Bitget UEX Daily Report | U.S.-Iran Talks Near Agreement; Robinhood Plans $1.5 Billion Share Buyback; Pinduoduo to Release Earnings Today

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | U.S.-Iran Talks Near Agreement; Robinhood Plans $1.5 Billion Share Buyback; Pinduoduo to Release Earnings Today

Overall, in the short term, energy easing and AI represent two prominent investment themes amid market volatility; in the medium to long term, opportunities along related industrial chains are promising.

Author: Bitget

I. Key Market Highlights

Federal Reserve Updates

No major new developments; markets focus on how geopolitical signals may influence policy trajectory

- The Federal Reserve maintains its prior interest rate stance; markets are closely monitoring progress in Middle East negotiations and their potential impact on inflation expectations.

- This follows emerging signs of de-escalation in the Middle East, where energy price volatility could shift rate-cut expectations.

- Market impact: Substantial progress in negotiations may ease energy cost pressures, granting the Fed greater flexibility—providing short-term support for risk asset pricing.

International Commodities

U.S.-Iran talks signal ceasefire; Thai oil tanker safely transits Strait of Hormuz

- Trump stated U.S.-Iran negotiations “may be quite close to reaching an agreement,” with the U.S. proposing a 15-point ceasefire plan—including a one-month truce—and Iran agreeing not to develop nuclear weapons.

- Thailand’s foreign minister confirmed that, following coordination among Iran, Thailand, and Oman, a Thai oil tanker has safely passed through the Strait of Hormuz and is expected to arrive in Thailand in early April—a positive signal.

- Market impact: Risk of energy supply disruption has significantly declined, pressuring oil prices in the short term; however, long-term geopolitical logic remains intact, supporting global supply chain stability.

Macroeconomic Policy

NASA shifts strategic focus: $20 billion allocated to lunar surface base construction

- NASA’s new administrator, Jared Isaacman, announced cancellation of the lunar orbiting space station plan and instead committed to building a $20 billion lunar surface base over the next seven years using existing components.

- This pivot reflects intensifying global space competition and rising geopolitical rivalry.

- Market impact: Strengthens investor expectations for U.S. space industry investment, benefiting related aerospace and advanced manufacturing supply chains.

II. Market Recap

Commodities & FX Performance

- Spot gold: Up ~2.05%, latest at $4,566/oz—strong rebound into the $4,500+ range after consecutive pullbacks; short-term safe-haven demand receded amid easing geopolitical tensions, yet capital inflows, technical rebound, and long-term bull thesis (central bank gold buying, persistent geopolitical uncertainty) jointly drove the late-session rally. Short-term rebound momentum remains strong, and the pullback is viewed as a favorable entry opportunity.

- Spot silver: Up ~3.75%, latest at $74/oz—more volatile than gold; rallied alongside gold due to its dual industrial and precious metal attributes, supported by early signs of recovering industrial demand and improved risk sentiment.

- WTI crude: Down ~5.68%, latest at $87.10/bbl—supply disruption concerns eased markedly following U.S.-Iran ceasefire talks and the Thai oil tanker’s safe passage through the Strait of Hormuz, triggering sharp profit-taking from elevated levels.

- Brent crude: Down ~6.41%, latest at $97.79/bbl—the international benchmark is more sensitive to geopolitical events; energy costs have clearly retreated from highs, though long-term Middle East geopolitical logic continues to provide some underlying support.

- U.S. Dollar Index: Minor fluctuations, latest at 99.18—improved risk sentiment amid easing geopolitical tensions leaves the dollar directionally neutral in the near term, though inflation expectations and Fed policy path continue to offer modest support.

Core driver: Markets rapidly priced in “easing geopolitical risk,” driving sharp declines in energy prices and alleviating earlier stagflation concerns sparked by high oil prices; precious metals saw a late-session rebound after temporarily losing some safe-haven support. Institutions broadly agree the long-term gold bull thesis (central bank gold purchases, enduring geopolitical uncertainty) remains intact, recommending accumulation on dips; crude faces near-term correction pressure, but if negotiations fail to yield a substantive agreement, energy-related narratives will likely resurface. Investors should continue monitoring developments in U.S.-Iran talks, the G7 foreign ministers’ meeting, and upcoming EIA crude inventory data for price guidance.

Cryptocurrency Performance

- BTC: +0.26% over 24H, latest at $70,874—minor rebound after extended consolidation; easing geopolitical tensions boosted risk appetite, while reduced safe-haven demand prompted capital reallocation back into crypto.

- ETH: +0.87% over 24H, latest at $2,162—mild recovery aligned with broader market; leveraged liquidation pressure eased.

- Total crypto market cap: +0.4% over 24H, ~$2.51 trillion—broad-based rebound across risk assets.

- Market liquidations: $234 million total over 24H—$117 million long liquidations; bidirectional liquidation volumes narrowed.

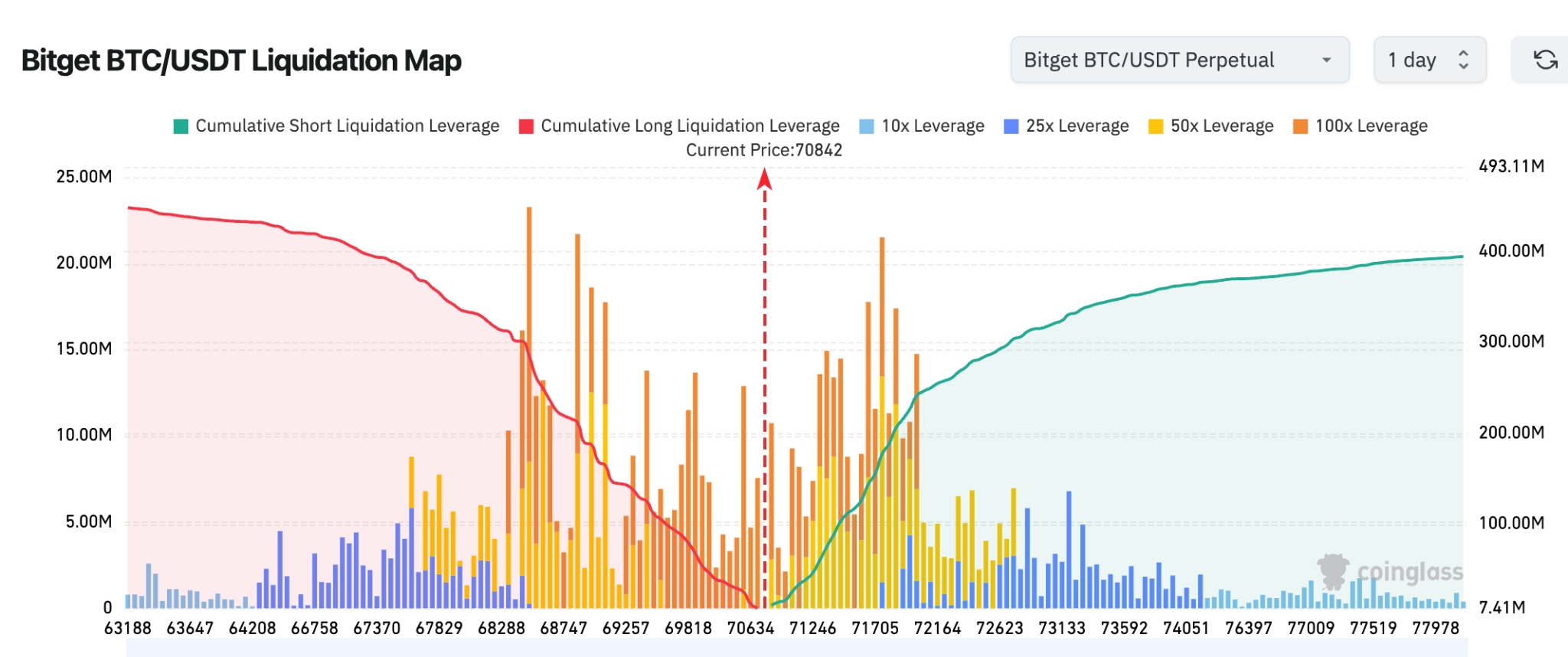

- Bitget BTC/USDT Liquidation Map: Current price ~$70,842. The dense long liquidation zone below has been largely cleared, while a significant cluster of highly leveraged short positions remains concentrated in the $71,000–$73,000 range above—making the price more susceptible to “short squeezes” in the near term. Overall structure shows notably higher liquidation pressure above versus support pressure below; if price remains range-bound, it is more likely to test the liquidity-rich upper zone before breaking down sharply.

- Spot ETF net inflows/outflows: BTC spot ETFs recorded $61.9 million net outflow yesterday; ETH spot ETFs recorded $61.9 million net outflow yesterday.

- BTC spot flows: $2.299 billion inflow vs. $2.472 billion outflow yesterday, net outflow of $174 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: -0.18%, closed at 46,124.06—minor consolidation

- S&P 500: -0.37%, closed at 6,556.37—dragged by software stocks

- Nasdaq Composite: -0.84%, closed at 21,761.89—technology sector diverged

Tech Giants’ Updates

- NVIDIA (NVDA): -0.27%, closed at $175.20—robust AI infrastructure demand provides long-term support

- Apple (AAPL): +0.06%, closed at $251.64—strong defensive characteristics, relatively resilient

- Alphabet (GOOGL): -3.89%, closed at ~$290.44—weighed down by broad risk sentiment and software sector weakness

- Microsoft (MSFT): -2.68%, closed at $372.74—accelerating data center expansion insufficient to fully offset sector-wide selloff

- Amazon (AMZN): -1.38%, closed at $207.24—entry into humanoid robotics offers structural support

- Meta (META): -1.84%, closed at $592.92—major Arm chip order bolsters AI application narrative

- Tesla (TSLA): +0.57%, closed at $383.03—synergistic chip and robotics initiatives underpin relative strength

Core reason: Signals from Middle East negotiations lifted risk appetite, yet profit-taking in software and growth stocks persists, resulting in clear tech sector divergence; optical communications surged on large orders, while software stocks weakened; AI infrastructure and domestic chip production themes continue to deliver structural support.

Sector Rotation Observations

Optical Communications Sector posted notable gains

- Key stocks: AAOI up 18.94%, Lumentum up 10.02%

- Catalyst: AAOI secured an $53 million order for 800G optical modules, reflecting robust data center demand

Extended Tech Software Sector declined significantly

- Key stocks: Salesforce down >6%, ServiceNow down 5.68%

- Catalyst: AWS and Anthropic’s launch of AI agents targeting white-collar roles accelerates office automation

III. In-Depth Stock Analysis

1. Robinhood – $1.5 Billion Share Repurchase Program

Event Summary: Robinhood announced authorization to repurchase up to $1.5 billion of its shares. Its stock has fallen 39% since early 2026, and the company views current valuation as an attractive window for buybacks. Market Interpretation: Strong confidence signaled by management and the board; long-term value creation capability recognized. Investment Insight: Buyback announcements during periods of depressed share prices convey strong signals; watch for execution impact on valuation recovery.

2. Li Auto – $1 Billion Share Repurchase Program

Event Summary: Li Auto’s board approved a share repurchase program authorizing up to $1 billion in repurchases of Class A ordinary shares and/or ADRs between approval date and March 31, 2027. Market Interpretation: Strong confidence in future growth prospects. Investment Insight: Repurchase programs reinforce shareholder returns and support medium-to-long-term valuation stability.

3. Arm Holdings – Launch of First In-House AGI CPU

Event Summary: Arm launched its first in-house AGI CPU, purpose-built for data center agent workloads, featuring up to 136 Neoverse V3 cores; Meta is the inaugural major customer, with OpenAI, Cloudflare, and SAP also planning procurement; Arm projects $25 billion in revenue from this business within five years. Market Interpretation: Accelerated domestic chip production and ecosystem collaboration enhance long-term growth visibility. Investment Insight: Surging AI compute demand opens new growth avenues for Arm’s chip business—monitor order fulfillment closely.

4. Microsoft – Acquires Texas Data Center Site & Launches Nuclear-Powered AI Initiative

Event Summary: Microsoft acquired Oracle’s and OpenAI’s abandoned 700 MW Texas data center project, investing ~$50 billion; simultaneously launched the “AI for Nuclear” initiative with NVIDIA to cut nuclear licensing approval timelines by 92%. Market Interpretation: Dual-track acceleration in compute and energy infrastructure marks a new phase in AI infrastructure expansion. Investment Insight: Synergy between energy and compute resources is increasingly evident—long-term tailwind for Microsoft’s cloud and AI businesses.

5. Amazon – Acquires Humanoid Robotics Startup Fauna Robotics

Event Summary: Amazon confirmed acquisition of humanoid robotics startup Fauna Robotics; financial terms undisclosed. Fauna launched its $50,000 humanoid robot “Sprout” earlier this year. Market Interpretation: Cloud giants accelerating robotics investments reflects a clear ecosystem expansion strategy. Investment Insight: Accelerating hardware integration of AI creates new growth vectors; Amazon stands to open fresh opportunities in robotics.

IV. Cryptocurrency Project Updates

1. Robbie Mitchnick, Head of Digital Assets at BlackRock, stated institutional investors are increasingly concentrating on Bitcoin and Ethereum, viewing most other tokens as short-lived and lacking long-term value. He emphasized that AI—not token proliferation—is the dominant long-term driver, and noted the natural symbiosis between crypto (“natively digital money”) and AI (“natively digital data and intelligence”).

2. Amy Oldenburg, Head of Digital Asset Strategy at Morgan Stanley, said Wall Street’s move into crypto stems not from fear of missing out (FOMO), but rather from years of infrastructure modernization. The firm is expanding its digital asset strategy across trading, asset management, and infrastructure, and plans to support tokenized equity trading on its Alternative Trading System (ATS) in H2 2026. Oldenburg highlighted that upgrading decades-old banking systems and coordinating global financial networks remain key challenges—even as interest in stablecoins and other tools grows—while institutional crypto activity accumulates quietly.

3. Bitcoin mining economics under pressure, with some miners facing cost constraints—monitor upcoming hash rate and difficulty adjustments.

4. BlackRock withdrew 2,267 BTC ($157.77 million) from Coinbase within the past 10 hours.

5. According to Wintermute market analysis, the U.S. decision to pause strikes against Iranian energy infrastructure for five days lowered geopolitical risk premiums, prompting Brent crude to retreat and Bitcoin to reclaim the $70,000 level yesterday. Wintermute notes that if Strait of Hormuz navigation normalizes and oil stabilizes near $100/bbl, Bitcoin may test resistance between $74,000 and $76,000; renewed escalation could push Bitcoin back toward $65,000; sustained de-escalation may trigger institutional dip-buying, lifting Bitcoin toward $80,000.

6. Bernstein reaffirmed in its latest report that Bitcoin has bottomed, reiterating its year-end price target of $150,000. It characterized Bitcoin’s recent correction as an emotional reset—not indicative of systemic fundamental risks—and noted Bitcoin has outperformed gold by ~25% since the Iran conflict erupted at end-February. Bernstein also upgraded MicroStrategy (MSTR), calling it a high-beta Bitcoin proxy holding ~3.6% of total Bitcoin supply (market cap ~$53.5 billion), assigning it an “Outperform” rating and $450 price target. The report further highlighted rising demand for MicroStrategy’s STRC preferred shares—offering 11.5% monthly dividends with low volatility—helping secure long-term capital while minimizing equity dilution.

V. Today’s Market Calendar

Data Release Schedule

| 22:30 | U.S. | EIA Crude Oil Inventories | ⭐⭐⭐ |

Key Event Preview

March 25 (Wednesday)

- PDD Holdings (Pinduoduo) earnings release (pre-market)—focus on narrowing cross-border e-commerce losses, Temu’s overseas expansion, and domestic competitive pressures; major sentiment driver for U.S.-listed Chinese internet stocks;

- Fed’s Miran speech;

March 26 (Thursday)

- U.S. initial jobless claims (20:30)—high-frequency labor market indicator;

- Multiple Fed officials’ speeches (Jefferson, Barr, etc.)—to validate recent policy trajectory and inflation response;

- G7 Foreign Ministers’ Meeting (March 26–27)—watch for statements on Middle East, Strait of Hormuz, and energy supply.

March 27 (Friday)

- Final March University of Michigan Consumer Sentiment Index—assess impact of geopolitics & oil prices on consumer mood and inflation expectations.

Institutional Views

Goldman Sachs, JPMorgan, and other investment banks recently opined that U.S.-Iran talks have released positive signals, and normalized Strait of Hormuz navigation has alleviated energy supply concerns—pressuring oil prices short term while preserving long-term geopolitical logic. Gold’s pullback is seen as a buying opportunity, with its long-term bull thesis unchanged. Tech sector divergence remains pronounced, with AI infrastructure and domestic chip production themes continuing to attract strong investor preference—Arm and Microsoft’s moves reinforce expanding compute capacity expectations. Overall risk sentiment has improved, yet investors must remain vigilant on tangible negotiation progress and Fed policy trajectory. In sum, amid near-term volatility, portfolios balancing easing energy tensions and AI-driven themes hold prominent tactical value, while longer-term exposure to related supply chains remains compelling.

Disclaimer: The above content was compiled via AI search and verified manually prior to publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News