Jump Crypto: Why We’re Bullish on the Crypto Derivatives Market in 2022?

TechFlow Selected TechFlow Selected

Jump Crypto: Why We’re Bullish on the Crypto Derivatives Market in 2022?

In 2021, critical infrastructure will continue to evolve to better support and guide institutions in this mobility (more information below), and an increasing number of institutions will gradually develop interest in the cryptocurrency market.

Author: Shanav K Mehta

Translation: TechFlow

Although the cryptocurrency derivatives market is expanding rapidly, its underlying instruments and infrastructure remain relatively immature compared to traditional financial markets. Given the increasing scale, improving quality, and growing institutional participation in infrastructure over the past year, we believe 2022 will bring breakthrough growth for crypto derivatives, along with greater market maturity. This article outlines the current state of the crypto derivatives market, key infrastructure developments that will drive future growth, and the areas where we expect expansion.

Overview

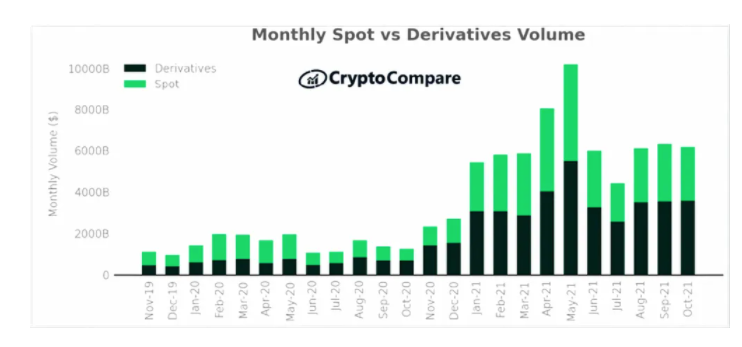

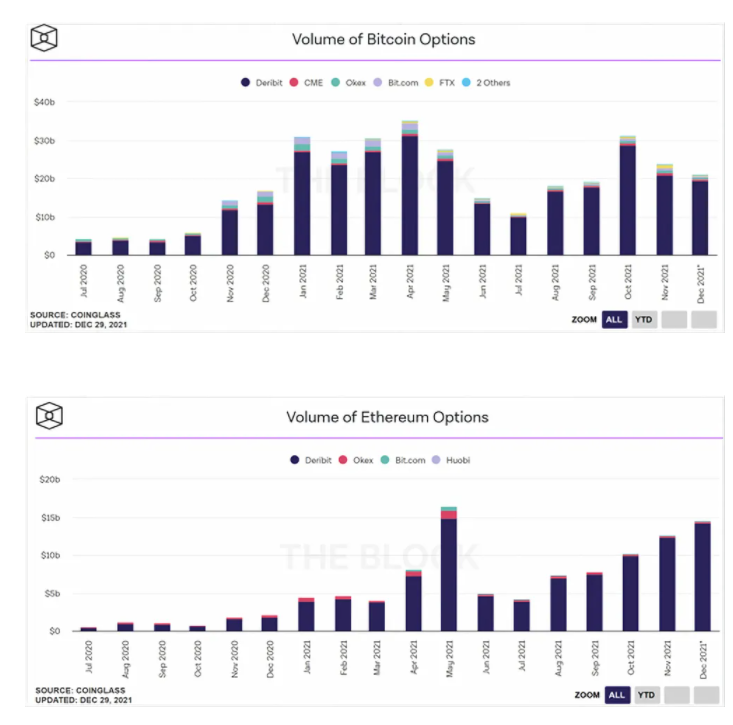

Today, cryptocurrency futures and options ("F&O") account for approximately 57% of total monthly trading volume. While this volume is substantial overall, we can assess market maturity by examining the relative distribution of volume across instruments and venues. The majority of trading remains concentrated in centralized perpetual futures, while options and related instruments are still in their infancy. Crypto options trading volume as a percentage of spot volume stands at just 2%, which has become a benchmark—compared to 35 times higher in the U.S. equities market.

Furthermore, the decentralized derivatives market (including both futures and options) remains significantly underdeveloped relative to its centralized counterpart. The chart below illustrates the relative market concentration.

We expect two main factors to further drive growth in crypto derivatives trading volume in 2022: 1) the rise of enabling infrastructure, and 2) increased institutional participation. To better understand the second factor, it's important to examine why TradFi institutions use derivatives more heavily than spot in equity markets. There are four primary reasons:

1. Capital Efficiency: Trading on margin offers superior capital efficiency when the potential percentage decline is less than the leverage used.

2. Tax Efficiency: In the U.S., 60% of gains from derivative contracts are taxed as long-term capital gains regardless of holding period, whereas spot assets must be held over one year to qualify for long-term treatment.

3. Hedging: Derivatives allow institutions to hedge temporarily while maintaining long-term exposure to physical equities.

4. Higher Liquidity: Derivatives markets offer better risk efficiency for market makers, resulting in deeper liquidity.

In 2021, critical infrastructure continued evolving to better support and channel this type of institutional liquidity (more details below), and increasing numbers of institutions began showing interest in crypto markets. As more institutions enter, relative volatility is likely to decline, enhancing the capital efficiency of derivatives trading. Additionally, as crypto assets appear on more institutional balance sheets, derivative tools will become increasingly vital for hedging short-term fluctuations. Together, these dynamics create a powerful wave that we believe will drive the crypto derivatives market over the next 12–24 months.

Overall, we anticipate 2022 will be the year of crypto derivatives, marked by three key trends:

1. The rise of centralized and decentralized options infrastructure;

2. Growth in decentralized perp futures volume;

3. Ongoing innovation around new crypto primitives such as structured vaults and perpetual options.

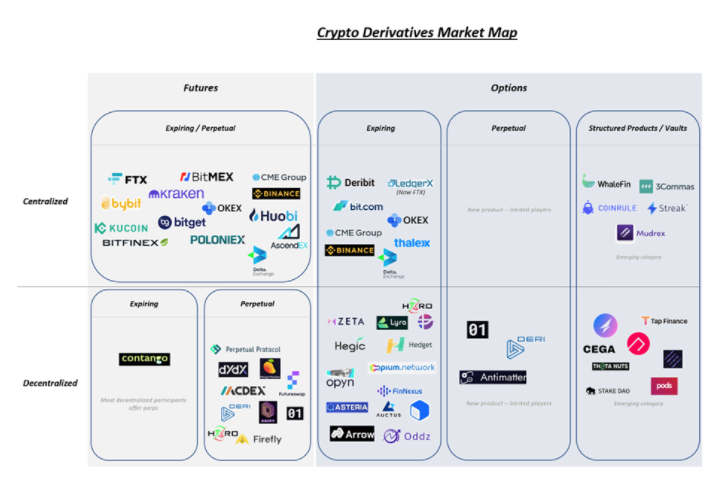

Centralized Infrastructure

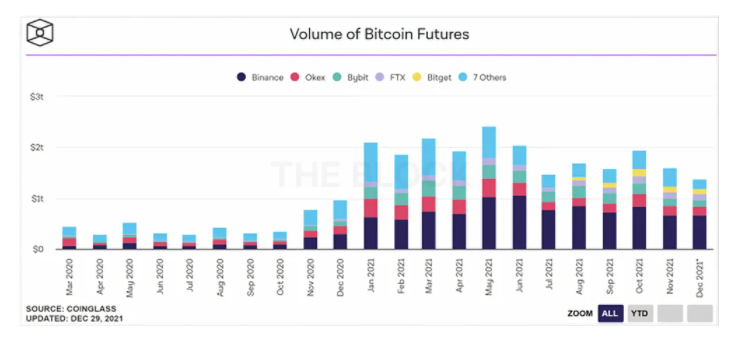

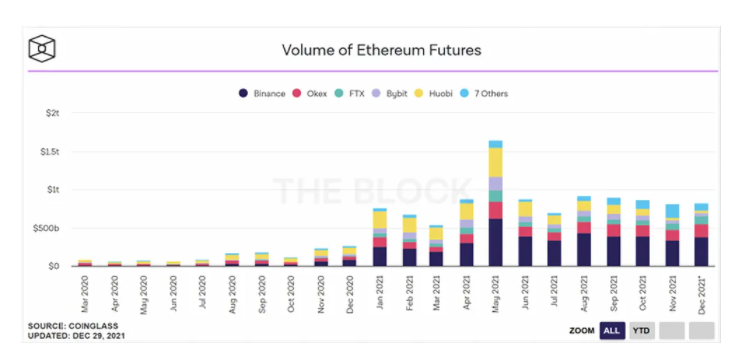

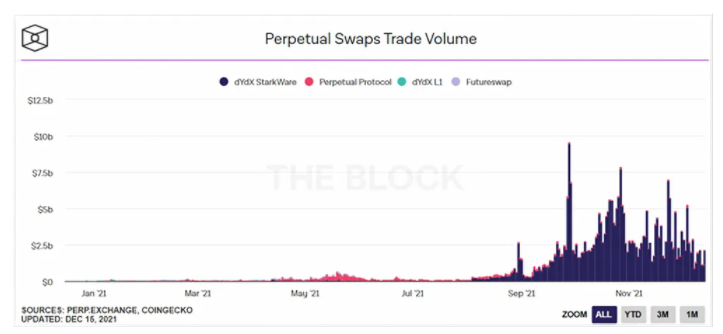

Today, most derivatives trading occurs on centralized exchanges, predominantly in perpetual futures. Perpetual futures were pioneered by BitMEX in 2016 and later popularized by Binance, CME, FTX, and others. Monthly BTC+ETH trading volume in perps now hovers around $250 million.

Given that centralized exchanges provide the regulatory and execution infrastructure required by institutional participants, we expect Ethereum futures volume to continue rising as organized players enter the market. As the perpetual futures market expands, we anticipate options platforms will follow. Although today’s crypto options market reaches $35 billion in monthly BTC+ETH volume, it remains relatively nascent and is dominated primarily by Deribit. One key reason may be that historically high volatility in crypto markets has made futures a preferred vehicle for traders to express directional views. Additionally, since few institutions historically held crypto on their balance sheets, demand for options as a hedging tool was limited. We expect both factors to change with increased institutional participation. Over the next 12 months, we anticipate more organized players entering the centralized options market to meet growing demand amid broader market expansion. We see FTX’s acquisition of LedgerX in October last year as an early signal of this trend.

As these markets mature, liquidity will naturally begin to fragment across venues in terms of execution efficiency and capital utilization. As a result, liquidity networks like Paradigm will become increasingly important, potentially serving as core infrastructure to facilitate institutional participation. Through Paradigm, institutions can submit automated, anonymous RFQs for futures and options trades, with guaranteed settlement against KYC’d counterparties. As more traditional financial institutions enter crypto, we believe such infrastructure will ensure ease of access and drive significant growth for centralized venues.

Decentralized Infrastructure

Like centralized venues, trading volume in decentralized derivatives is largely driven by perpetual futures. Initially led by perpetual swap protocols and recently dominated by dYdX, decentralized perps typically see daily trading volumes around $5 billion. Despite recent spikes, decentralized perp volume still accounts for less than 1% of total crypto derivatives volume. We expect substantial growth in decentralized perp volume over the next 12–24 months, driven by three main factors:

1. Compatibility with other DeFi applications: As new projects and protocols launch and build atop decentralized perpetual swap protocols, the value supported by these platforms will continue to grow.

2. Low-cost/high-speed execution infrastructure: Faster blockchains like Solana, and Ethereum scaling solutions such as Arbitrum, Optimism, and StarkEx/Net, offer lower transaction costs and improved user experience. We expect this to attract higher trading volumes. A prime example is dYdX’s recent implementation of StarkEx, which enables off-chain computation and reduced trading costs by an order of magnitude over the past three months. We believe we are still in the early stages of scalability—both within EVM and beyond—and expect these solutions to make the decentralized derivatives trading experience significantly smoother over the next 12 months. Projects like HXRO are already laying foundational infrastructure critical for the development of on-chain decentralized futures and options on chains like Solana.

3. Open access: Unlike centralized venues, decentralized protocols are permissionless. As crypto adoption grows globally—including in remote regions—we expect users excluded from centralized infrastructure to increasingly participate via decentralized protocols.

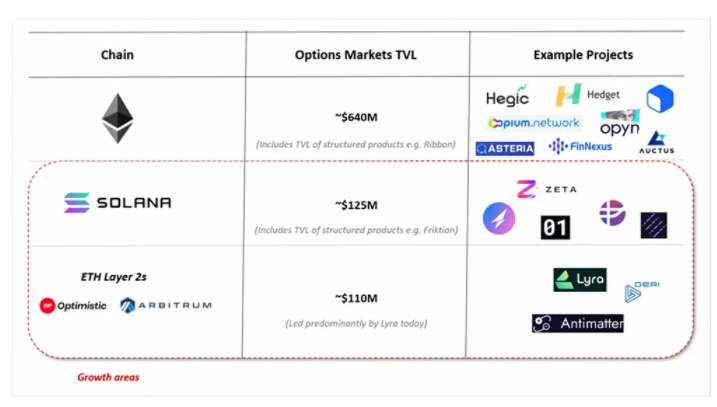

As decentralized futures markets evolve, we expect options markets to follow closely. Today, decentralized options represent only a small fraction of the overall derivatives market, with most mature protocols operating on the Ethereum mainnet. However, viable solutions are emerging to address three longstanding barriers that have constrained decentralized options growth. We anticipate these will unlock the market within the next 12 months:

1. Transaction fees + block time: Transaction fees can significantly impact margins, especially for longer-dated options. Historically, high Ethereum gas fees have disadvantaged decentralized options trading. Moreover, long block times introduce execution uncertainty and pose challenges for multi-leg trades unless atomic. These issues also hinder order book-based market making. Additionally, leveraged protocols require liquidators to step in when positions are at risk. If liquidators must pay high miner fees to clear bad debt and reduce platform risk, it discourages participation. To compensate, protocols must share more revenue with liquidators, undermining sustainable business models. With low-cost, high-speed environments now available via Solana and Ethereum scaling solutions like Arbitrum and Starkware, these challenges are being mitigated, enabling viable options trading.

2. Hedging AMM pool liquidity: Protocols selling options typically require liquidity backing. Most achieve this through AMM structures. However, this often leaves delta risk unhedged in pools, potentially leading to significant impermanent loss. Such events have previously caused protocols like Charm on Ethereum to pause their options offerings. Like traditional finance option sellers, decentralized options protocols must delta-hedge their liquidity pools to manage impermanent loss. This is typically done using futures—an internal DeFi market that has only recently begun emerging. As these primitives mature, we expect options protocols to become more liquid and active.

3. Full collateralization requirements: Due to block time limitations and the inability to implement atomic liquidations, many existing DeFi options implementations require full collateralization. By leveraging faster chains like Solana and more robust clearing engines (with more frequent oracle updates), we foresee protocols like Zeta eventually offering undercollateralized options.

Another set of primitives we expect to accelerate decentralized options usage is structured DeFi options vaults (“DOVs”). DOVs are game-changers—they democratize access to implied-volatility-driven yield while providing scalable ways to manage nonlinear risk. Through basic strategies like covered call writing and cash-secured put selling, DOV platforms give retail traders access to yield-enhancing hedged returns while ensuring liquidity for underlying options protocols. Vault platforms like Ribbon have grown to $300 million in TVL, while newer entrants like Friktion (over $100 million TVL) and Katana (over $45 million TVL) scaled rapidly within weeks of launch, signaling strong market demand. As these protocols scale further, we expect the decentralized options trading experience to become increasingly seamless.

Overall, the foundation for a thriving decentralized options market is finally in place. We expect significant capital inflows into this space over the next 12–24 months, particularly on Solana and Ethereum scaling solutions.

Beyond decentralized futures, options, and structured products, we are excited to see innovative crypto-native instruments like perpetual options developing in sandbox environments. Inspired by the success of perpetual futures, Dave White and Sam Bankman-Fried introduced the concept of perpetual options in their original paper. A perpetual option can be replicated using a series of options with different expirations, weighted arithmetically in an exponentially decaying manner (e.g., 50% weight on today’s expiry, 25% on tomorrow’s, etc.), making replication relatively straightforward. Protocols like 01 have implemented floating strike prices—exponentially weighted averages of the underlying asset price over time—allowing perpetual options to span all strike levels while preserving their perpetual nature. Finally, we’re seeing protocols like Deri offering both perpetual futures and perpetual options, enabling users to trade derivatives in a highly DeFi-native way, using options and futures for on-chain hedging, speculation, and arbitrage. We look forward to seeing more such services go live on mainnet soon.

Conclusion

We firmly believe we are on the cusp of massive growth in the decentralized derivatives market over the next 12–24 months.

The infrastructure needed to launch these products and support the next wave of billion-dollar protocols is already in place.

Entering 2022, we are excited to support some of the most fundamental projects driving this revolution—including Paradigm, Zeta Markets, Friktion, Lyra, Drift, and others.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News