Bitget UEX Daily Report | Trump Plans to Declare Iran Conflict “Victoriously Concluded”; SpaceX’s Secret IPO; Storage and Optical Communications Sector Strongly Rebounds

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Plans to Declare Iran Conflict “Victoriously Concluded”; SpaceX’s Secret IPO; Storage and Optical Communications Sector Strongly Rebounds

Overall, short-term market risk appetite is expected to continue. We recommend focusing on the technology, aerospace, and memory sectors, while maintaining a cautiously optimistic stance toward crypto assets. The ETF fund inflow trend is worth continued monitoring.

Author: Bitget

I. Key News Highlights

Federal Reserve Developments

Richmond Fed President Barkin: Oil price shock viewed as temporary; consumer spending remains resilient

- Richmond Fed President Thomas Barkin noted that although oil prices have risen due to geopolitical conflict, businesses and households widely perceive this as a transient phenomenon—consumer spending has not declined noticeably, and inflation expectations remain stable.

- He emphasized that future Fed policy adjustments will hinge primarily on whether inflation expectations rise significantly. No clear upward signal has yet emerged, and markets broadly anticipate the Fed will maintain its wait-and-see stance.

- Market impact: This statement eased investor concerns over prolonged high interest rates, supporting a rebound in risk assets—and further confirmed sustained consumer resilience amid improving macroeconomic data.

International Commodities

IEA Executive Director warns oil supply crisis will intensify in April; considers additional SPR releases

- Fatih Birol, Executive Director of the International Energy Agency (IEA), stated that the Iran conflict has already triggered oil supply shortages and pushed up prices, with the crisis expected to worsen over the next month.

- The IEA is evaluating the possibility of another Strategic Petroleum Reserve (SPR) release to ease global supply tightness.

- Market impact: In the near term, oil prices remain supported at elevated levels; however, if SPR releases materialize, they could rapidly alleviate the geopolitical premium and prompt a correction in crude oil prices.

Macroeconomic Policy

Trump plans to declare “victory” in Iran conflict and shift responsibility for Strait of Hormuz shipping restrictions to NATO; tariff reform and economic data both exceed expectations

- At 9:00 a.m. (UTC+8) today, Trump delivered a speech declaring the one-month-long Iran conflict nearing conclusion and announcing plans to assign responsibility for Strait of Hormuz maritime restrictions to NATO allies. Meanwhile, Iranian intelligence assessments indicate Tehran currently has no intention of engaging in substantive negotiations. However, according to a New York Times report citing U.S. officials, multiple U.S. intelligence agencies recently assessed that the Iranian government is unwilling to enter into substantive negotiations to end the U.S.-Israel war.

- The Trump administration is preparing to revise steel and aluminum tariffs: the new structure will impose a flat 25% tariff on finished goods, replacing the prior complex system that levied a 50% tariff based on metal value. A pharmaceutical tariff adjustment plan is also under consideration.

- U.S. February retail sales rose 0.6% MoM; March ADP private sector employment added 62,000 jobs—both figures surpassed consensus expectations.

- Market impact: Geopolitical de-escalation signals boosted risk appetite, while tariff simplification may benefit domestic manufacturing—but could also escalate trade tensions. Stronger-than-expected economic data further reinforces expectations of continued consumer resilience.

II. Market Recap

Commodities & FX Performance

- Spot gold: Up ~0.64% to ~$4,800/oz, extending gains amid ongoing geopolitical uncertainty.

- Spot silver: Up ~0.61% to ~$75.50/oz, tracking gold’s strength while remaining range-bound.

- WTI crude: Down ~2% to ~$98/bbl, driven by optimism surrounding an imminent end to the Iran conflict.

- Brent crude: Down ~1.48% to ~$99.66/bbl, as the geopolitical premium recedes.

- U.S. Dollar Index: Slightly volatile at 99.52, influenced jointly by the Fed’s wait-and-see posture and geopolitical easing signals.

Cryptocurrency Performance

- BTC: Up ~0.14% over 24H to ~$68,382, exhibiting a modest rebound amid geopolitical easing—reflecting improved market risk sentiment.

- ETH: Up ~1.76% over 24H to ~$2,146, broadly tracking the broader market and holding key technical support.

- Total crypto market cap: Up 0.1% to ~$2.43 trillion.

- Liquidations: ~$270 million liquidated over 24H—~$110 million longs, ~$160 million shorts.

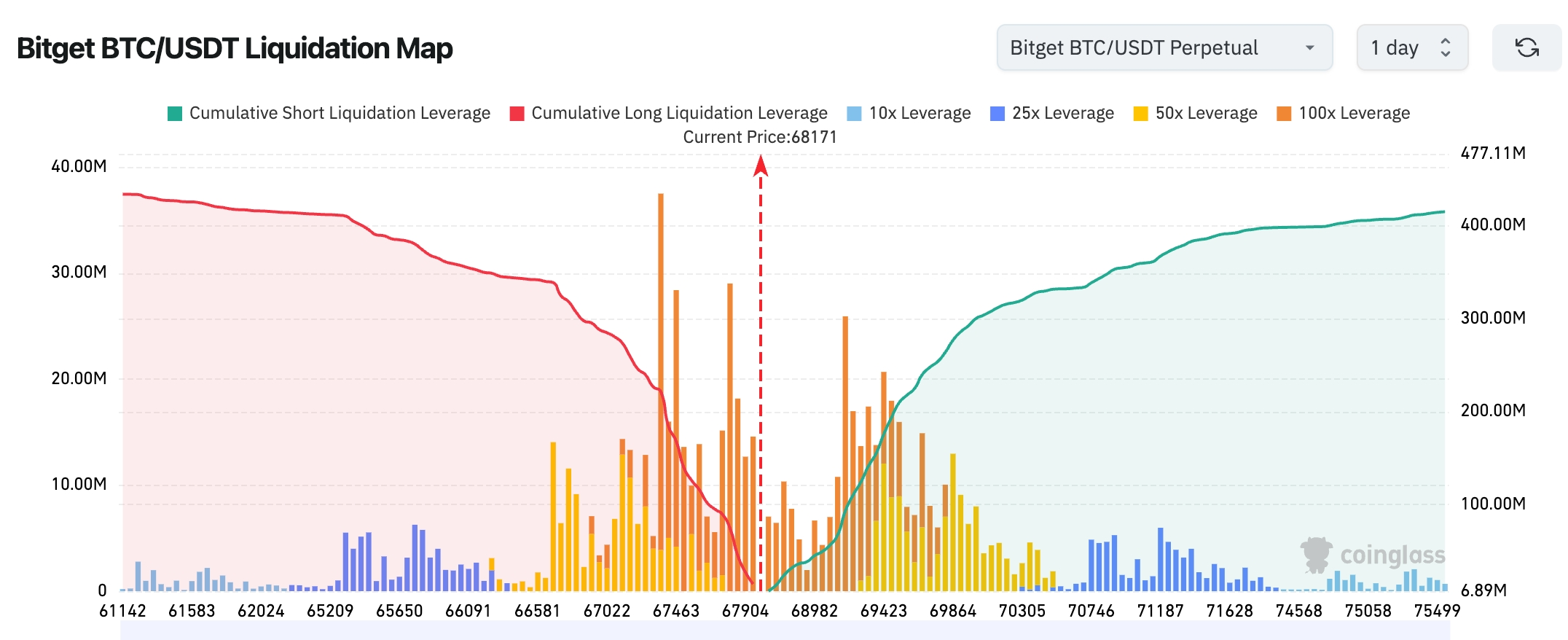

- Bitget BTC/USDT Liquidation Map: Current price ~$68,171. Heavy 50x–100x long liquidation pressure accumulates between $69,000–$70,000; any rally approaching this zone risks triggering clustered liquidations and forming upside resistance. The $67,000–$67,500 zone represents relatively solid support following gradual short liquidation—creating a structural “resistance above, support below.” Short-term price action is likely to consolidate around $68,000 before choosing direction.

- Spot ETF net flows: BTC spot ETFs saw ~$87.2 million net outflow yesterday; ETH spot ETFs recorded ~$19.7 million net inflow.

- BTC spot flows: $2.154 billion inflow vs. $2.082 billion outflow yesterday—net inflow of ~$32.08 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: Up 0.48% to 46,565.74—rebounding for two consecutive days.

- S&P 500: Up 0.72% to 6,575.32—gaining modestly, led by technology stocks.

- Nasdaq Composite: Up 1.16% to 21,840.95—driven by broad-based strength across tech names.

Tech Giants’ Performance

- Apple (AAPL): Up 0.73% to ~$255.63, buoyed by overall tech sentiment.

- Microsoft (MSFT): Down 0.22% to ~$369.37—supported by AI demand but experiencing minor pullback.

- NVIDIA (NVDA): Up 0.77% to ~$175.75, lifted by chip sector rebound.

- Google (GOOGL): Up 3.42% to ~$297.39—AI and search business performance stood out.

- Amazon (AMZN): Up ~1.1% to ~$210.57—boosted by satellite acquisition rumors.

- Meta (META): Up 1.24% to ~$579.23—following broader tech gains.

- Tesla (TSLA): Up 2.56% to ~$381.26—benefiting from overall market optimism. Core driver: Geopolitical easing signals combined with AI and tech fundamentals propelled all seven mega-cap stocks higher.

Sector Rotation Highlights

Memory & Optical Communications Sector: Up >8%

- Key stocks: SanDisk up >9%, LITE up >8%.

- Catalyst: Improved market expectations for data center and communications demand—sector continues rebounding.

Satellite & Aerospace-Related Sector: Strong after-hours performance

- Key stock: Globalstar surged >18% after hours.

- Catalyst: Rumors of Amazon’s acquisition talks, coupled with SpaceX’s rumored confidential IPO filing, created competitive anticipation.

III. Deep-Dive Stock Analysis

1. SpaceX – Filed Confidential IPO Application

Event Summary: According to sources, SpaceX has confidentially filed an IPO application with regulators, targeting a valuation of ~$1.75 trillion. This marks the transition of Musk’s most valuable private company toward public markets—and sets up potential competition with rumors of Amazon acquiring satellite firm Globalstar. Market Interpretation: Institutions broadly believe SpaceX’s listing would inject liquidity into the aerospace and satellite communications sector, with valuation premiums likely lifting related supply-chain stocks. Given SpaceX’s leadership in Starlink network deployment and reusable rocket technology, its IPO—if approved—could reshape market perceptions of commercial space value, much like Tesla did via public markets, enabling capital recycling to accelerate Starlink expansion and deep-space exploration. Analysts expect this move to dilute Musk’s personal stake and trigger a re-rating of the entire aerospace supply chain—especially as defense and commercial satellite demand rebounds amid current geopolitical easing. Investment Implication: The aerospace supply chain may offer long-term allocation opportunities. Investors should monitor Starlink-related component suppliers—but closely track regulatory approval progress and market capacity to absorb valuations, avoiding short-term overvaluation-driven corrections.

2. Globalstar (GSAT) – Amazon in Acquisition Talks

Event Summary: Amazon is reportedly in acquisition talks with satellite communications firm Globalstar—a development potentially positioning it in direct competition with SpaceX. Globalstar’s after-hours share price surged >18%. Market Interpretation: Analysts note that a successful acquisition would significantly strengthen Amazon’s low-earth-orbit (LEO) satellite network, reinforcing its cloud services and IoT ecosystem. As a pure-play U.S.-listed stock, Globalstar’s LEO assets align seamlessly with Amazon’s AWS infrastructure—quickly filling gaps in enterprise IoT and remote-area coverage left by Starlink. Moreover, this deal may spark a wave of M&A across the satellite communications industry, shifting focus from “conceptual hype” to “revenue realization”—particularly under pressure from SpaceX’s IPO. Amazon’s move is thus viewed as a defensive strategic play. Investment Implication: The satellite communications sector offers strong near-term catalysts. Investors are advised to monitor GSAT’s valuation recovery and merger probability—and consider concurrently allocating to Amazon stock to capture synergistic benefits across the value chain.

3. SanDisk (SNDK) / Memory Sector Stocks – Continued Rally

Event Summary: The memory and optical communications sector extended its strength, with SanDisk shares rising >9%, supported by robust data center demand. Market Interpretation: Institutions attribute surging memory demand to AI compute expansion—fundamentals remain solid. As a standalone U.S.-listed memory leader, SanDisk’s technological edge in high-bandwidth memory (HBM) and enterprise SSDs positions it directly to benefit from ramping AI servers such as NVIDIA’s GB200. Global data center capex grew >30% QoQ, and supply constraints are unlikely to ease soon. Analysts raised their 2026 revenue forecasts for the sector by 15%–20%, highlighting SanDisk’s high-margin advantage in AI training/inference applications—which should drive valuation recovery from current depressed levels toward historical averages. Investment Implication: Data center-related supply chains retain allocation appeal. Investors may accumulate core names like SNDK on dips—and watch next quarter’s earnings for confirmation of AI demand sustainability.

4. LITE (Lumentum) – Optical Communications Sector Leader

Event Summary: Optical communications stock LITE rose >8%, continuing the sector’s rebound momentum. Market Interpretation: Analysts underscore strong demand for 5G and data center optical modules—valuing the sector as undervalued and ripe for re-rating. As a pure-play U.S.-listed optical module leader, Lumentum holds leading market share in 800G/1.6T high-speed optical engines—benefiting from the global data center upgrade from copper to fiber. Coupled with surging AI cluster demand for ultra-low-latency, high-bandwidth interconnects, institutional models project LITE’s FY2026 EPS growth exceeding 25%. Its current valuation trades at a notable discount versus peers, and market expectations point to further order visibility confirmation during upcoming earnings reports. Investment Implication: The optical communications supply chain exhibits strong medium-term fundamentals—suitable for accumulation on dips in quality names like LITE, while aligning positioning with macro interest-rate trajectories to assess sustainability.

5. Eli Lilly (LLY) – Oral Weight-Loss Drug Approved

Event Summary: Eli Lilly’s oral weight-loss drug received FDA approval, driving shares up 3.78%. Market Interpretation: Institutions view Lilly as possessing a competitive edge in the weight-loss drug market, expecting further market share gains. As a benchmark for U.S. biopharma innovation, Lilly’s oral formulation fills a convenience gap in its pipeline while complementing injectables—positioning it to capture market share from Novo Nordisk’s Ozempic/Wegovy. Wall Street’s latest model raises Lilly’s 2026 weight-loss drug revenue forecast to >$15 billion, emphasizing clinical advantages of its GLP-1 drugs in cardiovascular complication indications—supporting long-term CAGR of >20%. Investment Implication: The biopharma innovation segment retains long-term growth potential. Monitor Lilly’s pipeline progression—and diversify across other U.S.-listed innovative biotechs to hedge regulatory risk.

IV. Cryptocurrency Project Updates

1. Zack Wainwright, Research Analyst at Fidelity Digital Assets, noted that Bitcoin’s current cycle retracement from its all-time high stands at ~50%, far shallower than the 80%–90% drawdowns seen in prior cycles—indicating market maturation, reduced volatility, and growing institutional confidence.

Nick Ruck, Director at LVRG Research, observed that this reflects Bitcoin’s evolution from a speculative asset toward a more stable store of value. Bitcoin hit its cycle low of ~$60,000 on February 6—down 52% from its October 2023 ATH of $126,000. In contrast, the prior cycle fell 77% from $69,000 (Nov 2021) to $16,000 (June 2022).

Analysts also estimate, based on historical decay patterns, that the bottom of this cycle may occur between late September and early October 2026.

2. Monad blockchain’s Total Value Locked (TVL) reached $355 million—surging >55% since early February—making it the fastest Layer-1 to breach $300 million TVL in recent years. However, Monad’s daily fee revenue remains below $3,000, meaning its $355 million capital base generates only ~six-figure annual income. Its fee-to-TVL ratio ranks lowest among all major blockchains with substantial TVL.

3. Aave V4 officially launched at EthCC, adopting a hub-and-spoke architecture to support Real World Assets (RWAs)—further expanding DeFi’s application frontier.

4. Michael Selig, Chairman of the U.S. Commodity Futures Trading Commission (CFTC), stated the agency is prepared to regulate the entire $3 trillion cryptocurrency industry—and reiterated the CFTC’s exclusive jurisdiction over prediction markets. The CFTC has signaled a notably more permissive enforcement and regulatory stance toward digital assets compared to the previous administration.

5. According to BitcoinTreasuries.NET, Strategy’s newly issued preferred stock (STRC) recently raised funds sufficient to purchase 2,724 BTC.

V. Today’s Market Calendar

Economic Data Release Schedule

| 20:30 | U.S. | Initial Jobless Claims | ⭐⭐⭐⭐ |

| 22:00 | U.S. | ISM Services PMI | ⭐⭐⭐ |

| 22:00 | U.S. | Trade Balance | ⭐⭐ |

Key Event Previews

- Trump’s Iran conflict-related speech: Today at 09:00 (UTC+8)—watch for “victory” framing and implications for geopolitical risk and oil prices.

- SpaceX IPO developments: Ongoing monitoring—track valuation re-rating opportunities in aerospace sector.

April 2 (Thursday)

- Dallas Fed President Lorie Logan (2026 FOMC voter) speaks at 23:00;

- U.S. initial jobless claims for week ending March 28 released at 20:30.

April 3 (Friday)

- U.S. March unemployment rate and nonfarm payrolls released at 20:30; U.S. March S&P Global Services PMI final reading released at 21:45;

- U.S. equity markets closed for Good Friday.

*This week’s U.S. equity theme centers on Fed official commentary, NFP and ADP employment data, and Tesla delivery figures. Overlapping labor data and policy signals suggest heightened market volatility.

Institutional Views:

Fueled by geopolitical de-escalation signals, U.S. equities rallied collectively yesterday—the Dow, S&P 500, and Nasdaq rose 0.48%, 0.72%, and 1.16% respectively, led by tech stocks. Gold held near $4,800, while crude oil fell ~2% on “victory in sight” expectations. Crypto markets rebounded in tandem—BTC edged up to ~$68,200 and total market cap rose to ~$2.35 trillion. Top-tier investment banks broadly agree that Trump’s confirmation of an imminent end to hostilities would materially reduce the geopolitical premium—favoring risk assets and consumer discretionary sectors—and ease pressure on the Fed to hold rates steady indefinitely. Goldman Sachs and JPMorgan strategists noted that while tariff simplification may raise certain import costs, it broadly benefits domestic manufacturing—and, combined with stronger-than-expected retail sales and ADP data, validates consumer resilience. However, institutions caution against overlooking actual Strait of Hormuz reopening progress: delayed negotiations could still lift oil and gold prices. Overall, short-term risk appetite appears poised to continue—recommended exposure includes tech, aerospace, and memory sectors; crypto assets warrant cautious optimism, with ETF fund flow trends meriting close tracking.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News