OpenAI’s Smartphone Venture: A Lifeline for a Money-Losing Company—or Another AI Hardware Graveyard?

TechFlow Selected TechFlow Selected

OpenAI’s Smartphone Venture: A Lifeline for a Money-Losing Company—or Another AI Hardware Graveyard?

The most likely outcome is not redefining the smartphone industry, but adding one more slide to the IPO roadshow PPT.

Author: Ada, TechFlow

Ming-Chi Kuo, an analyst at TF International Securities, posted a message stating that OpenAI is collaborating with MediaTek and Qualcomm to develop smartphone processors, with Luxshare-ICT serving as the exclusive manufacturing partner. Mass production is expected in 2028. This news has been confirmed and reported by multiple media outlets.

Upon the announcement, supply-chain stocks surged immediately. Analysts began calculating MediaTek’s incremental orders, Luxshare-ICT’s improved customer mix, and Qualcomm’s baseband licensing revenue.

But here lies the question: Why would a company projected to achieve profitability only by 2030—and potentially burn through nearly $115 billion in cumulative cash—enter the smartphone business?

The Subscription-Model Trap

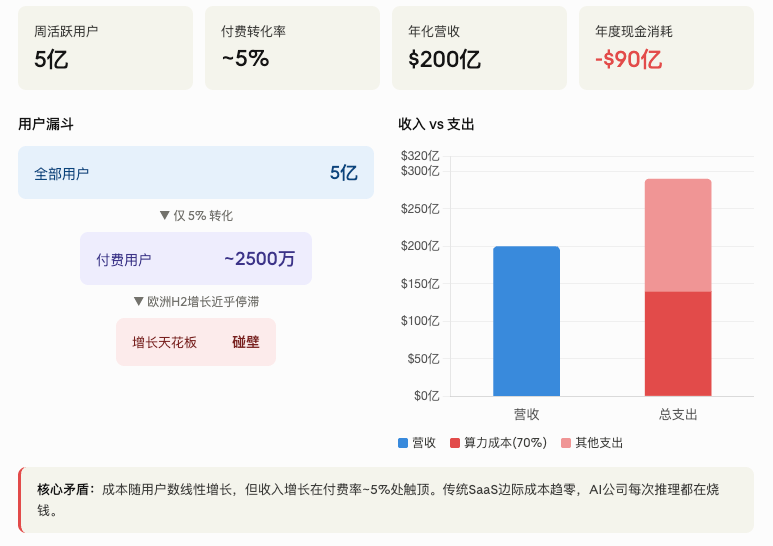

OpenAI achieved $20 billion in annual recurring revenue (ARR) in 2025—a 3,628-fold increase since 2020. ChatGPT boasts 500 million weekly active users, placing it among the world’s top-tier consumer internet products.

Yet according to Deutsche Bank’s October 2025 report, only about 5% of users actually pay.

The remaining 95% are free users—each interaction burning compute, electricity, and GPU resources. Even Sam Altman has acknowledged that the $200/month Pro subscription remains unprofitable. In 2025 alone, OpenAI burned approximately $9 billion in cash, with 70% of its revenue vanishing directly into server costs.

Moreover, per Deutsche Bank analyst Adrian Cox’s report, ChatGPT’s consumer-paid user growth in Europe stalled almost entirely in the second half of 2025. The ceiling for paid conversion may be far lower than anticipated, signaling that subscription-driven growth is hitting a wall.

The core problem with the subscription model is this: while costs scale linearly with user count, revenue growth inevitably plateaus. This isn’t a concern for traditional SaaS—but for AI companies, it’s fatal.

So what’s the alternative?

Advertising is one path. OpenAI has already begun testing ads within ChatGPT and recruited Meta’s monetization veteran Fidji Simo as CEO of its apps division. Yet advertising means head-to-head competition with Google, which generates over $100 billion annually in search ad cash flow—and possesses a formidable moat. OpenAI is unlikely to wrest meaningful share from such a rival.

Enterprise services represent another path. Enterprise revenue already accounts for over 40% of OpenAI’s total revenue—and is growing rapidly. But Anthropic’s annualized revenue from enterprise coding tools reached $30 billion as of March 2026, briefly pushing its secondary-market valuation above OpenAI’s. This path, too, is crowded.

That leaves only the third path: hardware.

Hardware Isn’t a Dream—It’s Financial Anxiety

OpenAI CFO Sarah Friar told CNBC: “Hardware will become the next layer of value creation for ChatGPT—and help drive user upgrades and subscription growth.”

In other words, OpenAI needs a vehicle to convert free users into paying ones. Sell a phone bundled with a ChatGPT subscription, and charge users automatically each month—no need to wait for them to manually upgrade via browser. Hardware locks in the entry point; subscriptions become the default option—just like how iPhones bundle iCloud storage.

So while Ming-Chi Kuo’s vision—redefining smartphones using AI Agents, where users execute tasks directly instead of opening dozens of apps—makes for compelling technical storytelling, the underlying driver is far more primal: OpenAI needs a new monetization channel to plug its ~$10 billion annual cash gap.

OpenAI’s fundamental motivation for building phones has nothing to do with innovation. It needs a way to shift compute costs off its own balance sheet—and hardware serves precisely as that conduit. When users buy the phone, they implicitly prepay for cloud inference.

OpenAI aims to go public as early as Q4 2026, targeting a $1 trillion valuation. Before listing, it must deliver Wall Street a growth narrative beyond “models keep getting better.” Enterprise revenue is being chased down by Anthropic; advertising is still nascent; AI Agents remain conceptual. A smartphone is a compelling story. With over a billion units sold globally each year, even capturing a sliver could dramatically reshape its revenue curve.

Lessons from the Past

The gulf between a good story and a good business has been repeatedly demonstrated in the AI hardware space.

The Humane AI Pin raised $230 million, launched at $699 plus a $24/month subscription, and shipped fewer than 10,000 units. In February 2025, it was acquired by HP for $116 million—after which the device was bricked, rendering all user units inoperable.

The Rabbit R1, hailed as CES’s breakout “little orange box,” sold 100,000 units before facing mass returns. Users discovered many demoed features didn’t work reliably—and voice response latency stretched up to 10 seconds, making real-time interaction impossible. By early 2026, reports emerged that the company struggled to pay employee salaries. Users also realized the device was essentially just an Android app wrapped in custom hardware.

Both cases shared a fatal flaw: mistaking technological novelty for product-market fit. Demos dazzled; waitlists ballooned; teams assumed this signaled market validation. In reality, users found the experience inferior to simply installing the ChatGPT app on their phones.

Jony Ive himself publicly labeled both the Humane AI Pin and Rabbit R1 “terrible products” and criticized the industry for lacking “products expressed with fresh thinking.” He then sold his startup io to OpenAI for $6.5 billion.

By 2028, the Competition Won’t Be Today’s iPhone

OpenAI’s smartphone is slated for mass production in 2028—just two years away.

What will the smartphone market look like then?

Apple has already integrated both Google Gemini and ChatGPT into the iPhone; Siri’s major AI overhaul is expected in 2026. Samsung’s Galaxy AI now spans flagship and mid-tier devices. Google Pixel natively runs Gemini, and Android XR glasses are underway.

In short, by 2028, every mainstream smartphone will be an “AI phone.” AI capability will be as standard as cameras, GPS, or fingerprint sensors.

So where does OpenAI differentiate?

Kuo’s answer: AI Agents require continuous contextual understanding—and only smartphones possess users’ full, real-time state information. Combined with OpenAI’s best-in-class models, this yields a uniquely superior experience.

This reasoning contains a glaring flaw: model capabilities can be delivered via API. OpenAI already sells its models to Apple and Samsung through APIs. If model quality is the core advantage, licensing models to all handset makers would generate higher revenue—and carry far less risk—than building phones itself.

Unless OpenAI believes API licensing revenue alone is insufficient.

Which brings us back to the central question: Is building phones driven by technological idealism—or financial survival?

Tech history is littered with hardware failures—and historically, software companies venturing into hardware have succeeded only rarely. Google spent a decade on Pixel, capturing under 2% global share. Microsoft operated Surface at a loss for years before barely breaking even. Both had hundreds of billions in cash reserves to absorb missteps. OpenAI does not.

An $85.2 Billion Bet

OpenAI’s smartphone narrative, at its core, reflects the storytelling demands of an $85.2 billion valuation.

Model capabilities are converging; lead time for new models may shrink to mere months, as Gemini, Claude, and Llama close the gap. Once models become commodities, margins from model sales will only narrow.

Meanwhile, subscription revenue is plateauing—the 5% paid conversion rate reveals the market’s true willingness to pay. The enterprise segment is also being eroded by Anthropic. On secondary markets, Anthropic’s trading price has already surpassed OpenAI’s—investors voting with their feet.

In this context, “building phones” offers investors a fresh narrative. If OpenAI sells 100 million AI phones, each bundled with a $20/month subscription, that’s $2.4 billion in annual recurring revenue—plus hardware revenue—doubling total revenue overnight.

The math is simple. So was the math behind Humane and Rabbit—beautiful on paper, disastrous in practice. Consumers won’t pay for a phone lacking an app ecosystem: no WeChat, no TikTok, no Google Play. No matter how powerful the AI Agent, it cannot fulfill everyday needs.

Kuo notes OpenAI may adopt a subscription-hardware bundling model—selling hardware at a loss and recouping costs through subscriptions. Another “lose first, profit later” story. OpenAI has told this story for three years—and investors have listened for three years.

But how long will the story hold when phones launch in 2028? By then, OpenAI will have burned over $100 billion. If sales falter, the flywheel won’t spin—it’ll reverse.

CFO Sarah Friar has already voiced doubts about OpenAI’s IPO timeline, stating the company isn’t ready—and expressing reservations about its proposed $60 billion annual expenditure plan over the next five years. According to Bloomberg, a survey firm that contacted hundreds of institutions found “not a single one willing to buy OpenAI shares on the secondary market.”

OpenAI’s smartphone venture is most likely to end not with the redefinition of the smartphone industry—but with an extra slide in its IPO roadshow deck. How much of that slide ultimately materializes may hinge on factors entirely outside OpenAI’s control.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News