a16z Weekly Chart: Tech Giants Monetize “Side Hustles” Through Investments; AI Products Can Go Viral in a Day

TechFlow Selected TechFlow Selected

a16z Weekly Chart: Tech Giants Monetize “Side Hustles” Through Investments; AI Products Can Go Viral in a Day

Four charts, four counterintuitive signals.

Author: a16z New Media

Translation & Editing: TechFlow

TechFlow Intro: This week’s a16z Chart Pack covers four topics: (1) Mega-platforms recorded abnormally high “Other Income” in Q1—driven by private investments; (2) AI-generated e-books are flooding Amazon, yet the volume of high-quality content is also growing; (3) Call center employment in the Philippines is rising against the trend, as voice AI remains too expensive to replace humans; and (4) AI app downloads, revenue, and time spent on mobile have all doubled—Codex’s daily installs even surpassed Claude Code’s. Four charts, four counterintuitive signals.

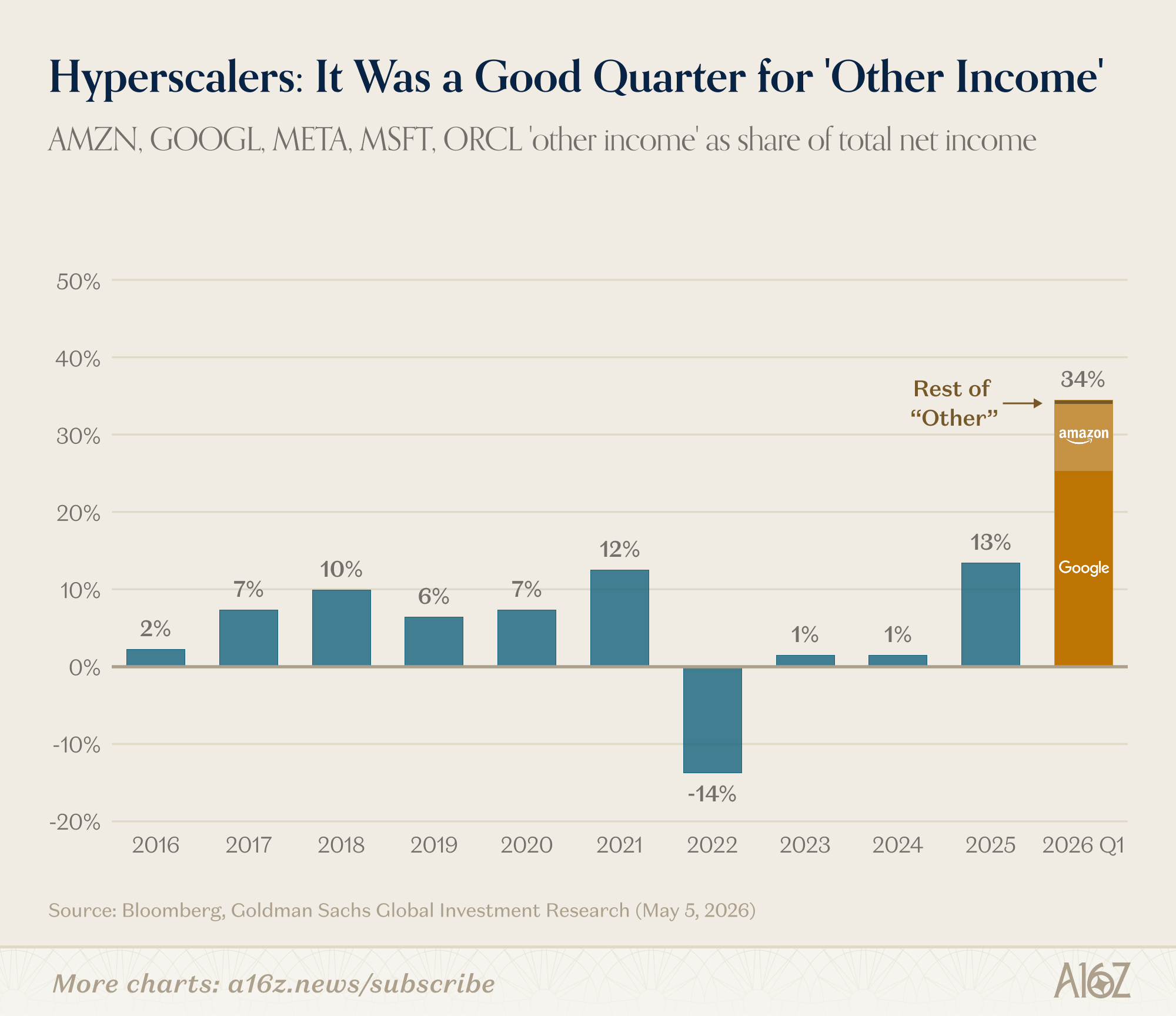

“Other Income”: Venture Capital as a Core Business for Tech Giants

Public-market profit growth has already been extraordinary—and Wall Street expects it to accelerate further this year.

But beneath those headline profit figures lies an unusual detail: mega-platforms’ income no longer comes exclusively from core operations. In Q1, “Other Income” accounted for an unusually large share of net income.

Caption: Share of “Other Income” in mega-platforms’ net income—over one-third in Q1, versus a historical norm of 5–10%

In Q1, “Other Income” accounted for over one-third of net income—a figure that historically hovered between 5% and 10%.

Where does this money come from? Primarily from private investment returns at Amazon and Google—totaling roughly $53 billion. Alphabet’s CFO stated on its earnings call that “other income and expense was $37.7 billion, primarily driven by unrealized gains from its non-public equity investment portfolio”; Amazon disclosed a $15.6 billion net gain from its investment in Anthropic in its 10-Q filing.

In short: Mega-platforms are running successful venture capital businesses.

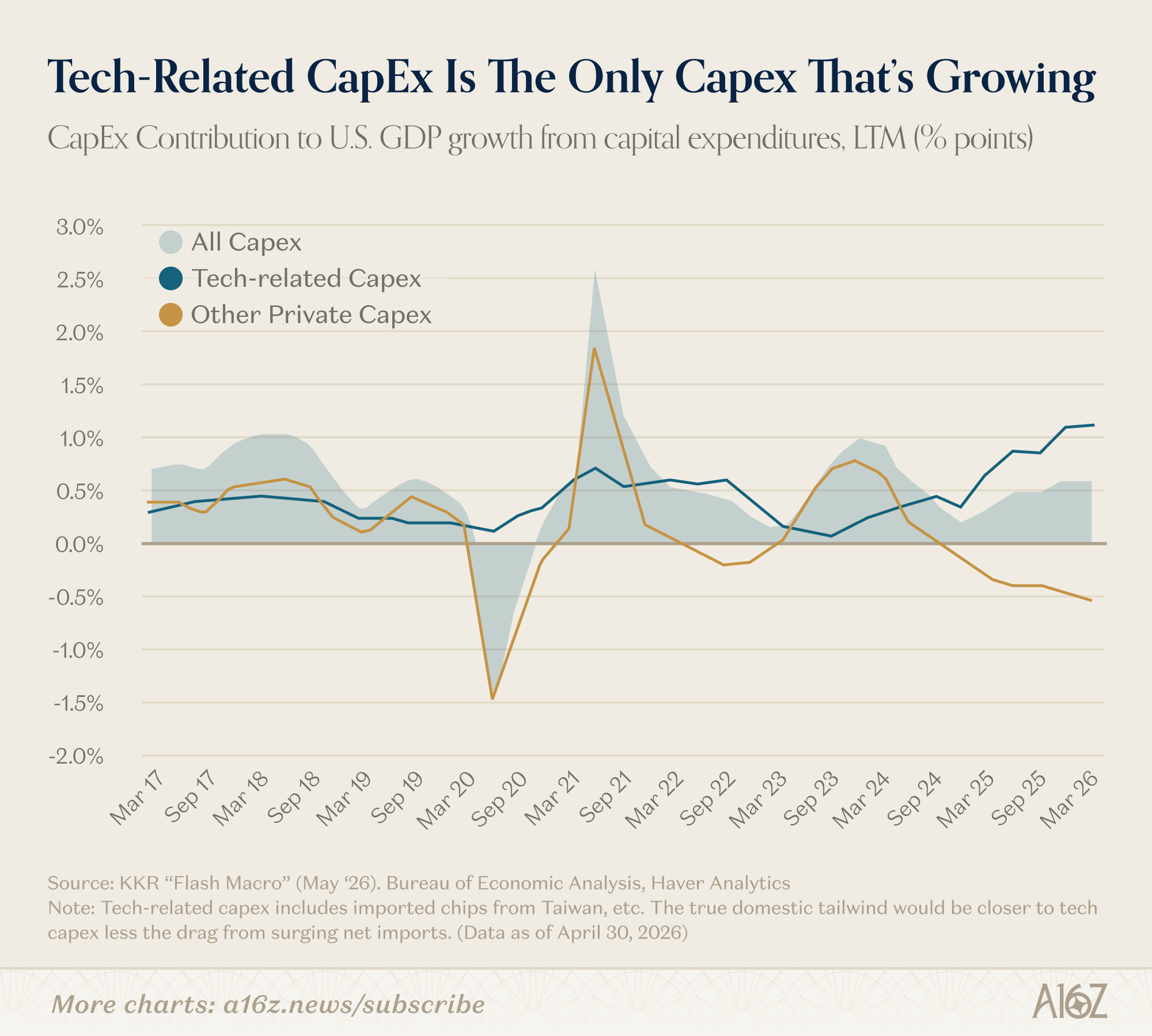

Yet tech investing is no longer just the domain of giants. KKR estimates that tech-related capital expenditures are now the *only* category of capex currently driving GDP growth:

Caption: Tech capex contributed 1.9 percentage points to Q1 U.S. GDP growth—nearly all of the 2% total increase

Q1 U.S. GDP grew by 2%, of which tech capex contributed 1.9 percentage points. In other words, without tech investment, GDP growth would have stalled.

Broadening the definition further—per the U.S. Bureau of Economic Analysis (BEA)’s measure of total corporate capital spending (including R&D and software)—tech now accounts for 55% of all U.S. corporate investment:

Caption: Tech’s share of total U.S. corporate capital spending has risen steadily—and now stands at 55%

This share has climbed consistently for years—and AI may accelerate the trend. Yardeni Research proposes an intriguing framework: Economics textbooks traditionally list three factors of production—land, labor, and capital. A fourth should now be added: data. AI makes data more valuable—and the more valuable data becomes, the greater the demand for both data itself and the tools to process it.

That Amazon and Google run successful VC arms is one thing. The larger reality is: everyone is now a tech investor.

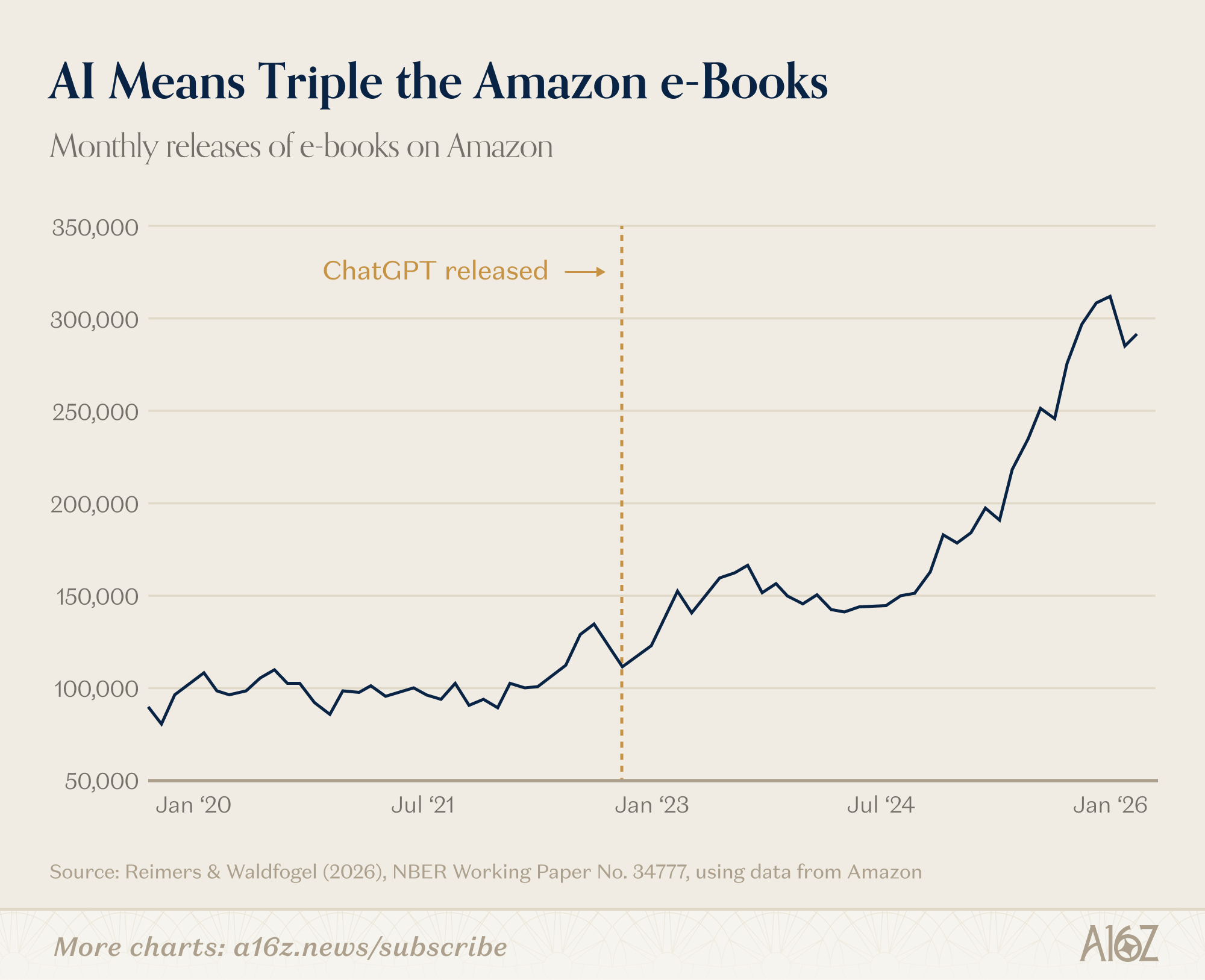

AI “Garbage Books” Are Flooding the Market—but High-Quality Content Is Also Growing

The good news: There are vastly more e-books on Amazon than ever before. The bad news: much of that growth consists of AI-generated “garbage.”

Caption: Monthly e-book releases on Amazon have tripled since ChatGPT’s launch—surpassing 300,000 titles per month by end-2025

Since ChatGPT’s release, monthly e-book releases on Amazon have surged from ~100,000 to over 300,000.

This chart admits two interpretations.

The first is straightforward: AI has arrived—and with it, a tsunami of low-quality, machine-generated content has overwhelmed Amazon.

The second interpretation is more nuanced: yes, garbage has increased—but so has the volume of “decent” books. A recent NBER paper by professors at Cornell and Minnesota quantifies this effect using a nested Logit demand model. It finds that the 2025 e-book selection set delivers approximately 7% more consumer surplus than a counterfactual baseline assuming purely human-authored books. Readers saw almost no benefit in 2023—but by 2025, the gains had become tangible.

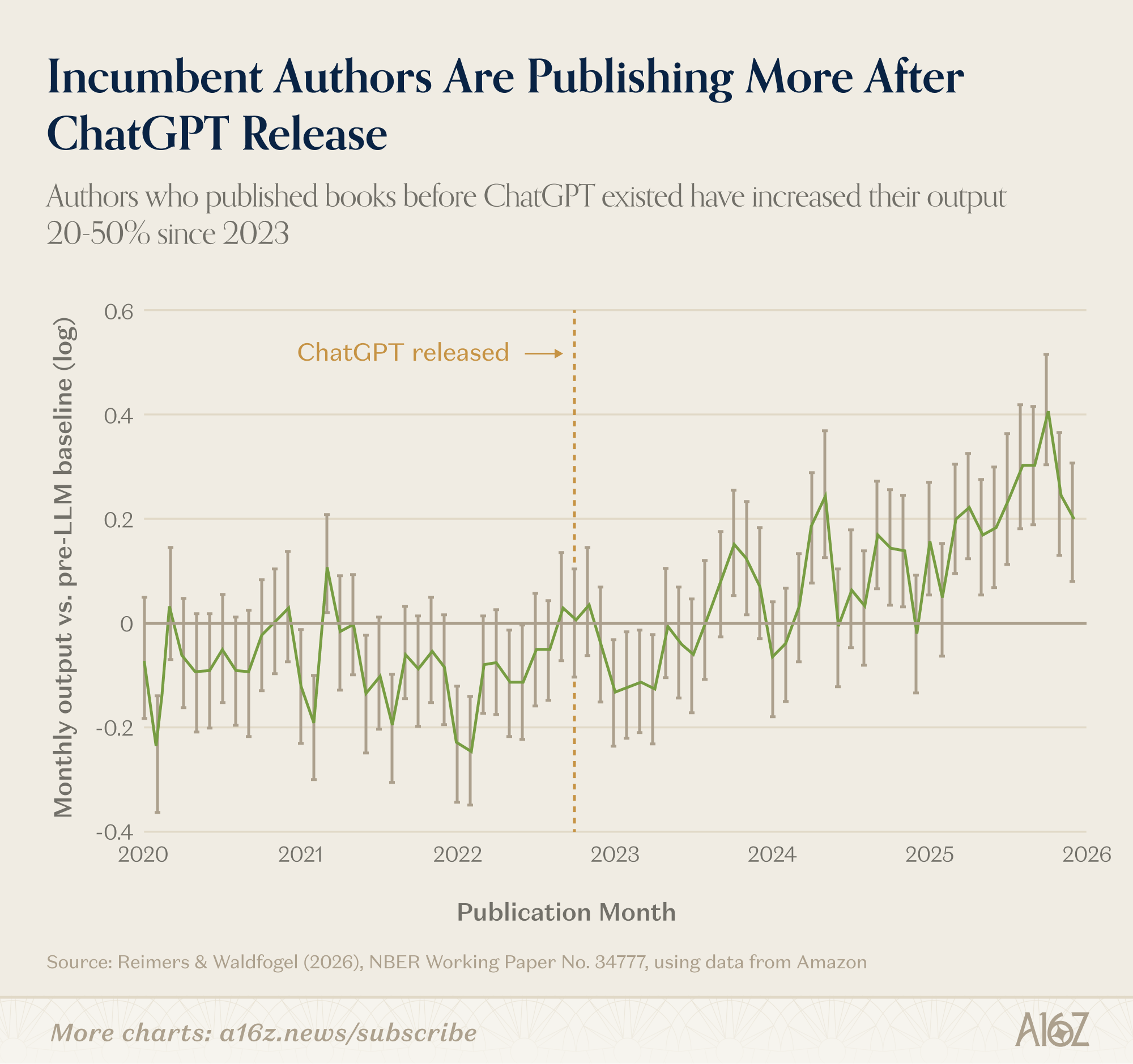

An even more interesting finding: AI benefits “legacy authors” (those who published *before* LLMs emerged) the most.

Caption: Post-2023, output from “legacy authors” (those publishing pre-LLM) surged dramatically—AI boosted their productivity

AI isn’t merely spawning robot authors—it’s also increasing human authors’ output efficiency.

Marc Andreessen predicted on David Perell’s podcast several years ago: writing will become so easy that low-quality content floods the market—but simultaneously, such powerful tools will also trigger an explosion in high-quality output. Garbage is real—but so is the residual value. Great writers are now writing *more*.

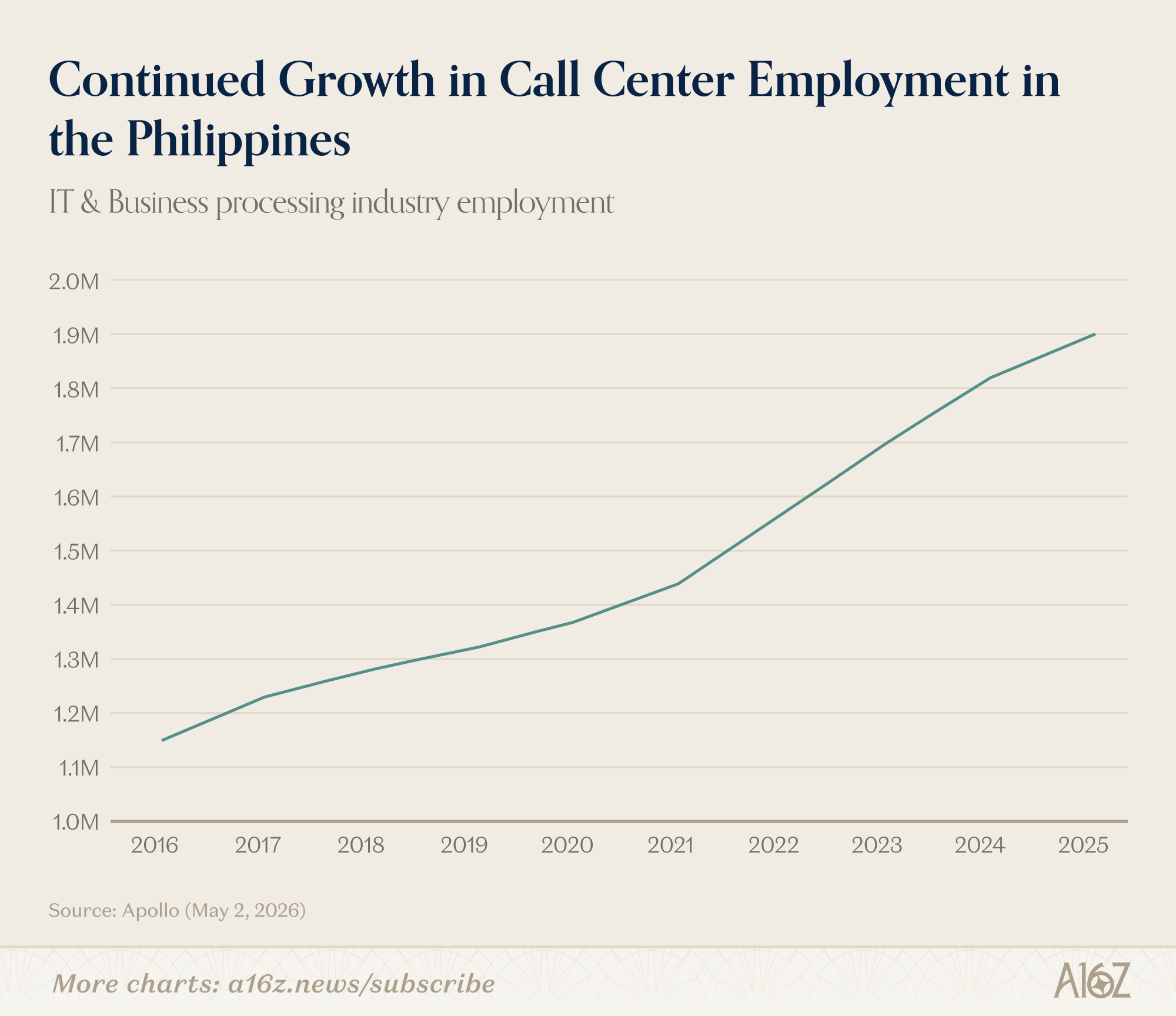

Call Centers Aren’t Dying—Voice AI Is Still Too Expensive

David George recently argued in an article that the “AI job apocalypse” is a myth. He distinguishes between “replacement” and “augmentation”—and customer service is perhaps the textbook case for replacement: AI can answer every question, with infinite patience.

The logic is sound. But the data disagrees.

Caption: Employment in the Philippines’ IT and business process outsourcing (BPO) sector rose from 1.15 million in 2016 to 1.9 million in 2025—spanning every major leap in AI capability

The Philippines is the world’s call center capital. Apollo data shows employment in the IT and BPO sector rose from 1.15 million in 2016 to 1.9 million in 2025—across every major AI advancement. The industry association projects 70,000 new jobs in 2026, a 3.7% year-on-year increase.

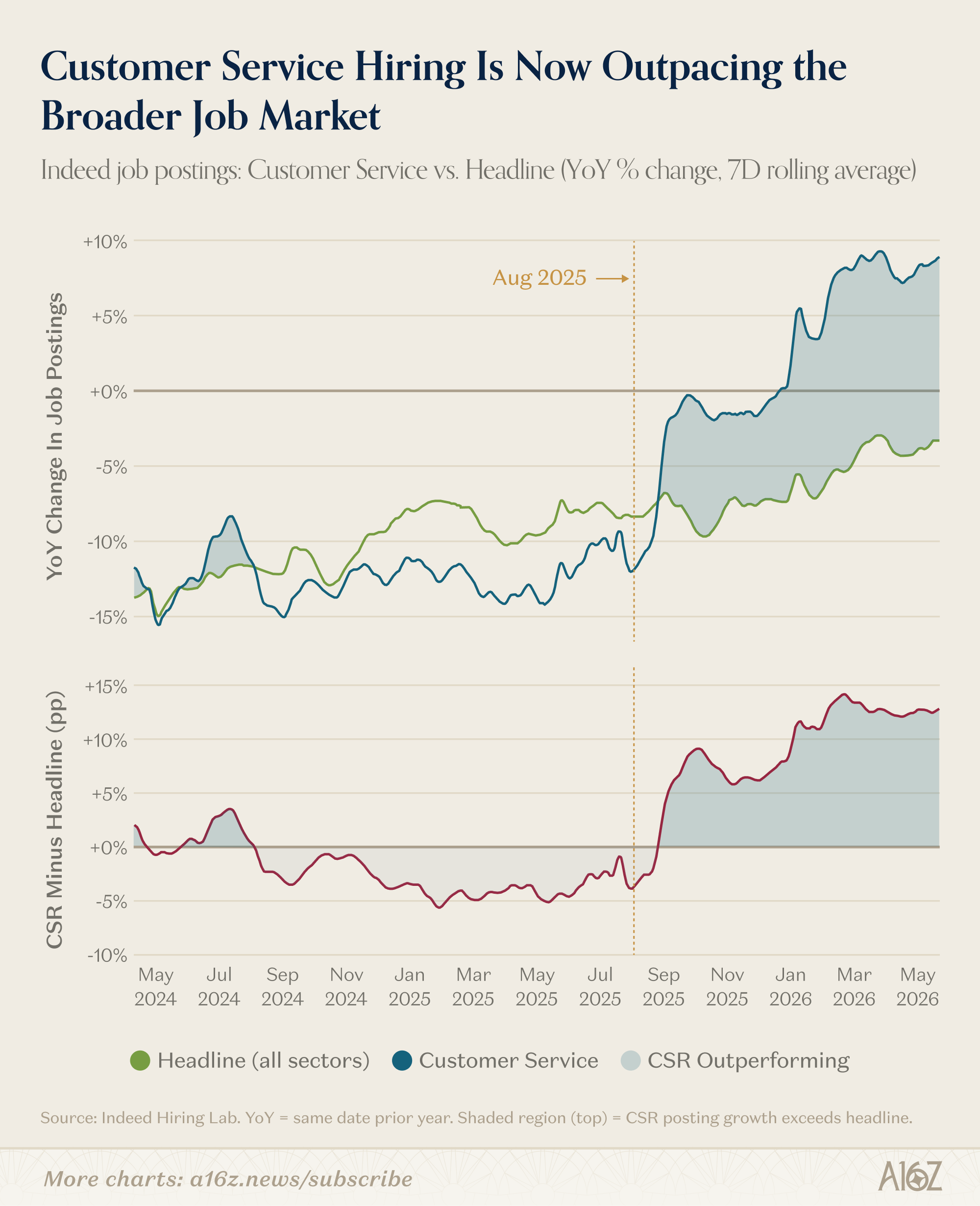

The U.S. tells a similar story. Indeed data shows customer service hiring hasn’t declined—in fact, it’s outperforming the broader market:

Caption: Indeed data shows customer service hiring grew ~10 percentage points faster YoY than overall hiring—the inflection occurred in August 2025

Customer service hiring grew about 10 percentage points faster YoY than overall hiring—and this inflection point occurred only recently, in August 2025.

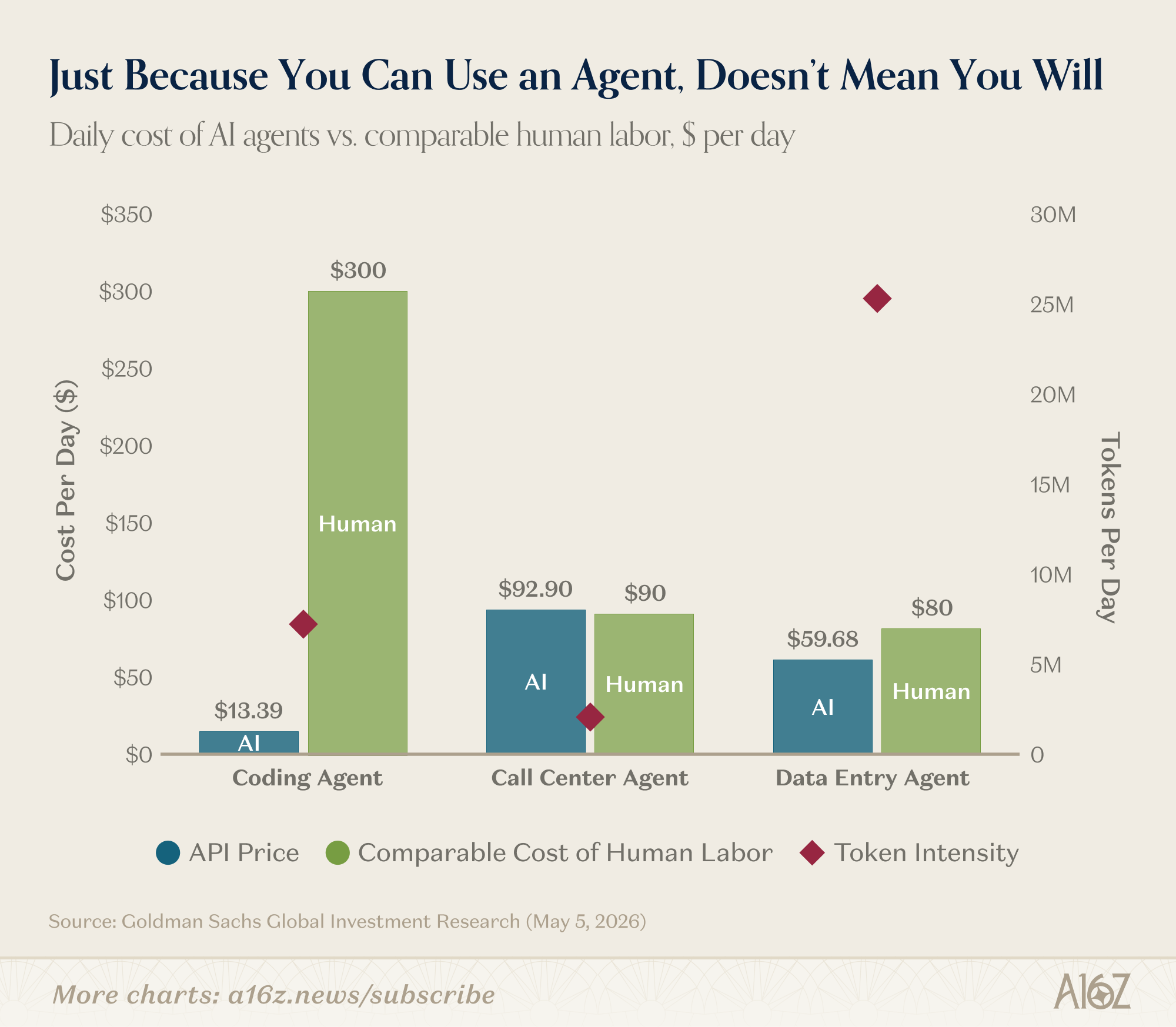

Does this mean AI is actually beneficial for the customer service industry? Probably not.

The core reason is cost. Text-based LLM outputs are cheap—but voice AI remains expensive. Goldman Sachs conducted an internal cost comparison between AI and human customer service agents:

Caption: Goldman Sachs estimates AI agent full cost at ~$92/day vs. ~$90/day for human agents—essentially flat

The full cost of an AI agent is ~$92/day, versus ~$90/day for a human agent—essentially unchanged. Compare that to programming agents: text-only output, with costs orders of magnitude lower than human developers. The difference between coding and customer service lies in latent demand—coding demand vastly exceeds customer service demand, so cost reductions yield completely different leverage effects.

Klarna’s story is the clearest illustration. In early 2024, Klarna announced it replaced 700 customer service agents with AI—and its CEO claimed AI handled *all* tasks. That became the canonical “AI replaces humans” case study. By May 2025, however, the CEO reversed course and began rehiring—due to declining service quality and repetitive, generic responses.

This won’t last forever. API costs are falling rapidly, and companies like Decagon are scaling fast—the cost comparison 18 months from now could look entirely different.

Great AI Products Scale Extremely Fast

AI’s penetration into mobile is astonishing:

Caption: Mobile AI app downloads, revenue, and time spent—Q1 data

Caption: AI app monetization and time spent up nearly 100% YoY in Q1

Downloads, monetization, and time spent all turned upward in Q1—with monetization and time spent nearly doubling YoY.

Perhaps people are spending less time on social media because they’re vibe-coding on their phones? Not necessarily a bad thing.

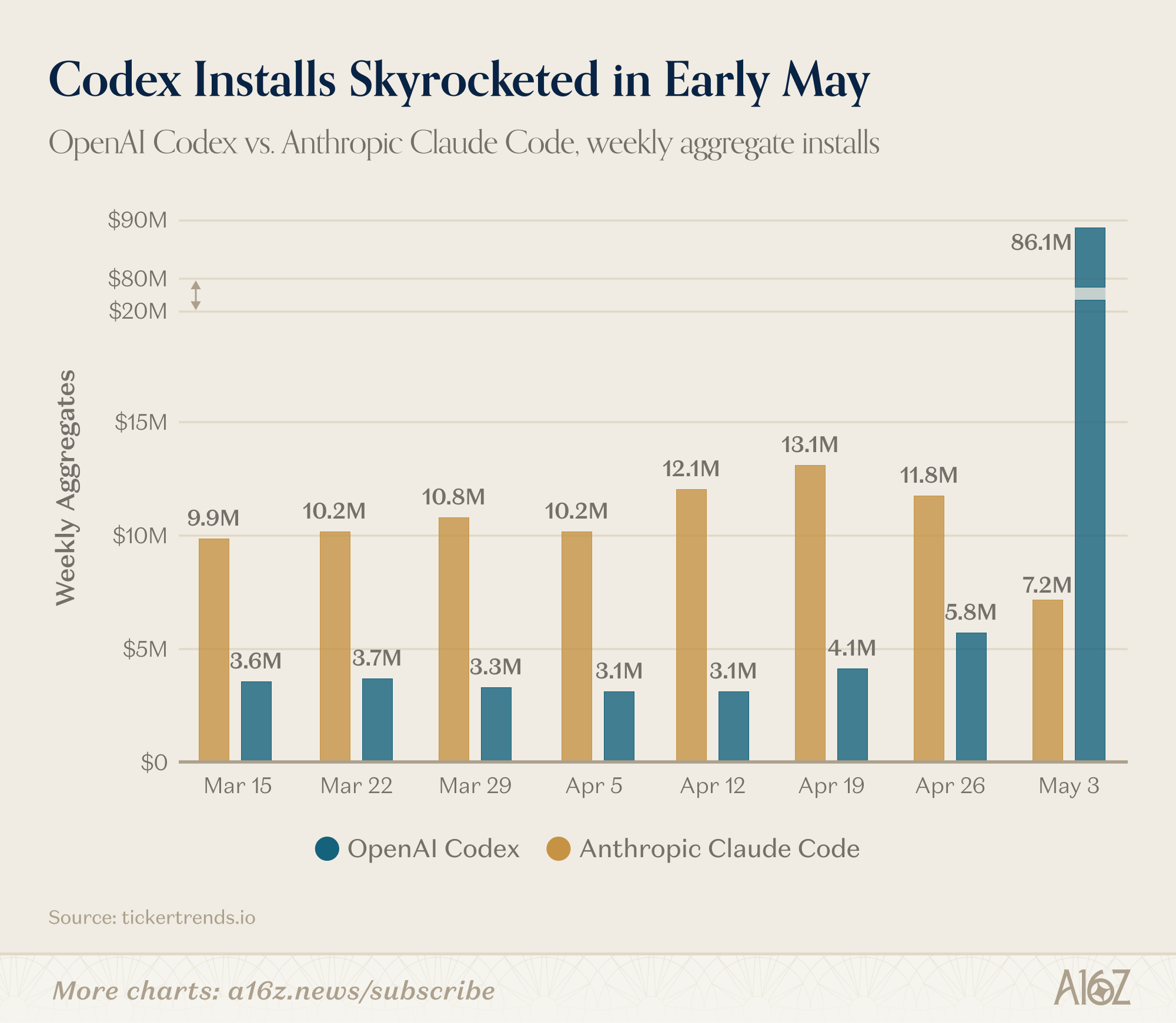

Speaking of vibe-coding—a new entrant has arrived:

Caption: Codex’s daily installs surged in May—briefly surpassing Claude Code, which had held the crown as top coding tool for the past year

Codex’s daily installs spiked in May, briefly exceeding Claude Code’s. Of course, this reflects a single-day metric—and Codex starts from a smaller base—but it underscores one key point: great products spread extremely fast.

Jeff Bezos said in 2012: “In the past, you could sell a mediocre product with marketing. That’s getting harder and harder.” Great products get customers to do the marketing for you.

In AI, this logic is pushed to the extreme. Signals propagate instantly, users switch loyalties readily—and no one is loyal to any platform or model.

The same holds true in B2B:

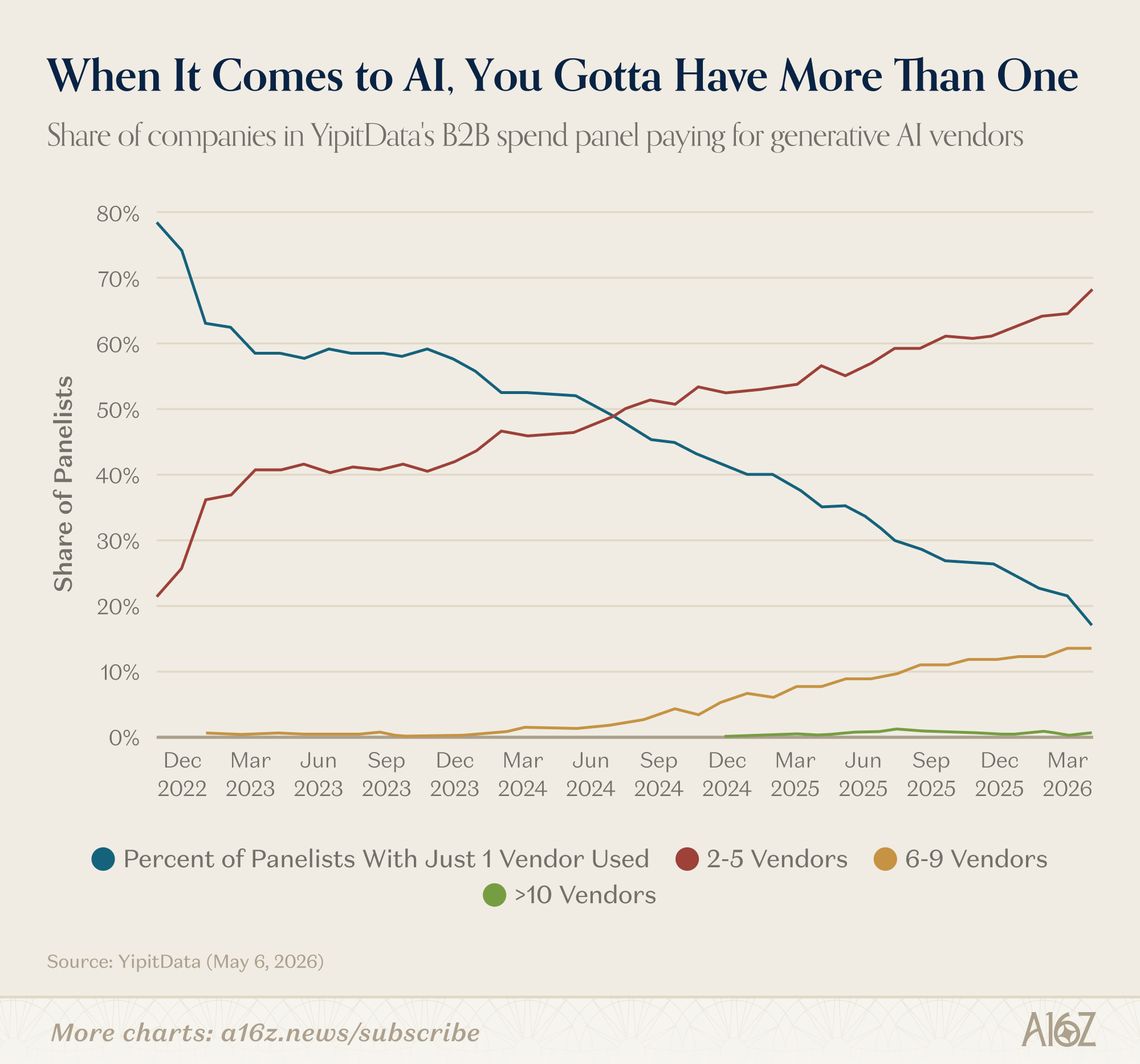

Caption: YipitData shows rising share of enterprises using 2–5 and 6–9 AI vendors—fewer than 20% rely on just one

The share of enterprises using multiple AI vendors continues rising—while those relying on only one vendor has fallen below 20%. The B2B AI market currently has no winner-takes-all player.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News