Will uncollateralized lending become the next growth explosion in DeFi?

TechFlow Selected TechFlow Selected

Will uncollateralized lending become the next growth explosion in DeFi?

This article will introduce you to this groundbreaking innovation—unsecured lending racing toward efficiency.

Author: cs361

Compiled by: TechFlow

Innovations in AMMs have driven the explosive growth of the DeFi industry, increasing from $500 million in the previous cycle to just under $20 billion today—an astonishing 400-fold surge.

What if I told you we're on the brink of another innovation that could have a similarly transformative impact? This article introduces you to this breakthrough innovation—unsecured lending racing toward efficiency.

Credit markets are key drivers of economic growth and central components of efficient financial systems. In TradFi, there are both secured and unsecured loans.

Secured loans require collateral assets such as real estate, vehicles, or stocks, with loan-to-value ratios around 110%. Due to minimal counterparty risk, these are low-risk instruments.

Unsecured loans carry higher interest rates and are backed solely by credit scores, without collateral.

While secured lending is already part of DeFi (albeit with high borrowing costs), the absence of unsecured lending remains a major bottleneck. Why has introducing this century-old tool onto blockchains been so difficult?

Default Risk

In the traditional world, professionals exist to "know your customer" and manage credit, but this contradicts DeFi's principles of automation, transparency, and non-discrimination.

Slower Speed

Any additional checks on borrowers significantly slow down loan approval times. Currently, over-collateralized lending offers extremely fast approvals—a unique selling point for DeFi.

Lower Liquidity/Flexibility

Most borrowers are only interested in predictable fixed-rate and term loans. But in this highly active market, few lock up their assets for long periods.

Regulatory Risk

Offering unsecured loans draws regulatory scrutiny to the protocols providing them, especially given the PTSD left by the 2008 financial crisis.

Loan-Specific Risks

• Real-world asset and NFT lending—asset liquidity;

• Credit scoring—scarce on-chain data, and anyone can create unlimited wallets;

• Off-chain credit integration—dependent on TradFi infrastructure;

......

Despite the risks and challenges, many protocols offer under-collateralized loans in some form.

As with most problems, multiple potential solutions exist. Let’s examine the most promising paths, what issues they solve, and what challenges remain unresolved.

1. zkKYC

Using zero-knowledge proof KYC ("know your customer") enables identity verification without pre-sharing personal information with counterparties. Lenders can verify borrower creditworthiness through validity proofs on issued zkKYC tokens.

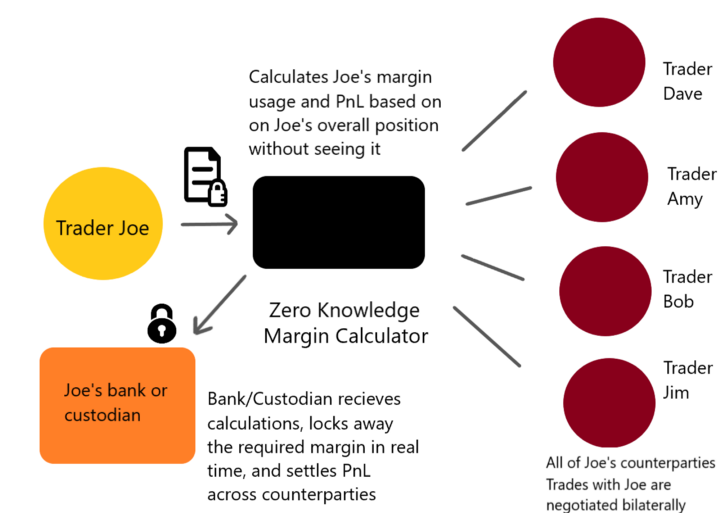

The Credora Platform leverages this technology to achieve efficiency through disintermediation. It transforms traditional clearing structures by offering a ZK margin calculator that sends margin and settlement instructions to custodians.

This implementation of zkKYC is not decentralized and focuses instead on institutional markets. However, maintaining centralization offers certain benefits and still represents a significant improvement over conventional clearing systems.

2. Debt Tokenization

Tokenizing debt makes it fungible, enabling trading and freeing up capital for lenders. This may also address maturity mismatches and allow fractionalization, increasing the number of potential investors/lenders.

ERC-20 tokens representing debts owed by institutions serve as ideal investment vehicles for private investors seeking safe returns. In the case of zero-coupon bonds, debt tokens appreciate in value until maturity.

3. Proxy Accounts

This solution works best for providing unsecured loans to retail users without requiring KYC. Borrowers deposit collateral and receive a proxy smart contract through which funds are lent.

Funds remain under borrower control, but since the proxy account is restricted to specific protocols and withdrawals are disabled, it prevents borrowers from absconding with the funds. Trust is enforced at the code level by limiting functionality within the proxy account.

In summary, zkKYC stands out as the most promising comprehensive solution, as it provides both institutional and individual participants with access to lending.

For investors, the optimal way to earn yield from loans is purchasing tokenized debt at a discount and either holding to maturity or selling early. Retail users can borrow funds via proxy accounts and interact with top protocols using leverage. On GearboxProtocol, these include Curve, Uniswap, Sushi, and Yearn.

Other solutions include:

- Contract-to-contract lending—largely untapped: flash loans (non-traditional lending);

- (Social) default recovery funds—using multisig funds to guarantee repayments;

- Native token incentives;

Building a secure and efficient debt issuance infrastructure will attract sticky capital into the market, becoming part of the shift of the $70 trillion global lending market onto blockchains.

I don’t believe full decentralization will prevail here, as traditional companies need a regulatory framework to enable this transition. As more protocols experiment with unique loan issuance models, it will be fascinating to observe the evolution of this sector.

Finally, my conclusion is:

Unsecured lending is leveraged. It contributed to the 2008 financial crisis and pushed the global economy to the brink of collapse.

Therefore, if we get it right, it will solidify DeFi’s position within this economic system. But if we fail, we face severe regulation—possibly until it disappears entirely.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News