Bitget UEX Daily Report | US Abandons Plan to Bomb Iranian Energy Facilities; Crude Oil Transportation Through the Strait of Hormuz Resumes; Memory Chips Face Supply-Demand Imbalance, Price Surge Expected

TechFlow Selected TechFlow Selected

Bitget UEX Daily Report | US Abandons Plan to Bomb Iranian Energy Facilities; Crude Oil Transportation Through the Strait of Hormuz Resumes; Memory Chips Face Supply-Demand Imbalance, Price Surge Expected

Geopolitical easing will be the biggest variable this week; investors are advised to balance their positions and pay attention to tonight’s PMI data.

Author: Bitget

I. Key News Highlights

Federal Reserve Updates

Fed Governor Miran Maintains Baseline Expectation of Four Rate Cuts This Year

- Miran stated that short-term oil price volatility triggered by the Middle East geopolitical conflict is insufficient to alter the baseline path of four rate cuts this year; last week, he cast a dissenting vote in favor of an immediate 25-basis-point cut.

- Goolsbee added that the latest inflation shock stemming from the Middle East situation has worsened the outlook, with the labor market nearing full employment while inflation remains significantly above the 2% target.

- Market impact: Near-term rate-cut expectations may undergo adjustments, but the baseline path remains unchanged. Sustained high oil prices will prioritize upside inflation risk, potentially pressuring bond yields.

International Commodities

Hormuz Strait Crude Oil Transport Resumes; SPR Release Probability Extremely Low

- The first mega-tanker carrying 2 million barrels of Iraqi crude successfully transited the Strait—marking the first such instance since the outbreak of hostilities.

- U.S. Energy Secretary Wright indicated that another Strategic Petroleum Reserve (SPR) release remains possible but highly unlikely; current daily releases stand at 1–1.5 million barrels and could be scaled up to 3 million barrels.

- Market impact: Supply concerns ease temporarily; although oil prices remain elevated, demand destruction has not yet been triggered. Consumers may face continued pressure for several weeks, while easing geopolitical risks benefit risk assets.

Macroeconomic Policy

U.S.-Iran Negotiations Enter “Rashomon” Phase; White House Adopts Cautious Stance

- Trump claimed Iran is “very eager to reach a deal,” suggesting an agreement could materialize within five days—or even sooner—and that key points have already been agreed upon.

- White House Press Secretary Levitt emphasized that the situation remains fluid and declined to confirm via media whether negotiations would occur this week. Reports indicate the U.S. may consider targeting Iran’s parliament speaker—a claim Tehran denies.

- Market impact: Optimistic sentiment boosts risk appetite, driving sharp gains in U.S. equities; however, sustainability hinges on tangible progress, and near-term volatility may intensify.

II. Market Recap

Commodities & FX Performance

- Spot Gold: After plunging sharply to $4,098.75 yesterday, it stabilized today and rebounded modestly to $4,369—a 24-hour decline of 0.79%. Recovery in risk sentiment and oil volatility jointly halted panic selling; short-term bottoming signs are emerging, though the dollar and inflation expectations continue to weigh.

- Spot Silver: Fell in tandem with gold yesterday to $60.99 before rebounding to $67.93—a 24-hour drop of 1.54%. The gold-silver ratio further compressed to ~61:1. Dual drivers—industrial demand and safe-haven appeal—confer greater resilience; silver’s industrial metal attributes support stronger rebound elasticity relative to gold.

- WTI Crude: Plunged over 9% yesterday but staged a technical rebound today to $90.47—a 24-hour gain of ~2.4%. With the geopolitical relief narrative fully priced in, the rebound reflects oversold conditions; however, supply restoration and demand uncertainty still cap upside, shifting key drivers toward inventory data and actual transit volumes through the Hormuz Strait.

- Brent Crude: Dropped 10% from recent highs yesterday but rebounded today to $97.76—a 24-hour gain of ~1.79%. It continues trading in a high-range consolidation pattern; supply recovery is underway, yet geopolitical risk premium has not fully dissipated. Clear resistance emerges between $100–$102, with Middle East developments remaining the dominant pricing factor.

- U.S. Dollar Index: Rose modestly today to 99.359—a 24-hour gain of ~0.23%. Having touched lows of 99.09–99.17 yesterday, it rebounded as early-stage risk-asset recovery exerted pressure—but inflation expectations and Fed policy uncertainty provide underlying support. Short-term stabilization above the 99.00 level appears likely.

Cryptocurrency Performance

- BTC: Up ~4.3% to $70,600 over 24 hours. Geopolitical de-escalation and improved U.S. equity risk sentiment fueled a strong rebound. Price surged rapidly from yesterday’s low near $67,600, breaking out of its prior consolidation range into a robust short-term bullish momentum. Key resistance lies at $71,000–$72,000.

- ETH: Up ~4.7% to $2,140 over 24 hours. Followed broader market rebound but with slightly less elasticity. Short-term focus centers on whether price can break decisively above the $2,200 psychological level.

- Total Crypto Market Cap: Up ~3.6% to ~$2.50 trillion over 24 hours. BTC dominance stands at ~58.4–58.6% (slight fluctuations or marginal uptick). Broad-based improvement in risk sentiment drove the rally; altcoins followed suit, though BTC remains firmly dominant. Increased volume signals capital inflow.

- Liquidations: Total liquidations reached ~$661 million over 24 hours—$291 million longs, $371 million shorts. Following yesterday’s short squeeze, today saw profit-taking among longs alongside pullback-driven liquidations. Overall scale expanded versus prior day, reflecting heightened leverage activity.

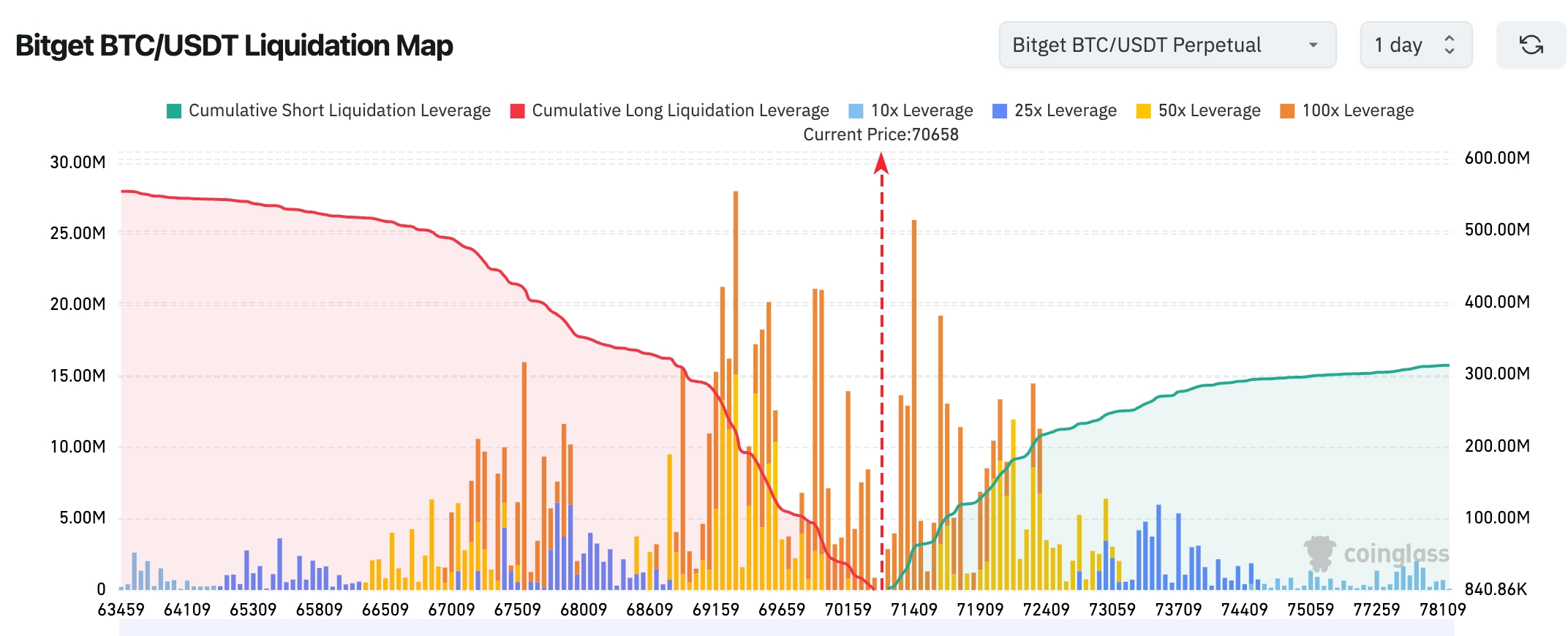

- Bitget BTC/USDT Liquidation Map: Current price ~$70,658. Downside long liquidation zones have largely been absorbed, whereas dense short liquidation clusters accumulate above $71,500–$74,000—indicating markets are more prone to upward short squeezes. Liquidation distribution shows greater upside short pressure than downside long pressure. If price continues consolidating, it is more likely to test upper liquidity zones first. Cumulative liquidation curves show short liquidation leverage substantially exceeds long liquidation leverage—suggesting a mildly bullish (short-squeeze-prone) structure. However, a high-leverage concentration zone exists near $72,000, which may amplify near-term volatility.

- Spot ETF Net Flows: BTC spot ETFs recorded net inflows of $640 million yesterday; ETH spot ETFs registered net outflows of $160 million.

- BTC Spot Flows: $3.18 billion inflow vs. $3.054 billion outflow yesterday—net inflow of $126 million.

U.S. Equity Index Performance

- Dow Jones Industrial Average: +1.38% to 46,208.47—second consecutive day of gains.

- S&P 500: +1.15% to 6,581—short squeeze contributed.

- Nasdaq Composite: +1.38% to 21,946.76—driven by tech and AI stocks.

Tech Giants’ Developments

- NVIDIA (NVDA): +~1.7% to $177.66 (notable intraday volatility). Catalysts: Easing geopolitical tensions lifted overall risk appetite; robust AI infrastructure demand persists (Blackwell series order outlook remains positive), though caution is warranted regarding potential “false breakout” risks if cyclical indicators weaken short-term. The rally is primarily macro-driven—not company-specific.

- Apple (AAPL): +~1.41% to $251.49. Catalysts: WWDC 2026 officially scheduled for June 8–12, with explicit preview of “major AI advancements”—fueling optimism around iOS ecosystem AI integration and upgrade cycles. Record iPhone upgrade rates and strong ecosystem switching trends also bolster sentiment. Morgan Stanley and others project Apple may become the sole major smartphone brand gaining market share in 2026. Geopolitical easing amplifies these tailwinds.

- Google-A (GOOGL): +~0.35% to $302.65. Catalysts: Broad tech sector recovery provided lift; Gemini model progress and cloud AI service growth offer support, though gains were relatively muted—primarily driven by macro risk sentiment rather than standalone events. Google Cloud’s AI business elasticity remains well-regarded amid evolving AI competition.

- Microsoft (MSFT): +~0.3% to $383.50. Catalysts: Steady Azure cloud and AI service demand (enterprise adoption continues rising), though intraday movement was dominated by broader market sentiment. As a leading “AI software tax” beneficiary, its long-term pricing power is widely acknowledged; the short-term rebound stems mainly from collective tech sector short squeezes and reduced geopolitical risk.

- Amazon (AMZN): +~2.32% to $210.14. Catalysts: Accelerated AI spending on AWS cloud services (hyperscaler capex remains strong), combined with resilient e-commerce and advertising revenue. As a dual “cloud + AI” play, Amazon benefits distinctly from AI infrastructure themes—the outperformance reflects market re-rating for renewed AWS growth acceleration.

- TSMC (TSM): +~2.8% to $338.45. Catalysts: Surging demand for advanced nodes (e.g., HBM4 and other AI chips), directly benefiting from AI fab buildout as NVDA/AVGO’s core foundry partner. Analysts forecast 2026–2028 revenue growth meaningfully exceeding Amazon’s. Reduced semiconductor supply chain risk following geopolitical de-escalation further supports valuation recovery.

- Meta (META): +~1.75% to $604.47. Catalysts: Progress in AI application deployment (advertising efficiency + metaverse productivity gains); resource reallocation strategy received endorsement from Goldman Sachs (shifting compute from low-efficiency to high-value AI workloads). Macro risk sentiment recovery amplified gains, though core drivers remain AI narrative continuity and EPS upgrade expectations.

- Broadcom (AVGO): +~4.1% to ~$323.84. Catalysts: Explosive demand for custom AI chips and optical interconnect solutions (key AI infrastructure upgrades), positioning AVGO as a critical “AI plumbing” enabler directly benefiting from hyperscaler order growth. Viewed as a more stable “tollbooth” asset in the AI cycle, its leadership in gains reflects both content growth and gross margin leverage expectations.

Optimistic U.S.-Iran agreement rhetoric meaningfully lowered geopolitical risk premiums, triggering broad-based risk-asset rallies and short squeezes. AI infrastructure investment themes—chips, cloud, interconnect—remain central; unexpectedly strong demand for memory, optics, and advanced nodes further bolsters semiconductor and cloud giant elasticity.

Sector Movement Observations

Memory Chip Sector: Expected Strong Rally

- Key names: Micron Technology (MU)—benefiting from price outlook; Seagate Technology (STX); Western Digital (WDC)

- Catalysts: Wedbush forecasts DRAM prices to surge 130–150% and NAND prices nearly triple in H1 2026—supply-demand imbalance worsening beyond market expectations.

Optical Communications Sector: Broad-Based Gains

- Key names: Applied Optoelectronics (AAOI) +9.39%, Lumentum +3.2%, Corning +5.13%

- Catalysts: AAOI announced a $53 million 800G module order after hours—AI compute demand continues pulling forward optical component orders.

III. In-Depth Stock Analysis

1. Apple Inc. – WWDC 2026 Confirmed

Event Summary: Apple announced WWDC 2026 will take place June 8–12, with the keynote centered on “major AI advancements,” including updates across iOS, macOS, and new developer tools. Bloomberg notes iOS 27’s debut will mark Apple’s AI counteroffensive launchpad. Market Interpretation: Analysts view the event as a demonstration of Apple’s AI catch-up capability; investor attention focuses heavily on system-level AI integration. Investment Implications: Historically a catalyst for the ecosystem, WWDC presents near-term opportunities across Apple’s supply chain and software services segments.

2. Meta Platforms – Strategic Restructuring Endorsed by Goldman Sachs

Event Summary: Meta’s layoffs and cost-cutting measures, along with delayed model launches, raised concerns about AI capital strain. Goldman Sachs countered that this represents proactive resource reallocation—from low-efficiency legacy workloads to high-value AI compute—with room for continued cost structure flexibility. Market Interpretation: Goldman expects sustained EPS upgrades as efficiency and growth rebalance. This is not “wintering over,” but rather “replacing old birds with new ones.” Investment Implications: Strategic adjustments strengthen long-term competitiveness; Meta’s valuation may find support—monitor AI application rollout progress closely.

3. Micron Technology – Anticipated Memory Price Surge

Event Summary: Wedbush reports intensifying DRAM and NAND supply-demand imbalances, forecasting triple-digit price increases in H1 2026—DRAM up 130–150%. Market Interpretation: Analysts believe demand recovery is accelerating faster than expected—directly benefiting memory manufacturers. Investment Implications: The price cycle has turned upward; consider positioning in core memory industry players and monitor earnings elasticity in H1 2026.

4. Alibaba Group – DAMO Academy May Unveil Critical Chip Product

Event Summary: DAMO Academy may unveil a new chip product today targeting AI Agent compute requirements. Tomorrow, Alibaba hosts its 2026 Xuantie RISC-V Ecosystem Conference—last year’s inaugural event featured a server-class RISC-V CPU. Market Interpretation: Institutions regard this as a pivotal step in Alibaba’s AI infrastructure development—drawing high market attention. Investment Implications: Chip breakthroughs could reinforce Alibaba Cloud’s competitive edge—track conference details and market feedback carefully.

5. Applied Optoelectronics – Secures Major 800G Order

Event Summary: Announced a $53 million 800G module order after hours—spurring further post-market share gains. Market Interpretation: The order validates robust AI compute demand and lifts the entire optical communications sector. Investment Implications: Order fulfillment enhances earnings visibility—monitor sustained optical module demand.

IV. Cryptocurrency Project Updates

1. BlackRock’s staked ETH ETF (ETHB) attracted $155 million in net inflows on its first day—emerging as the next institutional demand highlight after Bitcoin ETFs. Monthly staking yield distributions enhance attractiveness.

2. BTC spot ETFs posted three consecutive days of net outflows, yet March cumulative flows remain positive—confirming ongoing institutional accumulation. Whales continue buying near $70,000.

3. Solana Foundation released the report “Privacy on Solana: A Comprehensive Enterprise Approach,” asserting enterprise adoption requires flexible privacy controls—and framing privacy as a customizable feature, not a trade-off. The report argues the next phase of crypto adoption will hinge more on enabling enterprises to control who sees what, rather than relying solely on transparency.

4. The SEC and CFTC jointly issued Interpretive Release No. 33-11412, classifying most native tokens of decentralized networks as digital commodities—and explicitly stating that staking, LSDs, wrapped tokens, and compliant airdrops do not constitute securities offerings. Building on this, the report proposes three previously difficult-to-implement fundraising and treasury models: (i) Liquid Genesis Staking Pools (LGSP), anchored in ETH/SOL staking and incentivized via dual LSD yield and protocol token rewards; (ii) Commodity Pre-Participation Agreements (CPA), granting future network participation rights in exchange for work and funding—not pre-sale tokens; and (iii) Separation-Accelerated Revenue Rights (SARR), linking revenue sharing to decentralized milestones with diminishing payouts—designed to use the “separation principle” as an income tool that accelerates team decentralization.

5. Strategy expanded its ATM financing capacity by $4.41 billion. New authorizations include up to $2.1 billion in Class A common stock ATM, $2.1 billion in STRC preferred stock ATM, and $210 million in STRK preferred stock ATM. Moelis, Alliance, and StoneX were added as sales agents. STRC authorized share count was increased, while STRK’s was decreased.

6. Between March 16–22, Strategy purchased 1,031 BTC for ~$76.6 million—averaging ~$74,326 per coin. As of March 22, its cumulative BTC holdings stood at 762,099 BTC, with total acquisition cost ~$57.69 billion and average purchase price ~$75,694.

7. According to CoinShares’ latest weekly report, digital asset investment products saw net inflows slow to $230 million last week—following interpretation of the Fed meeting as “hawkish pause.” Inflows totaled $635 million in the two days preceding the FOMC meeting, followed by $405 million in outflows afterward. All regions remained net buyers: the U.S. recorded $153 million in inflows; Germany and Switzerland posted $30.2 million and $27.5 million, respectively. Bitcoin products drew $219 million in inflows, while short-Bitcoin products still attracted $6 million—highlighting widening long/short divergence.

V. Today’s Market Calendar

Data Release Schedule

| 09:45 | U.S. | S&P Global Manufacturing PMI | ⭐⭐⭐⭐ |

| 09:45 | U.S. | S&P Global Services PMI | ⭐⭐⭐ |

| 09:45 | U.S. | S&P Global Composite PMI | ⭐⭐⭐⭐ |

Key Event Preview

March 24 (Tuesday)

- S&P Global March Manufacturing & Services PMI flash estimates (leading economic indicator—watch manufacturing performance amid geopolitical stress);

- Fed Vice Chair Barr speech (clues on monetary policy path).

March 25 (Wednesday)

- PDD Holdings (Pinduoduo) earnings release (pre-market)—focus on narrowing cross-border e-commerce losses, Temu’s overseas expansion, and domestic competitive pressures; significant influence on sentiment toward U.S.-listed Chinese internet stocks;

- Fed Governor Miran speech;

March 26 (Thursday)

- U.S. initial jobless claims (20:30 ET)—a high-frequency labor market indicator;

- Multiple Fed officials speaking (Jefferson, Barr, etc.)—to corroborate recent policy stance and inflation response;

- G7 Foreign Ministers’ Meeting (Mar 26–27)—watch for statements on Middle East, Hormuz Strait, and energy supply.

March 27 (Friday)

- Final March University of Michigan Consumer Sentiment Index—assess impact of geopolitics and oil prices on consumer psychology and inflation expectations.

This week’s core U.S. equity themes: Hormuz Strait crisis dominance (oil price, inflation, energy stocks volatility); CERAWeek geopolitical energy discussions; intense Fed official commentary; economic data (PMI, jobs, sentiment); and key earnings (e.g., PDD). Amid geopolitical uncertainty and elevated oil prices, market volatility is expected to intensify sharply—energy and inflation-sensitive sectors will be most exposed.

Institutional Views:

Scott Rubner, Chief Investment Strategist at Citadel Securities, noted record short positions face covering risk—if geopolitical tensions ease, a powerful rebound may follow, with hedge funds and systematic strategies poised to drive buying. Wedbush analysts stressed memory chip price gains far exceed expectations—boosting MU, STX, and WDC. Goldman Sachs views Meta’s layoffs as strategic resource reallocation—not passive contraction—supporting continued EPS upgrades. Overall, markets are highly sensitive to positive catalysts, yet oil prices and inflation pressure continue weighing on Fed policy paths. In crypto, while BTC ETFs saw short-term outflows, cumulative inflows remain solid—suggesting institutions are accumulating during pullbacks. Broader risk sentiment is recovering alongside equities; near-term focus centers on the $70,000 psychological level and liquidation cluster zones. Geopolitical de-escalation is the biggest wildcard this week—investors should balance portfolios and closely monitor tonight’s PMI data.

Disclaimer: The above content was compiled via AI search and verified manually for publication only—it does not constitute any investment advice.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News