SupraOracles: Asset Tokenization and Financialization with Decentralized Oracles

TechFlow Selected TechFlow Selected

SupraOracles: Asset Tokenization and Financialization with Decentralized Oracles

Oracles expand trust and improve efficiency in the transition of traditional asset ownership and in trading digital assets on secondary markets.

By SupraOracles

Oracles expand trust and improve efficiency in the transition of traditional asset ownership and in trading digital assets on secondary markets.

Securitization is the process of designing financial instruments for illiquid assets that can be sold on secondary markets and may generate returns for owners. For example, mortgage-backed securities (MBS) are a common type of tradable security backed by large pools of individual home loans, which are typically illiquid. These securities are tailored to various risk tolerances based on borrower creditworthiness and investor time horizons.

After lenders originate mortgages, the loans are pooled together as collateral. These mortgage notes represent borrowers' commitments to make monthly payments. To diversify counterparty risks associated with mortgages—such as borrower default—loan underwriters sell MBS products to investors, who receive a portion of the mortgage repayments if loans are repaid, and share losses in case of defaults.

In Web3, tokenization essentially refers to the same process, except that securities are minted as NFTs on a blockchain and recorded as verifiable cryptographic assets on a digital ledger. As such, disregarding the current total market cap of cryptocurrencies, NFTs could arguably be more liquid than traditional securities. NFTs can be traded globally 24/7 and are protected as immutable assets through blockchain technology. Additionally, tokenized assets can embed smart contracts—for instance, dividend payouts similar to those in traditional securities.

Billions of dollars in securities and commodities have already been tokenized, and the market capitalization of tokenized fiat currencies (stablecoins) has reached tens of billions. Ultimately, once certain technical, legal, and social barriers are met, any asset could be tokenized and traded on crypto rails.

Of course, several obstacles remain, including regulatory clarity, Web3 adoption, blockchain scalability, and interoperability issues. Moreover, it remains unclear how institutions maintaining the status quo—built around centralized, regulated intermediaries—will respond to decentralized initiatives.

This article aims to summarize how Web3 tokenization will disrupt traditional securities markets by leveraging three key Web3 technologies: blockchains, NFTs, and oracles.

Tokenizing Traditional Assets on Blockchains

A notable example of tokenizing physical assets is Aspen Coin, a digital security representing partial ownership of the St. Regis Aspen Resort in Colorado. By tokenizing the Aspen REIT, investor entry barriers are lowered compared to publicly listed REITs, which require higher setup costs and larger minimum investments. Consequently, while traditional REIT holdings tend to have longer holding periods and relatively lower liquidity, tokenized Aspen Coins offer greater accessibility and flexibility.

Tokenizing real estate on blockchains reduces administrative friction in transactions and creates assets accessible on a global, 24/7 marketplace. This enables faster asset transfers and lower transaction fees.

Since tokens are divisible and can be bought and sold thousands of times per day, investors can purchase small fractions of tokenized assets, enabling shared ownership that previously required substantial capital investment. While such capital was historically illiquid, its tokenized form becomes highly liquid.

While this may impact real estate markets in terms of short-term price volatility, fractional ownership through tokenization offers younger generations fairer opportunities to take their first step into property ownership without being priced out by large down payments.

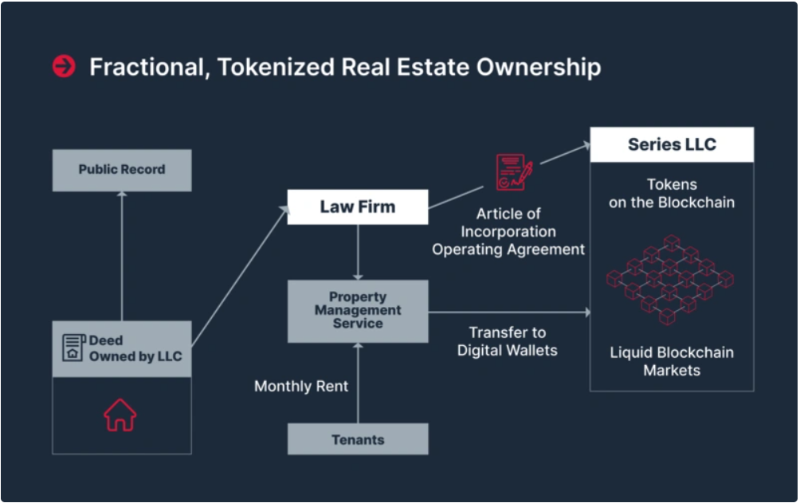

An example of tokenized luxury real estate is Aspen Coin, which pays dividends to token holders, giving them a percentage of passive income generated from the physical property. If more tokens like Aspen Coin become commonplace, they could level the playing field for retail investors and increase economic opportunities for millions worldwide who currently cannot afford real estate. The physical property is owned by a “Series LLC,” the same entity that mints tokens on the blockchain for retail investors to trade on secondary markets.

The physical real estate is owned by a “Series LLC,” the same entity that mints tokens on the blockchain for retail investors to trade on secondary markets.

By establishing an LLC to own the property, both physical and digital ownership operations can proceed while complying with established real estate ownership standards and liability regulations.

Smaller investors now gain access to passive income opportunities without facing insurmountable barriers at the point of initial investment. Such arrangements also distribute counterparty risk, encouraging healthier investment attitudes and diversified strategies.

Creative works such as music, art, films, or video games can also be tokenized as NFTs. This may seem trivial, but creating a unique, non-fungible version and preserving its uniqueness and immutability via blockchain ledgers in the digital world is groundbreaking. First, it prevents unauthorized copying and sharing—essentially theft of creators’ rights—that bypasses direct compensation or royalty mechanisms.

NFTs can also be financialized: Creators can earn not only from the original sale of an asset but also receive royalties on future secondary sales. This means creators will be able to monetize their creativity online more effectively. Thus, transforming NFTs into yield-generating financial instruments establishes robust, trustless, and flexible financial arrangements between content creators, consumers, and investors.

Oracles and Financialization: Web3 Technologies Empowering Us All

Oracles are crucial for acquiring and verifying external data for tokenized assets. They serve as communication channels between blockchains and off-chain data sources. Since tokenized assets often require knowledge of real-world conditions—such as occupancy rates at the Aspen Resort—oracles will play a key role in tracking ownership and the physical condition of tokenized assets.

Moreover, any creative work that can be represented digitally can be expressed as an NFT. Doing so provides immutable, transparent timestamps and copyright declarations for tokens on public blockchains. More importantly, tokenized assets may unlock new monetization capabilities for artists and knowledge workers through embedded smart contracts.

Decentralized oracles can provide secure performance analytics and content access control, allowing original creators to exercise sovereignty over their content and permissions. As such, oracles help original content creators unlock the latent value of their productivity using verified revenue models—such as cost-per-impression (CPI), cost-per-click (CPC), cost-per-lead, time-on-site, subscriptions, and more.

This makes oracles essential to the proper functioning of tokenized assets. If oracle nodes are compromised, digital assets might deviate from their spot value or fail to adequately distribute dividends to token holders. With this in mind, we can conclude that oracles represent potential single points of failure if not properly secured and decentralized. Deterministic smart contracts are irreversible, requiring the freshest possible raw data.

Web3 and secure digital ownership support new monetization strategies, enabling content creators to fully harness their productivity.

Oracles also help make tokenized assets—like NFTs—more productive through financialization. In fact, most real-world assets may eventually be priced with the help of oracles. By applying performance tracking metrics and pricing data via oracles and blockchains, non-productive assets can be transformed into revenue-generating digital assets.

For example, dynamic NFTs can be minted by creators, sold with immutable ownership recorded on the blockchain, and confer privileges that evolve or decay over time. Financialized NFTs will also allow creators to borrow against the future revenue potential of their creations and profit through perpetual royalty models. Likewise, fans of creators can support them more directly, free from gatekeeper interference.

Accelerating Broad-Scale Asset Tokenization

First, blockchain technology is still in its infancy, meaning misconceptions persist and it has yet to win full trust from traditional stakeholders. That said, early cryptocurrency adopters recognize blockchain’s potential in facilitating human collaboration and financial inclusion.

However, concerns about network attacks and other destabilizing or unexpected disruptions remain, implying initial resistance. Once data security and privacy issues are resolved and adoption gradually increases, this challenge will become less daunting.

Although blockchains can tokenize physical and digital assets, interoperability between blockchains and legacy systems must be secure and seamless. Assets should be able to move freely across blockchains or be redeemed in physical form without being trapped in siloed networks.

Furthermore, tokenization of traditional assets requires clear and strong regulations before going mainstream. For instance, in the U.S., the SEC and CFTC continue to evaluate regulatory frameworks for cryptocurrencies, DeFi entities, NFTs, and other digital assets. SEC Chair Gary Gensler has stated that whether a digital asset is considered a security depends on whether it represents a traditional security.

Beyond the SEC's cautious stance and bullish signals from governments in Russia and India, it remains to be seen when clearer regulatory language will be codified. Regulatory transparency and clarity will help balance innovation with safety and the rule of law, encouraging broader adoption among those waiting for legal safeguards. Additionally, the World Economic Forum has called on governments worldwide to act, implement regulatory infrastructure for digital currencies, and prepare to launch their own central bank digital currencies (CBDCs).

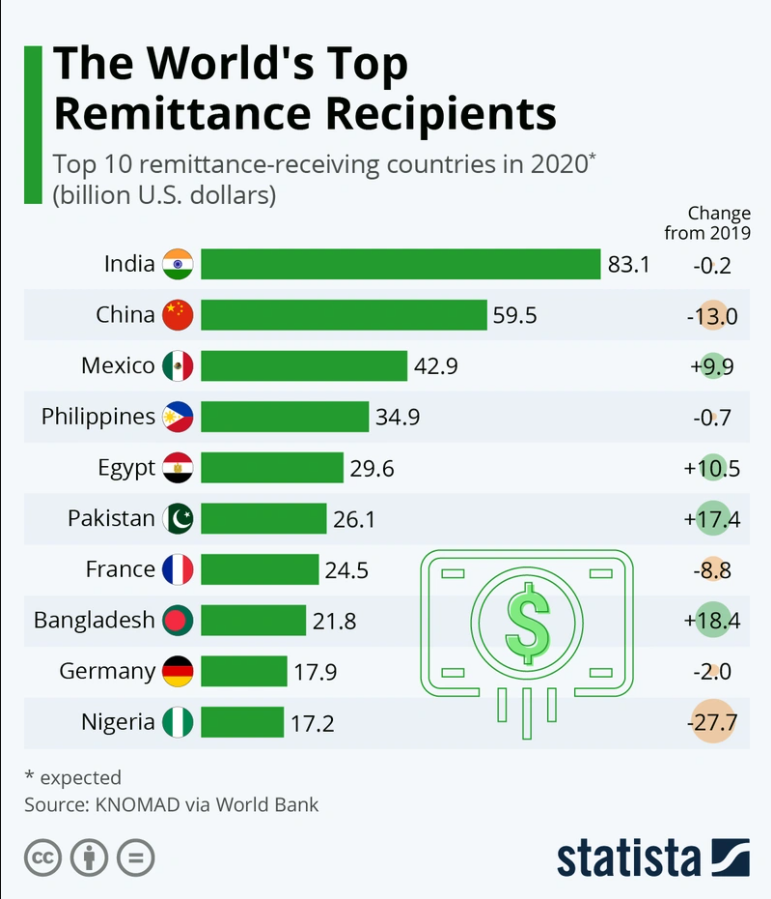

Reducing fees will significantly improve living standards for households dependent on remittance inflows.

Finally, entrenched financial intermediaries will certainly resist disruptive Web3 companies through lobbying and negative publicity. After all, global remittances exceeded $700 billion in 2020, actually declining slightly from the previous year, with approximately $540 billion flowing into low- and middle-income countries.

This means low- and middle-income individuals pay significant fees to large banks and financial institutions just to transfer money to themselves or their families. Moreover, transferring these funds usually takes several business days rather than minutes, regardless of date or time. Third parties benefiting from international remittance arrangements will not readily accept becoming obsolete—and losing their ability to charge high fees as before.

Looking Forward to the Rise of Tokenization

Tokenization of physical and digital assets is rapidly becoming a reality and will continue to grow more prevalent in the coming years. Due to the fragmented challenges currently facing Web3 as a whole, tokenization may initially be adopted gradually, focusing on specific aspects of blockchain-based securitization.

That said, market participants and investors have responded positively, showing interest in NFTs and other tokenized assets. Furthermore, macro forces such as the growing emphasis on environmental, social, and governance (ESG) mandates and the need for more transparent and efficient financial disclosures should accelerate the adoption of Web3 and tokenized securities.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News