You Can Buy OpenAI Stock for Just $500—the Most Respectable “Bag Holder” Invitation from Silicon Valley

TechFlow Selected TechFlow Selected

You Can Buy OpenAI Stock for Just $500—the Most Respectable “Bag Holder” Invitation from Silicon Valley

AngelList, Silicon Valley’s largest venture capital platform, is packaging “inclusive finance” as a channel for retail investors to absorb losses?

Author: David, TechFlow

When venture capitalists in Silicon Valley finally invite ordinary people to the table, it usually signals one thing:

The game is nearly over.

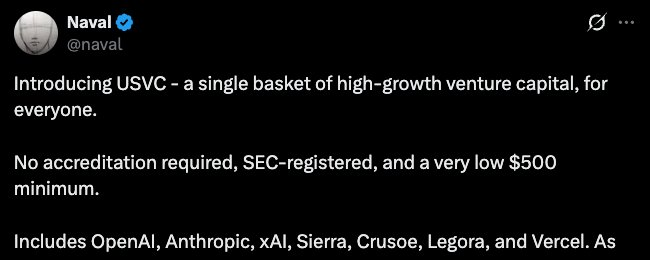

Yesterday, AngelList launched a fund product called USVC. AngelList is Silicon Valley’s largest venture infrastructure platform; according to its official website, it manages over $125 billion in assets and has served more than 25,000 funds.

Now it’s effectively opening a door to all U.S. investors—starting at just $500, with no accredited investor requirement—granting direct exposure to equity stakes in seven AI companies, including OpenAI, Anthropic, and xAI.

Naval Ravikant, AngelList’s co-founder, is endorsing the product. His book, The Almanack of Naval Ravikant, has made him one of the rare figures in Silicon Valley who combines proven investment performance with broad public influence.

On X, he published a lengthy post promoting USVC, arguing that early-stage tech investing is today’s “adventure capital,” long inaccessible to ordinary people—and by the time powerful AI companies go public, their explosive growth phase is already over. USVC aims to open that door.

Within hours of the post going live, commenters began asking an uncomfortable question:

These tech firms’ valuations have already soared into the stratosphere; all their explosive growth happens in the private markets. So what’s the difference between inviting retail investors in now and simply providing exit liquidity?

USVC holds stakes in seven companies, with its largest position in xAI. According to Decrypt, as of end-March, roughly 44% of USVC’s capital had already been deployed across these seven companies.

Yet none of these companies are publicly listed—so where do these shares come from?

Per the fund’s prospectus, USVC acquires positions through three channels: investing in emerging fund managers, participating in growth-stage financing rounds, and purchasing secondary shares via AngelList’s network.

The first two are straightforward—the third is key.

“Secondary shares” means the company itself does not issue new shares to you; instead, existing shareholders transfer their stakes to you. Who’s selling? Early angel investors, VC funds, and early employees.

These sellers likely entered when the company was valued at just a few million dollars. Now, with valuations in the tens or even hundreds of billions, they want to convert paper gains into real cash before IPO—but unlike public stock exchanges, the private market lacks a ready queue of buyers.

USVC solves precisely this problem: it raises capital from retail investors and uses those funds to buy shares from insiders eager to exit.

AngelList is uniquely positioned for this. Its website states that over 4,500 active fund managers operate more than 25,000 funds on its platform, having invested in over 13,000 startups.

This vast network contains abundant sellers—and abundant shares to sell. AngelList sits squarely at the center. This is the “exclusive channel” USVC repeatedly highlights.

The channel is indeed exclusive—but the transaction flow doesn’t favor retail investors.

In this trade, sellers got in when valuations were in the low millions; buyers are entering when valuations sit in the hundreds of billions. Sellers lock in returns of dozens—or even hundreds—of times their initial investment. Buyers are betting these already-richly-priced companies still have significant upside.

Meanwhile, the terms offered to retail investors raise further questions.

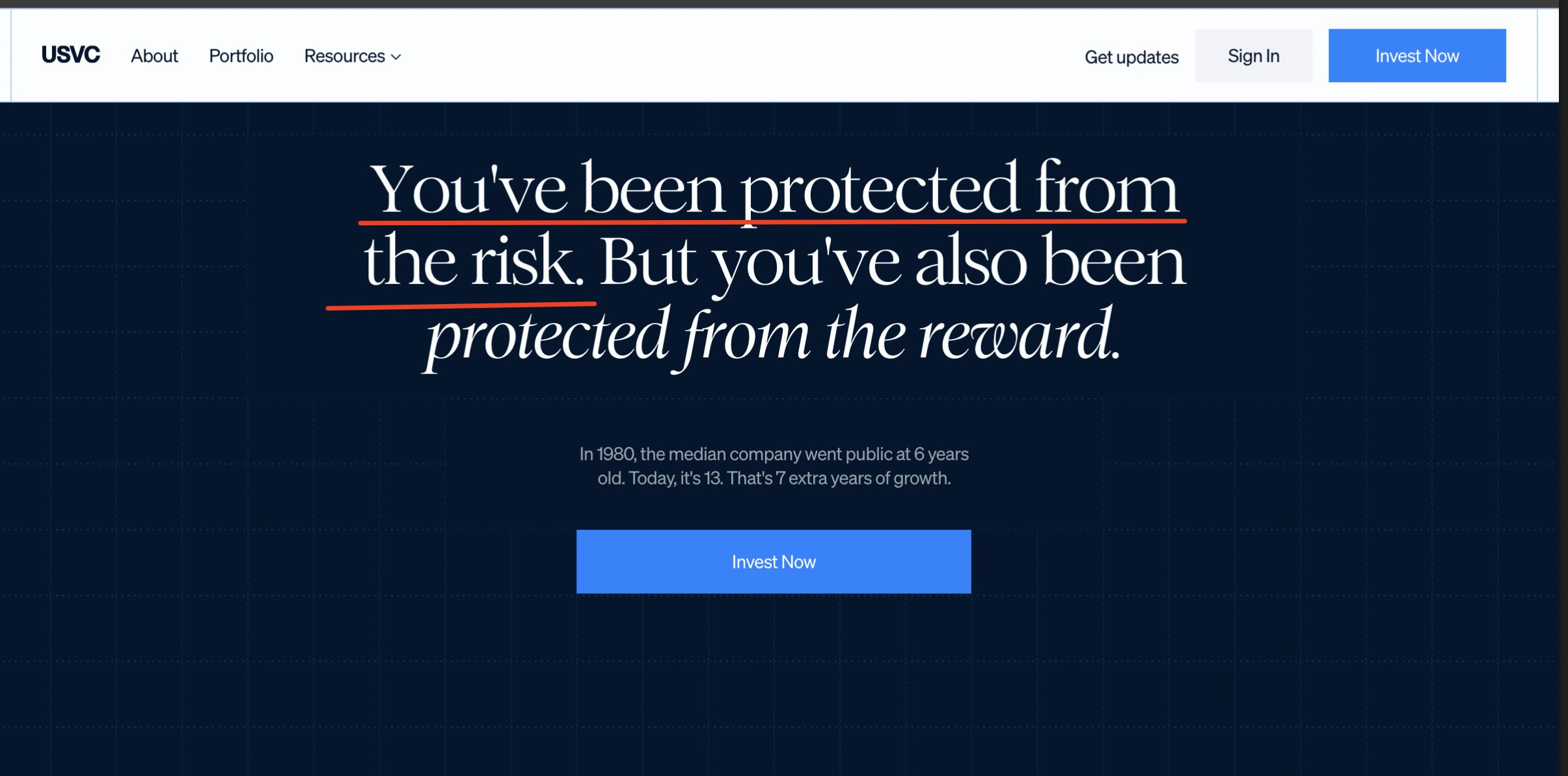

According to the USVC prospectus, the fund is not listed on any exchange, and no secondary trading market is expected. It may repurchase up to 5% of net asset value per quarter—entirely at the board’s discretion, with no guarantee. Additionally, the estimated annualized total expense ratio is 3.61%, far exceeding the prominently advertised 1% management fee—the difference stems from layered fees embedded in underlying funds.

You can’t sell freely, and exits depend on a queue—while annual fees alone will erode nearly 4% of your principal. For a $500-minimum product targeted at ordinary people, that’s not cheap.

So the full picture may look like this:

On one side, insiders seeking exit secure liquidity and lock in gains. On the other, newly arrived retail investors receive illiquid stakes, face queue-based redemptions, and bear effective fees far above the headline rate. Capital flows unidirectionally—from later entrants to earlier ones.

A Stock-Market Version of “Low Circulating Supply, High FDV”

Breaking down USVC’s model: insiders accumulate positions at low valuations; after asset prices surge, a retail-accessible vehicle packages those stakes so later entrants’ capital absorbs insiders’ exits.

This logic was exhaustively rehearsed across the crypto industry between 2021 and 2024.

During those years, VC-backed token projects followed a standard template: seed round valuations in the low millions, private rounds rising into the tens of millions—and by the time tokens hit exchanges, fully diluted valuations (FDVs) had ballooned to several billion, even tens of billions. Yet only 2–5% of total supply entered circulation; the rest remained locked in VC and team hands, unlocking gradually per vesting schedules.

Low circulating supply. High FDV.

What USVC does is, in essence, identical to low-circulation, high-FDV dynamics: insiders enter at multi-million-dollar valuations; after valuations climb into the hundreds of billions, they offload stakes via a retail-facing product.

Naval’s own trajectory is also telling. Last October, he tweeted: “Bitcoin is insurance against fiat; Zcash is insurance against Bitcoin.” That tweet sent ZEC surging over 100% in a week. Soon after, the community uncovered public reports showing Naval had invested $715,000 in Zcash’s development company back in 2015—and even served on the Zcash Foundation’s board.

The community’s conclusion was simple: he was using his personal influence to pump his own early investment. Naval did not respond to these allegations.

From Zcash to USVC, the model hasn’t changed. A celebrity leverages public credibility to generate demand, then channels that demand toward assets in which they hold early positions.

Of course, nothing about USVC appears illegal.

USVC is a registered fund; its prospectus includes thorough risk disclosures. Naval’s Zcash tweet did not constitute securities advice.

Yet legality and reasonableness often occupy an ambiguous gray zone. A platform managing a trillion-dollar venture ecosystem frames its narrative around “enabling ordinary people to invest in the future,” then uses the raised retail capital to absorb exits from insiders within its own network…

Every step complies with regulations. But taken together, the entire sequence easily triggers painful memories among merchants.

And on the very same day USVC launched, Robinhood announced its fund had purchased $75 million worth of OpenAI shares—also made available to ordinary investors. Two firms, in the same week, built exit conduits for private-market insiders using their respective retail investor networks.

Each time the financial industry suddenly champions ordinary investors’ rights, it’s rarely because their circumstances have improved—but rather because insiders’ exit paths have narrowed.

This held true when crypto opened its doors to retail in 2021—and it holds true again as Silicon Valley opens its doors in 2026. The timing of the door’s opening has never been decided by those waiting to walk through it.

For ordinary people, there’s a simple way to assess whether an investment opportunity is truly meant for you:

Look at those who entered before you—are they buying more, or selling? If they’re selling—and you’re being invited to buy—you must ask yourself one critical question: Are you bringing capital—or liquidity?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News