Delphi Digital Report Quick Read: Trends to Watch in the 2022 Crypto World

TechFlow Selected TechFlow Selected

Delphi Digital Report Quick Read: Trends to Watch in the 2022 Crypto World

The scalability race between public blockchains will continue to intensify before L2 solutions become available; more creators and brands will enter the Web3 space.

Original Title: Delphi Digital Report Summary: Key Trends to Watch in Crypto for 2022

Source: Delphi Digital

Compiled by: angelilu, Foresight News

The Delphi Digital "Year Ahead 2022" report analyzes key topics, projects, and trends in the crypto space. Foresight News has compiled and translated the key takeaways below:

Key Takeaways:

1) Scalability Wars: Competition among Layer 1 blockchains will intensify until Layer 2 solutions become widely usable;

2) Cross-chain DeFi / Interoperability / Bridges: The Cosmos ecosystem is rising, and cross-chain bridges will benefit indirectly from the scalability race;

3) Stablecoin: Curve’s TVL is expected to reach $23 billion, making it the largest DeFi application;

4) Decentralized Derivatives: Decentralized derivatives platforms will launch across various scalability solutions;

5) Metaverse, GameFi, and Play-to-Earn (P2E): The play-to-earn model ushers in a new era of blockchain gaming, with dedicated gaming chains competing fiercely;

6) DAOs: Growth in DAO numbers will drive demand for governance and coordination tools;

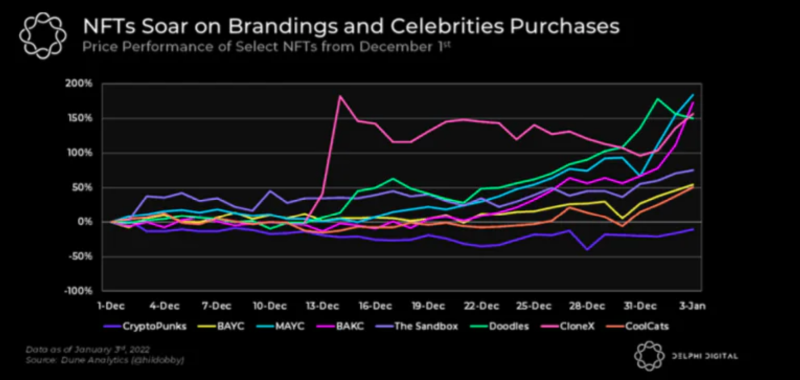

7) NFTs: NFTs had a strong start in 2022, with NFT tools and infrastructure moving into the spotlight;

8) Creators and Brands Entering Web3: More influencers are using NFTs and tokens to deepen fan engagement; music NFTs are poised for explosive growth in the coming years;

9) Crypto Market 'Homogenization' Will Improve: Mainstream cryptos like BTC will begin to exhibit characteristics of traditional asset classes, while broader crypto performance will depend more on whether assets or protocols achieve real adoption.

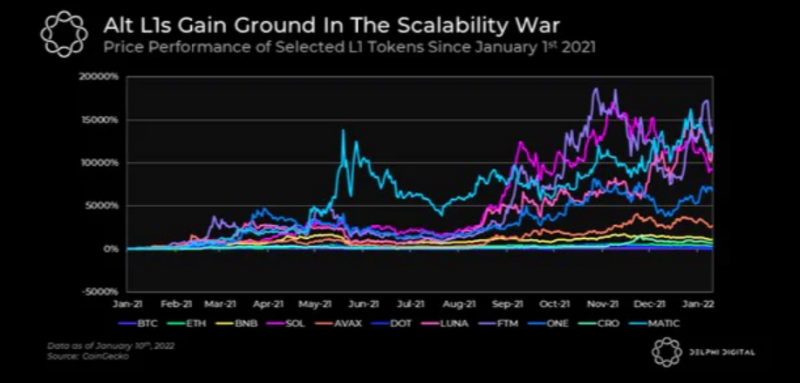

Scalability Wars

In 2021, major Layer 1 blockchains such as LUNA, SOL, and AVAX gained significant investor attention. Despite heavy promotion around Ethereum's Layer 2 solutions and the transition to ETH 2.0, Ethereum still suffers from high transaction fees. In 2022, the “scalability war” will continue to heat up, as alternative blockchains use different methods to increase throughput, reduce transaction costs, and attract top developers to capture market share. High fees and congestion on Ethereum will continue pushing developers toward other Layer 1s until Layer 2 solutions become more practical (e.g., StarkNet, dYdX for trading, Immutable X for NFT minting/trading).

Modular Blockchains and Data Availability: The rise of rollups has introduced the concept of modular blockchains. A mature blockchain consists of three core components: execution, settlement, consensus, and data availability. However, a single blockchain does not need to handle all these functions independently. Instead, modular blockchains specialize in one or more components and outsource the rest to specialized chains, enabling greater scalability. A key element of this modular stack is dedicated data availability chains like Celestia, which offer extremely high data capacity. Many rollups can leverage this capacity by offloading their data to Celestia, achieving shared security while focusing on scaling execution.

The Ethereum Merge is arguably the most important milestone in Ethereum’s history, marking its shift from PoW to PoS. However, without a hard deadline set, it has been repeatedly delayed. Public expectations point to completion by the end of Q2, but updates can be tracked here. From an investor perspective, after EIP-1559, ETH fees were split into base fees and tips. Post-merge, the tip portion will go to validators/stakers, combining with block inflation to make ETH a yield-bearing asset. Additionally, since the August 2021 rollout of EIP-1559, ETH has become deflationary.

Notably, as more traditional institutional investors dive deeper into crypto, capital flows are beginning to expand beyond just BTC and ETH—potentially benefiting more liquid L1 assets within the top 10–20 cryptocurrencies.

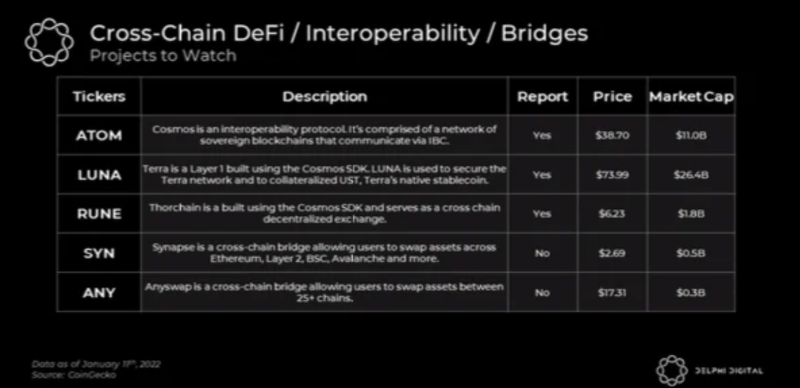

Cross-chain DeFi / Interoperability / Bridges

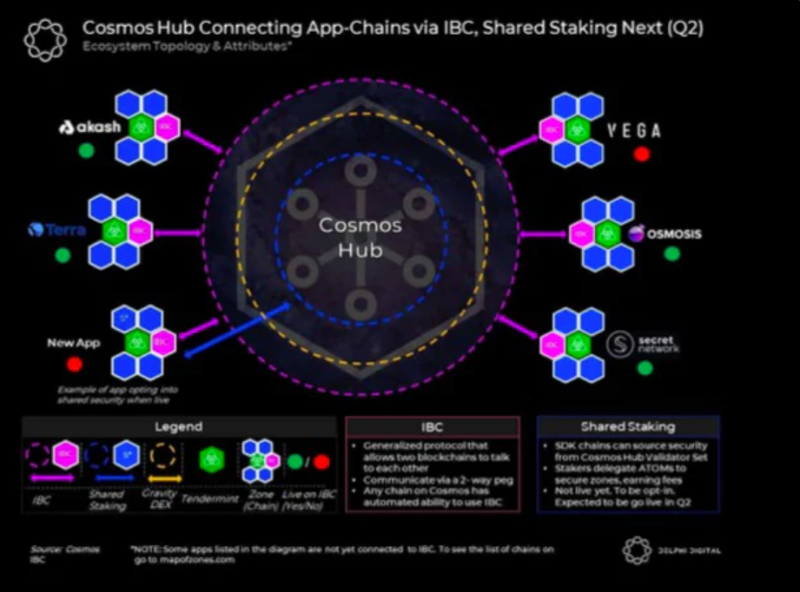

Interoperability and the Rise of the Cosmos Ecosystem

As highlighted in Delphi Digital’s in-depth research on Cosmos, in an interoperable world powered by IBC, previously isolated blockchains can now communicate. Looking ahead, Cosmos’ Q2 roadmap includes Interchain Staking, Interchain Accounts, liquid staking, and improved bridges connecting Cosmos networks—developments expected to fuel its next wave of growth. Notably, Interchain Staking could significantly accelerate the incubation of the Cosmos ecosystem by making it easier for developers to launch applications.

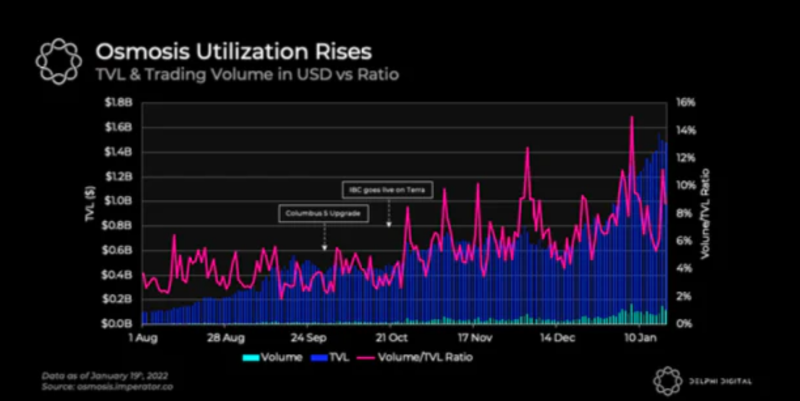

IBC-Supported DeFi: The Cosmos Hub will face competition from emerging hubs such as Evmos, Archway, and Juno, each offering distinct value propositions that can further stimulate DeFi activity across the Cosmos ecosystem. In fact, Osmosis has already begun competing with the Cosmos Hub—processing over twice as many IBC transfers in the past 30 days. Delphi Digital believes the Cosmos “season” will be large enough to accommodate multiple players. While Osmosis focuses on Cosmos-native DeFi, THORChain has chosen not to join IBC and instead supports Asgard, maintaining access to a vast market leveraging native BTC and other assets.

New Liquidity Bootstrapping Models: The emergence of IBC-native DEXs like Osmosis makes it easier to organically bootstrap liquidity for community-driven projects on IBC without relying on centralized exchanges (CEX). Users, stakers, and liquidity providers of tokens like ATOM and OSMO may receive additional airdrops this year.

IBC’s Dominance Outlook: While ATOM’s fundamentals are improving and tokenomics are expected to evolve positively, IBC may struggle to maintain dominance due to the influx of new protocols. That said, Cosmos has a healthy start—over the past 30 days, its 27 chains processed 3 million IBC transfers.

Bridges / Cross-chain Infrastructure

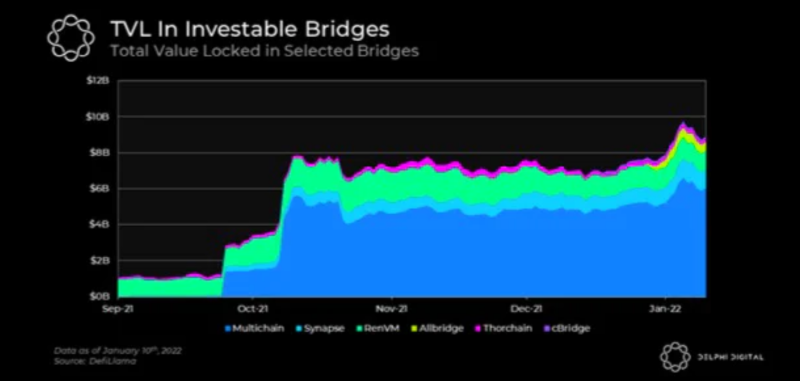

Another way to support alternative Layer 1s and scaling solutions is through bridges and cross-chain infrastructure. Ultimately, the goal of cross-chain infrastructure is to enable seamless and efficient (and ideally decentralized) transfer of assets across chains. With the continuous emergence of new L1s and L2s, it's too early to pick a single winner—or even a dominant set of assets. However, one thing is certain: competition in this space will only intensify, as the multi-chain narrative that exploded in 2021 shows no signs of fading.

The table above shows that the TVL of several cross-chain bridges surged since September, reaching approximately $9 billion. From September 1 to early January 2022, these bridges delivered an average return of 108%, compared to -1% for ETH—highlighting the strong momentum of alternative L1s in the second half of 2021.

Below are some cross-chain bridges highlighted by Delphi Digital analysts:

Hop Bridge (Hop): A pioneer in cross-rollup development, Hop currently has a relatively small TVL (~$100M), and has not yet launched a token. Nonetheless, Hop Bridge is expected to become a foundational component for Ethereum-centric rollups.

THORChain (RUNE): A key milestone for THORChain was the introduction of vault nodes, allowing the community to pool RUNE to contribute to network security. This enables pools to grow without hard caps.

Synapse (SYN): Synapse connects different L1s and L2s. Since launching in September, SYN has outperformed most other L1s, though it carries higher risk than SOL, LUNA, or AVAX.

Cosmos (ATOM): Amid the L1 and L2 scalability race, cross-chain liquidity bridges stand to benefit indirectly. Cosmos is well-positioned to shine in a multi-chain future, as more chains and protocols adopt its infrastructure and IBC standard.

Stablecoins & The Curve Wars

Stablecoins experienced explosive growth in 2021, surpassing $150 billion in total market cap. This surge confirms stablecoins as crypto’s “killer app,” demonstrating strong product-market fit. Assets like USDC and USDT have become ubiquitous across the crypto ecosystem—a trend expected to continue.

Decentralized Stablecoins

If regulators crack down on stablecoins, users and builders may turn to decentralized alternatives instead. Click here to read Delphi Digital’s analysis on LUNA and UST.

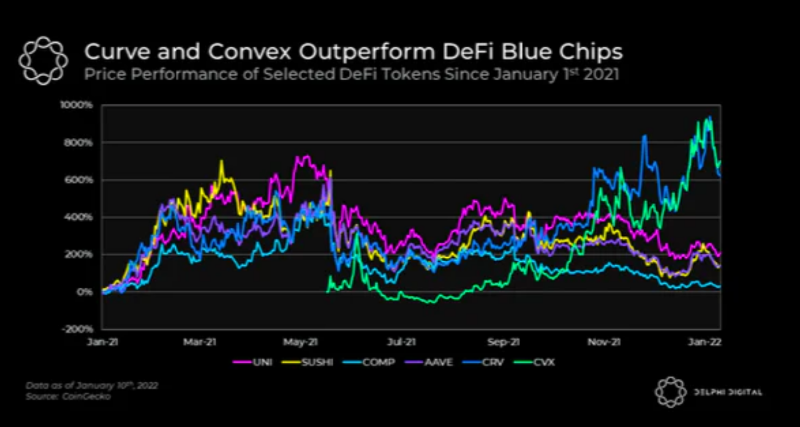

Delphi Digital also predicts that Curve (CRV), the minting king of decentralized stablecoins, along with its symbiotic relationship with Convex, will become the largest application by TVL—reaching $23 billion (compared to nearly $19 billion at time of publication)—outperforming other DeFi blue-chips in financial metrics.

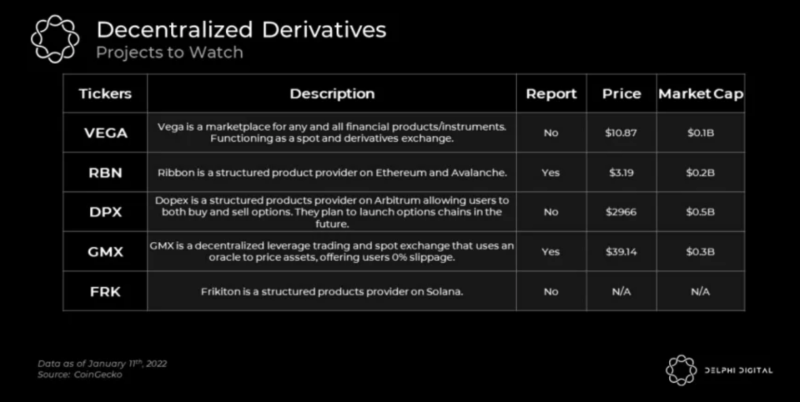

Decentralized Derivatives

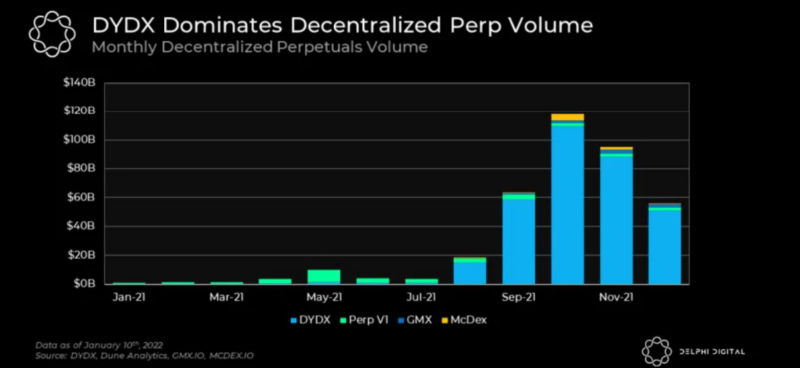

Decentralized derivatives heated up rapidly in 2021 and still have massive room for growth before surpassing their centralized counterparts. dYdX dominates the DeFi derivatives space, and Delphi Digital expects it to remain a major player. However, competition in decentralized derivatives is expected to intensify in 2022 as more perpetual contract platforms launch across various scalability solutions.

In its current state, the dYdX token lacks value accrual beyond governance rights—a situation that may change with the launch of dYdX V4. Below are other perpetual contract protocols and DEXs highlighted by Delphi Digital analysts:

Vega: A decentralized derivatives and spot trading market.

GMX: Uses oracle-based pricing and functions as both a spot and leveraged trading platform.

Additionally, emerging options and structured products are becoming increasingly viable across various L1s and L2s. Ribbon and Opyn launched decentralized options products back in April 2021. Integration between options protocols and perpetual platforms is another area of innovation, enabling delta hedging and improved capital efficiency. Two options projects highlighted by Delphi Digital:

Zeta Markets: An options trading platform built on Serum’s order book with a native Zeta AMM integrated. Combined with Solana’s high throughput, low latency, and low fees, this could be a compelling project for institutional participants to seriously engage in DeFi options trading.

Dopex: Employs a covered call strategy where call options are sold directly back to buyers on the platform—not to market makers who typically charge spreads. Dopex is also developing a Deribit-like options chain, with pricing based on IV multipliers represented by market makers.

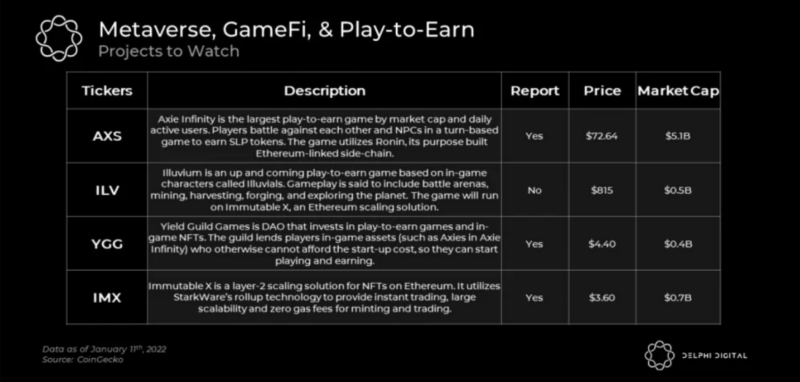

Metaverse, GameFi, and Play-to-Earn

Last year, Axie Infinity exploded and proved the viability of the play-to-earn model. Now, a wave of P2E games are attempting to replicate Axie’s success. As the ecosystem grows, filtering signal from noise will become increasingly critical—and challenging. Most projects will eventually fail, but this marks only the beginning of a new era in gaming. Projects like Illuvium, Crypto Unicorns, and Ember Sword promise AAA-quality graphics and gameplay. Gaming-specific chains are also competing fiercely, with notable contenders including Immutable X, Ronin Chain, Solana, and Polygon.

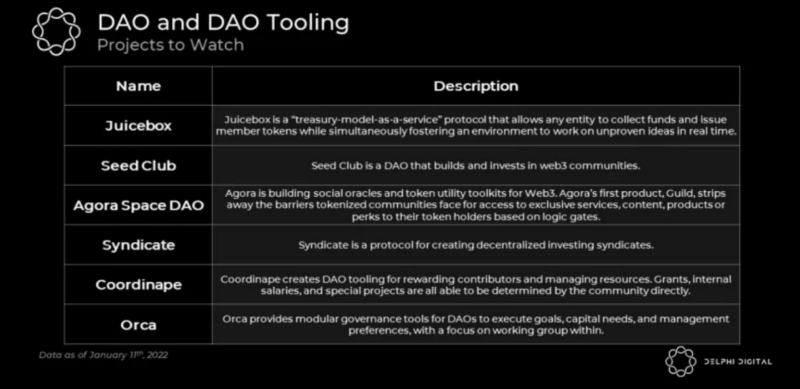

The Evolution of DAOs

2021 was the breakout year for DAOs, during which their definition evolved. Previously, DAOs were used by protocols like Uniswap to vote on grants and treasury allocations. Today, DAOs are seen as immediate entities for group coordination—with shared bank accounts and payment capabilities—combining crowdfunding, capital deployment, and voting tied to tangible outcomes. Experiments like Constitution DAO demonstrated that decentralized autonomous organizations can raise tens of millions of dollars within weeks and collectively purchase assets. Some DAOs now manage hundreds of millions—or even billions—of dollars in treasury and serve tens of thousands of members, with new DAOs forming constantly.

DAOs need to accumulate secondary assets to build sustainable treasuries; otherwise, they risk substantial loss of native token value during market downturns. As a result, many DAOs are experimenting with strategies such as acquiring voting-escrowed tokens, hoarding stablecoins, adopting Protocol Controlled Value (PCV), and deploying capital to generate yield.

Growth in DAO numbers will drive demand for governance and coordination tools. Smaller sub-DAO units are also expected to emerge within larger DAOs, with micro-autonomous groups proliferating and operating on tools like Orca Protocol and Squads. Additionally, meme DAOs may experience explosive growth, with the biggest beneficiaries being the tools and platforms that enable DAO creation and management.

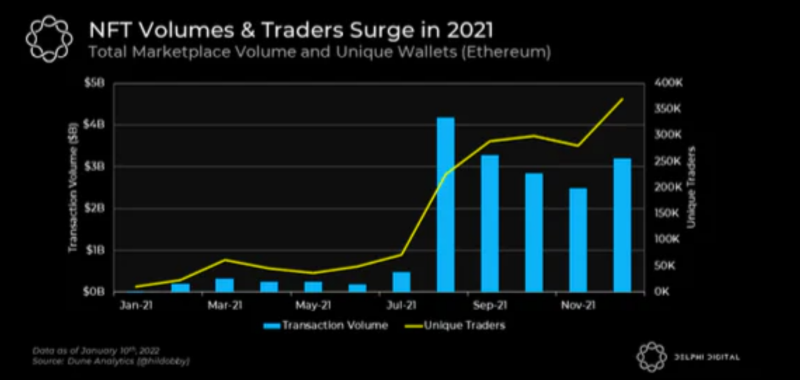

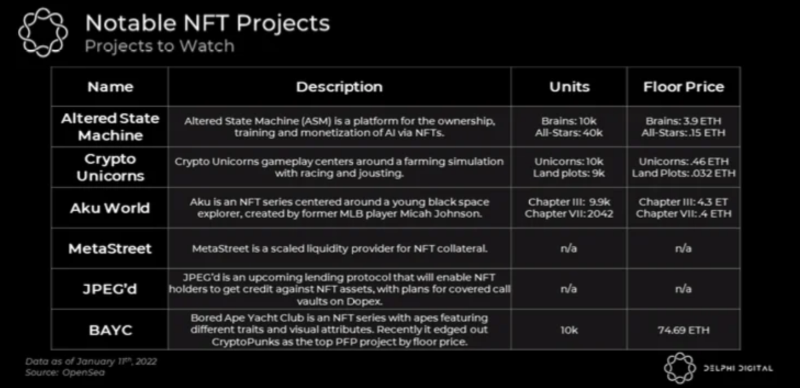

NFTs: From Static Collectibles to Interactive Digital Ownership

NFTs took off in 2021—though they’ve existed for years, 2021 marked their entry into mainstream discourse, with platforms like OpenSea experiencing explosive growth. The NFT market attracted numerous traditional companies and celebrities. NFTs started 2022 strongly—January 2022 was the best month on record for NFT volume and number of transactions, with buyer enthusiasm for new projects remaining very high.

NFT tools and infrastructure are also stepping into the spotlight, enabling artists to launch NFT projects by customizing and deploying smart contracts with just a few clicks—no technical expertise required.

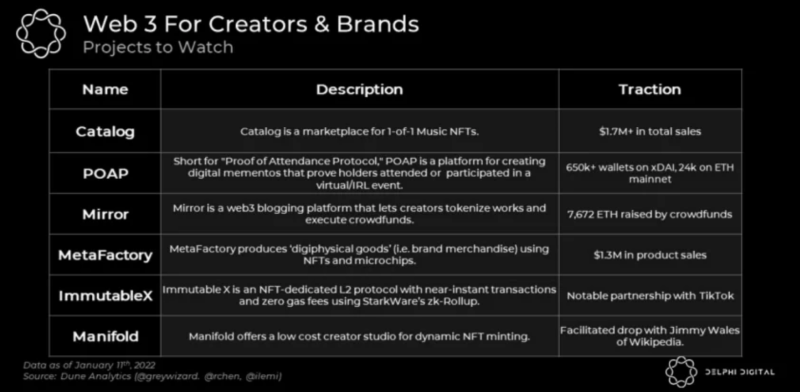

Creators and Brands Enter Web3

Web2 platforms like Patreon and Substack revolutionized creators and brands by giving them control over distribution and monetization. Now, with the rise of NFTs and tokenized communities, this is being elevated to a new level. Tokenizing intangible value—such as fanbases—creates an entirely new investable asset class for individuals. Artists, athletes, celebrities, and influencers are already exploring how NFTs and tokens can strengthen connections with fans and followers.

Music NFTs offer a concept similar to copyright—but without legal complexity—and represent a sub-sector poised for explosive growth in the coming years. Catalog’s 1-of-1 music NFT model appears particularly compelling, though models like Royal and Sound also hold significant potential.

Crypto Market 'Homogenization' Will Improve

Fundamentals will become an increasingly important driver of performance, especially as crypto attracts more capital and investor attention. Recent weeks have shown high correlation among crypto assets—driven largely by spikes in market volatility, which tend to strengthen positive correlations across crypto regardless of fundamentals. However, this phenomenon isn't unique to crypto; traditional asset classes like equities also exhibit higher intra-market correlations during volatile periods. During times of extreme uncertainty, macro events still dominate price action.

Yet, as in mature financial markets, similarly categorized assets do not remain highly synchronized indefinitely. The crypto market is expected to mature further, reducing the long-criticized “homogenization” effect. Performance across segments like BTC, ETH, DeFi, NFTs, and L1/L2s will become more differentiated. Over the next few years, crypto investing will increasingly bifurcate between “mainstream” cryptos (e.g., BTC), which remain sensitive to key macro drivers and gradually exhibit traits of traditional asset classes, and “Web3 cryptos,” whose performance will depend more on the type of asset or protocol and whether specific events directly impact their value proposition. In short, the success of these DApps and protocols will be driven more by adoption and usage activity.

This doesn’t mean macro factors won’t affect the broader crypto market. Rather, specific sectors and their associated assets will benefit from strong fundamentals. Investors who can identify trends early will be better positioned to manage their portfolios effectively.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News