Bitget UEX Daily Report | Jensen Huang Unveils NemoClaw; IEA Still Has Additional Oil Reserves Available; Bitcoin Reclaims $75,000

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Jensen Huang Unveils NemoClaw; IEA Still Has Additional Oil Reserves Available; Bitcoin Reclaims $75,000

The overall market sentiment is cautiously optimistic, and institutions recommend paying attention to the ripple effects of the Fed meeting on global assets.

Author: Bitget

I. Top News Highlights

Federal Reserve Updates

Trump Administration Asks Judge to Reconsider Decision to Quash Subpoena for Powell

- Attorneys for the Trump administration have asked a federal court judge to reconsider the decision to quash a grand jury subpoena issued to Federal Reserve Chair Jerome Powell—a move that could delay Philip Jefferson’s potential succession as Fed Chair.

- Key Republican senators have repeatedly referenced the case, underscoring the risk of political interference in Fed appointments.

- This development intensifies market concerns over the Fed’s independence, potentially amplifying short-term USD volatility and reshaping investor expectations for the interest rate path.

Global Commodities

Trump Hints at Strike on Iran’s Kharg Island Oil Facilities; IEA Says Further Oil Reserves Can Be Released

- Trump warned that pipelines on Iran’s Kharg Island may be targeted, noting that U.S. forces have already struck over 7,000 Iranian targets; Iran responded with vows of retaliation against U.S. assets across the Middle East.

- The International Energy Agency (IEA) stated that current emergency oil reserve releases have drawn down only 20% of reserves and affirmed its capacity to release more if needed, while also exploring demand-side measures to ensure energy security.

- Escalating geopolitical tensions raise upside risks to oil prices, potentially lifting global inflation expectations—short-term tailwinds for energy stocks but headwinds for broader equity markets.

World’s Largest Bauxite Exporter Considers Export Controls

- Guinea is in discussions with mining companies to regulate bauxite output volumes to prevent further price declines; exports reached 183 million tonnes last year, up over 25% year-on-year.

- This follows precedents set by the Democratic Republic of Congo’s cobalt export quotas and Zimbabwe’s lithium export ban—aimed at stabilizing corporate revenues and government tax income.

- Export restrictions on raw materials could exacerbate global supply chain tightness, push aluminum prices higher, and increase cost pressures on downstream industries such as automotive and construction.

Macroeconomic Policy

U.S. SEC Proposes Eliminating Mandatory Quarterly Earnings Disclosure for Public Companies

- The SEC plans to propose allowing public companies to opt for semi-annual instead of mandatory quarterly earnings reporting, with the proposal expected as early as next month.

- The initiative aims to reduce corporate reporting burdens but may lower market transparency.

- Relaxed disclosure requirements could improve operational flexibility for firms, yet heighten information asymmetry risks for investors—potentially triggering short-term market volatility.

Goldman Sachs Warns CTA Strategy Selling Pressure Not Yet Exhausted

- Goldman Sachs estimates $6.9–7.0 billion in global equity sell-offs from CTA strategies over the coming week, rising to $9.8–10.0 billion within one month; U.S. equities face the strongest impact as trend signals turn negative.

- Attention turns to this Friday’s “triple witching” day, when $1.3 trillion in options expire; Goldman recommends overweighting stagflation-resistant portfolios—long commodity and defensive stocks, short semiconductors.

- This warning intensifies expectations of market correction and may accelerate capital rotation into defensive assets, amplifying overall volatility.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Down 0.12% to $5,000/oz, pressured by USD strength and easing inflation expectations.

- Spot Silver: Down 0.55% to $80.19/oz, weighed down by weak industrial demand and broad precious metals correction.

- WTI Crude: Up 2.66% to $94.92/bbl, rebounding on stabilized geopolitical risk assessments.

- Brent Crude: Up 2.01% to $102.87/bbl, supported by eased global supply concerns.

- Dollar Index: Up 0.11% to 99.93, modestly strengthened by Fed policy expectations.

Cryptocurrency Performance

- BTC: +3.8% over 24H, climbing steadily to ~$75,200, driven by short-position liquidations and institutional buying.

- ETH: +8.4% over 24H, surging to ~$2,350 amid broad market momentum.

- Total Crypto Market Cap: +~3.6% over 24H to $2.65 trillion, buoyed by easing oil-driven inflation concerns improving overall sentiment.

- Liquidations: $571 million total liquidated in 24H—$124 million longs, $447 million shorts.

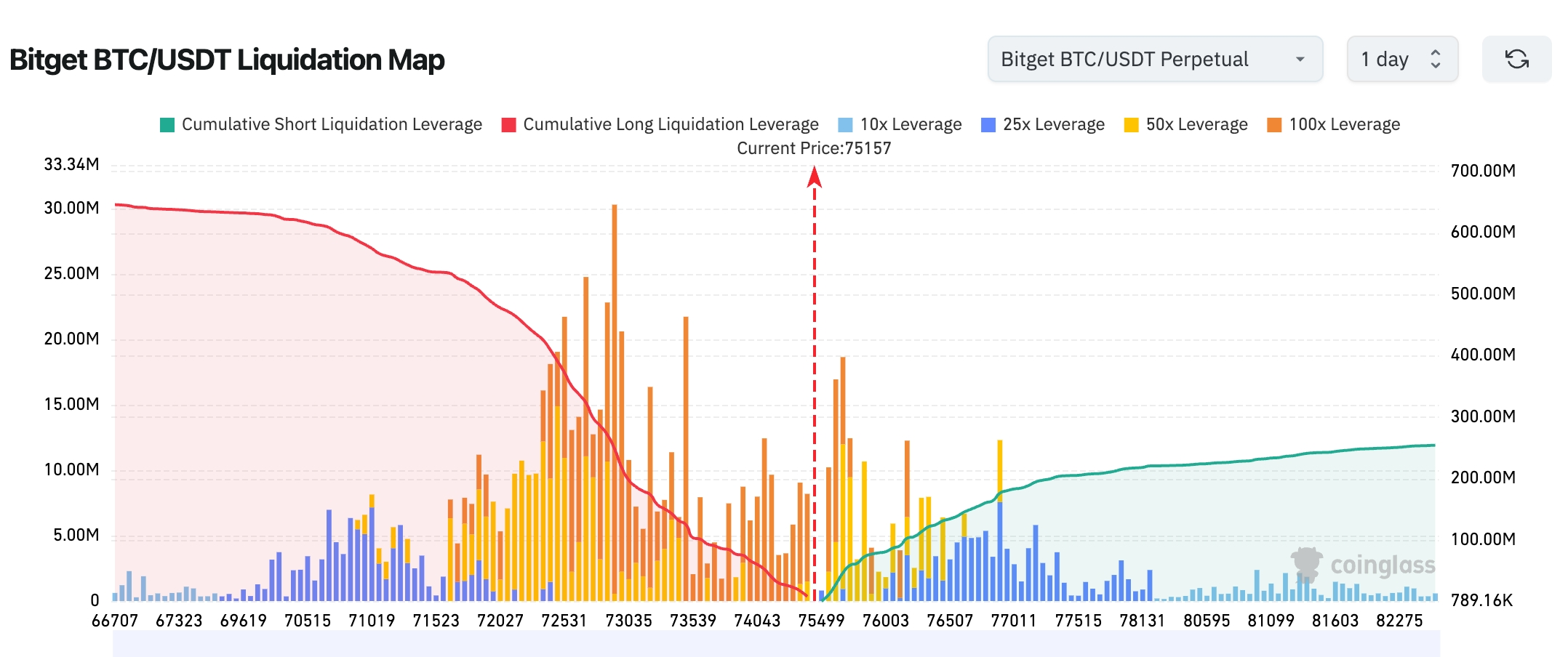

- Bitget BTC/USDT Liquidation Map: Current price ~$75,200. A dense cluster of long liquidations lies between $72,000–$74,000; a retest of this zone could trigger cascading long liquidations and accelerate downside moves. A clear concentration of short liquidations exists between $76,000–$78,000; continued upside may spark short squeezes and fuel further gains.

- Spot ETF Net Flows: BTC spot ETFs saw ~$60M net inflow over 24H; ETH spot ETFs saw ~$19.7M net inflow over 24H.

- BTC Spot Net Flows: Previous day saw ~$3.454B inflow vs. ~$3.216B outflow, netting ~$237M inflow.

U.S. Equity Index Performance

- Dow Jones: +0.83% to 46,946.41—ending recent losses, supported by rebounds in tech and energy sectors.

- S&P 500: +1.01% to 6,699.38—with large-cap leadership driving the rally.

- Nasdaq: +1.22% to 22,374.18—led by tech and innovation-related stocks.

Tech Giants’ Moves

- Apple (AAPL): +1.08% to ~$252, lifted by broader tech rebound.

- Google (GOOGL): +0.98% to ~$180, supported by improved ad revenue outlook.

- Microsoft (MSFT): +1.11% to ~$399, underpinned by robust cloud demand.

- Amazon (AMZN): +1.96% to ~$211, driven by e-commerce and AWS growth.

- Meta (META): +2.33% to ~$627, reflecting higher social platform user engagement.

- Tesla (TSLA): +1.11% to ~$395, buoyed by optimistic EV sales forecasts.

- NVIDIA (NVDA): +1.65% to ~$183, lifted by confidence following full-stack AI keynote. Core drivers: falling oil prices eased inflation worries; broad tech strength ended prior losing streak.

Sector Rotation Watch

Crypto-Related Stocks +~8%

- Examples: BMNR +13.88%, Circle +9.06%.

- Catalyst: Bitcoin breaking above $75,000 and ETF inflows spurring related stock rallies.

Memory Stocks +~5%

- Examples: SanDisk +6.35%, Western Digital +5.11%.

- Catalyst: Strong AI and data center demand, plus stable supply chain outlook.

Copper & Aluminum Stocks +~4%

- Examples: Alcoa +4.73%, Southern Copper +3.49%.

- Catalyst: Guinea’s proposed bauxite export controls boosting raw material price expectations.

III. In-Depth Stock Analysis

1. NVIDIA – Full-Stack AI Keynote Paints $1 Trillion Revenue Roadmap

Event Summary: In a two-hour-plus keynote, NVIDIA CEO Jensen Huang unveiled the “one-click shrimp farming” platform NemoClaw and projected aggressive revenue targets for AI compute chips—reaching $1 trillion by 2027. The company emphasized its full-stack AI strategy spanning chips, software, and services. Shares rose over 4.3% intraday before closing +1.65%. This vision rests on explosive AI demand to reinforce NVIDIA’s dominance in data center markets—though supply chain bottlenecks and geopolitical risks remain key watchpoints. Market Interpretation: Analysts view the forecast as emblematic of surging AI infrastructure investment. Goldman Sachs sees NVIDIA benefiting in stagflationary environments—but cautions that ongoing CTA selling pressure may weigh on shares near term. Investment Takeaway: Continued AI theme momentum may propel shares toward new highs, though investors should monitor indirect oil-price impacts on broader markets.

2. Yaocai Securities Financial – Ant Group Tender Offer Approved; Stock Resumes Trading Today

Event Summary: Yaocai Securities Financial received regulatory approval for Ant Group’s tender offer and resumes trading today. The acquisition aims to integrate resources and enhance digital financial services capabilities, with Ant injecting technological support to bolster Yaocai’s competitiveness in the Hong Kong equity market. Post-resumption performance—including trading volume and share price action—will be closely watched; potential integration risks include regulatory scrutiny and cultural alignment challenges. Market Interpretation: Analysts see this as positive for Hong Kong’s fintech ecosystem but flag potential cross-border business headwinds from U.S.-China trade friction. Investment Takeaway: Short-term rebound potential exists post-resumption, but long-term success hinges on Ant Group’s strategic execution.

3. SK Hynix – Exploring U.S. ADR Listing Possibility

Event Summary: SK Hynix confirmed it is evaluating the feasibility of issuing American Depositary Receipts (ADRs) in the U.S., aiming to broaden global funding channels and elevate brand visibility. Targeting growing memory chip demand—especially for AI applications—the move seeks to attract more institutional investors. The company stressed this remains an early-stage exploration contingent upon regulatory and market condition assessments. Market Interpretation: Institutional views are broadly positive, citing ADRs’ potential to mitigate FX risk—but caution that U.S.-China tech tensions could pose listing hurdles. Investment Takeaway: Successful implementation could lift share price, albeit with heightened short-term volatility.

4. TSMC – Gains Amid Broader China-Exposure Stock Rally

Event Summary: As a prominent China-exposed stock, TSMC rose 0.57% on the back of the broader rally. Its foundry business remains strong, propelled by AI and semiconductor demand—but escalating geopolitical tensions continue to cloud supply chain outlooks. Market Interpretation: Analysts deem TSMC’s valuation reasonable but warn of potential headwinds from U.S. Section 301 investigations. Investment Takeaway: Near-term gains likely track broader market momentum; medium-to-long-term performance depends on the global chip cycle.

5. Micron Technology – Memory Sector Strength Lifts Shares

Event Summary: Micron rose 3.68%, riding the broader memory sector rally. Its HBM chips remain in high demand, with AI applications fueling earnings growth—though intensifying competition poses risks. Market Interpretation: Institutions expect Micron to gain market share in data centers but highlight rising raw material cost pressures. Investment Takeaway: Significant sector rotation opportunities exist; monitor oil-price impacts on inflation dynamics.

IV. Cryptocurrency Project Updates

1. BlackRock withdrew 2,018 BTC from Coinbase over nearly nine hours. According to Lookonchain, address “bc1qfs” withdrew 1,938 BTC from Binance over the past six days—worth ~$138 million at current prices.

2. Bitwise CIO Matt Hougan noted that from the January 2024 launch of Bitcoin spot ETFs through October 2025, cumulative ETF net inflows totaled ~$60 billion. Though Bitcoin’s price later fell ~50%, ETF net outflows remained below $1 billion—indicating sustained institutional holding.

3. Blockworks data shows weekly on-chain spot BTC transaction volume exceeded $3 billion as of March 8, 2026—with over 97% concentrated across six chains: Base (43%), Ethereum (13%), Arbitrum (12%), BNB and HyperCore (10% each), Solana (9%). Base has emerged as the dominant network for on-chain spot BTC trading.

4. BitMine increased its ETH holdings by 60,999 tokens last week, bringing its total to 4.596 million ETH.

5. Japanese Bitcoin treasury firm MetaPlanet announced revisions to its Capital Allocation Policy—maintaining its long-term BTC hold strategy while enhancing flexibility in fundraising and share buybacks. It currently holds ~35,100 BTC and will pursue diversified financing via perpetual preferred shares, common stock issuance, corporate bonds, and BTC-collateralized credit lines.

6. Trader Eugene turned bullish yesterday in a post on his personal channel, highlighting crypto’s resilience amid declining global risk—its first relative strength since the drop from $60,000. While he didn’t bottom-pick, he prefers entering on breakouts from consolidation ranges to manage risk. Several altcoins are forming natural rounding-bottom patterns, suggesting elevated odds of near-term upward movement. He expects a decisive breakout above $74,000 to trigger broad-based crypto gains—with ETH and SOL recovering prior ranges to ~$2,400 and ~$100 respectively. BTC has now cleared $75,000.

7. The U.S. Securities and Exchange Commission (SEC) proposed amendments to Rule 15c2-11 under the Exchange Act, clarifying that the rule applies solely to equity securities—excluding cryptocurrencies and other non-equity assets from its scope.

V. Today’s Market Calendar

Data Release Schedule

| 10:00 | U.S. | Pending Home Sales Index (MoM) | ⭐⭐⭐ |

| 10:00 | U.S. | Pending Home Sales Index (YoY) | ⭐⭐⭐ |

Key Event Preview

March 17 (Tuesday)

- NVIDIA’s GTC Conference continues—markets await Jensen Huang’s keynote.

March 18 (Wednesday)

- U.S. February PPI data release;

- Micron reports latest quarterly results—market eyes memory chip cycle signals as a semiconductor bellwether.

March 19 (Thursday)

- Fed announces interest rate decision—expected to hold rates steady;

- Dot plot may signal just one rate cut in 2026—significantly narrowing from prior market expectations;

- lululemon reports latest quarterly results.

March 20 (Friday)

- FedEx reports latest quarterly results.

*This week’s core U.S. equity themes revolve around the Fed’s rate decision, economic data releases, Micron’s earnings, and NVIDIA’s GTC Conference—expect heightened market volatility.

Institutional Views:

Top-tier investment bank analysts widely attribute the U.S. equity rebound to falling oil prices easing inflation fears. Goldman Sachs warns CTA selling pressure remains unexhausted—up to $6.9 billion in equity sales over the coming week may amplify volatility. They recommend allocating to stagflation-resilient assets like commodity stocks. On precious metals, UBS maintains its $6,200/oz gold target, citing geopolitical risk and structural demand—but notes gold could fall to $4,600/oz if oil sustains above $100/bbl and reignites inflation. For crude, ANZ analysts point to diplomatic progress in the Strait of Hormuz supporting oil price pullbacks, though Iranian retaliation risks persist—targeting WTI above $96/bbl. In FX, after a 0.5% USD index correction, JPMorgan expects the FOMC’s rate hold to drive USD strength toward 100.5. Overall, the market leans cautiously optimistic—advising close attention to how the Fed meeting reverberates across global asset classes.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News