Bitget UEX Daily Report | Iran’s Negotiation Foundation Undermined; Strait of Hormuz Closed; Intel Surges Due to Involvement in Terafab Project

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Iran’s Negotiation Foundation Undermined; Strait of Hormuz Closed; Intel Surges Due to Involvement in Terafab Project

Overall, the easing of geopolitical tensions has provided the market with some breathing room; however, the two-way risks highlighted in the Federal Reserve’s March meeting minutes serve as a reminder to investors that the macroeconomic policy path remains uncertain. Investors are advised to pay attention to today’s PCE data, which will serve as a key verification of inflation expectations.

I. Key News Highlights

Federal Reserve Updates

Fed’s March Meeting Minutes: Iran Conflict Amplifies Two-Way Economic Risks

- The minutes revealed notable divergence among policymakers over the Iran conflict: prolonged hostilities could impair the labor market and necessitate rate cuts, while simultaneously exerting upward pressure on inflation—potentially prompting hikes. A majority of officials believe restoring inflation to the 2% target will take longer than previously anticipated.

- Some officials supported adopting “two-way language” in the post-meeting statement to describe future interest-rate decisions.

- San Francisco Fed President Mary Daly stated that the U.S. economy remains fundamentally sound, but the impact of the conflict on oil & gas markets—and its broader ripple effects—requires more time to assess; it is too early to draw conclusions. Market impact: Heightened uncertainty regarding the Fed’s policy path; near-term downward pressure on rate-cut expectations, though signs of geopolitical de-escalation may ease overall inflationary pressures.

Global Commodities

Iran Claims Three Provisions Violated in “10-Point Plan”; Strait of Hormuz Closes Again

- Ali Larijani, Speaker of Iran’s Islamic Consultative Assembly, posted on social media accusing the U.S. of violating three key provisions of Iran’s ceasefire “10-Point Plan,” declaring the “negotiation foundation destroyed” and reiterating long-standing distrust toward U.S. commitments.

- On local time April 8, the Strait of Hormuz closed again; the tanker “AUROORA” abruptly reversed course back into the Persian Gulf.

- White House Press Secretary Karoline Leavitt confirmed that the first face-to-face U.S.-Iran talks will be held on April 11 in Islamabad, Pakistan, led by Vice President J.D. Vance. Iran’s revised, streamlined proposal has been accepted as the basis for negotiations and will be aligned with the U.S.’s “15-Point Plan.” Core U.S. red lines remain unchanged—especially the prohibition on uranium enrichment within Iran. Market impact: While geopolitical tensions show signs of easing, volatility persists; short-term sharp oil price corrections, alongside improved sentiment for risk assets.

Macroeconomic Policy

White House Clarifies Ceasefire Details; U.S. Government Considers Adjusting NATO Military Deployments

- Vice President Vance, speaking in Hungary, clarified the U.S. never committed to including Lebanon in any ceasefire agreement; Israel has agreed to exercise restraint to support negotiations.

- According to government officials, the Trump administration is considering withdrawing U.S. military deployments from certain NATO members that have failed to meaningfully assist U.S. actions against Iran—a punitive measure still in early planning stages. Market impact: Highlights the Trump administration’s hardline stance toward allies, potentially reshaping global geopolitical dynamics and energy security expectations.

II. Market Recap

Commodities & FX Performance

- Spot Gold: ~$4,720/oz, down 0.2% over 24 hours; safe-haven buying eased temporarily amid geopolitical de-escalation, yet prices remain elevated.

- Spot Silver: $74.50/oz, down 0.3% over 24 hours; moved in tandem with gold and broader risk sentiment.

- WTI Crude Oil: Up 2.3% to $97/bbl; technical rebound following ceasefire announcement.

- Brent Crude Oil: Up 2.1% to $97/bbl; driven by same factors as WTI.

- U.S. Dollar Index: Down 0.8% to 99.05; improved risk appetite dampened safe-haven demand.

Cryptocurrency Performance

- BTC: Down 1.2% over 24 hours, trading near $70,900; profit-taking intensified after short-term geopolitical risk subsided, shifting price action to consolidation.

- ETH: Down 2.2% over 24 hours, trading near $2,190; underperformed relative to the broader market.

- Total Crypto Market Cap: Down 1.4% over 24 hours, now ~$2.41 trillion, dragged lower by major coins’ pullbacks.

- Liquidations: ~$263 million liquidated over 24 hours, including $160 million in long positions.

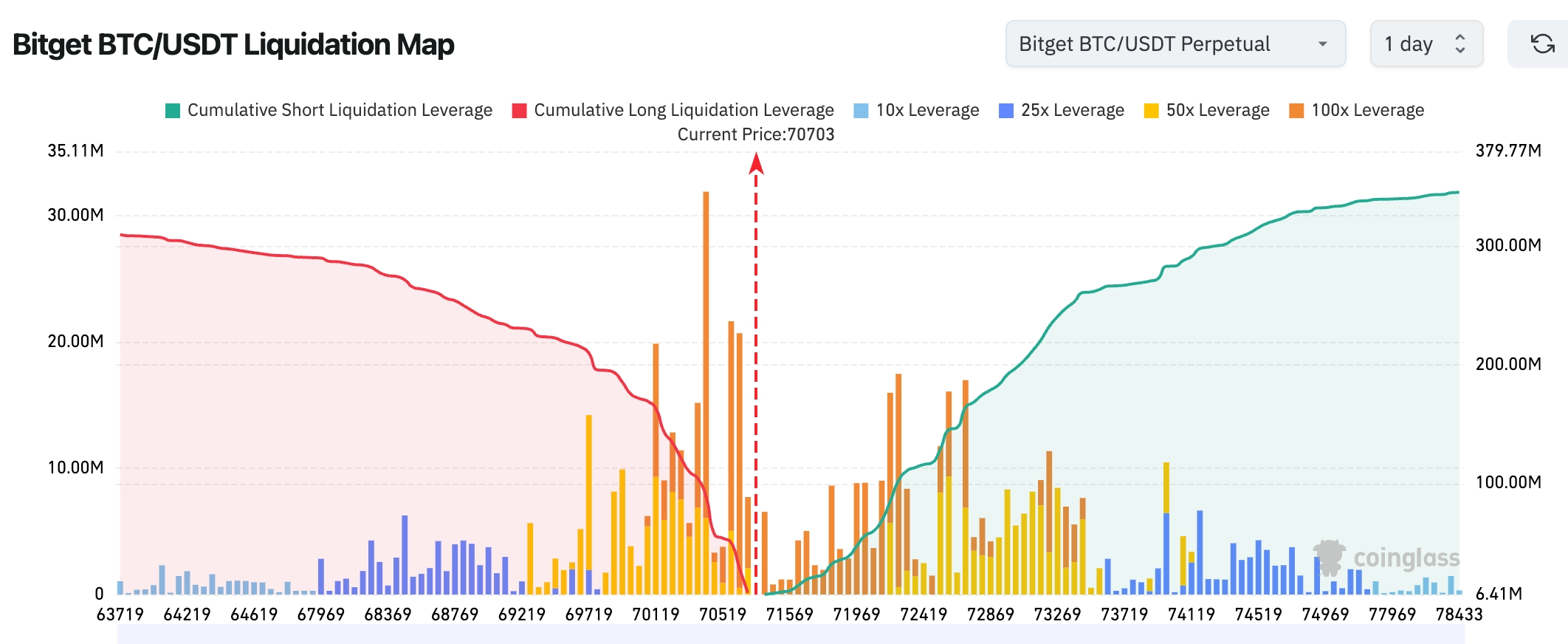

- Bitget BTC/USDT Liquidation Heatmap: Current price (~$70,703) sits at a dense confluence zone between long and short liquidations. A large cluster of long liquidations accumulates below $70,000; a break below could trigger rapid cascading sell-offs. Conversely, the $72,400–$73,300 range above shows significantly thicker short liquidation density; if price breaks above $71,500, the market is more likely to be pulled upward into this zone—triggering a short squeeze.

- Spot ETF Net Flows: BTC spot ETFs saw ~$85 million net outflow yesterday; ETH spot ETFs recorded a modest $9.8 million net outflow.

- BTC Spot Flows: $2.592 billion inflow vs. $2.607 billion outflow yesterday, resulting in a net outflow of $15.32 million.

Summary: Yesterday’s BTC rally was primarily driven by temporary geopolitical de-escalation, with the Strait of Hormuz crypto transit fee announcement serving as an important supplementary catalyst—significantly reinforcing market confidence in BTC’s long-term value proposition. This event underscores Bitcoin’s unique role in high-risk international trade, offering a new dimension for market analysis. Investors should closely monitor progress of the April 11 talks and actual implementation of related payment cases.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +2.85% to 47,909.92—driven higher at open and sustained gains following ceasefire news.

- S&P 500: +2.51% to 6,782.81—marked by six consecutive days of gains.

- Nasdaq Composite: +2.80% to 22,635—led by technology and memory/optical communications sectors.

Tech Giants’ Performance

- Intel (INTC): +11.42% to $58.95—top performer, buoyed by recovering memory chip demand and improving semiconductor supply chain stability outlook.

- NVIDIA (NVDA): +2.23% to $182.08—supported by robust long-term AI compute demand.

- Google (GOOG): +3.56% to $317.32—AI-powered search and application developments progressing well.

- Apple (AAPL): +2.13% to $258.90—seasonal recovery in consumer electronics demand.

- Amazon (AMZN): +3.50% to $221.25—positive growth outlook for cloud business.

- Broadcom (AVGO): +4.99% to $350.63—strong demand for AI-custom chips.

- Meta (META): +6.50% to $612.42—continued momentum in advertising recovery.

- Tesla (TSLA): -0.98% to $343.25—minor pullback amid broad-based improvement in risk sentiment.

Core Summary: Temporary geopolitical de-escalation lifted risk assets broadly; memory/optical communications stocks surged across the board, forming the primary leadership theme. Intel, as a critical supplier, stood out most prominently—aligning with rising AI supply-chain demand.

Sector Movement Observations

Energy Sector: Down ~4–10%

- Representative Stocks: Chevron (CVX) -4.4%, Exxon Mobil (XOM) -4.7%, APA Corp. (APA) -10%.

- Driver: Sharp oil price decline triggered broad energy stock selloff.

Memory/Optical Communications Sector: Broad-based surge

- Representative Stocks: Semiconductor and communications-related equities led gains.

- Driver: Improved market expectations for supply chain stability.

III. In-Depth Stock Analysis

1. Intel (INTC) – Tech Sector Leader

Event Overview: Intel shares rose 11.42% Wednesday to $58.95, leading Nasdaq tech stocks—the highest single-day volume increase in over 40% versus prior day. Key catalysts include a marked rebound in memory chip demand and strong market optimism around Intel’s AI packaging initiative (“Terafab”), developed in deep collaboration with Elon Musk’s xAI to deliver high-density advanced packaging solutions for next-gen AI training clusters. Temporary geopolitical de-escalation (U.S.-Iran ceasefire agreement) further bolstered semiconductor supply chain stability expectations—Intel, as a globally critical supplier, benefited directly. Broader tech strength amplified the effect; Intel’s memory business revenue has risen sequentially for three consecutive quarters, and AI-related orders now account for nearly 25% of total orders. Market Interpretation: Goldman Sachs and Morgan Stanley analysts jointly upgraded their ratings, noting that with geopolitical risks easing, global semiconductor supply chain disruption risks have fallen sharply—Intel’s capacity ramp-up in HBM and advanced packaging is poised for accelerated order fulfillment. Analysts estimate that if AI capital expenditures remain elevated, Intel’s FY2026 EPS could be revised upward by 15–20%. Investment Implications: Near-term, monitor oil price declines’ positive pass-through to inflation and the Fed’s policy flexibility; mid-to-long term, track AI server capex trends and Intel’s production ramp closely. Recommended phased entry in the $55–$60 range.

2. Meta Platforms (META) – Social Media Leader Strengthens

Event Overview: Meta shares rose 6.5% to $612.42, extending its six-session winning streak—cumulative gain now exceeds 18%. Advertising recovery remains robust: Q1 ARPU (average revenue per user) rose 8.2% quarter-on-quarter, driven by AI-enhanced precision targeting algorithms and improved monetization of Reels short-form video. Geopolitical easing boosted global consumer and enterprise ad spending confidence, while Meta Reality Labs’ VR/AR hardware shipments exceeded expectations. Open-sourced Llama-series AI content-generation tools expanded ecosystem influence, resonating strongly with Nasdaq tech-weighted peers. Market Interpretation: J.P. Morgan and Bernstein analysts highlight that improved risk appetite combined with macro-level disinflation expectations will drive overall digital ad market expansion. Meta’s valuation still offers room for re-rating—its current forward P/S ratio stands at just 7.8x, 15% below historical average. With dual engines—advertising and AI—2026 revenue growth is expected to sustain double-digit pace. Investment Implications: Geopolitical easing supports consumption and ad spend. Investors should focus on AI product commercialization updates in Q2 earnings guidance. The $330–$650 range represents an attractive entry window.

3. Anthropic – New Breakthrough in AI Management Agents (Core AI Ecosystem Event)

Event Overview: Anthropic officially launched Claude Management Agents—a new product suite comprising composable APIs and managed environments—elevating AI from a conversational tool to a continuously operating productivity system. Deployment speed increased over 10x, supporting multi-step complex decision-making, real-time auto-correction, and cross-system integration. The product integrates natively with Google Cloud and AWS infrastructure; over 150 enterprise clients have completed internal testing—marking a pivotal transition point from “generative tool” to “enterprise-grade autonomous agent.” This breakthrough synergizes with geopolitical de-escalation-driven supply chain stability, further boosting demand across AI hardware and cloud services. Market Interpretation: Former OpenAI executives-turned-analysts view this as a milestone in AI’s evolution from “tool” to “productivity system,” with long-term implications for corporate IT spending structure. Goldman Sachs forecasts the global AI agent market will expand from $15 billion today to $120 billion by 2026–2027—Anthropic, as a pioneer, will significantly lift upstream chipmakers and cloud providers’ earnings. Investment Implications: Monitor AI infrastructure-related listed companies (e.g., Intel, Broadcom); accelerating technological iteration will boost industry-wide capex. Treat this event as a key signal for AI-themed portfolio allocation.

4. Micron Technology (MU) – Memory Chip Demand Surge

Event Overview: Micron shares rallied alongside the broader memory sector, fueled by surging AI data center demand for high-bandwidth memory (HBM) and DRAM. The company has sold out its entire 2026 HBM production capacity; spot memory chip prices are up 28% since year-start, reflecting persistent AI memory shortages. Geopolitical de-escalation eased supply bottlenecks—Micron, as the world’s second-largest DRAM supplier, benefits directly from order acceleration from downstream AI server makers like Intel and NVIDIA. Recent earnings showed data center business revenue now accounts for 58% of total, growing 112% YoY. Market Interpretation: Citigroup and UBS joint report emphasizes AI-driven memory supply-demand imbalance will persist through H2 2027; Micron’s gross margin is expected to rise from current 42% to over 55%. Analysts widely maintain “Buy” ratings, with price targets ranging $110–$130. Investment Implications: Maintain long-term conviction in structural AI server memory shortages; hold through periods of elevated HBM pricing. Monitor quarterly capacity utilization metrics as a forward-looking indicator.

5. Broadcom (AVGO) – AI Custom Chip Orders Materialize

Event Overview: Broadcom announced expanded long-term partnerships with Google and Anthropic—to supply next-generation Tensor Processing Unit (TPU) custom chips for Google and multi-gigawatt-scale AI compute capacity for Anthropic. Total contract value is projected to exceed $4.5 billion, representing Broadcom’s largest-ever custom semiconductor agreement. Enhanced supply chain stability amid geopolitical easing further secures chip delivery timelines; AI-related revenue now comprises 41% of Broadcom’s total—up 65% YoY. Market Interpretation: Jefferies and Barclays analysts note this significantly improves visibility into Broadcom’s AI revenue stream, cementing its absolute leadership position in custom ASIC chips. FY2026 AI revenue guidance is expected to rise 18–22%, driving overall valuation re-rating. Investment Implications: AI infrastructure capex remains robust; Broadcom’s long-term growth trajectory is clear. Prioritize allocation during AI-themed sector rotation—monitor follow-on partnership execution timing with cloud giants.

IV. Cryptocurrency Project Updates

1. Bernstein: Quantum threat to Bitcoin is real but manageable; the industry has a three- to five-year window to upgrade for quantum resistance. Michael Saylor, Founder & Executive Chairman of Strategy, contends the risk is overstated—it remains theoretical and may not require addressing for decades, by which time solutions will exist.

2. Michael Saylor, Founder & Executive Chairman of Strategy, speaking at a Mizuho event, stated Bitcoin likely bottomed near $60,000 in early February—driven more by seller exhaustion than valuation metrics. He believes current selling pressure is limited, daily supply is being absorbed by ETF inflows, and corporate treasury allocations to Bitcoin continue generating steady demand. Saylor predicts the next bull market catalyst will be the emergence of banking and digital credit systems built atop Bitcoin—transforming it from a non-yielding asset into a capital markets engine.

3. Morgan Stanley’s spot Bitcoin ETF (MSBT) recorded ~$34 million in inflows on its April 8 debut, with over 1.6 million shares traded.

4. On-chain analyst Yujin reported that the Ethereum Foundation has sold 3,750 ETH ($8.3 million) of its planned 5,000 ETH sale; average sale price was $2,214.

5. Chainalysis released a report forecasting stablecoin transaction volume could reach up to $150 trillion by 2035. Even under baseline growth assumptions, adjusted stablecoin transaction volume would hit $71.9 trillion by 2035; incorporating macro catalysts such as demographic shifts and merchant adoption would push the ceiling much higher. The report notes stablecoins processed ~$28 trillion in “real-world economic activity” in 2025—excluding noise, counting only payments, remittances, and settlements. Two key drivers: (i) An estimated $100 trillion in wealth transfer from older generations to digitally native Millennials and Gen Z between 2028–2048; (ii) Deeper stablecoin integration into merchant checkout and back-end payment systems—making underlying crypto technology imperceptible to end users. Chainalysis projects stablecoin payment volumes will match Visa and Mastercard levels between 2031–2039.

6. The Block reported that Canary Capital filed an S-1 registration statement with the U.S. Securities and Exchange Commission (SEC) on Wednesday to launch an ETF tracking the spot price of PEPE tokens. Canary noted PEPE launched in April 2023 with a total supply exceeding 420 trillion tokens and emphasized the meme coin lacks utility. Last year, Canary also filed similar ETF applications tracking MOG and Pengu token prices.

V. Today’s Market Calendar

Data Release Schedule

| 8:30 | U.S. | Personal Income (Feb) | ⭐⭐⭐ |

| 8:30 | U.S. | PCE Price Index (Feb) | ⭐⭐⭐⭐ |

| 8:30 | U.S. | GDP (Q4 Final) | ⭐⭐⭐⭐ |

| 8:30 | U.S. | Initial Jobless Claims (Week ending Apr 4) | ⭐⭐⭐ |

Key Event Preview

April 9 (Thursday)

- U.S. February core PCE Price Index, Q4 final real GDP (quarterly SAAR), and initial jobless claims for week ending April 4.

April 10 (Friday)

- U.S. March CPI YoY & MoM ★★★★★; University of Michigan Consumer Sentiment Index (preliminary) + 1-Year Inflation Expectations (preliminary).

Institutional Views:

Top-tier investment banks broadly attribute the strong April 8 rallies in U.S. equities and crypto assets to improved risk appetite following the U.S.-Iran two-week ceasefire agreement. Sharply falling oil prices further eased inflation concerns—preserving the Fed’s policy flexibility. Morgan Stanley and others note markets will pivot to outcomes of the April 11 Islamabad talks; substantive progress could extend upside for risk assets. Yet Iran’s parliamentary statements indicate unresolved rifts, and the Strait of Hormuz’s recurring closures remain a source of uncertainty—investors are advised to maintain disciplined position sizing. Goldman Sachs analysts emphasize the dollar’s weakness and gold/silver rebounds reflect a temporary release of safe-haven sentiment, while crypto’s total market cap surpassed $2.5 trillion and ETF inflows remain sustained—highlighting robust institutional allocation demand. Overall, geopolitical easing provides breathing room, but the Fed’s March minutes underscore persistent two-way risks—reminding investors that macro-policy paths remain fluid. Focus today on PCE data to validate inflation expectations.

Disclaimer: The above content was compiled via AI search and verified manually for publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News