Bitget UEX Daily Report | Iran Denies Negotiations to Return Oil Prices to $100; Nasdaq-100 Index Introduces New Rules—SpaceX Likely to Be Included

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Iran Denies Negotiations to Return Oil Prices to $100; Nasdaq-100 Index Introduces New Rules—SpaceX Likely to Be Included

Overall, geopolitical uncertainty remains the dominant variable; investors are advised to monitor subsequent statements by Federal Reserve officials and the latest developments in the Middle East.

Author: Bitget

I. Top News Highlights

Federal Reserve Updates

Chair Powell: Likely to Hold Rates Amid Energy Shock Federal Reserve Chair Jerome Powell stated on Monday that the Fed could temporarily disregard the impact of rising energy prices triggered by U.S.-Israeli military action against Iran, and is inclined to hold interest rates steady for now. However, he cautioned that if inflationary pressures begin shifting long-term public inflation expectations, the Fed may act accordingly. New York Fed President John Williams added that the current monetary policy stance effectively balances risks to employment and price stability. Governor Michelle Bowman noted she will remain in her role until a new Fed Chair is confirmed and supports approximately a 100-basis-point rate cut this year. Powell’s remarks swiftly eased market concerns about forced policy tightening, boosting trader bets on a small chance of a rate cut this year; short-term U.S. Treasury yields fell more than 10 basis points. Overall, his comments injected some certainty into markets and helped stabilize investor expectations regarding the path of monetary policy.

Global Commodities

U.S. Crude Oil Re-Enters $100/Barrel Era Amid Escalating Iran Conflict Since the U.S.-Israeli military campaign against Iran began, U.S. WTI crude oil futures surged over 3% on Monday to close at $105 per barrel—the highest since July 2022—and continued climbing on Tuesday; Brent crude followed suit. The IMF warned the conflict could trigger a “global but asymmetric” shock—pushing up prices and weighing on economic growth, especially in oil-import-dependent countries. Soaring oil prices directly reflect heightened tensions in the Strait of Hormuz, compounded by former President Trump’s threats to strike additional energy infrastructure—short-term supply concerns are now dominating markets. Investors should monitor the duration of the conflict: a near-term agreement could prompt oil price corrections.

Macroeconomic Policy

White House Says Trump Aims to Reach Iran Deal by April 6; Iran Denies Direct Talks White House Press Secretary Karoline Leavitt stated that the U.S. military operation against Iran is proceeding as planned and expected to last four to six weeks. She revealed Trump hopes to reach an agreement before April 6—the previously extended deadline for striking energy facilities. Iran has agreed to allow 20 tankers to pass through the Strait of Hormuz, with another 20 expected shortly. Iranian Foreign Ministry Spokesperson Nasser Kanaani firmly stated that no negotiations have taken place with the U.S. in the 31 days since hostilities began—only proposals have been received via intermediaries like Pakistan. Iran’s parliament approved a bill imposing transit fees on vessels passing through the Strait of Hormuz and banning U.S. and Israeli ships from passage. Iran’s First Vice President warned that any U.S. military assault on Kharg Island would result in “no return.” Geopolitical uncertainty and oil prices are increasingly correlated; the IMF expects supply chain disruptions to push up food and fertilizer prices, raising global inflation risks in the short term—longer-term outcomes depend on how the conflict evolves.

II. Market Recap

Commodities & FX Performance

- Spot Gold: Up 0.37% to ~$4,527/oz, consolidating for two consecutive days—supported by geopolitical risk aversion but capped by stronger oil prices and a modestly firmer dollar.

- Spot Silver: Down 0.05% to ~$70/oz, exhibiting higher volatility amid mixed industrial demand and safe-haven appeal.

- WTI Crude Oil: Up over 3.4% to $106/barrel, driven by supply disruption fears stemming from the Iran conflict.

- Brent Crude Oil: Up ~2.37% to $109/barrel, reflecting significant geopolitical risk premium.

- U.S. Dollar Index: Up 0.02% to ~100.51, supported by safe-haven flows and oil-driven strength.

Cryptocurrency Performance

- BTC: +0.92% over 24H at $66,945—continuing consolidation, weighed down by oil-driven inflation concerns and U.S. equity pullbacks.

- ETH: +1.75% over 24H at ~$2,033.

- Total Crypto Market Cap: +0.4% over 24H to ~$2.38 trillion.

- Liquidations: ~$216 million liquidated in 24H—~$111 million longs, ~$105 million shorts.

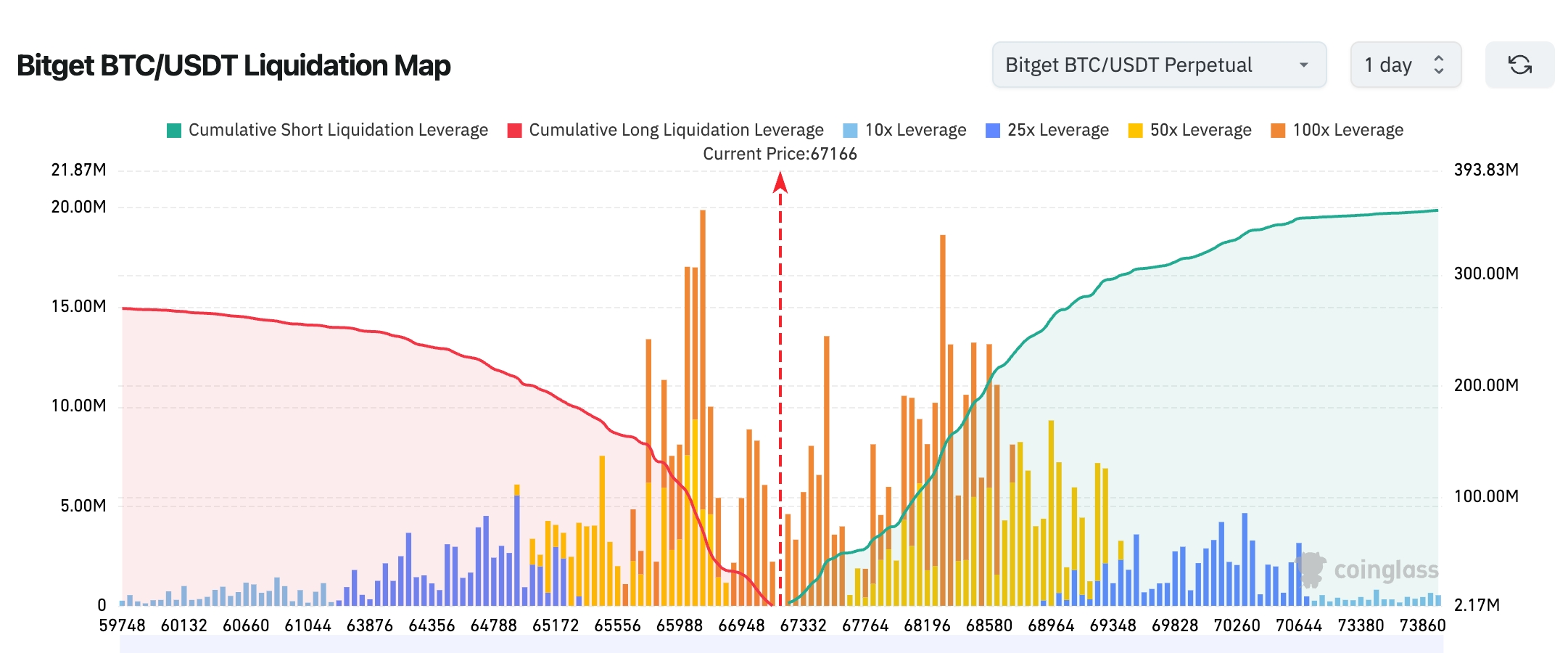

- Bitget BTC/USDT Liquidation Map: Current price ~$67,166. Dense short liquidation zone visible between $66,800–$67,000; heavy concentration of 50x–100x leveraged long positions above $68,000–$69,000—any breakout could trigger cascading long liquidations. Structure leans toward “stronger resistance above, sturdier support below”; near-term likely range-bound with repeated tests of $67,000 support. A decisive, volume-backed break above $68,000 would signal true directional momentum.

- Spot ETF Net Flows: BTC spot ETFs saw ~$61.9M net inflow yesterday; ETH spot ETFs saw ~$10.6M net inflow.

- BTC Spot Flows: ~$2.334B inflow vs. ~$2.274B outflow yesterday—net inflow ~$60M.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +0.11% to 45,216—continuing modest rebound.

- S&P 500: -0.39% to 6,343—energy sector gains insufficient to offset tech-sector weakness.

- Nasdaq Composite: -0.73% to 20,794—tech stocks led declines, though overall drop narrowed.

Tech Giants Update

- Apple (AAPL): -0.87% ($246.63), dragged down by broader tech selloff.

- Microsoft (MSFT): +0.61% ($358.96), underpinned by AI business resilience.

- Google (GOOGL): -0.31% ($273.50), stable search and cloud performance.

- Amazon (AMZN): +0.81% ($200.95), solid e-commerce and cloud services results.

- NVIDIA (NVDA): -1.40% ($165.17), chip-cycle concerns resurfacing.

- Meta (META): +2.03% ($536.38), advertising strength drove outperformance.

- Tesla (TSLA): -1.81% ($355.28), pressured by vehicle delivery data. Overall, Meta and Amazon rose against the trend—driven by earnings resilience and defensive characteristics—while others were weighed down by high oil prices and geopolitical risk.

Sector Rotation Insights

Energy Sector: +~2.5%

- Key Stocks: ExxonMobil (XOM) +3.2%, Chevron (CVX) +2.8%.

- Catalyst: Iran conflict pushed oil prices higher; supply disruption fears made energy the top避险 choice.

Semiconductor Sector: -~1.2%

- Key Stocks: NVIDIA (NVDA) -1.4%, AMD -1.8%.

- Catalyst: Oil-driven inflation concerns raised fears of Fed tightening, pressuring growth-stock valuations.

III. In-Depth Stock Analysis

1. Tesla (TSLA) – TERAFAB Superchip Factory Initiative

Event Summary: Tesla is accelerating its TERAFAB superchip factory project—a $20–25 billion global initiative to build large-scale semiconductor manufacturing facilities in partnership with SpaceX and xAI. The project aims to deliver up to 1 terawatt (TW) of computing power annually, primarily supporting humanoid robot training, autonomous driving system optimization, and broader AI infrastructure development. This marks a pivotal step in Tesla’s strategic pivot from traditional automotive manufacturing to a vertically integrated AI ecosystem. Against the backdrop of escalating geopolitical tensions and rising energy costs, the move strengthens Tesla’s internal compute self-sufficiency while directly addressing long-standing global AI chip supply-demand imbalances. Upon completion, TERAFAB will further consolidate Tesla’s hardware-software-data loop advantages, establishing a unique competitive moat. Market Interpretation: Multiple Wall Street firms broadly view the project as a major catalyst for Tesla’s long-term competitiveness in AI hardware. Goldman Sachs analysts note it could drive a re-rating from auto-centric valuation toward higher-margin AI services—but caution investors to closely track capital expenditure pacing and supply chain stability to avoid near-term cash flow pressure. Investment Takeaway: Near-term progress updates may fuel tactical rallies; medium- to long-term investors should prioritize monitoring production ramp timelines, humanoid robot delivery milestones, and synergy realization with partners—to capture core opportunities in the AI hardware space.

2. Apple (AAPL) – Major Redesign for Foldable iPhone

Event Summary: Apple’s next-generation foldable iPhone will undergo its most extensive design overhaul to date—including abandoning Face ID in favor of side-mounted Touch ID fingerprint recognition, comprehensive mitigation of screen creasing, and significantly enhanced durability and ergonomics. The device is slated for launch in late 2026. This redesign reflects Apple’s deep analysis of early-market feedback on foldables, aiming to resolve persistent user pain points and stimulate upgrade demand among existing iPhone users. Amid slowing global smartphone growth, this innovation represents a critical lever for Apple to reignite premium consumer electronics revenue growth—and further cement its leadership in high-end foldable technology. Market Interpretation: Analysts widely expect this design shift to meaningfully lift iPhone sales trajectories. Morgan Stanley and others have upgraded Apple’s medium- to long-term revenue and profit forecasts—though they emphasize monitoring supply-chain adjustments and associated short-term cost pressures, particularly amid elevated energy prices that may amplify raw material and logistics cost volatility. Investment Takeaway: The opening of this innovation cycle may catalyze Apple’s valuation recovery. Investors should proactively position in key supply-chain partners and continuously track product pre-launch signals and partner capacity dynamics to capture potential upgrade-cycle upside.

3. Meta (META) – Testing Instagram Premium Subscription Service

Event Summary: Meta Platforms has launched internal testing of an Instagram Premium subscription service—offering subscribers exclusive content access, drastically reduced ads, and personalized AI tools—across select key markets. This marks Meta’s latest effort to diversify beyond its ad-dominated revenue model, aiming to de-risk income streams and boost user engagement and average revenue per user (ARPU). As AI accelerates content creation and recommendation capabilities, this move not only enhances platform health but also injects fresh growth momentum into Meta’s social and entertainment businesses—complementing its existing ad and e-commerce operations. Market Interpretation: Analysts suggest this subscription model will meaningfully diversify Meta’s revenue mix, reducing reliance on advertising alone. Coupled with deeper AI integration, Meta’s long-term growth trajectory appears clearer and more resilient. Still, analysts urge close attention to subscriber conversion rates and pricing strategy effectiveness to ensure scalable monetization. Investment Takeaway: Scaling subscription revenue stands to significantly strengthen Meta’s earnings resilience. Investors should consistently monitor test metrics, user conversion indicators, and ARPU trends as key barometers of platform monetization efficiency.

4. SpaceX & Other Unicorns – Impact of Nasdaq Index Rule Changes

Event Summary: Nasdaq officially announced revisions to its “Fast Entry” index methodology, effective May 1, 2026. Under the new rules, newly listed companies become eligible for evaluation on their seventh trading day—if they meet the Nasdaq-100 market-cap threshold, they can be rapidly added to the index. This change directly benefits high-valuation unicorns like SpaceX and OpenAI, signaling Nasdaq’s commitment to enhancing index liquidity and inclusivity—and attracting more innovative, high-growth enterprises to boost overall market vitality. Amid intensifying geopolitical risks and energy-price volatility, the update offers private and early-stage investors more efficient exit and valuation realization pathways—and accelerates the capital-market journey for high-quality tech assets. Market Interpretation: Multiple investment banks believe this rule refinement will substantially improve secondary-market liquidity and valuation premiums for top-tier tech firms—bolstering the broader innovation financing ecosystem long term. Analysts also highlight market-cap thresholds as the primary selection filter, forecasting rapid surges in funding attention across related value chains—though short-term index rebalancing may introduce valuation recalibration risks. Investment Takeaway: Related value chains stand to attract incremental capital inflows. Investors should closely track index constituent changes and listing timelines for SpaceX and other unicorns—seizing tactical opportunities around rule implementation timing.

IV. Cryptocurrency Project Updates

1. Bloomberg ETF analyst Eric Balchunas disclosed on X that LeverageShares has filed applications for three Bitcoin volatility-linked ETFs: the Leverage Shares Bitcoin Volatility Daily Long ETF, the Leverage Shares 2x Bitcoin Volatility Daily Long ETF, and the Leverage Shares -1x Bitcoin Volatility Daily Short ETF. These products mirror XIV and TVIX—but track Bitcoin instead.

2. Jack Dorsey’s Square has begun automatically enabling Bitcoin payments for millions of U.S. merchants. Transactions convert instantly to USD at checkout; merchants receive payments without extra setup—and bear no price-volatility or custody risk. The feature includes near-instant settlement and waives processing fees through 2026.

3. Strategy disclosed in its latest regulatory filing that it purchased no new Bitcoin during the week ended March 29, 2026, maintaining its holdings at 762,099 BTC—valued at over $51.5 billion at prevailing market prices.

Bitmine Immersion Technologies (BMNR) reported purchasing 71,179 ETH last week, bringing its total ETH holdings to 4,732,082—approximately 3.92% of total ETH supply.

4. U.S. Republican Senators Cynthia Lummis and Bill Cassidy introduced the “American Mining Act,” designed to expand cryptocurrency mining’s role in the U.S. economy—and codify President Trump’s executive order establishing a Strategic Bitcoin Reserve into law. The bill directs the Department of Commerce to establish a voluntary certification program for mining pools and facilities, requiring certified operators to phase out mining equipment manufactured by companies affiliated with foreign adversaries.

V. Today’s Market Calendar

Data Release Schedule

| 20:30 | U.S. | Chicago PMI (March) | ⭐⭐⭐ |

| 22:00 | U.S. | Consumer Confidence Index (March) | ⭐⭐⭐⭐ |

Key Event Previews

- Event: Progress on Indirect U.S.-Iran Negotiations—Watch for deal confirmation before April 6, impacting oil prices and global risk sentiment.

- Event: Nasdaq-100 Index Methodology Revision Observation Period—New rules take effect May 1; monitor likelihood of SpaceX and other unicorns entering the index.

- April 1 (Wed), April 2 (Thu), April 3 (Fri): This week’s U.S. equity focus centers on Fed speeches, nonfarm payrolls, ADP employment data, and Tesla delivery reports—converging labor-market signals and policy cues are expected to heighten market volatility.

- U.S. March unemployment rate and seasonally adjusted nonfarm payrolls released at 20:30; S&P Global U.S. Services PMI final reading (March) at 21:45.

- U.S. equities closed for Good Friday.

- Dallas Fed President Lorie Logan (2026 FOMC voter) speaks at 23:00.

- U.S. initial jobless claims (week ending March 28) released at 20:30.

- EV manufacturers—including Tesla—report Q1 delivery figures; Tesla has lowered its 2026 full-year delivery forecast to 1.689 million units.

- St. Louis Fed President Alberto Musalem (2028 FOMC voter) speaks on the U.S. economy and monetary policy at 21:05 (UTC+8).

- U.S. ADP employment change (March) at 20:15; U.S. retail sales MoM (February) at 20:30; S&P Global U.S. Manufacturing PMI final (March) at 21:45; ISM Manufacturing PMI (March) at 22:00.

Institutional Views:

Goldman Sachs and JPMorgan analysts concur that the Iran conflict will continue pushing oil prices into the $100–$110/barrel range in the near term, potentially forcing the Fed to maintain a “higher for longer” policy stance in 2026. Yet Powell’s “temporary disregard” comment provides a buffer—U.S. equities are expected to trade sideways in the short term, with tech valuations under pressure and energy stocks supported. On crypto, Morgan Stanley notes sustained BTC ETF inflows coupled with leveraged liquidation releases have laid groundwork for a potential rebound; if geopolitical risk recedes, BTC could reclaim $70,000. Conversely, persistently high oil prices will continue weighing on risk assets. Overall, geopolitical uncertainty remains the dominant variable—investors should closely follow subsequent Fed official commentary and developments in the Middle East. Disclaimer: The above content was compiled via AI search and verified manually prior to publication—not intended as investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News