A Comprehensive Overview of the Current Crypto Market: Utopian Narratives and Sector Rotation

TechFlow Selected TechFlow Selected

A Comprehensive Overview of the Current Crypto Market: Utopian Narratives and Sector Rotation

The most recent two bull market cycles (2020 and 2021) were characterized by the dominance of "narratives."

Author: Kevin Zhou

Translation: TechFlow Intern

Overview

The most recent two bull cycles (2020 and 2021) were defined by the dominance of "narrative." For a token project, marketing prowess and meme virality mattered more than the actual merits of the project itself.

First, trading firms transformed into venture capital firms.

Second, anonymous influencers gained the power that once belonged exclusively to VCs in 2017.

We can observe the evolution of narratives—shifting from DeFi to NFTs, then briefly to DAOs, L2s, followed by Play-to-Earn, Metaverse, Web3, and finally circling back to NFTs. During this time, the L1 wars have already passed through five shared narratives.

The crypto space is searching for new stories to justify deploying fresh capital and satisfy investors' appetite for outsized returns. Such returns were once feasible on early fundamental grounds, but now the only viable path left is luring in less sophisticated capital and using their money as "exit liquidity" to pay out earlier investors. Years ago, I would have considered this shameful—misallocated capital doesn't create value; it merely preys on TikTok users dreaming of getting rich, tricking them into handing over their money. Every industry has its self-serving speculators. Today, my view is entirely different.

I believe each bull cycle embodies the natural life cycle of the animal kingdom, where within humanity there exists a food chain—greedy individuals get eaten by slightly smarter counterparts. It’s ugly, but inevitable. I am now a believer in crypto accelerationism.

For years, we've been unable to achieve progress in this industry through logic or any form of dialectical reasoning. We advance only by witnessing the outcomes of experiments—most of which are destined to fail—and learning from them (though some do succeed, at least for now).

Debates about Small Block vs Big Block, PoW vs PoS, this PoS vs that PoS, this L1 vs that L1, L1 vs L2, (3,3) vs (-3,-3), Punks vs Apes, DOGE vs SHIB, CLOBs vs AMMs—cannot be resolved without observing how these things actually function in reality.

Theoretical research into mechanism design, flowcharts with boxes and arrows, historical analogies, hardcore textual descriptions—none of these are sufficient to convince one tribe to abandon their sacred cows and join another. As an industry, we must experience the quality and effects of things firsthand before they become engraved in our zeitgeist and collective memory. Only then can we move forward.

The introduction of jargon is an interesting development in crypto culture. In traditionally protected and supply-constrained fields like medicine and law, technical terminology serves two purposes. First, it saves time when both parties share a mutually understood vocabulary. Second, it prevents outsiders from easily extracting value that “rightfully” belongs to insiders. Crypto is no exception. As the industry becomes wealthier, we will increasingly use group-specific jargon to prevent outsiders from eating our lunch. This may lead to more M&A activity, as crypto is a high-margin yet difficult-to-penetrate industry, and non-crypto companies attempting to enter lack the necessary expertise. I make no normative judgment here—it's simply a natural phenomenon.

Capital allocation always comes after novel and useful innovations emerge. During a bull cycle, an increasing amount of capital chases progressively lower-quality projects. Founders and scammers alike eagerly launch half-baked ideas and generate supply to meet the incoming demand from new fiat flowing into the space. Some see through the “emperor’s new clothes,” but fear strong backlash from Shillers and Bag Holders, so they engage in maximum self-censorship regarding counter-narratives.

It is precisely under such conditions that narrative reaches maximal upward reflexivity. At peak mania, people buy only what they believe they can flip to the next greater fool; valuations grow absurd, and common sense is drowned out by communal hysteria praying for price increases. Had macro conditions not shifted, we might have reached even more ridiculous heights. The mania hasn’t yet reached its true peak. As tides turn, “narratives” across crypto and other domains weaken. The true nature of many projects surfaces—some mildly fraudulent, others outright scams. When madness becomes the rule, nuanced trade-offs and cautious considerations are branded heretical. Indeed, only after the “narrative” fades can such thoughts be expressed without ideological persecution.

Currently, pricing for major equities appears fair, though agents remain somewhat overleveraged. Initially, skepticism surrounded Fed rate hike rhetoric, but now most believe it, and it's reflected in market prices. Minor dips due to new hawkish Fed developments were quickly bought up. Expectations point to 4–5 hikes this year, no more, no less—at least for now. Speculative allies and major cryptos like BTC and ETH have seen some pullbacks, but nothing close to 2018 levels. Most massive third- or fourth-party funds raised by crypto VCs will likely go toward new projects rather than old ones. If macro conditions improve, new projects could still deliver 10x or 100x returns with such backing, but older projects likely won’t see similar growth again.

Greed and Utopia

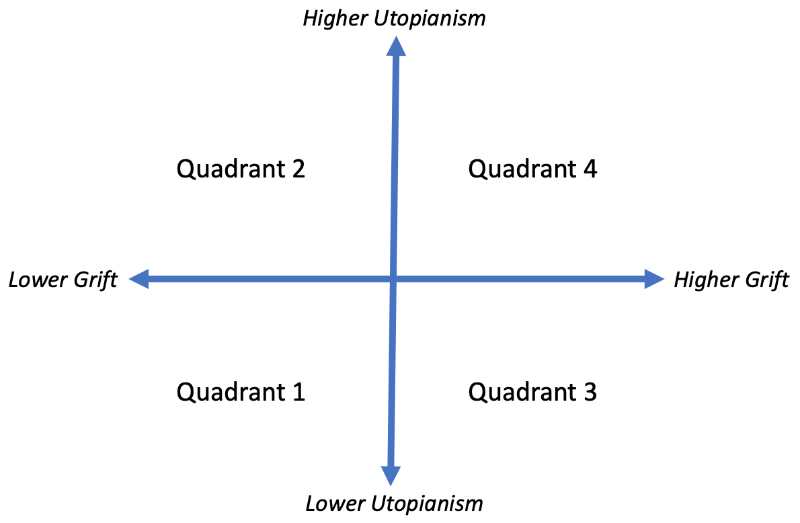

Based on my recent thinking, we can categorize various crypto situations along two dimensions: “fraud” and “utopianism” (here, “fraud” isn’t pejorative—it’s akin to Alpha). For example, on the fraud dimension, we all agree OHM is more fraudulent than TIME, and TIME more than other OHM forks. I’m not setting absolute thresholds for fraudulence—I’m just saying relative rankings are possible. A general rule here: forks are scarier than originals.

On the utopianism dimension, BTC is less utopian than ETH, and ETH less than SOL/AVAX and other new L1s. Here, the general rule is: newer projects attempt to “solve” inherent problems in older ones, thus appearing more utopian. Understanding these dimensions allows us to analyze the investability, returns, and timing of each quadrant. These quadrants are:

1) Low fraud, low utopia; 2) Low fraud, high utopia; 3) High fraud, low utopia; 4) High fraud, high utopia. The beloved 2x2 Thinkboi matrix.

Quadrant I (low fraud, low utopia) represents projects genuinely tackling solvable problems—ones that don’t require fundamental technological breakthroughs. Examples include (past) crypto exchanges, new crypto infrastructure games, and early successful cryptos like BTC. These are often solid long-term investments, though they may appear unattractive in the short term, especially during bull mania.

Quadrant II (low fraud, high utopia) represents projects striving to build grand designs and usher us into a dazzling new world. These often require at least one (if not multiple) technological breakthroughs to work. You’ll frequently hear followers of these projects criticize Quadrant I projects for failing to meet their standards—using this as justification for why their own project needed to exist in the first place. Utopias are only worth pursuing if the current world has serious flaws. Due to founder sincerity and project feasibility, Quadrant II projects are often excellent early-stage investments. This enables founders to craft a myth that sustains fundraising for one or two rounds. Later, they’re only good investments if breakthroughs occur and the utopia is “realized.”

It’s unclear whether these utopian pursuits will succeed, but VCs only need a few wins—the profits from successful projects cover losses from failed ones. A key tactic is making Quadrant II projects look as much like Quadrant I projects as possible, reducing perceived risk and making investors feel safer. In this process, the actual breakthrough requirements are often artificially obscured, and the proposed designs are repeatedly asserted as fully viable, with perfect game-theoretic and incentive-aligned mechanisms. Quadrant II resembles Quadrant I—but higher risk, higher reward. Risk differs, but potential upside does not.

Quadrant III (high fraud, low utopia) represents poorly executed money-grab schemes—an example being Bitconnect. Everyone involved knows it’s a scam. That’s why Bitconnect targeted audiences outside the crypto community—frankly, less experienced individuals. To inexperienced investors, these projects appear more utopian than they are—precisely their goal: blending into Quadrant II. Ultimately, utopianism often becomes a smokescreen for fraud, attracting the worst actors in our industry—self-serving speculators. The dumb and greedy scam the dumber and greedier, and these blowups eventually give regulators justification for harsher oversight of the entire crypto space. Can you think of any current crypto projects deliberately targeting non-crypto audiences? They’re all intentional scams!

Quadrant IV (high fraud, high utopia) represents either Rube Goldberg machines or perpetual motion devices (the former contrived, the latter baseless). Like Quadrant III, they’re scams, but more sophisticated. Even insiders struggle to dissect their complex structures—doubters conclude, “it might not work, but it might, because I can’t pinpoint exactly why.” Like the mythical Gordian Knot, no one sees where it might loosen or how it could be untied.

Quadrant IV projects try hard to mimic Quadrant II. If they achieve short-term success, they may transition from fake to real and enter Quadrant II. What separates WeWork from Theranos? The former was a Quadrant IV scam turned genuine Quadrant II project; the latter remained a fraud throughout. Overall, Quadrant IV projects offer excellent short-term returns for many participants. Sad but true—partly because token projects achieve liquidity faster than traditional private companies; effectively conducting IPOs early. After “going public,” all incentives shift to short-term, quarterly-oriented behavior. Founders can “retire” early, without waiting for proof of product efficacy or unsubsidized product-market fit—especially evident in projects where access is purchased via tokens. Most seemingly successful crypto projects fall into Quadrant IV, as the temptation of quick cash doubling is irresistible.

The fraud in Quadrant IV benefits founders, employees, investors, traders, exchanges, market makers, OTC desks, SAFT sellers, lawyers, and third-party service providers. The only losers are the final holders—the ones who “love” these projects, sold a utopian dream by those smarter but worse than them, clinging desperately to it.

I find the two-dimensional framework of fraud and utopianism highly explanatory for the cyclical phenomena we observe in crypto. In summary: Quadrant I is good long-term, unattractive short-term. Quadrant II pretends to be Quadrant I—if they solve a possibly unsolvable problem, they may enter Quadrant I. Quadrant II offers short-term profitability, high-risk/high-return long-term. Quadrant III pretends to be Quadrant II but only scams newbies—avoid completely. Quadrant IV also pretends to be Quadrant II—if they avoid bad outcomes after initial success, they may transition into Quadrant II. If you care only about money, Quadrant IV projects are currently the best short-term investments, and VCs benefit most from arbitrage in Quadrant IV access. Quadrants II and IV are where accelerationism is most needed.

NFTs

We’ve largely stayed away from trading NFTs and NFT-related tokens. We don’t believe we have a sufficient competitive edge in this game. Aesthetically, we lack refined taste. In terms of mimicry, we don’t have enough Twitter followers. There are plenty of other markets to trade—plenty of fish in the sea.

First, consider art and pfp NFTs. As symbols of status/signaling, Veblen/luxury goods, heirlooms/prestige items, some will retain long-term value. Just as there are two or a dozen top fashion houses in physical space, we may see a similar number of NFT collections with enduring brand value. That said, just as we won’t have 1,000 top fashion brands in reality, most NFT collections in crypto cannot hold high value. At best, this leads to a power-law distribution of value—winner-takes-all. Also, status signaling requires display to others—just as wearing designer clothes among peers signals status in real life, for NFTs the display venues are limited to social media like Twitter and Discord. It’s hard to say which realm offers broader visibility, though a reasonable argument exists: virtual worlds are far vaster than physical ones—Twitter and Instagram are actively integrating NFT features, and people spend increasing time online, making virtual expansiveness particularly evident. Moreover, pfp NFTs outperforming general art NFTs isn’t surprising—they serve better as avatars for online identity. Still, investing in NFTs requires caution; this sector has seen the worst corruption recently. Gamer and streamer communities largely despise NFTs—I personally blame Ice Poseidon.

Second, I do believe vampire attacks like LOOKS could capture market share. They target precisely the right audience—the ideal user for their platform. That said, LOOKS’ price and market cap have recently been slashed, most volume is wash trading, and founders keep cashing out. Given the team is anonymous and the token reached extreme highs quickly, confirmation of a full-blown scam wouldn’t surprise anyone. Nevertheless, given high fees and room for competition, the idea of multiple competing platforms for NFT trading makes sense. Also, unlike order books, there’s no strong liquidity network effect, making it easier for challengers to compete with incumbents. NFT exchange liquidity network effects are weaker than delta-one exchanges, which in turn are weaker than options exchanges.

Finally, the design space for non-artistic, non-pfp NFTs remains largely unexplored—I believe exploration here is worthwhile. Like all innovation, much may be nonsense, but I’m optimistic people will discover some excellent, useful applications.

L1s

Since technical merits are irrelevant until they materialize (at some uncertain future time), we shouldn’t waste time debating them.

I simply say it makes perfect sense for different people to support different L1s. Chicago HFT shops love SOL; Koreans love LUNA; grad students love AVAX (the only professor coin, and it performed well); Andre’s followers love FTM; Silicon Valley VCs love everything—because one correct bet can make the whole fund. Sometimes they favor smaller L1s like NEAR, since if you don’t already have hundreds of millions in market cap, NEAR could grow tens of billions more. Ethereum maximalists now stand alongside old BTC maximalists in defending against attacks from “new things.” Generally, their defense fails—people love novelty. With something new, you can dream your grandest dreams; with something established and moving steadily, you only see cold, hard reality.

Utopianism stems from the brutality of the real world and human ugliness. People crave perfect worlds and exploit others’ cravings for perfection. Ultimately, true believers become disillusioned traitors, needing a Girardian scapegoat for their anger. Who better than prophets who promised futures never meant to be delivered? I’m not saying these L1s won’t succeed—only that founders know the sword of Damocles hangs above them. Their best move is victory; second-best is making larger concessions on decentralization—since decentralization matters little until achieved, and who knows if or when it ever will be? Maybe we fear demons, maybe we don’t.

As we rebuild financial and monetary systems, we start sympathizing with past Fed chairs. No Fed chair wants economic collapse under their watch—so why kick the can down the road? Given all participant incentives are aligned, I hope the best L1 wins. That’s all I’ll say. Not everyone enters for technology. In fact, few do.

At this point, I’ve waited over seven years—I don’t even dare ask if we’ll get Ethereum’s PoS machine this year. Which will come first: ETH 2.0 or Hal Finney’s frozen body reviving? Ha, now who knows? I’m joking—don’t come at me.

Regarding cross-chain bridges, the main challenge is ensuring synthetic assets on one chain aren’t artificially inflated without proper backing, and securing transport. We recently saw the Wormhole vulnerability between SOL and ETH, caused by a SOL-side issue. I’m not overly concerned—it was a fixable bug. Though Jump rescued Wormhole, they likely paid themselves. If a bridge fails, their SOL wallet loses substantial value—I believe they’d have skin in the game too. But that’s not the main worry. My concern is whether bridges have fundamental issues even with perfect code—that remains to be seen. Also, even today’s bridges are quite centralized, but as long as decentralization without sacrificing security is eventually possible, it should improve. People will wait and see—I’ll remain skeptical.

DeFi

DeFi 2.0 is like DeFi 1.0, but 2 > 1—bigger numbers are better. DeFi 2.0 features the idea of protocols controlling or owning assets—sometimes called PCV (Protocol Controlled Value) or POL (Protocol Owned Liquidity). Same concept: run a DeFi protocol while simultaneously operating a hedge fund. Whether this is good or bad is left to the reader. Now some protocols hold other protocols’ tokens and participate in governance votes—we’ve entered an era of systemic risk. Easier to imagine: this relatively small TIME-MIM-LUNA slice feeding into a larger composite product network, or perhaps into a CDO-squared level of structured products like pre-2008 crisis? Scary stuff. Composability is great—it enables previously impossible things. But systemic risk accumulates over time, entangled protocols grow harder to disentangle—so we must stay cautious, or it ends as a bigger mess.

Play-to-Earn

You work to earn money, then spend that money on play. Always done that way, right? Work is essentially what you’d rather not do—you do it for compensation. Play is what you want to do because you enjoy it—even willing to pay for it. So what the hell is P2E? If you’re a rural Chinese farmer earning a living by farming WoW gold, that’s work. If you play WoW and enjoy it, you might buy WoW gold on RMT sites—gold sourced from rural China—that’s play.

In P2E, people overload terminology again, making it sound cool and trendy, suggesting P2E lets you “have your cake and eat it too.” In most regular games, some work to earn, others pay to play—little overlap. In most “P2E” games, while earners still work, those paying to play are mostly replaced by a new group: those paying to acquire workers’ output and resell it to other payers. In short, most regular games have workers and players; most P2E games have workers and speculators. Clearly, almost no one truly wants to play P2E games.

If the P2E industry ever releases genuinely fun games, it becomes a normal game with workers and players—differing subtly: it provides bearer-chain assets for virtual in-game items, enabling active secondary markets outside developers’ platforms, though devs can still tax them easily. Industry consensus holds secondary markets hurt revenue—hard to take cuts on every transaction, and they cannibalize primary markets. Now with crypto, while primary market erosion remains unsolved, taxation is easy. I see this as positive—many top-tier games historically had active secondary markets, and now there’s stronger incentive for devs to return to the pre-anti-secondary-market golden age. Players get what they want, devs get half. Thus, crypto and gaming can create powerful synergies—but current P2E games don’t.

Metaverse

If “Metaverse” means virtual reality (VR), we already have it—and it’s a growing industry. If Metaverse means more than VR, we must define it precisely, avoiding inflation of ordinary words through abstraction—think: when people say AI, they mean ML; when they say ML, they mean statistics; when they say statistics, they mean linear regression. Money is inflated enough—don’t let words inflate too. If Metaverse means virtual communities, we already have Telegram chats, Discord servers, even that company formerly known as Facebook.

If Metaverse describes a trend—people spending more time in virtual worlds, less in physical spaces—then it’s already happening. Japan’s hikikomori are our future. Central banks print too much money, half of humanity ends up sexless, basement-dwelling shut-ins, while the rest become zombie salarymen in giant corporations, inevitably dying from karoshi. Believe me—it’s true, but the evidence won’t fit in this article’s margins.

Practically speaking, when discussing Metaverse investment—whatever it means—it usually takes two forms: investing in a virtual world or zone, or in specific virtual land/assets within a zone. For the former, crypto enables two innovations previously impossible: first, you can let users gain ownership of “zones” via Web3-style yield farming, provided you have anti-Sybil mechanisms; second, you can organize users to conduct commerce without relying on centralized payment rails. In other words, you log into Decentraland, walk your avatar into a virtual art gallery, find a punk you like, click it to link directly to its auction on OpenSea. Click again, your Metamask opens, and you buy it. Once bought, you can leave it in the gallery, take it home to display in your virtual house, or show it in both. That’s pretty cool. But take VRChat—its zones are centralized, yet it could integrate this feature directly. Does Decentraland have unique advantages over VRChat? Hard to say clearly now, but maybe the next topic offers insight.

What happens when we turn land ownership into bearer instruments? When virtual land ownership becomes bearer instruments? This is a core difference between Decentraland and Second Life—creating scarcity and immutable, tamper-proof land titles. One issue remains: how much more valuable is land near transit hubs versus remote areas? Virtual land value benefits from foot traffic, like physical land—but in VR you can teleport and fly. If a project restricts teleporting/flying, competitors won’t. Since gravity needn’t govern virtual worlds, I imagine land stacked vertically. Thus, I don’t expect virtual land value gaps to match city-rural disparities in physical space, but some plots may still attract more attention and thus hold higher value. Finally, how irreversible is virtual land ownership? If someone puts something extremely vulgar or illegal (e.g., gore porn) on their Decentraland plot, what then? Can Decentraland take it down? True bearer ownership means Decentraland has no authority in such cases.

Web3

Unlike Gabe Newell’s Valve, we actually managed to count to 3. To avoid conceptual bloat, we adopt Chris Dixon’s definition: Web1 is read; Web2 is read/write; Web3 is read/write/own.

Thus, FCoin basically invented reverse fee mining, later popularized in DeFi as yield farming. So is Web3 just yield farming? Kidding—the paradigm shift isn’t mature enough. Web3 enables widespread yield farming on equity-like instruments, which securities regulators will struggle to enforce against. Could be good or bad—depends if you’re a regulator. Imagine Uber (or Lyft, if you’re Chris Dixon) issuing tiny amounts of stock to riders and drivers for every ride, with zero paperwork, middlemen, or regulatory overhead. Might actually be beneficial—a great way to bootstrap two-sided markets, solve chicken-and-egg problems, acquire users, and turn them into evangelists. Well, let’s see. When ambitious entrepreneurs start name-dropping Web3 in pitches—like past trends with “AI” and “sharing economy”—be extra careful.

Conclusion

In conclusion, everything in crypto is fine. Long-term, as usual, I remain bullish on crypto. Short-term, the space has work to do, cleanup required. I know some will call my post silly—I have no comment on that.

So don’t try copying your college friend who 10x’d on NFTs. Except for those impossible successes, we’ll eventually succeed. Life goes on, crypto goes on—keep building, keep hodling, try doing some good for the world, but make sure your good deeds don’t drag us all to hell. And go outside once in a while…

We really need to clean up our own space, or at some point it’ll explode systemically, and everyone will cry for regulation—history repeating as in mature markets. I can’t believe Gerko blocked me on Twitter for telling the truth. You know how people say “no offense,” and the next thing is always offensive? Sorry, not sorry. Whatever happened to artforz, I can’t believe they came up with such a clever scam. I mean, usually there’s a problem with rug pulls—once scammers dump, prices drop, and community members get furious. But what if they can dump stealthily without price drops—or even cause price rises while monetizing? Turns out, they actually found such geniuses! If you ask me about next-stage DeFi 3.0 monetization, these contraptions are insanely complex—so complex even Daniel Larimer might feel outclassed.

Readers who made it this far must be deeply curious—kudos to you! Francis Bacon said Solomon said there’s nothing new under the sun, and Plato imagined all knowledge as recollection. So Solomon said all novelties will be forgotten. Barry can profit from closed-end funds as compromise, but if people just buy more crypto, all sales pressure might be bad.

Nietzsche said sitting thinkers are nihilists—good thing I’m a pacing thinker. Mev is like the Olympics of intellectual sports—I don’t understand sports. I mean, there are only so many ways to put a ball in a hole, while StarCraft, WC3, DOTA are more strategic, more interesting competitions. Readers who got this far might be obsessive-compulsive—truly meticulous.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News