Cracks Behind the S&P’s New High: Financial Sector Down 6% Year-to-Date; $2 Trillion Private Credit Undercurrent Spreading

TechFlow Selected TechFlow Selected

Cracks Behind the S&P’s New High: Financial Sector Down 6% Year-to-Date; $2 Trillion Private Credit Undercurrent Spreading

“The U.S. stock market cannot thrive without support from the financial sector, yet financial stocks are currently not even participating in the upward market trend.”

Author: Claude, TechFlow

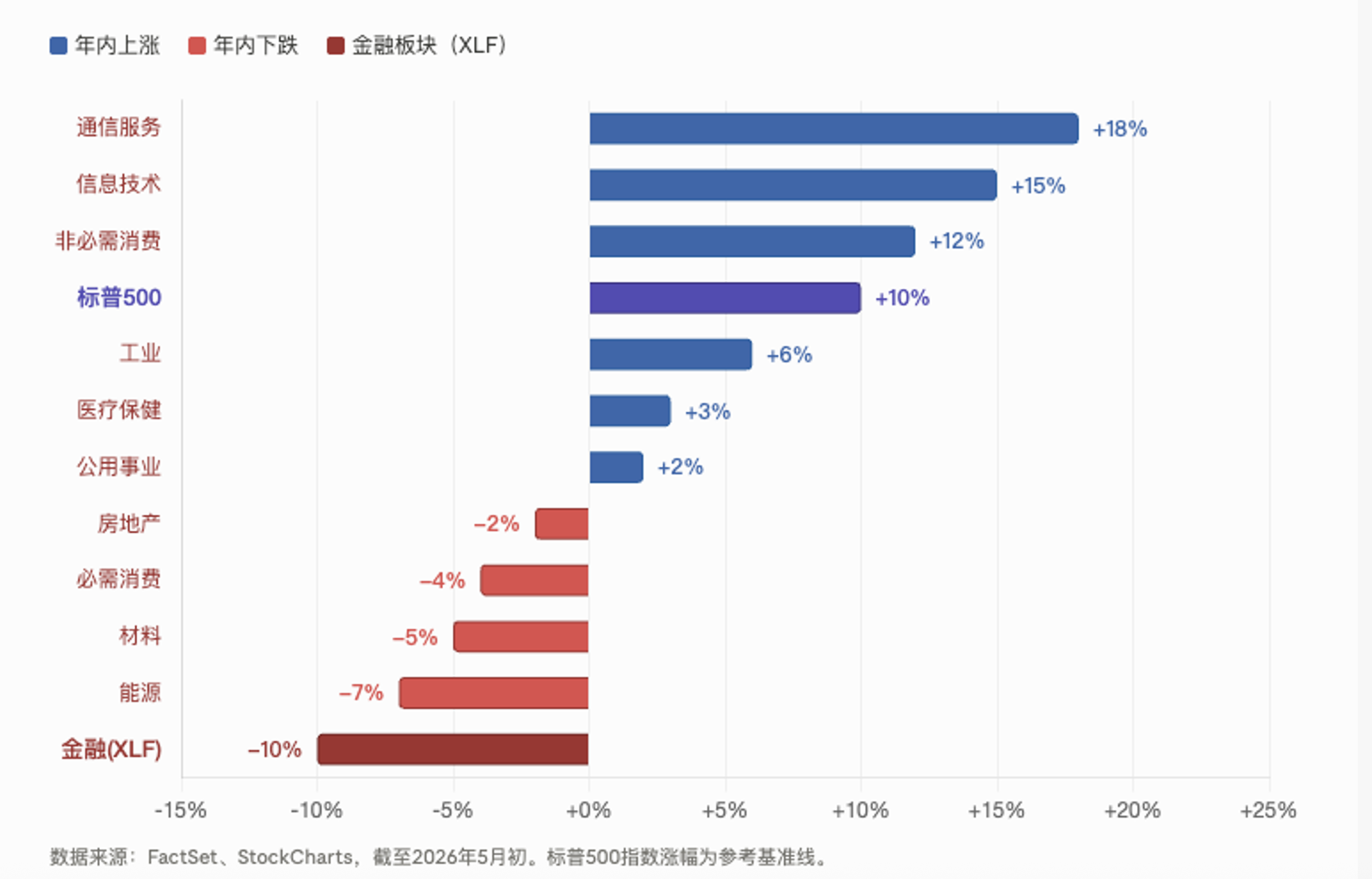

TechFlow Insight: While the S&P 500 hits successive all-time highs and Q1 earnings growth reaches 27.1%, the financial sector has underperformed all 11 sectors—down over 6% year-to-date. The XLF ETF’s relative performance versus the broader index has slumped to its lowest level since its inception in 1998—worse than during both the Global Financial Crisis and the pandemic. Driving this deterioration is the accelerating exposure of cracks in the $2 trillion private credit market: Blackstone’s flagship fund faced a $3.7 billion redemption wave, and just two days ago, the Financial Stability Board (FSB) issued a systemic risk warning.

The S&P 500 closed April at a record high of 7,209 points. Q1 earnings growth hit 27.1%—the strongest since Q4 2021—with 84% of index constituents beating expectations. On the surface, U.S. equities have never looked healthier.

Yet the financial sector is sending a starkly different signal. The XLF ETF—which tracks the sector—is down over 6% year-to-date, the worst performer among all 11 S&P 500 sectors. This divergence is more severe than during either the 2008 Global Financial Crisis or the 2020 pandemic shock. According to FactSet and MarketWatch data, XLF’s relative performance versus the S&P 500 has fallen to its lowest level since the ETF’s launch in 1998.

Scott Brown, founder of Brown Technical Insights, states bluntly: “The U.S. equity market cannot sustain itself without support from the financial sector—and right now, financial stocks aren’t even participating in the rally.”

Banks’ Profits Hit Records—While the Sector Hits Lows

This weakness in the financial sector is especially counterintuitive.

Per FactSet data released May 1, S&P 500 Q1 earnings growth reached 27.1%—the highest since Q4 2021—and financials ranked among the top four sectors by revenue growth. Major banks—including JPMorgan Chase, Bank of America, and Wells Fargo—reported robust quarterly results in April.

Yet markets are not pricing current-quarter income statements—but rather off-balance-sheet risk exposures that remain invisible on financial statements.

The root cause lies in private credit. This roughly $1.5–$2 trillion market expanded rapidly after the 2008 crisis, filling the lending vacuum left by retreating banks. It is now deeply interwoven with banks, insurers, and asset managers. Once credit quality deteriorates, the transmission chain will extend far beyond what appears on the surface.

$2 Trillion in Private Credit: From “Cockroaches” to Systemic Warnings

Jamie Dimon, CEO of JPMorgan Chase, previously likened emerging issues in private credit to “cockroaches”: spotting one implies many more are lurking nearby. That analogy is increasingly supported by data.

On May 6, the Financial Stability Board (FSB) released a strongly worded report on private credit risks, warning that the market’s complexity, high leverage, and deep interconnections with the banking system could amplify stress under adverse scenarios—posing risks to broader financial stability. The FSB specifically highlighted that private credit’s high leverage is concentrated in technology, healthcare, and services—and has never been tested through a prolonged economic downturn.

The report also flagged an ominous signal: an increasing number of private credit borrowers are resorting to payment-in-kind (PIK) loans—using new debt to repay old debt instead of cash—a widely recognized indicator of deteriorating credit conditions.

Two days earlier, Sarah Breeden, Deputy Governor of the Bank of England, publicly voiced concerns about asset quality, valuation discipline, and liquidity in private credit. The European Central Bank has recently issued similar warnings. Barclays disclosed $20 billion in private credit exposure; Deutsche Bank’s stands at approximately $30 billion.

Blackstone’s Flagship Fund Faces $3.7 Billion Redemption Wave—A Clear Signal of Retail Retreat

Beyond macro-level warnings, funding-level turbulence is even more immediate.

According to a Reuters report dated March 3, Blackstone’s $82 billion flagship private credit fund, BCRED, received $3.7 billion in redemption requests during Q1—equivalent to 7.9% of fund assets—the highest rate since the fund’s inception. JPMorgan analysts labeled this BCRED’s first-ever net outflow, calling it “a major expression of sharply deteriorating investor sentiment toward direct lending.” To meet full redemption demands, Blackstone raised its standard 5% redemption cap to 7% and injected $400 million of its own capital—alongside contributions from senior executives.

The day after the news broke, Blackstone’s stock plunged nearly 8% to a two-year low.

Another private credit giant, Blue Owl Capital, faces an even more precarious situation. Its flagship fund OCIC received redemption requests totaling 21.9% in Q1—but honored only 5% of those requests pro rata, meaning roughly three-quarters went unfulfilled. Its tech-focused fund OTIC saw redemption requests of 17% in the prior quarter.

Investment bank RA Stanger delivered a particularly striking assessment: alternative assets are entering a “sharp U-turn” phase, with capital fleeing private credit. It forecasts Business Development Company (BDC) capital formation will decline ~40% year-on-year in 2026.

A PitchBook survey of ~100 credit firms found that 35% of respondents cited negative perception of private credit as the industry’s biggest headwind—signaling markedly deteriorated sentiment compared to six months earlier. Morgan Stanley forecasts private credit default rates will rise to 8%, with roughly 20% of loans extended to software companies—assets whose outlook is especially bleak amid AI-driven disruption.

Technical Signals: A 90% Historical Probability of Correction

Turning to technical indicators for the financial sector itself, signals are similarly bearish.

Scott Brown notes that XLF has not only declined while the S&P 500 hit new highs—it has remained persistently below its 200-day moving average. Historical data shows that in the previous 32 instances where the S&P 500 made a new high while XLF traded below its 200-day MA, the S&P 500 fell within one month in 29 cases—averaging a 3.3% decline. Over six months, outcomes were closer to a coin toss—but the maximum drawdown observed was as high as 41.5%, underscoring asymmetric tail risk.

Among all 11 SPDR sector ETFs tracking the S&P 500, XLF is currently the only one whose price and 50-day moving average both sit below its 200-day moving average—indicating weakness across both short- and long-term trends.

Historically, the financial sector has twice signaled market tops ahead of the broader index. In April 1999, XLF’s relative performance versus the S&P 500 began weakening—roughly 11 months before the S&P 500 peaked. In February 2007, XLF again flashed an early warning—about eight months before the market’s peak.

The Year-Start “Trump Rally” Expectation Has Fully Unraveled

At the start of the year, the financial sector was widely expected to outperform. Markets broadly anticipated that a second Trump administration would bring lower interest rates and looser regulation—creating favorable conditions for banks, insurers, and asset managers.

But according to an Investing.com report from early April, the opposite has occurred. Over a year into Trump’s second term, the financial sector is the worst-performing S&P 500 sector. Failed rate-cut expectations, the surfacing of private credit landmines, and Middle East conflict-driven oil price and inflation pressures have converged into a perfect storm of headwinds.

Melissa Brown, Global Head of Investment Decision Research at SimCorp, observes that the financial system is highly interconnected—and risks emanating from private credit could spread more widely than currently anticipated.

Scott Brown’s recommendation is caution—not aggression. While identifying market tops remains difficult, investors may consider gradually reducing exposure rather than chasing further gains—and certainly avoid deploying fresh capital into the market.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News