Waiting for the Right Price: Pricing the Bubble, Valuing the Narrative

TechFlow Selected TechFlow Selected

Waiting for the Right Price: Pricing the Bubble, Valuing the Narrative

How Is the Crypto Valuation Framework Being Reshaped?

By: Zuo Ye

In July 2020, Andre Cronje (AC), the “King of DeFi,” personally launched the “fair launch” model—no pre-mining, no presale, no team or VC allocation—a move widely celebrated at the time.

By 2026, Aave’s core team and DAO remain locked in relentless internal conflict, while Across has even proposed “rewinding” back to a traditional corporate structure—and its token is to be strategically abandoned in favor of ordinary shares.

Zooming out, compared to DeFi projects’ existential dilemmas, the most profitable exchanges are experiencing a wave of high-value acquisitions.

Coinbase valued Bybit’s 80 million users at $10 billion; Nasdaq’s parent company valued OKX’s 120 million users at $25 billion; Forbes even pegged Binance’s 300 million users at $100 billion.

All this signals that the crypto market has reached an inflection point—the moment for strategic exits has arrived. Early-generation founders are opting to “cash out,” yet consensus on what comes next remains elusive.

We must acknowledge reality: most crypto projects cannot directly equate network effects with user count and trading volume the way exchanges do. Regarding token utility and governance rights, projects must handle token valuation and governance with caution—and craft a narrative logic appropriate to their own context.

The questions of crypto pricing, valuation, and exit strategies have likewise reached a stage demanding systematic review—and preparation for the next leg of the journey.

Crypto Is a Market of “Zero to One” Only

Peter Thiel disdains scale, preferring post-disruption monopoly effects.

When the “high FDV, low circulating supply” VC-coin model collapsed, Binance—as the quintessential exchange—faced industry-wide backlash. Though Binance Alpha temporarily delayed Binance’s decline, it can no longer carry the entire industry’s future.

If we insist on interpreting the VC-coin collapse through the lens of “narrative,” delivery quality proves far more consequential than mass adoption—revealing the bizarre reality where “launch token first, deliver later” has devolved into “launch token only, never deliver.”

It wasn’t always like this. Ethereum’s ICO truly delivered foundational infrastructure after Satoshi—while tokens like $EOS represented necessary, painful exploration and reform. The dot-com bubble did not halt the dawn of the information age.

Since Ethereum, history—including AC’s ill-fated fair launches and Uniswap’s retroactive airdrops rewarding users—has unfolded without orientation toward listing on Binance. We genuinely believed in tokens’ magic and governance’s meaning. Whether you believe it or not, at least a16z truly does.

More bluntly, exchanges, VCs, market makers—and recently, KOL agencies scrambling to pivot—have all discovered, consciously or not, that distorting token sales processes yields far greater and faster wealth effects than waiting for user base > holder base.

Drawing from Web2’s investment–IPO–exit logic, Web3 boils down to just three steps: valuation, TGE, and pricing.

Image caption: Crypto valuation framework. Source: @zuoyeweb3

This results in a bloated middle layer: everyone spontaneously orbits around trading—the industry’s most lucrative, arguably only, profitable segment.

Normally, primary-market valuations should reflect long-term businesses—measured in decades. Even the fastest-maturing asset, ETH, took six years (2015–2021). Secondary-market valuations should follow enduring models; exchanges and market makers shouldn’t cannibalize retail investors’ long-hold returns.

October 11 stripped away all pretense: secondary-market pricing logic shattered value investing entirely. A distorted market logic left decentralized DAOs powerless to sustain even the illusion of viability.

Crypto has mounted numerous countermeasures: in the primary market, evolving from SAFTs to SAFE + Token Warrant dual structures; expanding U.S.-centric operations into global foundations. Yet against the transaction costs embedded in the middle layer, all such efforts prove futile.

Consider Hyperliquid’s Dutch auction spot-listing mechanism—an elegant design ultimately superseded by HIP-3, which sells liquidity itself. Today, markets trade only established assets like BTC/ETH—or traditional commodities and precious metals. No one still believes in crypto’s capacity for genuine asset creation.

Where the skin goes, the hair follows. Tokenomics collapses; token holders’ status becomes precarious.

On one hand, VCs and exchanges claim token allocations, yet long-holding and governance participation yield no urgently needed financial ROI. On the other, project teams and DAO members hold misaligned interests—Uniswap’s fee switch has long ceased to matter.

Image caption: DAO spirit erosion. Source: @zuoyeweb3

Much like stablecoin legislation, more and more DeFi protocols are reverting to corporate structures; more and more stocks are being tokenized—both trends unfolding simultaneously on America’s surreal soil.

After MakerDAO rebranded as Sky, founder-team interests were duly respected. Jupiter acknowledged buybacks couldn’t sustain token price or business expansion. Circle acquired Axelar for talent—not tokens. Gnosis chose to roll back. Everyone reported calm.

We can summarize: crypto markets only reach the “zero-to-one” moment before entering capital-markets mechanics. The “one-to-N” phase remains a fantastical mirage. Amid FOMO-driven cashouts, equity, tokens, people (founders, VCs, token holders), and product fully fracture.

Tokenomics and DAOs hold historical value: tokens served as fragile glue binding complex, competing interests—functioning as a minimal common denominator recognized across stakeholders.

Yet now, even stablecoins and public blockchains stand at the threshold of their own “one-to-N” transition—where even marginal user growth exerts centrifugal force on existing structures.

Under normal conditions, development follows a cyclical pattern: “bubble → growth → SaaS → bubble.” For instance, from AlphaGo (2016) to ChatGPT (2022), we’re at the inception of AI’s second bubble.

Crypto markets, however, behave abnormally: “bubble → bubble” is the absolute norm. Combined with humanity’s largest-ever monetary expansion, the market swells perpetually within bubbles—until stablecoins and agents finally converge in households.

Then the entire industry faces a growth crisis. Alpha hunters—masters of irrational exuberance—cannot explain how it all began.

Some embrace institutionalization, using sheer capital size to soothe anxiety. Ignoring the questionable discount rate implied by such thinking, merely clarifying unstructured financial standards would take years.

Let us learn from the bloated middle-layer elite—identify the lifeblood of today’s structure, and rebuild from there.

People Are the Subject of Narrative

Market structures evolve—but the logic whereby secondary markets dictate primary valuations remains unchanged. If “I reckon” suffices for comparable multiples in a purely bubbly market, then during periods resembling SaaS-style stable growth, benchmarking against established human narratives—even valuing public blockchains—becomes feasible.

Multiple = Pricing × Narrative

Yet before escaping our own echo chamber, crypto must first develop a self-consistent valuation framework—expanding external returns and converting them into demand for Web3 assets, rather than absorbing Web2 bubble sell-offs.

Image caption: Post-narrative divergence. Source: @zuoyeweb3

Starting from Bitcoin’s narrative—peer-to-peer electronic cash—we’ve proven crypto’s capacity for “self-bootstrapping,” requiring only personal PC-level computational resources externally.

In some sense, this is more scientific than traditional equity + IPO models: IPOs require selling product-and-sales stories to mass financial markets and institutions—far beyond the user base—over extended capital cycles.

Bitcoin’s users, capital, and financial markets are perfectly identical. It requires no fiat-convertible financial market—making this deeper than technical decentralization.

Alas, all this unraveled amid equity-token infighting—proving that simple, one-size-fits-all solutions fail in complex environments.

- Infrastructure like Ethereum needs no equity but requires token-based incentives to sustain long-term developer engagement—for example, confronting AI and quantum threats.

- Protocols like Uniswap need no token rights; token holders bear no product responsibility yet compete with teams, VCs, and LPs for revenue share.

Intermediaries multiply; stakeholders obscure information. Paradoxically, achieving decentralization demands *de*-intermediation—culminating in PumpFun’s spiritual return: primary valuation fully “secondary-ized” and algorithmic, yet securing a firm market foothold.

I’ve long held that PumpFun’s significance lies in eliminating intermediaries at near-zero cost—though it spawns new problems (e.g., scientists gaming the system). Perhaps perfect answers simply don’t exist.

Still, crypto retains a sliver of asset-creation potential: post-Binance Alpha, pre-market trading arbitrages spot prices; stablecoin yield products absorb retail capital—forming a uniquely crypto-native “IPO” mechanism.

Pricing = Pre-market trading + Stablecoin yield products

This model bypasses many extractive middle layers—but still fails to resolve “narrative,” the core determinant of valuation multiples.

Fortunately, DCF (Discounted Cash Flow) has operated for decades, with applicability across industries well understood. Pure memes may ignore DCF—but any project facing market scrutiny must articulate its own narrative.

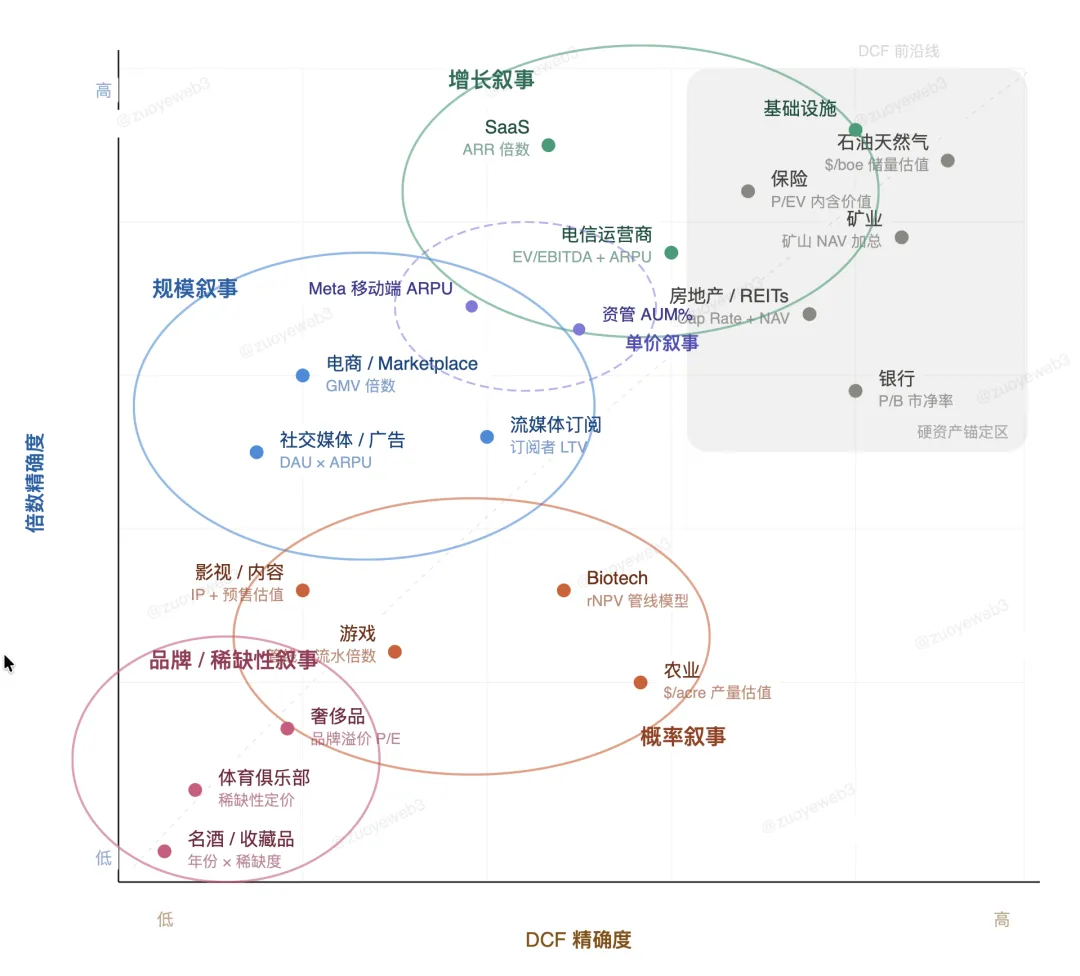

Image caption: Narrative taxonomy. Source: @zuoyeweb3

This isn’t complicated. Financial narratives broadly fall into five categories:

- “Growth” matters most: e.g., SaaS software’s ARR (Annual Recurring Revenue) is relatively fixed—so accelerating ARR growth is key.

- “Scale” matters most: e.g., internet feed-ad revenue depends entirely on traffic scale—0.01% conversion on billions of users is terrifyingly potent.

- “Unit price” matters most: a hybrid of growth and scale narratives—and mobile internet’s secret for the past decade. Netflix and Apple’s streaming subscriptions compete to seize scale and speed from traditional TV, theaters, and studios.

- “Probability” matters most: e.g., biotech pipeline models measure drug-development success rates to market approval. Not a scale-driven market; no profit via imitation—only luck prevails.

- “Brand” matters most: luxury goods aren’t about quality—they’re about recognition. In crypto? We’re stuck with penguin memes for now.

Narrative = DCF Model × Fit Rate

What fits best is best. Heeding Socrates, humanity’s narrative frameworks are largely settled—crypto belongs to human narrative, so it must find its own fitting model.

For example, among L2s, Arbitrum, Polygon, and Optimism chose Hyperliquid, Polymarket, and Base—under gas-based models, aligning broadly with the “unit price” narrative. Yet all face mass enterprise-client exodus, threatening relegation to SaaS—pursuing growth with only stagnant scale.

In the coming RWA, credit, and stablecoin-adoption waves, competition won’t center on user scale or fund-processing volume. Instead, choosing the right capital-market narrative and pricing/sales strategy becomes paramount.

Take Circle’s USDC + Canton emerging B2B model versus “old-school” ETH + YBS “for everyone” model: superficially similar, fundamentally divergent—yet both face intense pressure on token and stock prices. The outcome remains uncertain.

Or consider SpaceX’s record-setting $1.5 trillion IPO—handled by Goldman Sachs for institutional investors, Citigroup for retail shares, and UBS for overseas clients via subcontracting.

We must all prepare for change. Irrational exuberance won’t return. We’ll each need to choose a narrative and pricing strategy—whether selling tokens or products.

Conclusion

Cryptocurrency is fundamentally a consumer good—echoing money’s original evolution.

Middle-layer actors (VCs, CEXs, market makers, KOL agencies) sever information and capital flows—and disrupt seamless onchain-offchain experiences. Hyperliquid, Polymarket, and PumpFun’s pricing (listing) strategies all aim to minimize insider advantage and arbitrage arising from information asymmetry—albeit via distinct methods.

Polymarket doesn’t reject insiders—it even encourages them to disclose information, prioritizing market-trading balance. PumpFun outright denies the necessity of value investing, pricing every ticker purely via PvP. Hyperliquid chose the correct path: establishing price via pre-market trading.

Yet Binance still commands the deepest liquidity. Still, let us never forget: crypto began with hackers standing atop the wave.

I deeply anticipate how the AI wave—liberating ordinary people’s creative potential—will intersect with finance’s future (blockchain) to reshape human finance in profound ways.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News