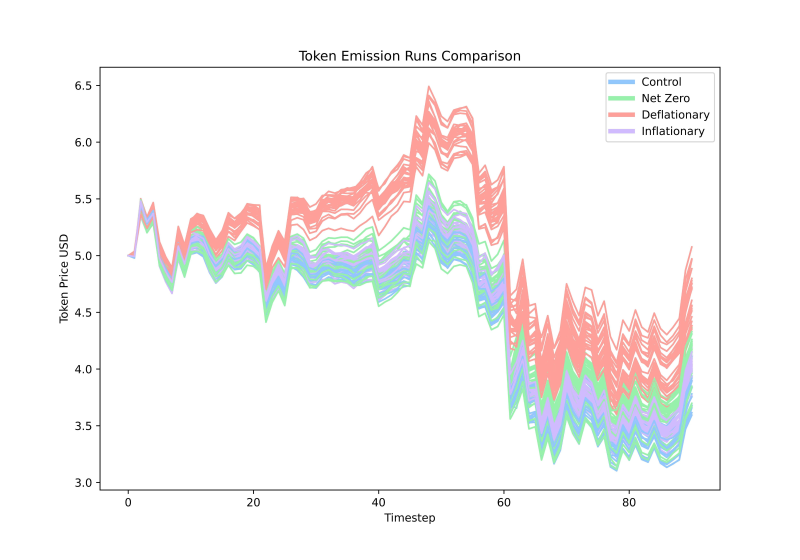

Case Study 2: Token Distribution Schedules

A key component of token design is inflation rate. A common approach is to increase token issuance to a maximum before transitioning to deflation or stabilization. Other protocols may use algorithmic equilibrium, burning tokens to offset fluctuations in minting rates. We categorized these into four types: high inflation, stable inflation (our control group), zero inflation, and deflation.

Through simulation, we found the control group (~+8% inflation) exhibited the highest stability. High inflation (~+37%) slightly reduced token price but did not significantly harm stability, while deflation (~-37%) led to a slight price increase but lower stability.

Surprisingly, these results contradict intuitive scarcity assumptions in tokenomics. Making tokens deflationary increased scarcity, yet we saw only a marginal price uplift and slightly reduced stability. There was no significant difference in token price between zero and high inflation runs, though we noted slightly improved stability under high inflation. This may be because a short 90-day simulation fails to capture long-term inflation effects on token prices.

Following Ethereum’s merge, it became a deflationary asset, yet its price did not sustainably rise—instead falling due to strong external shocks in the crypto market—mirroring our model’s findings. We note some tokens adopt inflationary or deflationary strategies. Overall, we discourage token designers from treating issuance rate as a primary driver of price growth, and instead encourage focus on incentive alignment. What specific behaviors should the token incentivize? Which behaviors could harm your economy? How can the token mitigate negative impacts? Without answering and implementing these foundational questions, the practical impact of issuance rate on token price will be minimal.

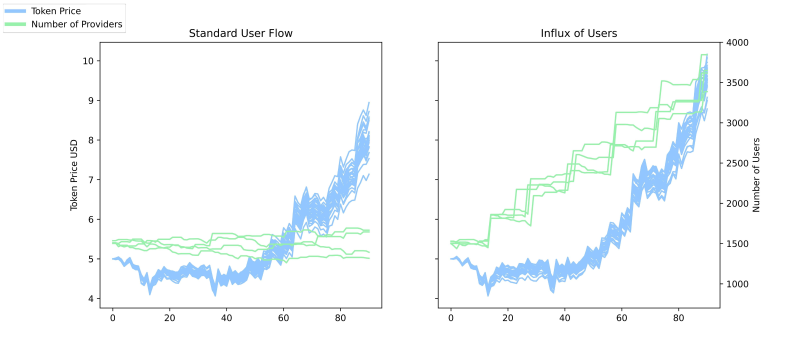

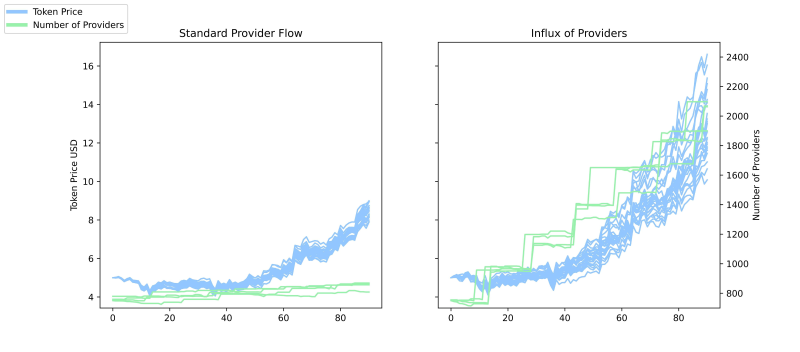

Case Study 3: Impact of User and Provider Adoption

In two-sided markets, a persistent question is: which side should be incentivized? In our simulated infrastructure economies, it is useful to understand whether growth in users or providers benefits the economy more. We ran two simulations, adjusting the “network growth” parameter to introduce waves of either providers or users.

We found that increasing providers led to higher token growth and slightly lower stability, while increasing users resulted in significantly less token growth but slightly higher stability.

These trends can be explained by dynamics between users and providers: when provider numbers increase, it attracts more stable new users, leading to rising token prices across most runs. When simulating large influxes of new users, the number of providers entering the economy was about 23% lower compared to proportionally introducing new users.

Clearly, any protocol must balance user and provider growth. Depending on the business, one may be prioritized over the other. Our results indicate that in infrastructure economies, introducing providers has a greater impact than introducing users.

Token designers in infrastructure economies should carefully consider how to incentivize users and providers. For example, provider rewards should attract sufficient participants without causing underutilized surplus resources that lead to failed provider investments.

For instance, a common issue in Filecoin’s 2020 model was insufficient liquidity and user traffic to support storage providers’ financial needs. By overemphasizing provider inflow, the network suffered inefficient utilization, negatively impacting token price performance. Similarly, user growth should be carefully incentivized to match network capacity, avoiding demand surges exceeding provider capabilities.

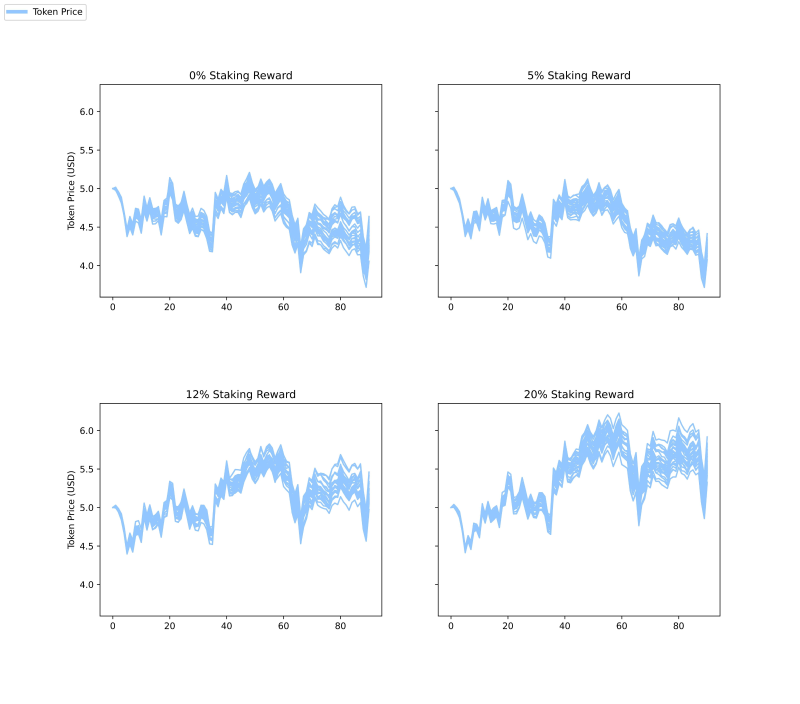

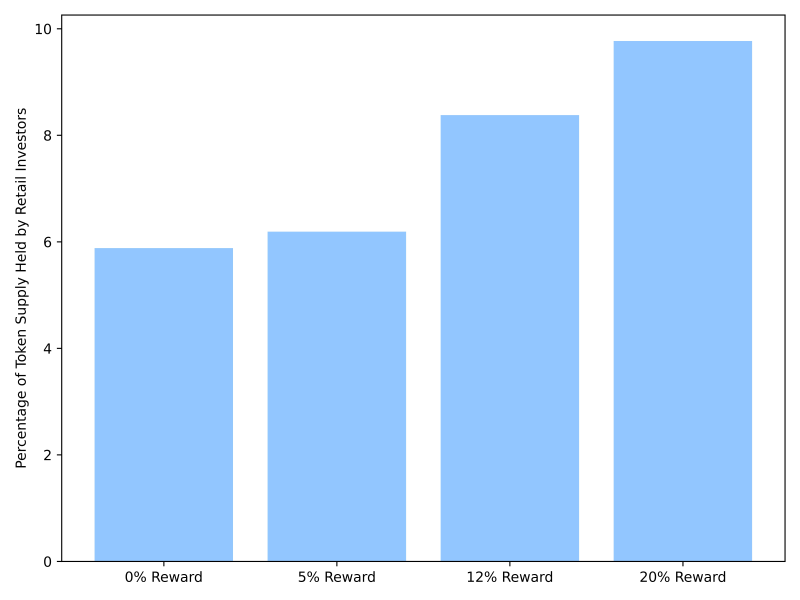

Case Study 4: Varying Staking Rates

Staking allows token holders to lock up tokens for a period to earn additional rewards. In our model, token holders can stake at each time step. Their decision depends on expected returns, opportunity cost of locking funds, and other factors like market trends and past behavior. To study the impact of different staking incentives, we varied staking yields between 0%, 5%, 12%, and 20%.

As expected, in models with no staking rewards, no agents chose to stake. We found that increasing staking rewards to 5% had little impact on token price or stability. Increasing rewards to 12% and 20% both boosted token prices, but the 20% scenario showed higher instability.

As staking yield increases, network growth accelerates and wealth flowing through the economy rises, naturally driving up token prices. However, we also observed increased speculative trading and a higher number of retail investor agents, resulting in lower stability under 20% staking yield.

These results suggest a “sweet spot” in staking rewards, where protocol designers must balance capital inflow against increased speculation. In our experimental economy, 12% was closest to this sweet spot, delivering clear token price growth with minimal loss in stability. When using our simulation as a consulting tool, we can scan more staking levels or simulate alternative reward schemes for higher analytical precision.

While 12% offers network growth with minimal stability loss, this does not mean every protocol should adopt 12%. For example, early-stage protocols may want to minimize retail investor participation to focus on core network users and providers, and may benefit from keeping tokens liquid with low or no staking incentives. We recommend protocols monitor the proportion of speculative activity within their economy and consider staking adjustments to incentivize their desired mix of token holders.

More broadly, we encourage protocols to offer stakers utilities beyond financial APY—such as greater governance weight, contributions to network security, and other intangible rewards. Staking motivated purely by financial gain, especially in emerging protocols, may distort fundamentals and attract speculative liquidity that exits once rewards decrease.

Conclusion and Outlook

The dynamics of token economies are extremely complex. Using ABMs, we can move closer to understanding this complexity by analyzing interactions among individuals and how tokens influence their behavior.

We follow the well-known adage: “All models are wrong, but some are useful.” The most critical step in creating predictive models is clearly understanding their limitations and assumptions. Some shortcomings of this initial model may include the 90-day runtime and calibration based on only three tokens. As we expand our experimentation, we will refine these assumptions and strive to add new agent types, agent capabilities, and protocol designs.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News