Bitget UEX Daily Report | Trump Says Iran Has Requested a Pause in Strikes; U.S. Stocks Record Largest Drop Since the Outbreak of the U.S.-Iran Conflict; Apple Opens Siri to External AI

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | Trump Says Iran Has Requested a Pause in Strikes; U.S. Stocks Record Largest Drop Since the Outbreak of the U.S.-Iran Conflict; Apple Opens Siri to External AI

Investors should focus on data verification and policy signals while maintaining flexible positioning.

Author: Bitget

I. Top News Highlights

Federal Reserve Updates

Traders hedge war-related risks, betting on an emergency Fed rate hike within weeks

- Trump extended the deadline for strikes against Iranian energy infrastructure by another 10 days, with the new cutoff now set for April 6 (Eastern Time). He stated the extension was “at Iran’s request” and that negotiations were progressing smoothly—yet he also acknowledged uncertainty over whether the new deadline would be strictly enforced, depending on negotiation progress. However, U.S. media subsequently reported conflicting information. The Wall Street Journal, citing mediators, reported that Iran had not requested a delay in airstrikes and had yet to issue a final response to the U.S. ceasefire proposal; meanwhile, Iran explicitly rejected making its missile program or uranium enrichment activities preconditions for talks, underscoring significant remaining disagreements. With mounting concerns over escalating tensions with Iran, bond traders are pricing in SOFR increases via interest-rate options markets—potentially triggering a Fed rate hike as soon as two weeks.

- Market expectations of three rate cuts this year have been fully reversed. Since the conflict erupted on February 28, the probability of a year-end rate hike has risen to approximately 50%. If rate-hike expectations intensify ahead of the April 29 FOMC meeting, such hedging trades stand to profit—placing downward pressure on short-term Treasury prices. This development reflects how rapidly geopolitical risk is feeding into monetary policy expectations—and may further elevate market volatility.

Global Commodities

U.S. Treasury Secretary Bessent announces imminent launch of Strait of Hormuz shipping insurance program

- The program aims to secure safe passage across this critical chokepoint, which handles roughly one-fifth of global oil and gas shipments;

- Bessent emphasized that Trump-era production policies have significantly boosted domestic U.S. oil and gas output, enhancing economic resilience to short-term energy disruptions;

- Launched against the backdrop of potential Iranian conflict impacts on Strait shipping, the insurance initiative could mitigate supply-chain disruption risks—though its real-world implementation effectiveness remains to be seen. While injecting stability into oil markets, it also highlights persistent geopolitical stress on commodity supply chains.

Macroeconomic Policy

Private credit sector faces concentrated redemption wave, with over $46 billion locked up

- Investors applied for redemptions totaling ~$130 billion this quarter—but due to a 5% quarterly cap, only about two-thirds were processed;

- This week, Apollo Global Management and Ares Management joined BlackRock and Morgan Stanley in imposing redemption restrictions;

- More firms are expected to implement similar measures in the coming weeks, potentially worsening liquidity strains in private credit. Combined with geopolitical risks, this episode may amplify financial system fragility—raising concerns about transmission of credit tightening to the real economy.

II. Market Recap

Commodities & FX Performance

- Spot gold: +0.16%, at ~$4,380/oz.

- Spot silver: −0.54%, at ~$67.70/oz.

- WTI crude: −0.83%, at ~$92–94/bbl.

- Brent crude: −0.78%, at ~$101/bbl.

- U.S. Dollar Index: −0.01%, at ~99.92.

Cryptocurrency Performance

- BTC: −3.39% over 24H, at ~$68,750—dragged down by U.S. equity pullbacks and geopolitical risk, though showing stronger resilience relative to gold;

- ETH: −4.56% over 24H, at ~$2,067—tracking broader market weakness, lacking independent catalysts.

- Total crypto market cap: −3.3% over 24H, declining to $2.44 trillion amid drag from major coins.

- Liquidations: ~$333 million liquidated over 24H, including ~$293 million long positions.

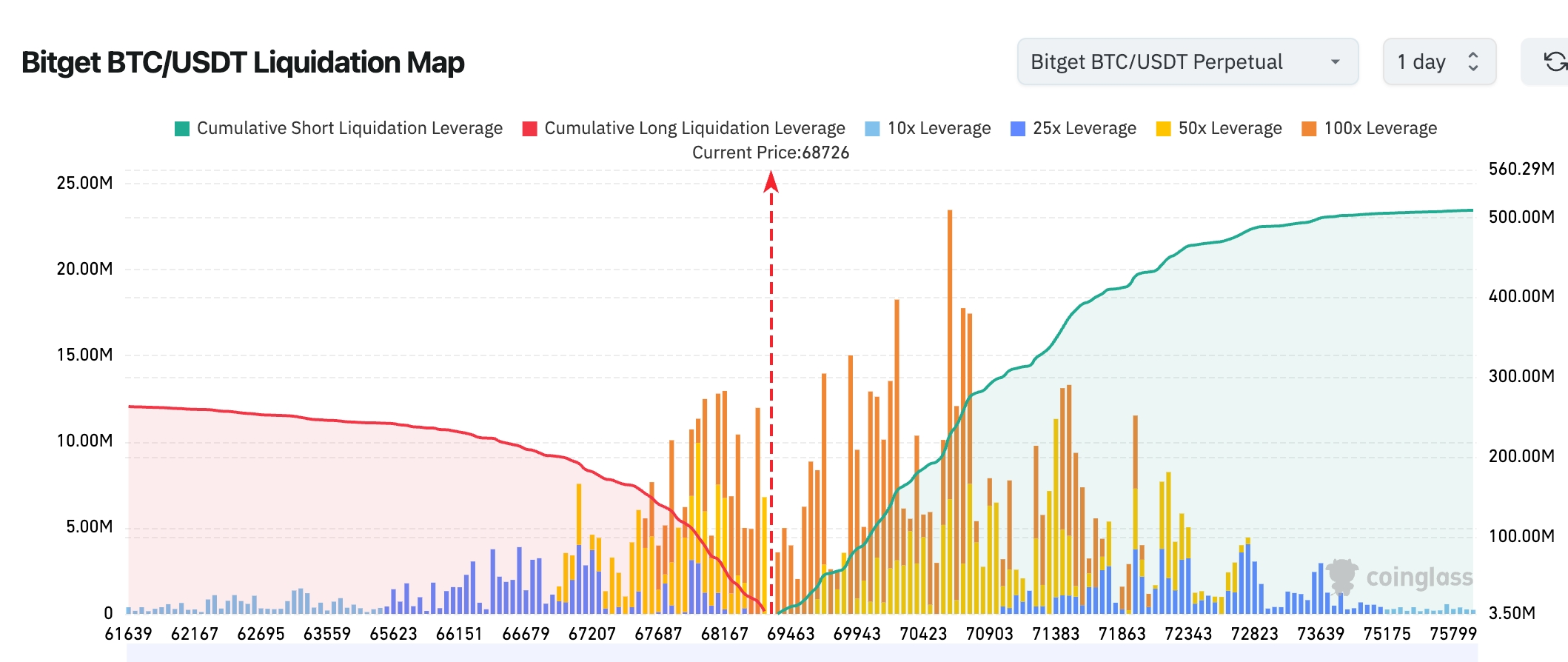

- Bitget BTC/USDT liquidation heatmap: Current price ~$68,726. Downside long-liquidation zones have notably shrunk, while a dense cluster of high-leverage short positions remains concentrated between $69,500–$71,500—making upward short squeezes more likely near-term. Overall structure shows markedly stronger liquidity above than below—suggesting price action favors testing upper liquidation density if consolidation continues.

- Spot ETF net inflows/outflows: BTC spot ETFs saw $129M net outflow yesterday; ETH spot ETFs saw $49M net outflow.

- BTC spot flows: $2.192B inflow vs. $2.359B outflow yesterday—net outflow of $166M, continuing recent volatility patterns.

U.S. Equity Index Performance

- Dow Jones: −1.01%, at 45,960.11—relatively stable trend;

- S&P 500: −1.74%, at 6,477.16—the largest single-day drop since February 28’s conflict onset;

- Nasdaq: −2.38%, at 21,408.08—driven by broad tech-stock weakness.

Tech Giants’ Updates

- Apple (AAPL): +0.11%, at $252.89—Siri’s open-AI strategy lifted AI-platform expectations;

- NVIDIA (NVDA): −4.16%, at $171.24—dragged by broad market and memory-sector weakness;

- Google-A (GOOGL): −3.44%, at $280.92—AI compression algorithm news intensified memory-stock selloff;

- Microsoft (MSFT): −1.37%, at $365.97—aligned with broader tech correction;

- Amazon (AMZN): −1.97%, at $209.50—no standalone catalyst;

- Meta (META): −7.96%, at $547.54—weighed down by overall tech selling pressure;

- Tesla (TSLA): −3.59%, at $372.11—compounded by lowered delivery expectations. Overall, tech giants face dual pressure from geopolitics and macro conditions—Apple’s modest gain underscores AI-strategy strengths.

Sector Rotation Watch

Semiconductor Memory Sector: Sharp decline (~8–11% average)

- Key stocks: Micron (MU) −6.97%, SanDisk −11.02%, Seagate −8.33%, Western Digital −7.7%;

- Catalyst: Google’s TurboQuant AI model-compression algorithm significantly lowers anticipated demand for high-bandwidth memory and storage chips—amplified by broader market corrections, prompting investor profit-taking and cyclical concerns. Morgan Stanley semiconductor analyst Joseph Moore noted the pullback reflects premature pricing-in of cycle-sustainability worries—not fundamental deterioration—as AI capital expenditures remain elevated, supporting long-term demand.

China-U.S. Listed Stocks (ADR) Sector: Down 2.55% alongside broader market

- Key stocks: Alibaba (BABA) −3.43%, Baidu (BIDU) −4.92%, Bilibili (BILI) −4.67%;

- Catalyst: Primarily driven by falling U.S. equity risk appetite and geopolitical uncertainty—high-beta assets under pressure, with no notable stock-specific headwinds.

III. In-Depth Stock Analysis

1. Tesla (TSLA) – Revises Down Market Delivery Expectations Again

Event Summary: Ahead of Q1 vehicle delivery data release, Tesla proactively published a “sell-side analyst consensus summary,” showing 23 investment banks now project ~1.689 million annual vehicle deliveries for 2026—down sharply from the prior year-end forecast of 1.75 million. Concurrently, Wall Street bullish firm Wedbush was removed from Tesla’s select analyst list. This move aligns with Tesla’s consistent expectation-management strategy—designed to avoid sharp share-price volatility should actual deliveries fall short of overly optimistic forecasts. With intensifying EV competition, slowing demand, and macro interest-rate pressures, Tesla is preemptively tempering market hopes for rapid sales rebound. Market Interpretation: Analysts view this as management actively steering the narrative—while potentially pressuring near-term valuations, it helps prevent disappointment-driven sell-offs over the longer term. Given geopolitical energy-price volatility and potential inflationary pressures, EV penetration forecasts face recalibration; analysts expect Tesla to rely on Robotaxi and energy businesses as new growth levers to restore investor confidence. Investment Implications: Investors should closely monitor upcoming Q1 delivery figures and management guidance. Near-term volatility may present entry opportunities—but sustained macroeconomic and competitive pressures warrant caution.

2. Apple (AAPL) – Siri Opens to Third-Party AI, Major Strategic Pivot

Event Summary: Per Bloomberg, Apple plans to break Siri’s current exclusive partnership with ChatGPT in the upcoming iOS 27, enabling users to directly invoke competing AI services—including Gemini and Claude—via Siri. Apple will also develop new tools and launch a dedicated App Store section to facilitate deep integration of third-party AI chatbot apps with Siri and Apple Intelligence. This marks Apple’s strategic shift from a closed ecosystem toward a more open AI platform—aiming to accelerate catch-up in generative AI. Market Interpretation: Analysts broadly see this as a pivotal step to revitalize Siri and enhance iPhone AI appeal. Though still reliant on external AI models short-term, the openness strategy promises ecosystem expansion and heightened user stickiness—alleviating investor concerns over Apple’s slow AI progress. Amid the tech-AI arms race, this could reshape market valuation of Apple’s hardware-software synergy. Investment Implications: Siri’s open strategy is a long-term tailwind for Apple’s ecosystem. Investors should track market reception and real-world adoption rates around the iOS 27 launch—key potential catalysts for Apple’s next growth phase.

3. Micron (MU) and Other Memory Stocks – Google’s AI Algorithm Triggers Sector-Wide Pullback

Event Summary: The memory sector suffered heavy losses—Micron declined for six consecutive trading days, dropping 6.97% Thursday and down over 23% from its March 18 all-time high; SanDisk −11.02%, Seagate −8.33%, Western Digital −7.7%. Beyond broader market correction, Google’s TurboQuant AI model-compression algorithm emerged as a key catalyst—sparking fears that AI training demand for high-bandwidth memory may fall short of prior expectations. Market Interpretation: Morgan Stanley semiconductor analyst Joseph Moore observed that the current pullback reflects premature pricing-in of memory-cycle sustainability concerns—not fundamental deterioration. With AI capex remaining robust, long-term demand trends remain intact—though near-term sentiment dominates sector movement, resonating with broader tech weakness amid geopolitical risk. Investment Implications: Memory stocks face near-term valuation pressure, but fundamentals could support rebounds if AI infrastructure demand continues validating. Investors should distinguish sentiment-driven corrections from genuine demand shifts—monitoring for cyclical inflection signals.

4. Meta Platforms (META) – Texas Data Center Investment Soars to $10 Billion

Event Summary: Meta announced expanding its El Paso, Texas data center project to a $10 billion investment—nearly six times its original $1.5 billion commitment. Targeting 1 gigawatt of power capacity by 2028, the facility will train and run inference for next-gen large language models—supporting Meta AI assistants and content recommendation systems across Facebook, Instagram, and WhatsApp. This underscores Meta’s aggressive, sustained AI infrastructure spending. Market Interpretation: This highlights the intensity of the generative-AI “arms race” among tech giants. Despite high capex pressure, markets view Meta’s self-built compute as reducing reliance on external vendors—and laying groundwork for long-term AI product evolution. Under current high-interest-rate conditions, investors remain attentive to the sustainability of capital-intensive AI investments. Investment Implications: Meta’s massive AI infrastructure investment raises near-term cost burdens—but could translate into core competitiveness long-term. Investors should track monetization progress of Meta’s AI products and return-on-capital metrics.

5. Microsoft (MSFT) – Freezes Cloud Sales Hiring, Tightens Cost Controls

Event Summary: Microsoft recently froze hiring across key divisions—including Azure cloud and North America sales—with some executives forecasting minimal overall workforce expansion over the next few years. This occurred as the company’s fiscal year draws to a close—reflecting how tech giants simultaneously ramp up AI infrastructure investment while enforcing strict cost discipline. Market Interpretation: Analysts view this as Microsoft’s textbook balancing act—managing growth and efficiency amid heavy AI spending. Though hiring freezes may temporarily constrain sales expansion, they bolster profitability and ease investor concerns over capital returns. Efficiency optimization is emerging as a unifying theme across the tech sector during AI transformation. Investment Implications: Cost-control measures help sustain healthy cash flow. Investors should assess whether AI cloud-service growth can offset slower near-term expansion—and maintain long-term conviction in Microsoft’s leadership in enterprise AI markets.

IV. Cryptocurrency Project Updates

1. David Sacks, White House AI and cryptocurrency policy lead, stepped down upon reaching the 130-day term limit for Special Government Employees. Core crypto agenda items—including market-structure reform and stablecoin legislation—remain incomplete. During his tenure, Sacks shaped Trump administration crypto policy, advancing related legislation and advocating for a U.S. Strategic Bitcoin Reserve—yet many industry-anticipated major reforms remain unresolved.

2. JPMorgan has begun accepting Bitcoin and Ethereum as collateral for institutional loans—signaling further expansion of traditional finance’s crypto exposure.

3. According to CoinDesk analysis, Strategy’s perpetual preferred stock STRC rebounded to its $100 par value in just nine trading days after its March 13 ex-dividend date—slightly faster than the historical average recovery period of ten days. Its accelerated rebound may unlock additional funds for Bitcoin purchases.

4. JPMorgan analysts noted that during the Iran conflict, Bitcoin outperformed both gold and silver—showing rising inflows and activity, whereas precious metals experienced sharp outflows and position unwinding. Analysts pointed out that gold ETFs saw nearly $11 billion in outflows during the first three weeks of March, and silver ETF inflows since last summer have been fully erased—while Bitcoin posted net inflows, demonstrating relative strength versus traditional safe-haven assets.

5. U.S. mortgage agency Fannie Mae will accept “cryptocurrency-collateralized mortgages” for the first time. Mortgage lender Better Home & Finance and crypto exchange Coinbase Global launched a new mortgage product allowing homebuyers to pledge Bitcoin and other crypto assets as collateral when applying for Fannie Mae-backed mortgages—without needing to sell crypto for cash down payments.

6. Hashdex’s Hashdex Nasdaq CME Crypto Index ETF (ticker: NCIQ), in its first SEC annual 10-K filing, disclosed adding ADA and LINK to its portfolio—expanding constituent assets to seven. Previously, the ETF held only BTC, ETH, XRP, SOL, and XLM.

V. Today’s Market Calendar

Data Release Schedule

| 10:00 | U.S. | ISM Manufacturing PMI | ⭐⭐⭐⭐ |

| 10:00 | U.S. | Consumer Confidence Index | ⭐⭐⭐ |

Key Event Preview

22:00 (UTC+8): Final March University of Michigan Consumer Confidence Index—watch for impacts of geopolitics and oil prices on consumer sentiment and inflation expectations.

Institutional Views:

With ongoing uncertainty surrounding the Iran conflict—and the U.S. equities market posting its largest single-day drop since March 26’s conflict onset—Wall Street analysts hold divergent but generally cautious-optimistic views. Bernstein reaffirmed its view that Bitcoin has bottomed and remains bullish, highlighting its 25% outperformance versus gold since conflict onset—underscoring crypto’s resilience as a safe-haven asset. Morgan Stanley and others raised 2026 oil-price forecasts, with Macquarie lifting its WTI average estimate to $83/bbl and warning of supply-disruption risks. Morningstar strategists note that historical impacts of geopolitical events tend to be short-lived, and current U.S. equity pricing embeds an optimistic “Trump will always back down” assumption—yet warn of dual pressures from oil prices and inflation. Overall, institutions expect elevated volatility to persist short-term; tangible progress in negotiations could spark risk-asset rallies, whereas reinforced Fed rate-hike expectations may further test market lows. Investors should prioritize data validation and policy signals—and maintain flexible positioning.

Disclaimer: The above content was compiled via AI search and verified manually for publication. It does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News