Bitget UEX Daily Report | Iran Conflict Drives Up Oil Prices; US Proposes Global AI Chip Controls; Nonfarm Payrolls Data to Be Released

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Iran Conflict Drives Up Oil Prices; US Proposes Global AI Chip Controls; Nonfarm Payrolls Data to Be Released

Geopolitical risks dominate; we recommend diversifying allocations into defensive assets.

Author: Bitget

I. Key Market News

Federal Reserve Updates

Nonfarm Payrolls Due Tonight; Inflation Concerns Mount

- The U.S. February nonfarm payrolls report will be released tonight at 21:30 ET. Markets expect a slowdown in hiring but stable unemployment.

- Initial jobless claims rose slightly last week, yet the four-week moving average declined to 215,750—indicating labor market resilience.

- Amid mounting inflationary pressures, this data could influence the Fed’s rate path, potentially boosting the U.S. dollar and weighing on risk assets.

Global Commodities

Iran Conflict Spillover Sends Oil Prices Soaring

- WTI crude hit its highest level since July 2024; Saudi Arabia sharply raised its Asian crude pricing—the largest increase since August 2022.

- The U.S. is considering releasing strategic petroleum reserves or coordinating international action to mitigate oil price surges’ impact on global supply chains.

- Escalating geopolitical risks may further inflate energy costs, stoke inflation, and dampen economic recovery momentum.

Macroeconomic Policy

U.S. Plans to Extend AI Chip Export Controls Globally

- A draft government proposal would require export licenses for companies like Nvidia and AMD, aiming to maintain control over global AI development.

- Over 20 U.S. states have sued the Trump administration over its proposed 15% global tariff plan, citing executive overreach and economic harm.

- While reinforcing U.S. tech hegemony, such measures risk triggering international trade friction, undermining supply chain stability and market confidence.

II. Market Recap

Commodities & FX Performance

- Spot Gold: -0.06% to $5,078/oz—trading sideways for three consecutive days, supported by geopolitical tensions.

- Spot Silver: -0.34% to $82/oz.

- WTI Crude: -2.91% to $78.69; surged yesterday to $82.16—the highest in recent years. The primary driver remains Iran-related disruptions to Strait of Hormuz supply.

- Brent Crude: -2.35% to $83.40/bbl—similarly driven by geopolitical spillover and supply concerns.

- U.S. Dollar Index (DXY): -0.06% to 98.988.

Cryptocurrency Performance

- BTC: -3.23% to $70,825—short-term pullback but holding above $70,000; increased volatility evident in recent price action.

- ETH: -2.92%, broadly tracking broader market corrections.

- Total Crypto Market Cap: -1.6% to $2.49 trillion.

- Liquidations: $242 million liquidated in the past 24 hours—$160 million long positions, $82 million short positions.

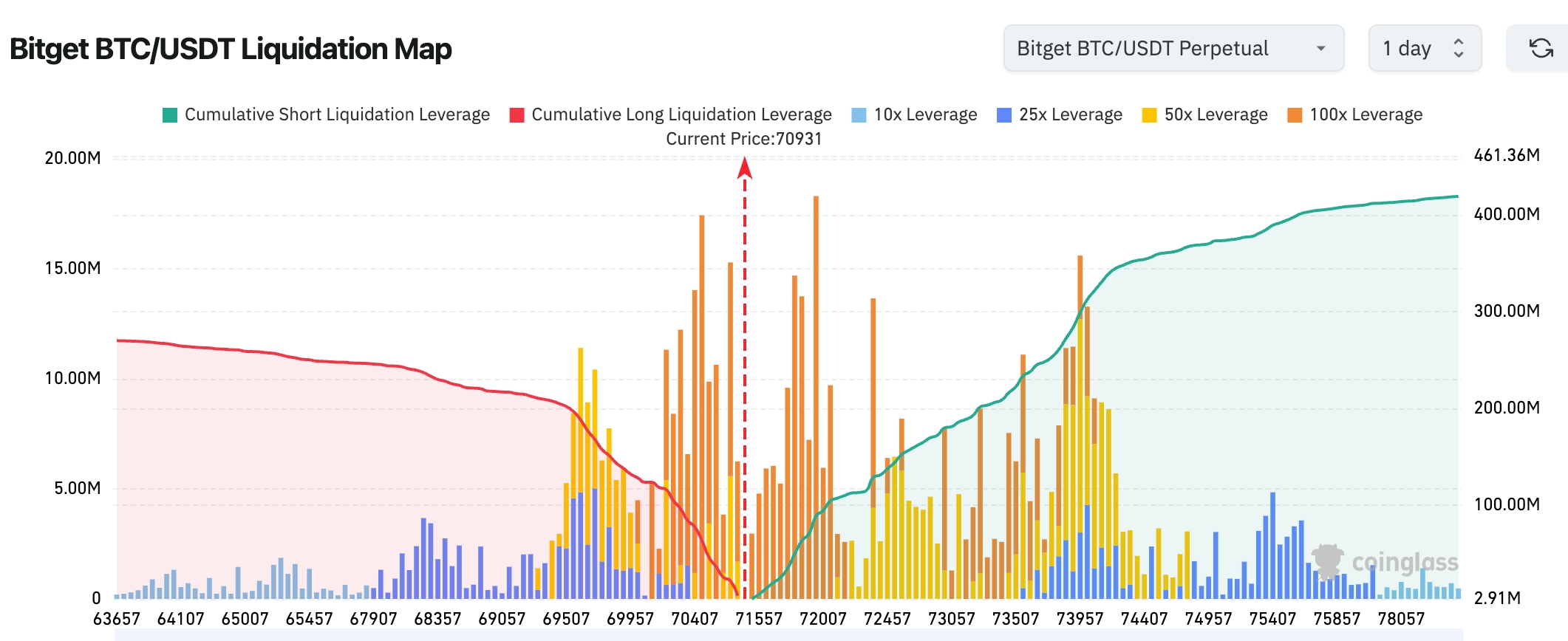

- Bitget BTC/USDT Liquidation Heatmap: Current price ~$70,931. A dense cluster of high-leverage long positions faces liquidation between $69,500–$70,500—if breached, cascading long liquidations may accelerate downside. Conversely, significant short liquidation pressure lies between $73,500–$75,000; a breakout could trigger a sharp short squeeze.

- Spot ETF Net Flows: BTC spot ETFs saw net outflows of $96.6 million yesterday; ETH spot ETFs recorded $8.9 million in net outflows.

- BTC Spot Flows: $3.184 billion inflow vs. $3.586 billion outflow over 24 hours—net outflow of $401 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: -1.61% to 47,954.74—down two days consecutively, dragged by energy stocks.

- S&P 500: -0.57% to 6,830.71—with notable divergence between tech and energy sectors.

- Nasdaq Composite: -0.26% to 22,748.99—AI stocks performed strongly, but overall risk-aversion sentiment dominated.

Tech Giants Update

- Nvidia: +0.16%—benefiting from AI chip demand, though impacted by export control proposals.

- AMD: -1.3%—export licensing requirements add uncertainty.

- Microsoft: +1.2%—AI product launches provided tailwinds.

- Amazon: +0.9%—cloud services growth remained supportive.

- Apple: -0.85%—supply chain concerns weighed on sentiment.

- Google: -0.74%—stable advertising revenue.

- Meta: -1.2%—user growth on social platforms offset by regulatory headwinds. Summary: AI-related stocks gained technical support, but geopolitical tensions and export controls triggered broad-based corrections.

Sector Highlights

Energy Sector: +8%

- Key stock: Chevron (+2.1%).

- Catalyst: Iran conflict-driven oil price surge and supply disruption fears.

Semiconductor Sector: -1.5%

- Key stock: Broadcom (+4.9%).

- Catalyst: Export control draft adds uncertainty despite strong fundamentals.

Tech Application Software Sector: +5%

- Key stock: The Trade Desk (+18%).

- Catalyst: Strong demand for ad-tech and AI integration.

III. In-Depth Stock Analysis

1. Marvell Technology – Q4 Earnings Beat Expectations

Event Summary: Marvell reported Q4 fiscal revenue of $2.219 billion, up 22% YoY—exceeding the midpoint of guidance by $190 million. Adjusted net income totaled $685 million, with diluted EPS of $0.80. CEO stated that FY2027 revenue growth will accelerate sequentially, driven by robust data center business momentum and order growth. Despite AI funding constraints, the company emphasized strong investment in AI cloud infrastructure. Market Interpretation: Analysts view this as evidence of semiconductor demand recovery. KIS analysis notes new inference chips won’t replace HBM/DRAM but rather complement them in niche markets. Investment Takeaway: Shares surged nearly 15% after hours; consider exposure to data center plays—but remain cautious regarding global regulatory risks.

2. Nvidia – Developing New Inference Chip

Event Summary: At its GTC conference, Nvidia will unveil a new inference chip based on Groq’s SRAM architecture—prompting investor concerns about reduced HBM demand. However, analysts clarify SRAM targets ultra-low-latency use cases and serves as a supplement—not a replacement—for existing memory solutions. Nvidia also faces new global export licensing requirements, necessitating applications to the U.S. Department of Commerce. Market Interpretation: KIS highlights market misinterpretation—memory tier segmentation will expand the industry’s total addressable market. Evercore views U.S. controls as positioning America as the “AI gatekeeper,” not as an outright ban. Investment Takeaway: Chip innovation underpins long-term growth; consider buying into regulatory uncertainty.

3. Oracle – Plans Thousands of Layoffs

Event Summary: Oracle plans to cut thousands of jobs to ease funding pressure from AI data center expansion. Layoffs may begin this month across all departments, with cloud hiring frozen. Massive AI cloud investments are expected to push cash flow negative; the company aims to raise $50 billion. Its share price has fallen 54% from its September 2025 peak. Market Interpretation: Bloomberg analysis links heavy AI spending to a broader tech-sector layoff wave—capital scarcity is now a widespread challenge. Investment Takeaway: Near-term pressure remains elevated; monitor fundraising progress to assess rebound potential.

4. Berkshire Hathaway – Resumes Share Buybacks

Event Summary: With $373.3 billion in cash, Berkshire Hathaway resumed buybacks of both Class A and Class B shares this week. Incoming CEO Greg Abel pledged to allocate his entire salary increase toward share purchases annually. The company’s policy permits buybacks when shares trade below intrinsic value. Market Interpretation: Regulatory filings show the prior buyback occurred in Q2 2024; institutions see this as a strong vote of confidence, backed by ample cash reserves. Investment Takeaway: A top-tier long-term value play—consider accumulating at current undervalued levels.

IV. Cryptocurrency Project Updates

- OpenAI launched the GPT-5.4 model, emphasizing factual accuracy and efficiency, supporting a 1-million-token context window for enhanced long-context reasoning.

- Bloomberg ETF analyst Eric Balchunas noted that Bitcoin rose ~12% following Iran’s airstrikes and escalating geopolitical tensions, while gold fell—yet cautioned against concluding gold’s safe-haven status is “broken” or that Bitcoin fully supplants it. Balchunas stressed short-term price moves likely reflect shifts in market-making participation (e.g., Jane Street) and sentiment—not fundamental asset re-rating. Gold’s pullback may stem from profit-taking or capital rotation into Bitcoin; drawing definitive conclusions from short-term behavior is flawed.

- Bitcoin miner CleanSpark released its February operational update: mined 568 BTC and sold 553 BTC—achieving a record 97% sales ratio, generating ~$36.65 million in cash at an average sale price of $66,279. Proceeds fund its expansion into AI and high-performance computing data centers.

- Hyperliquid’s native token HYPE activated its deflationary mechanism, achieving $1 billion daily trading volume; 9.92 million HYPE tokens were unlocked on March 6.

- Dynamic Funds launched the diversified crypto ETF DXMC, offering exposure to BTC, ETH, SOL, and XRP.

- Suspected fallout from Aave governance debates prompted investment firm ParaFi Capital to swap $5 million worth of AAVE for SKY within the past three days.

- Short-selling firm Culper Research announced its short position on Ethereum and ETH-linked securities—including BMNR. It argues the December 2025 Fusaka upgrade damaged ETH’s tokenomics: raising the gas limit to 45–60 million did not yield the anticipated 10–30% gas fee reduction, but instead slashed fees by ~90%. Vitalik and validators’ L1 demand elasticity models were outdated, with errors ranging from 3x to 9x.

- CryptoQuant Head of Research Julio Moreno described Bitcoin’s recent rally as a short-term “relief rally” driven by easing selling pressure—not the onset of a new bull cycle. Though BTC briefly climbed above $73,000, on-chain metrics still indicate bearish conditions, with CryptoQuant’s Bitcoin Bullishness Score remaining at just 10/100.

V. Today’s Market Calendar

Data Release Schedule

| 21:30 | U.S. | Nonfarm Payrolls Report | ⭐⭐⭐⭐⭐ |

| 13:30 | U.S. | Retail Sales | ⭐⭐⭐⭐ |

| 14:30 | U.S. | Average Hourly Earnings | ⭐⭐⭐ |

| 10:00 | U.S. | ISM Manufacturing PMI | ⭐⭐⭐⭐ |

| 08:30 | U.S. | Productivity & Costs | ⭐⭐⭐ |

Key Event Preview

- Friday, March 6, 21:30 ET: February Unemployment Rate and Seasonally Adjusted Nonfarm Payrolls—forecast: +60K jobs (5-star event).

Institutional Views:

Top-tier investment banks hold cautiously optimistic views on yesterday’s market action. Goldman Sachs raised its Q2 Brent crude forecast to $76/bbl, warning sustained Iran conflict beyond five weeks could push prices to $100—triggering demand destruction. Morgan Stanley attributes tech giant divergence to AI regulatory drafts, yet strong data center demand continues to support Nvidia. Precious metals benefit from safe-haven flows, while margin reductions for gold/silver free up liquidity. On FX and oil, Deutsche Bank cautions that AI-related risks may challenge the dollar’s safe-haven status—but expects DXY to remain strong near term. In crypto, Bernstein forecasts BTC reaching $150,000 and total market cap doubling, though warns heightened volatility and liquidation risk in the short term. Overall, geopolitical risk dominates—diversified allocation to defensive assets is advised.

Disclaimer: The above content was compiled via AI search and verified manually for publication only. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News