Trader Taiki’s Self-Reflection: Bitcoin Is Brewing a “God-Level Bullish Candle,” While Small Positions Are Taken on Zcash

TechFlow Selected TechFlow Selected

Trader Taiki’s Self-Reflection: Bitcoin Is Brewing a “God-Level Bullish Candle,” While Small Positions Are Taken on Zcash

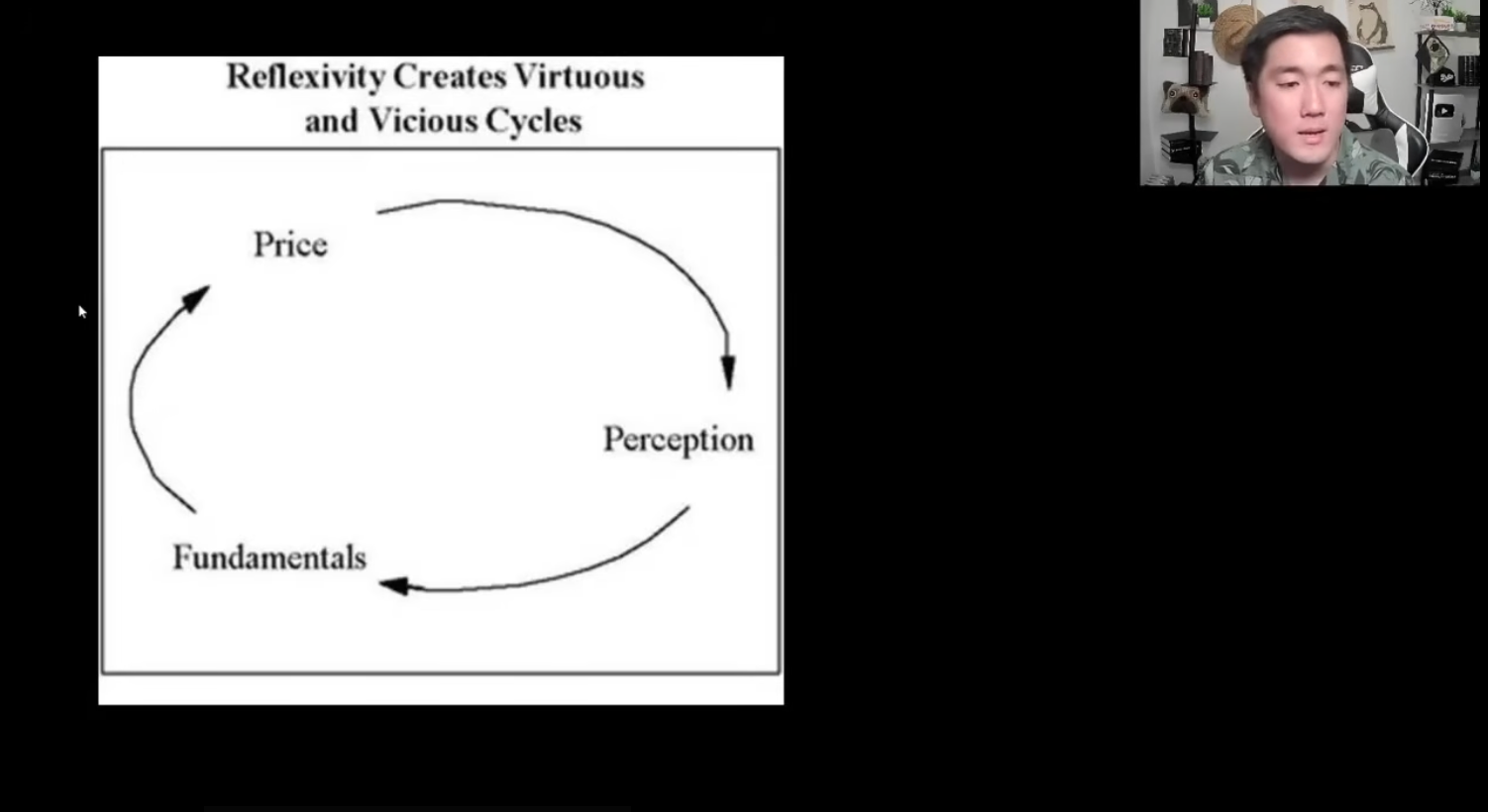

In Taiki’s view, Bitcoin’s most critical support at present is not market sentiment, but rather structural buying pressure that can be quantified and tracked on a monthly basis.

Compiled & Translated by TechFlow

Host: Taiki Maeda

Podcast Source: Taiki Maeda

Original Title: Why Bitcoin is About to Print A God Candle

Air Date: May 5, 2026

Key Takeaways

In this episode, Taiki Maeda conducts an in-depth analysis of Bitcoin’s (BTC) current market dynamics and shares his latest views on the ongoing rally.

He argues that marginal sellers have largely been exhausted, while the conventional “four-year Bitcoin halving cycle” narrative has caused many investors to exit prematurely. Meanwhile, Michael Saylor’s continuous BTC purchases via Strategic Capital (STRC) are propelling the market into a reflexivity-driven upward channel.

According to Taiki, BTC’s most critical support right now isn’t sentiment—it’s structural, quantifiable monthly buying pressure. As long as STRC’s demand for Bitcoin remains intact, BTC is likely to continue rising steadily “up the wall of worry.”

Built on this assessment, Taiki also explains why he seeks to move beyond the “midcurve bias”—an overcomplication-induced cognitive distortion—and instead allocate a small portion of his portfolio to Zcash ($ZEC), viewing it as an asset with the highest degree of reflexivity (i.e., where market sentiment and price action mutually reinforce each other). He further elaborates on why he believes this bull run will begin with Bitcoin leading the charge, gradually spilling over into more volatile crypto assets.

Highlights of Key Insights

The Bullish Logic for BTC and the Failure of the “Four-Year Cycle”

- “At previous market tops, marginal buyers were largely exhausted, and the DAT cohort driving valuation higher had already run out of steam. Now the situation is reversed: marginal sellers appear nearly depleted, and DATs are regaining momentum.”

- “When BTC was hovering around $65,000–$66,000, market pessimism even exceeded levels seen after the Luna collapse, the 3AC implosion, and the pandemic crash.”

- “The best time to buy is rarely comfortable. Investors often wait until social media sentiment turns uniformly bullish—by which point the optimal entry has usually passed.”

- “Many assume everyone can sell at the top together, then collectively wait until Q4 to bottom-fish—but I see this as a lazy expectation already priced in six to seven months ago.”

- “If all those who wanted to sell have already done so, who would drive prices lower again in Q4?”

STRC (Saylor)’s Reflexive Flywheel

- “In March, he bought roughly $1.5 billion worth of Bitcoin; in April, another ~$3.4 billion. Crucially, most of these purchases occurred during the second week of each month.”

- “Historically—and during the prior bull run—Saylor tended to buy aggressively only after BTC had already accelerated sharply and sentiment ran extremely hot. That was his role. But recently, he’s been buying on dips—a development worth serious attention.”

- “Saylor’s consecutive announcements of multi-billion-dollar BTC purchases naturally lift Bitcoin’s price. Rising BTC prices, in turn, boost MSTR’s market net asset value (mNAV), reinforcing shareholder confidence in his leveraged strategy to increase BTC holdings per share. Higher mNAV then makes further fundraising easier, enabling yet more BTC purchases.”

- “As long as STRC trades above $100, Saylor can issue new shares and use proceeds to buy BTC. In effect, he’s accumulating BTC at a dollar-cost basis of ~11.5%. As long as BTC’s appreciation exceeds this threshold, the model remains self-sustaining.”

- “Starting mid-July this year, he plans to split each month’s large BTC purchase into two tranches—one mid-month, one month-end. This adjustment makes his buying less predictable and harder for the market to front-run. Going forward, he may increase purchase frequency to weekly.”

Escaping the ‘Midcurve Bias’

- “In my first cycle, I leaned too far left; in the second, I drifted too far toward the center. So in this third cycle, I’m trying a new approach: synthesizing lessons from both—retaining risk sensitivity without letting bear-market PTSD permanently trap me in the ‘middle ground.’”

- “Markets don’t always reward the person who delivers the slickest PPT—they reward those who actually catch the primary uptrend. This time, I want at least part of my portfolio to tilt toward maximum reflexivity.”

Zcash ($ZEC) Investment Rationale and Reflexivity

- “Once ZEC drops below $50, the narrative instantly shifts to ‘Who even cares about privacy anymore?’ Yet if it rallies near $400, the narrative flips to ‘Privacy is a human right—the most critical sector.’ In other words, much of Zcash’s narrative is ignited by price itself.”

- “Naval once said, ‘Bitcoin is insurance against fiat; Zcash is insurance against Bitcoin.’”

- “Like BTC, Zcash has a fixed supply cap of 21 million coins and follows a halving schedule. Its current market cap is only ~0.5% of BTC’s. So it’s entirely plausible the market could soon start telling a new story: Why couldn’t Zcash reach 1%, 2%, or even more of BTC’s market cap?”

The Rotation Between BTC and Altcoins

- “The first stage of any bear-to-bull transition is BTC leading the way. I don’t believe in scripts where Ethereum rockets off immediately upon market bottoming. Restoring industry-wide confidence requires Bitcoin to take the lead.”

- “The smarter move is accepting a higher entry price and rotating profits from BTC into higher-beta assets—not pre-emptively stacking up narratives you’re not fully confident in.”

- “Narratives like VC tech, Layer-1s, and DeFi aren’t currently the most easily digestible for capital. By contrast, straightforward, intuitive stories—like Bitcoin as ‘digital gold’ or Zcash as ‘privacy infrastructure’—are simpler, more direct, and faster to gain traction in a bull market.”

Trading Psychology and the Logic of Big Money

- “I increasingly believe investing should aim for a ‘sleep-quality-adjusted return.’ Holding assets you truly believe in—while sleeping soundly and living comfortably—often proves more sustainable long-term than constant high-stress monitoring.”

- “Many assume returns come from frequent trading, but most real money is made by holding appreciating assets—not by incessant churning.”

- “In highly reflexive markets like crypto, sometimes just one or two strong green candles are enough to reset investor psychology. Price rises breed renewed confidence, risk appetite, and belief in the industry’s future. Green candles themselves generate new buying pressure.”

- “Shorts often sound smarter, especially in bull markets, where they spin elegant risk narratives—but reality tends to favor the optimists when big money is made.”

- “Real wealth isn’t created in buying and selling—it’s forged in waiting. You profit in bull markets; you grow richer in bear markets.”

Reviewing My Bullish Thesis for BTC

Taiki Maeda:

I believe Bitcoin is about to print a ‘god candle’ powerful enough to silence bears outright—a long-overdue ‘green candle therapy’ for the entire market. In this video, I’ll explain why I remain bullish on BTC, why I’ve added Zcash to my medium- to long-term portfolio, and outline my broader plan ahead.

First, why do I think the market has bottomed and entered a new bull phase? For months, I’ve emphasized one key observation: At prior market tops, marginal buyers were largely exhausted, and the DAT cohort pushing valuations higher had run out of steam; now the opposite holds—marginal sellers appear nearly depleted, and DATs are regaining momentum. Here, ‘DAT’ refers primarily to structural buyers like Michael Saylor and Strategy Capital—and I believe that as long as Saylor’s playbook continues working, others will inevitably follow.

Over the past six months, my primary focus has been on capital flows. When assessing the market, I repeatedly ask myself three questions: Where is consensus positioned? Who else remains to sell? Who else remains to buy? Six to seven months ago, with BTC still in six figures, consensus expected $250K for BTC and $8K–$10K for ETH—and the Q4 altcoin season was treated as gospel. In that environment, the correct move was precisely to sell into that uniform bullishness.

One critical signal I watched closely was MSTR’s mNAV collapsing starting last October and November—I interpreted that as the final warning sign of a major bull cycle ending. But over recent months, sentiment has flipped entirely. As BTC dipped near $60K, cries of $40K–$50K bottoms returned; ETH was expected back at $1,000; and Q4 was guaranteed to offer a better bottom. To me, that’s laziness. During the Iran war, U.S. equities fell 10%, yet Bitcoin held $65K—and the Fear & Greed Index posted its lowest monthly reading since its 2017 launch. Put simply: At $65K–$66K, market pessimism exceeded levels seen post-Luna, post-3AC, and post-pandemic crash.

I’m not a mechanical sentiment trader, but such extreme pessimism signals one thing clearly: Many have already sold; many have rotated into equities; Twitter is saturated with exhaustion and despair. If you’re a long-term Bitcoin believer, that at least warrants reflection. The right time to buy is rarely comfortable—most wait until social media sentiment turns uniformly bullish, but by then, the optimal price is usually gone.

I’m also increasingly skeptical that the four-year cycle will hold this time. Many assume everyone can sell at the top together, then collectively wait for Q4 to bottom-fish—but I see this as a lazy expectation already priced in six to seven months ago. Last year, near $120K, many believed ETFs and Trump would usher in a ‘super-cycle.’ After BTC corrected 40%–50% to the $60K–$70K range, those same bulls finally capitulated—switching allegiance to the four-year cycle and declaring Q4 the true low.

But here’s the problem: If everyone who wanted to sell has already done so, who drives prices lower in Q4? Sure, black swans like recession or quantum computing remain possible—but looking purely at current market structure, buyer/seller positioning, and relative standings of U.S. equities versus crypto, I struggle to identify what force could meaningfully push BTC lower. For me, below $70K is already a zone worthy of risk-taking, DCA, and strategic accumulation.

Another thought I’ve been revisiting: Even if you believe in cycles, the ‘true top’ may not have occurred during BTC’s brief $125K spike last October. Rather, I suspect peak sentiment coincided with ETH’s surge to $5,000 last August—when Tom Lee was aggressively buying and ETH enthusiasm felt far more top-like than BTC’s wick-heavy rejection. If we treat that moment as sentiment’s apex, then we’ve already traversed most of the bear market—making summer a reasonable time to resume risk exposure.

So my core conclusion is simple: Historic fear, no new lows during the Iran war, exhausted marginal sellers, and Saylor’s phoenix-like rebirth of structural demand—together, these factors sustain my bullish stance on BTC.

STRC Investment Thesis Update

Taiki Maeda:

Next, let’s turn to my ongoing tracking of the STRC thesis, which has thus far unfolded almost exactly as anticipated—and I expect it to persist.

I’ve been logging Saylor’s monthly BTC purchases. In March, he bought ~$1.5 billion worth of Bitcoin; in April, another ~$3.4 billion. More importantly, these purchases clustered heavily in the second week of each month. With May just beginning, I anticipate he’ll ramp up buying next week—starting with several hundred million dollars this week, culminating in a larger peak mid-month.

One thing that struck me deeply: If you list Strategy Capital’s largest historical BTC purchase announcements, three of them—January, March, and April—have already occurred this year. Plotting those dates onto BTC’s price chart reveals a stark difference between past and present. Historically—and in the prior bull run—Saylor typically bought aggressively only after BTC had already accelerated sharply and sentiment turned overheated. That was his role. But recently, he’s been buying on dips—a development demanding serious attention.

Rather than focusing solely on price, I prefer watching MSTR’s mNAV. In the past, Saylor typically executed large purchases only when mNAV exceeded 2x—meaning he could sell MSTR’s premium to the market and use proceeds to buy BTC. But his three recent mega-purchases all occurred when mNAV hovered near 1x. In other words, he secured fresh funding and continued buying BTC—even as MSTR traded near par.

What matters most is the underlying reflexive flywheel. Saylor’s repeated announcements of multi-billion-dollar BTC purchases lift Bitcoin’s price. Higher BTC prices boost MSTR’s mNAV, reinforcing shareholder confidence in his leveraged strategy to increase BTC holdings per share. Higher mNAV then facilitates further fundraising, enabling more BTC purchases. Yes, risks exist—but in my view, we’re still in the early innings of this reflexive loop. Rather than betting on apocalypse now, I prefer acknowledging it’s running—and placing a bet it continues.

The STRC mechanism itself is straightforward. If you hold STRC before the ex-dividend date, you earn ~11.5% annualized yield. And as long as STRC trades above $100, Saylor can issue new shares and use proceeds to buy BTC. In essence, he’s accumulating BTC at a dollar-cost basis of ~11.5%. As long as BTC’s appreciation exceeds that hurdle, the model sustains itself.

Certainly, some call this dangerous. Yes, leverage is involved—but danger doesn’t imply imminent failure. Saylor could sell MSTR shares, repurchase and retire some STRC, and de-lever once BTC reaches higher levels. Or he could reduce STRC’s yield—from 11.5% down to 10%—as STRC consistently trades above $101, lowering future risk. To me, STRC’s equilibrium yield sits near 10%; if the Fed cuts rates, that threshold could fall further.

When Saylor tells his ‘digital credit’ story, its most crucial element is its ability to unlock a new class of BTC buyers who otherwise couldn’t access it directly. For example, BlackRock’s preferred stock and income-focused ETFs have already added STRC to significant allocations; VanEck’s similar products assign it meaningful weight. The quip that ‘baby boomers buy it for 11.5% yield’ sounds like a joke—but reality is, once they buy, Saylor gets real money to buy more BTC.

Moreover, anyone truly convinced BTC will fall to $40K or $50K has zero reason to buy STRC. Precisely because of this, STRC demand is, in essence, a subtler expression of BTC long exposure. You may dislike Saylor or doubt STRC’s longevity—but as long as the market buys it with real capital, that deserves respect.

For me, the clearest trading takeaway is: Knowing a single entity will predictably buy billions of dollars in BTC every month’s first half means the simplest path to profit is often just holding BTC itself. How much he’ll buy in May? I don’t know. But as long as STRC stays anchored near $100, I see compelling reasons for BTC to keep rising—not just this month, but next month, and across coming quarters.

One key to profiting in markets is understanding certain things more deeply than others. Over recent months, grasping Stretch’s mechanics proved an exceptionally effective investment strategy—and I believe that opportunity persists as long as Stretch performs well.

Michael Saylor is set to adjust his BTC purchasing strategy. Starting mid-July this year, he plans to split each month’s large BTC purchase into two tranches—one mid-month, one month-end. This reduces predictability, making front-running harder; eventually, he may raise frequency to weekly. Benefits include increased STRC liquidity, reduced volatility, and greater appeal to institutional investors.

Currently, Saylor has found a viable path for STRC’s sustained operation. Leverage usage remains light—but if excessive leverage emerges—e.g., using STRC as collateral to borrow stablecoins or USD, then reinvesting those funds into more STRC, repeating to chase 40% APY—risk would rise sharply. That hasn’t happened yet. So as long as markets maintain caution and avoid aggressive leverage, I remain confident holding BTC and other crypto risk assets.

Over the next two weeks, I expect Saylor to buy billions of dollars in Bitcoin. My forecast isn’t precise—I predicted $2B for April but he bought $3.5B. So this time I’ll conservatively estimate—but I believe this round of purchases could push BTC above $80,000. At that point, I plan to sell part of my position. I’ll detail this in the portfolio section later. Right now I’m long, but I won’t stay that way indefinitely.

Regarding Stretch’s future, some predict ultimate failure—I don’t fully agree. Even if Stretch fails, it could still lift certain tokens along the way. This isn’t binary: Saylor retains options to de-lever or cut yields. I find current market sentiment overly pessimistic—many fixate on collapse triggers like quantum computing or the four-year cycle, ignoring positive catalysts. For instance, digital credit’s success could inspire other DATs to emulate it, triggering a bull market—and ‘green candle therapy.’

Of course, I’m no oracle—I cannot foresee the future. I’m simply someone trying to understand crypto’s reflexivity and flywheel effects—and hoping to share those insights with you.

Escaping the ‘Midcurve Bias’

Taiki Maeda:

Next, I’d like to discuss why I’ve recently begun actively shedding the ‘midcurve bias,’ and share my psychological journey across past crypto cycles.

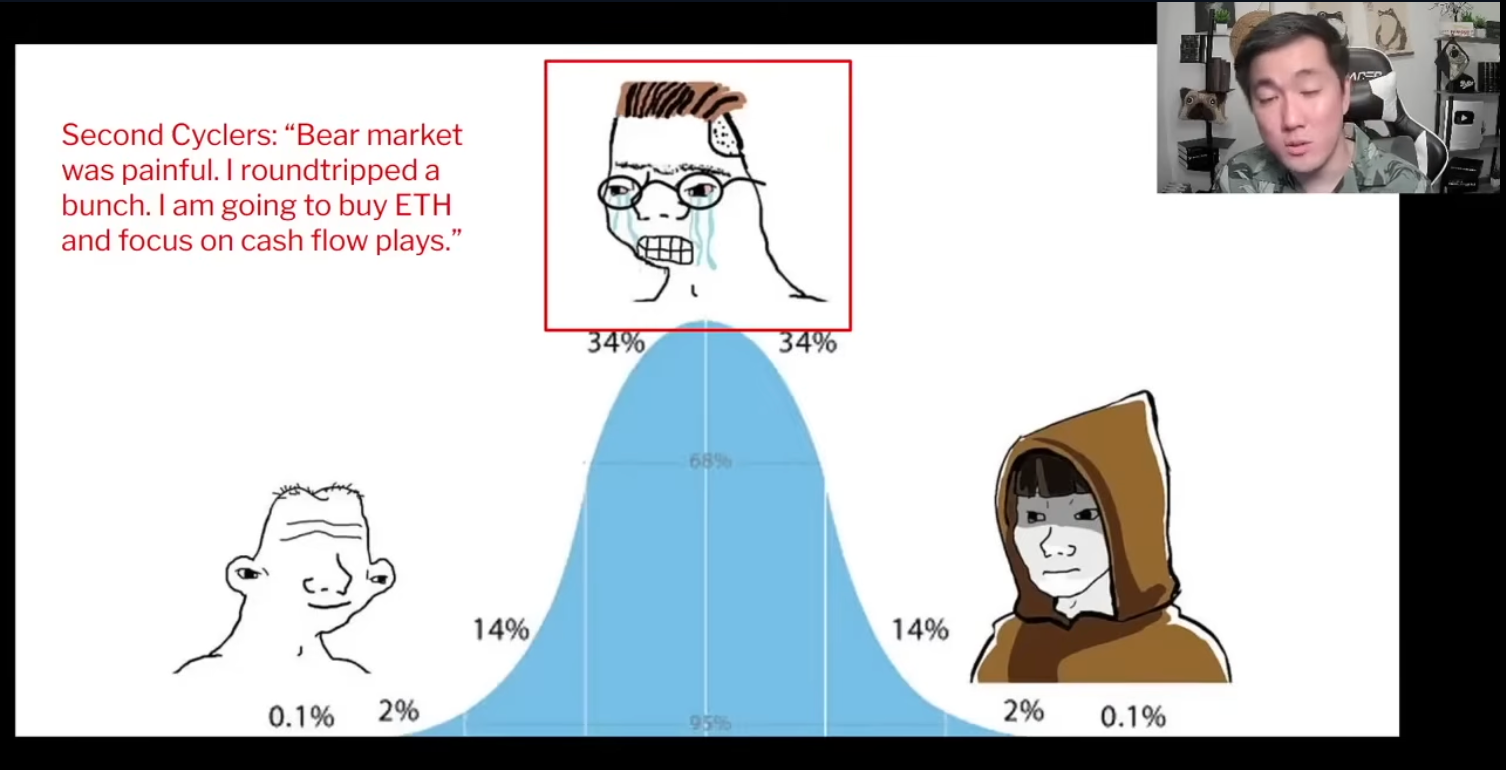

If you’ve lived through multiple crypto cycles, you may resonate with this evolution. In my first cycle, I operated firmly on the left tail—chasing the hottest projects, ignoring risk entirely. My highest-viewed YouTube video at the time taught viewers how to participate in high-yield Polygon projects.

During the 2022 bear market, I sold near the top—but bottom-fished too early, suffering heavy losses. Because of that pain, from 2023 through 2025, I became a textbook midcurve player. I focused obsessively on cash flow—buying ETH, researching DeFi, Uniswap, MakerDAO—and did make money. But looking back, I clearly underperformed.

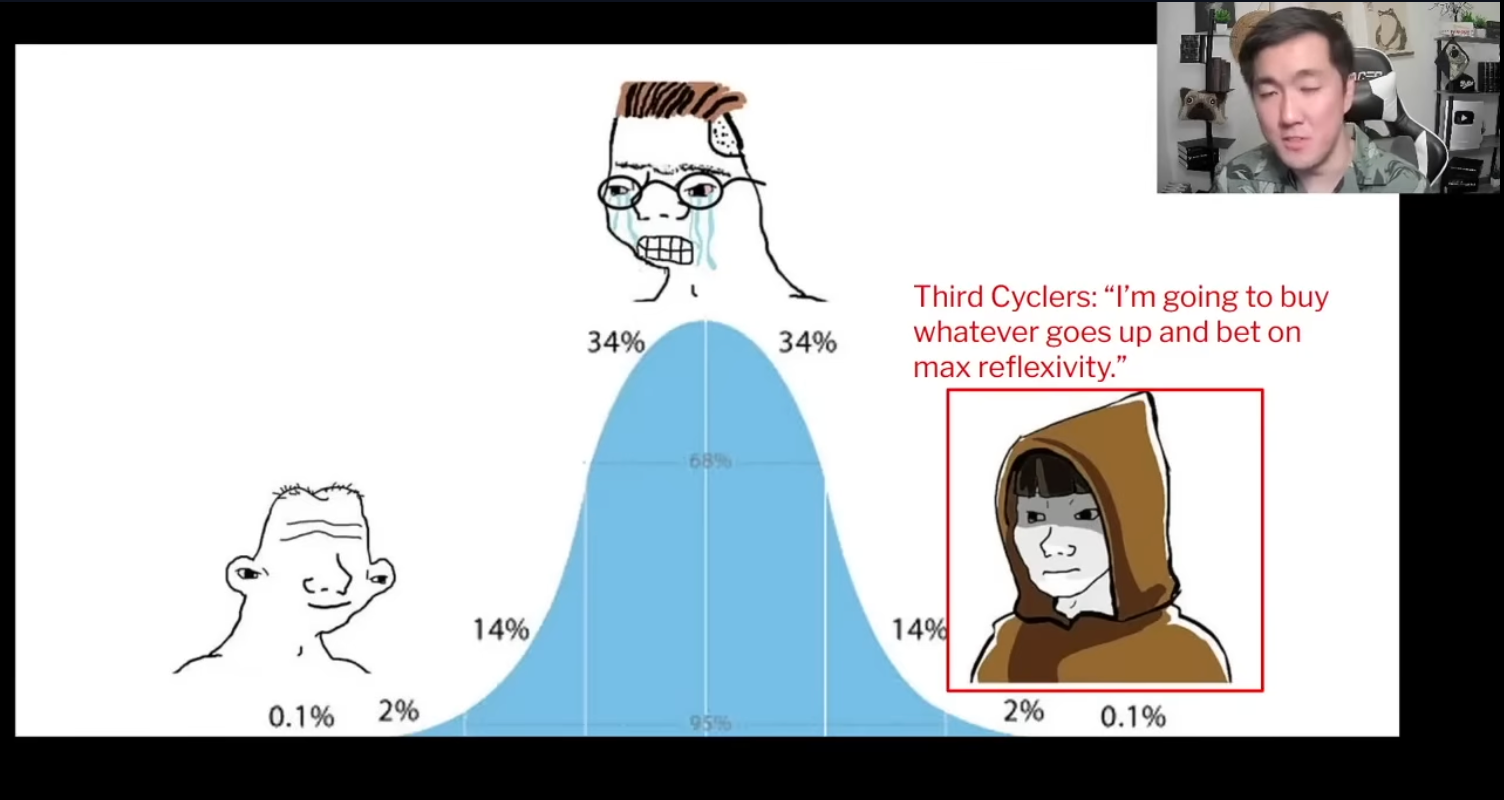

In short: My first cycle was too left; my second, too midcurve. So entering this third cycle, I sought a new framework—blending lessons from both: preserving risk sensitivity without letting bear-market PTSD permanently anchor me in the ‘middle ground.’ If we truly are entering a new bull market, I want to allocate to the most reflexive assets—the ones whose narratives strengthen most as their prices rise.

This doesn’t mean allocating my entire portfolio to the wildest assets—only that I no longer wish to constrain returns through excessive rationality. Markets rarely reward the slickest PPT-maker—they reward those who catch the main uptrend. So this time, I intend to allocate at least a small portion of my portfolio toward maximum reflexivity.

Market Reflexivity and ZEC’s Investment Logic

Taiki Maeda:

Within this framework, I bought some Zcash—not a large position, but I consider it among the most archetypal and intriguing reflexive assets I’ve seen recently.

My definition of reflexivity is simple: Price appreciation strengthens market confidence in an asset’s fundamentals and narrative. Zcash’s history fits this perfectly. For the past nine years, its price has mostly oscillated within a wide band. Yet once it dips below $50, the narrative instantly becomes ‘Who even cares about privacy?’—and once it rallies near $400, the narrative flips to ‘Privacy is a human right—the most vital sector.’ In other words, Zcash’s narratives are often ignited by price itself.

I recall last October, when Balaji, Naval, Mert, and Arthur Hayes almost simultaneously began touting Zcash. My initial reaction was confusion—especially Naval’s line: ‘Bitcoin is insurance against fiat; Zcash is insurance against Bitcoin.’ At the time, I was short alts and ETH, uninterested. But anything that surges suddenly forces a re-examination—so I started researching anew.

Upon review, I conceded it had points impossible to ignore. First, it’s existed nearly nine years—not a VC-packaged project hyped by fleeting narratives. Second, the SEC’s multi-year investigation into the Zcash Foundation concluded with zero enforcement action. Third, Zcash’s Open Development Lab recently raised new funding from a16z, Paradigm, and others. Simultaneously, I observed growing lobbying and advocacy efforts around compliant privacy coins.

Many compare Monero and Zcash, claiming Monero is the ‘purer’ privacy coin. But in my view, such races hinge on social consensus—not technical specs. Like Bitcoin, which isn’t necessarily optimal for daily payments yet dominates as ‘sound money’ due to broader adoption, Zcash could emerge as the ‘compliant privacy coin’—especially if regulatory or legal environments shift. It may yet regain market recognition.

Another angle I can’t fully dismiss is quantum computing. As a major BTC holder, I’m acutely aware of quantum risks—and agree the Bitcoin community appears overly complacent. In that sense, Zcash functions partly as a hedge against Bitcoin. And if price rises first, narratives around privacy and quantum resistance only strengthen—amplifying its reflexivity.

If forced to cite a ‘fundamental,’ I’d point to its shielded pool, which has grown steadily upward. My understanding: You deposit Zcash into the shielded pool, then withdraw from another address—functionally akin to a mixing pool. Larger pools mean bigger anonymity sets and stronger utility. With millions of ZEC already in the pool, it’s clearly not an unused asset reliant solely on price narratives.

Of course, I acknowledge privacy narratives can feel abstract. Zcash lacks BTC’s clear cash-flow anchor or obvious floor/ceiling—so it swings violently. But precisely because of this—and given my substantial BTC and HYPE holdings—I find Zcash ideal as a genuinely ‘left-tail’ portfolio addition.

It shares BTC’s 21-million supply cap and halving schedule; its current market cap is only ~0.5% of BTC’s. So it’s entirely plausible the market begins asking: Why couldn’t Zcash reach 1%, 2%, or more of BTC’s market cap? I don’t know the answer—but I recognize it’s an asset easily carried by price, capable of explosive breakout in a bull market—so I’m willing to allocate a small position.

BTC and Alts

Taiki Maeda:

The first stage of any bear-to-bull transition is BTC leading the charge. I reject the script where Ethereum rockets off immediately upon market bottoming. Restoring industry-wide confidence requires Bitcoin to take the lead. Examining BTC’s market share chart reveals similarities to the prior bottom: a double-bottom formation followed by rising share as BTC climbs. To me, this signals healthy structure—if BTC’s market share climbs toward 60% or even 70%, it suggests a firmer base.

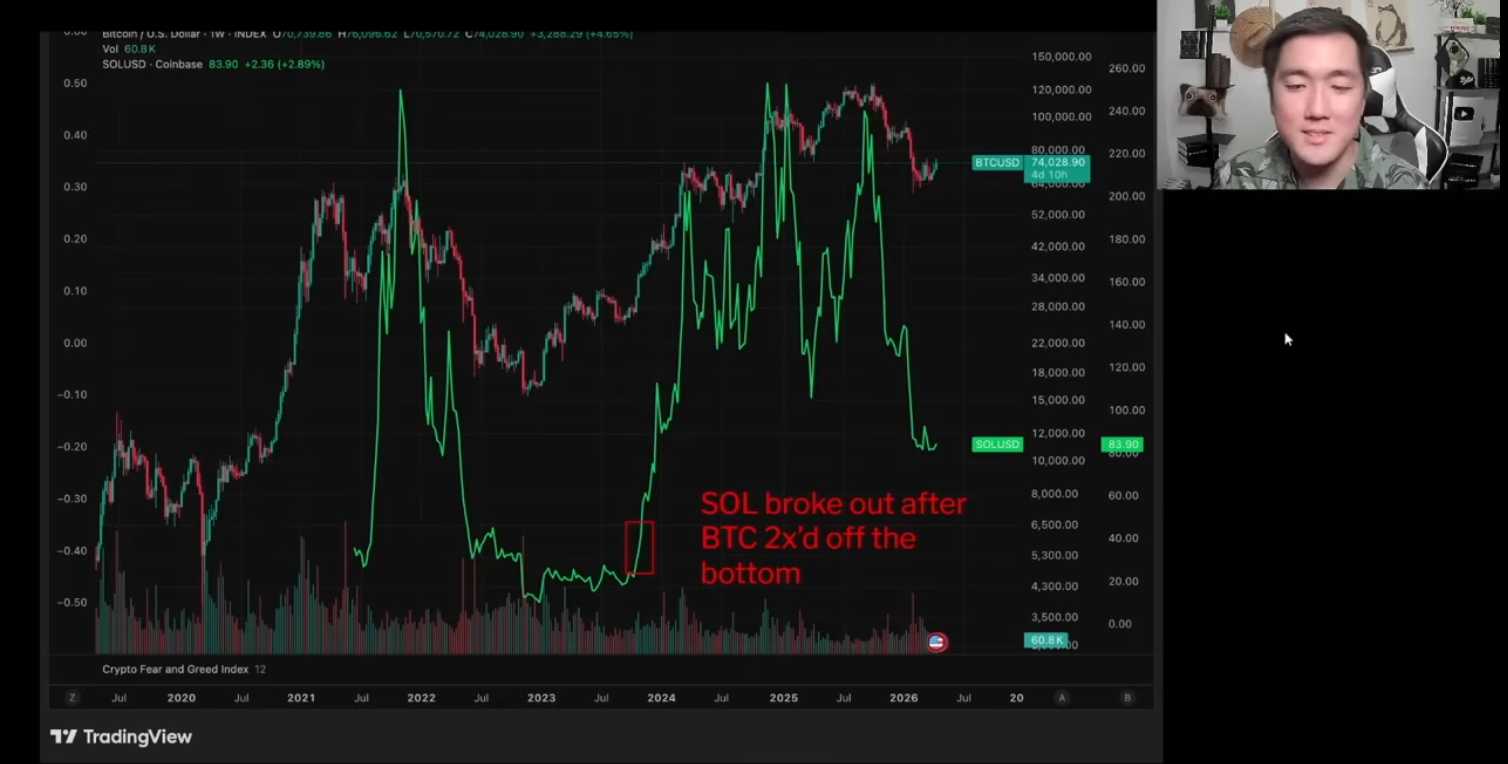

The prior cycle offered clear guidance: In the first stage of bear-to-bull transitions, most alts show little movement—real alpha arrives later in the bull run. Solana exemplifies this: It truly emerged only after BTC rose from $16K to $35K. First, Bitcoin restored confidence and generated wealth effects—then investors chased ‘the next big thing.’

So I prefer focusing energy on BTC now—and waiting for clear signals before deciding which alts merit participation. Perhaps the optimal move then is accepting higher entry prices and rotating BTC profits into higher-beta assets—not pre-emptively stacking uncertain narratives today.

I’ve also pondered whether AI and automation tools could increase hacking incidents. We’ve already seen numerous security breaches. If vulnerabilities, exploits, and code risks become more widespread, complex, execution-heavy crypto narratives may face persistent headwinds. DeFi’s TVL isn’t particularly strong right now—Aave metrics continue declining—which feels personally uncomfortable, given my background covering DeFi.

Yet perhaps the market is signaling something: Narratives like VC tech, Layer-1s, and DeFi aren’t currently the most accessible for capital. By contrast, Bitcoin’s ‘store of value’ story—or Zcash’s ‘privacy’ narrative—is simpler, more direct, and easier for bull markets to embrace quickly. They carry execution risks, yes—but at least investors don’t need to grasp complex mechanisms before understanding why they should buy.

So if you ask me what the market will prioritize next, my answer is: It will prioritize the simplest, most intuitive, and most reflexive narratives first. BTC leads; alt rotation follows.

My Investment Plan and Positioning

Taiki Maeda:

I currently hold substantial BTC spot, plus some perpetual long positions—totaling ~150% long exposure. I also hold some Zcash and HYPE. I’ll likely unwind these BTC perpetual longs over the next one to two months.

Saylor’s purchases cluster in the second week of each month—so I may wait this month, or even the next, to reduce leverage after this structural buying wave concludes. I don’t want to live perpetually monitoring liquidation prices and funding rates.

I increasingly believe investing should target a ‘sleep-quality-adjusted return.’ Holding assets you truly believe in—while sleeping soundly and living comfortably—often proves more sustainable long-term than constant high-stress monitoring. Perhaps only a few times yearly will ‘alt seasons’ erupt—then I’ll act more aggressively. But day-to-day, the priority is researching, building conviction, establishing positions in bear markets—and holding through the rally.

Many assume returns come from frequent trading, but most real money is made by holding appreciating assets—not by incessant churning. Today, I prefer being a comfortable spot holder—not a perpetually leveraged, nerve-wracked trader.

On-chain, I’ve recently been farming Saturn. My logic is straightforward: If STRC’s model grows, an on-chain version is highly probable—and on-chain capital always seeks yield. Tokenizing such assets and looping them in DeFi—with leverage—is almost inevitable. When that happens, the mechanics themselves will further benefit BTC.

So I’m willing to allocate some capital to farming these projects’ points. Of course, they’re not risk-free—and I won’t claim they suit everyone. But over the past six months, few ‘stable yield’ opportunities on-chain have drawn my research attention—whereas these on-chain STRC derivatives rank among the few directions I deem worth exploring.

From a more speculative lens: If these projects launch tokens, they could become the first ‘Saylor-indirectly-endorsed’ on-chain altcoin. Saylor himself frequently discusses STRC-based on-chain stablecoins, risk-layering, and digital credit structures—so I trust others will continue building along this axis. Whether and when they launch tokens is for you to research. I’m participating on both sides: Saturn’s TVL has approached $100M—if it progresses toward $500M, market attention will intensify.

BTC’s ‘God Candle’ and Green Candle Therapy

Taiki Maeda:

Though not religious, I do believe in Bitcoin’s ‘god candle’—and in ‘green candle therapy.’

What I truly mean is: In highly reflexive markets like crypto, just one or two strong green candles can instantly repair investor psychology. Prices rise, confidence returns, risk appetite rebounds, faith in the industry’s future reignites. In essence, this echoes my earlier discussion of reflexivity: Green candles themselves generate new buying pressure.

The industry has suffered deeply from scams and failures—but I remain convinced Bitcoin will lead the market out of the doldrums. As long as you don’t believe BTC will go to zero, its continued ascent alone suffices to restore industry confidence. Moreover, the next top won’t rely solely on Saylor. What truly warrants vigilance is the coming months and years—when more players observe STRC’s effectiveness and replicate it.

Imagine Tom Lee endorsing ‘digital credit’ and launching an ETH staking-yield version—or other DATs copying the playbook across BTC, ETH, SOL. Markets would re-enter a phase where everyone borrows to buy, then uses price gains to fund more borrowing. At that point, you’d likely want to sell into those massive green candles—it would signal dangerous late-stage excess.

Until then, I believe too many focus exclusively on what could go wrong—and neglect what could go right. Shorts sound smarter, especially in bull markets, spinning elegant risk narratives—but reality favors optimists when big money is made. Especially with the Fear & Greed Index dipping below 10, the rational choice isn’t clinging to disaster narratives—but adopting a more constructive lens on the industry.

Real wealth isn’t created in buying and selling—it’s forged in waiting. You profit in bull markets; you grow richer in bear markets. A bear market’s greatest gift is time—to calmly acquire quality assets from those panicking at lows. Once the market recovers, you simply hold and live your life—looking back later to find prices higher.

So my top priority now is avoiding premature panic—preventing bear-market PTSD from hijacking my judgment. I truly believe a new bull market began in February 2026. Today, that may sound radical—but I’m confident future hindsight will show BTC’s $65K price as a pivotal inflection point—prompting many to ask: Why didn’t I buy? Why didn’t I recognize the market had already shifted?

That’s my conclusion. I love the assets I hold—I hope they rise. I believe in green candle therapy—and hope bears keep getting schooled by the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News