IOSG Weekly Brief | $PUMP Valuation Breakdown: On-Chain Data Debunks “Volume Inflation” Claims—Where Does the Real Discount Come From?

TechFlow Selected TechFlow Selected

IOSG Weekly Brief | $PUMP Valuation Breakdown: On-Chain Data Debunks “Volume Inflation” Claims—Where Does the Real Discount Come From?

The discount stems from three factors: market skepticism regarding revenue sustainability, lack of institutional coverage, and an absence of established management credibility.

Author| Max Wong @IOSG

Introduction

Pump.fun launched in early 2024 as a permissionless meme launchpad on Solana, enabling anyone to create and trade tokens in seconds via a bonding curve mechanism. Initially a niche experiment, it quickly became one of the highest-revenue applications on public blockchains.

Between 2024 and 2025, Pump.fun’s daily protocol revenue consistently matched—and at times surpassed—that of Hyperliquid, despite operating in the inherently cyclical meme market—a fact that makes this performance especially noteworthy. Its native token, $PUMP, was issued via a $600 million ICO at $0.004, with an FDV of $4 billion.

Over the past several months, protocol revenue hit an all-time high and the token’s value doubled—but $PUMP is currently trading at ~$0.0019, down ~80% from its all-time high of $0.086 (corresponding to an FDV of $8.6 billion). Its current market cap stands at ~$679 million, with an FDV of $1.9 billion. The gap between revenue trends and valuation is stark.

This report traces Pump.fun’s product evolution and ecosystem strategy, stress-tests whether its revenue contains artificial inflation, and assesses whether its current valuation reflects mispricing—or a rational discount for real underlying risks.

Product Suite

Pump.fun is no longer just a launchpad. Starting in late 2024, it began expanding into adjacent businesses—broadening revenue streams and deepening control over onchain speculative traffic.

Launchpad (Core Product)

The original product—and the foundation of brand recognition. Anyone can deploy a token upon paying a small fee.

PumpSwap

PumpSwap is Pump.fun’s in-house AMM DEX, launched in March 2025 with a clear objective: recapture “graduation fees” previously flowing to Raydium (which charges 6 SOL per graduating token). As of May 2025, the fee structure was updated: the protocol takes 0.05% per trade, LPs receive 0.20%, and token issuers receive 0.05%.

Features include: free liquidity pool creation for any token, liquidity provision into existing pools, and trading of all tokens listed on PumpSwap.

Padre / Pump Terminal

Padre, acquired by Pump.fun and rebranded as Terminal, positions itself as a professional trading terminal supporting Solana, BNB, Base, and Ethereum.

Its features mirror those of comparable terminals: Trenches (to monitor newly migrated or soon-to-migrate tokens), customizable UI, sniping and instant buy functionality, multi-wallet strategies, and bundle detection.

Pumplive

Pumplive is an in-platform live-streaming feature where streamers can link a token to their broadcast.

The logic follows a “publisher-as-exchange” model—similar to Parti and Kick/stake.com: streamers benefit from increased trading volume, as they earn a share of total fees; token holders benefit from higher volume and buying pressure. The more a streamer broadcasts, the more active the token becomes—and the higher the trading volume.

Ecosystem Initiatives

Since its Token Generation Event (TGE), Pump.fun has held ~$1 billion in cash reserves, continuously launching new product lines (e.g., the acquisition of Padre) while executing several key initiatives:

Pumpfund

A $3 million “Build in Public” (BiP) hackathon launched on January 19, 2026. Using a $10 million valuation benchmark, it awarded $250,000 each to 12 projects. Selection prioritized market-driven, public-attention-oriented criteria—not traditional VC-style due diligence.

Glass Full Foundation (GFF)

Launched in August 2025, GFF is a liquidity injection program. Through five transparent wallets, it deployed ~$1.7 million (~2,022 SOL) across ten tokens—including Tokabu (21.3%), House (20.6%), USDUC, NEET, MASK, and FART—with selection favoring projects demonstrating strong community engagement.

Project Ascend

A creator incentive program launched in 2025, centered on dynamically tiered creator fees (ranging from 0.95% to 0.05%). Its dual goals are to increase creator earnings tenfold and accelerate CTO (Community Takeover) application processing.

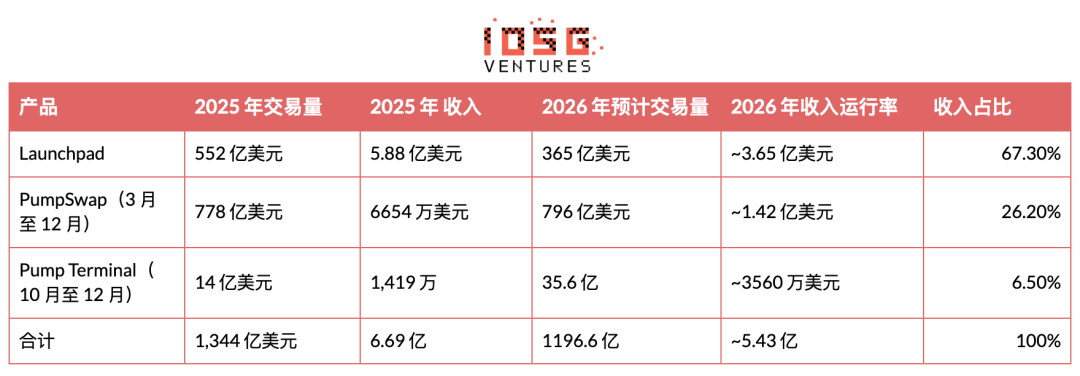

Consolidated Metrics (All Products)

The table below summarizes performance across all three product lines. 2025 figures reflect actuals; 2026 figures represent projected run rates.

Currently, ~32.7% of total revenue originates from non-Launchpad products—early evidence that revenue diversification is already bearing fruit.

Currently, ~32.7% of the platform’s total revenue comes from non-Launchpad products—clearly indicating initial success in diversifying revenue sources and pursuing growth beyond its core offering.

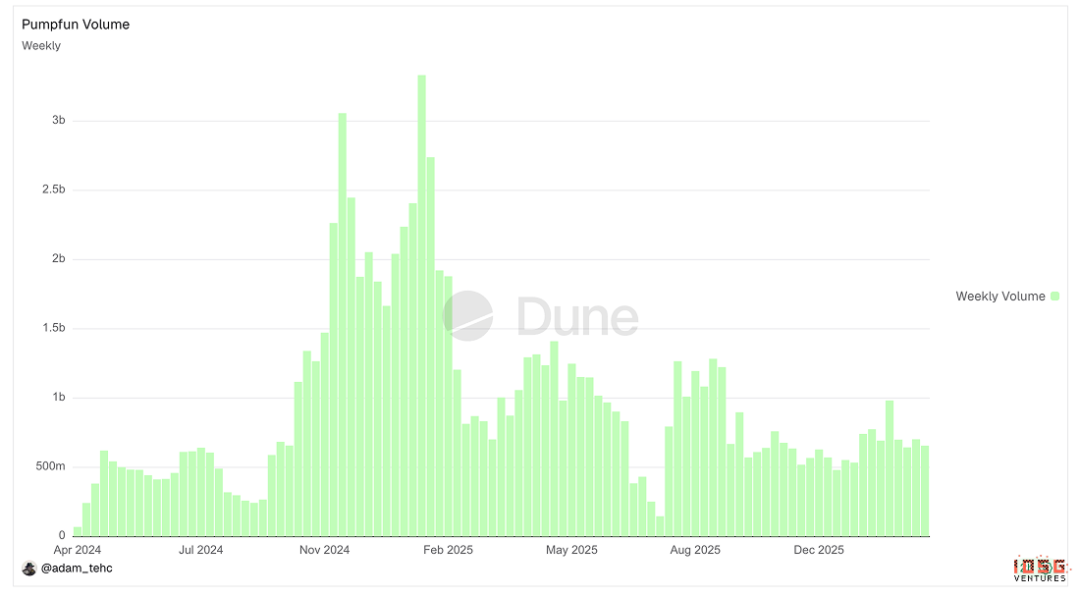

▲ Pump.fun Volume Chart

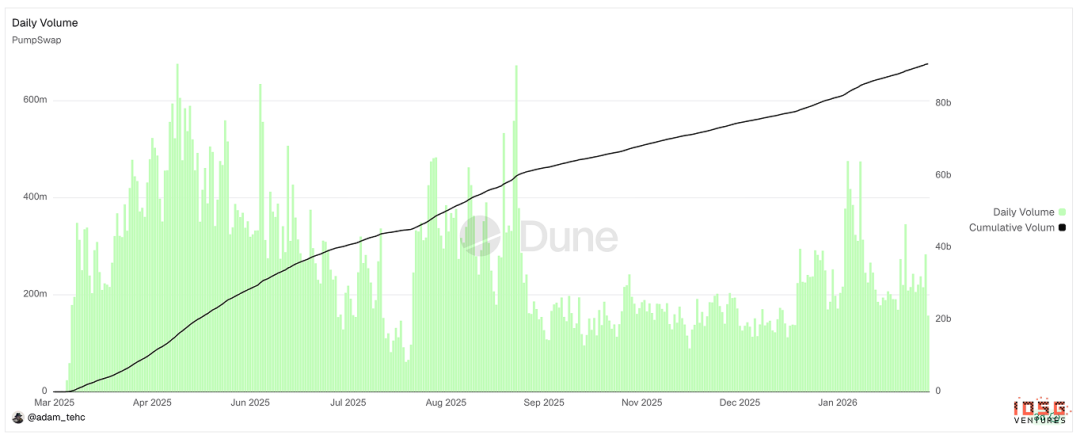

▲ PumpSwap Volume Chart

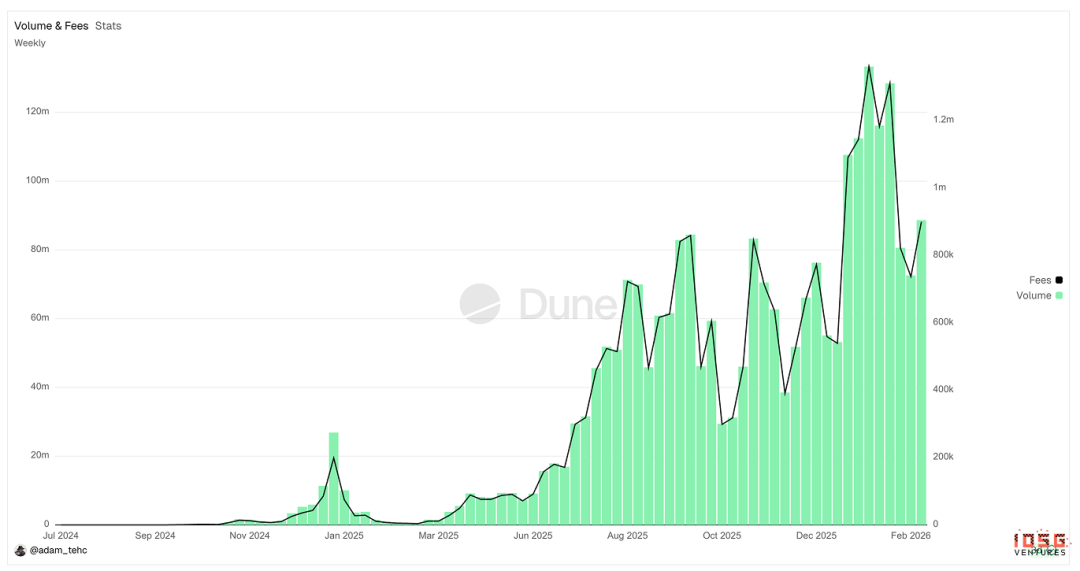

▲ Padre / Pump Terminal Volume Chart

Does Pump.fun Have Wash Trading?

$PUMP’s surface-level fundamentals appear robust—but the central question remains: Does its trading volume reflect genuine economic activity—or is it artificially inflated by users and bots?

Volume Correlation Analysis

The logic is straightforward: In an organic market, Launchpad and PumpSwap volumes should be positively correlated—with time lag. High Launchpad activity signals strong speculative interest; part of that capital flows into PumpSwap via the graduation mechanism, sustaining post-listing trading.

If severe wash trading exists, this relationship breaks down. Artificially inflated Launchpad volume leads tokens to “graduate” based on fabricated curve activity—only to enter PumpSwap without real buyers. The result? A surge in Launchpad volume, while PumpSwap volume stagnates—or even declines—causing correlation to approach zero or turn negative.

The most telling signal combination: a spike in graduation rate (more tokens artificially hitting curve thresholds), coupled with low—and rapidly decaying—per-token trading volume on PumpSwap, and no corresponding growth in PumpSwap’s liquidity depth alongside rising numbers of graduated tokens.

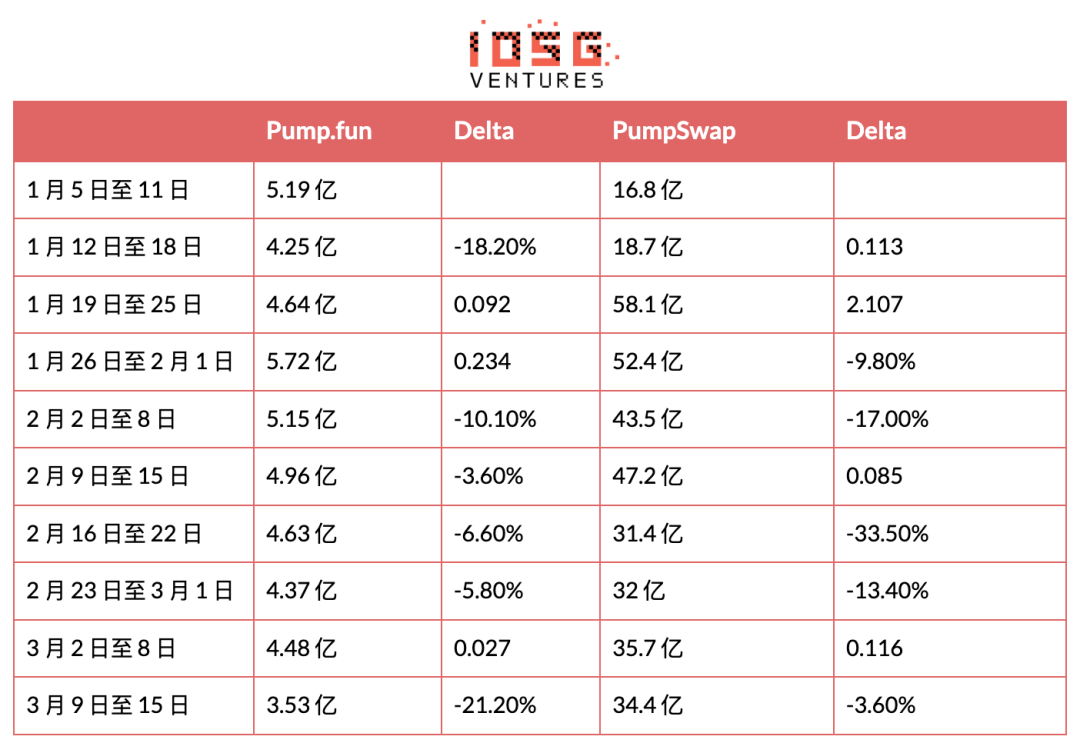

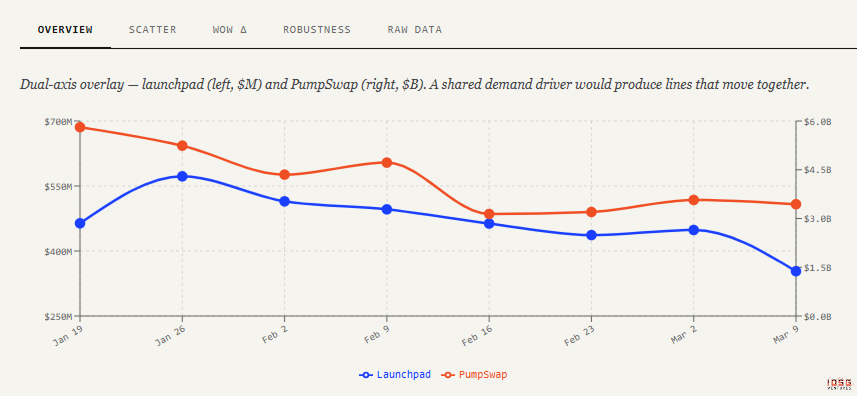

Data from January 2026 to present:

(The first two data points were excluded from correlation analysis due to anomalies caused by PumpSwap fee and market-maker policy adjustments.)

Findings:

Launchpad volume remains stable—fluctuating between $400M and $570M over eight weeks (~40% range). Given the presence of many bundlers and volume manipulators maintaining a baseline, this is unsurprising.

PumpSwap volume is far more volatile—ranging from $3.5B to $5.8B over the same period (~60% range)—driven primarily by surging meme-trading demand in mid-January and additional team incentives. Yet Launchpad volume showed no corresponding uptick.

r = 0.579—moderate positive correlation. With n = 8 samples, statistical significance (p < 0.05) requires r > 0.63—so this falls short of the threshold. However, both direction and strength align with the organic-growth hypothesis.

University of Pisa Paper

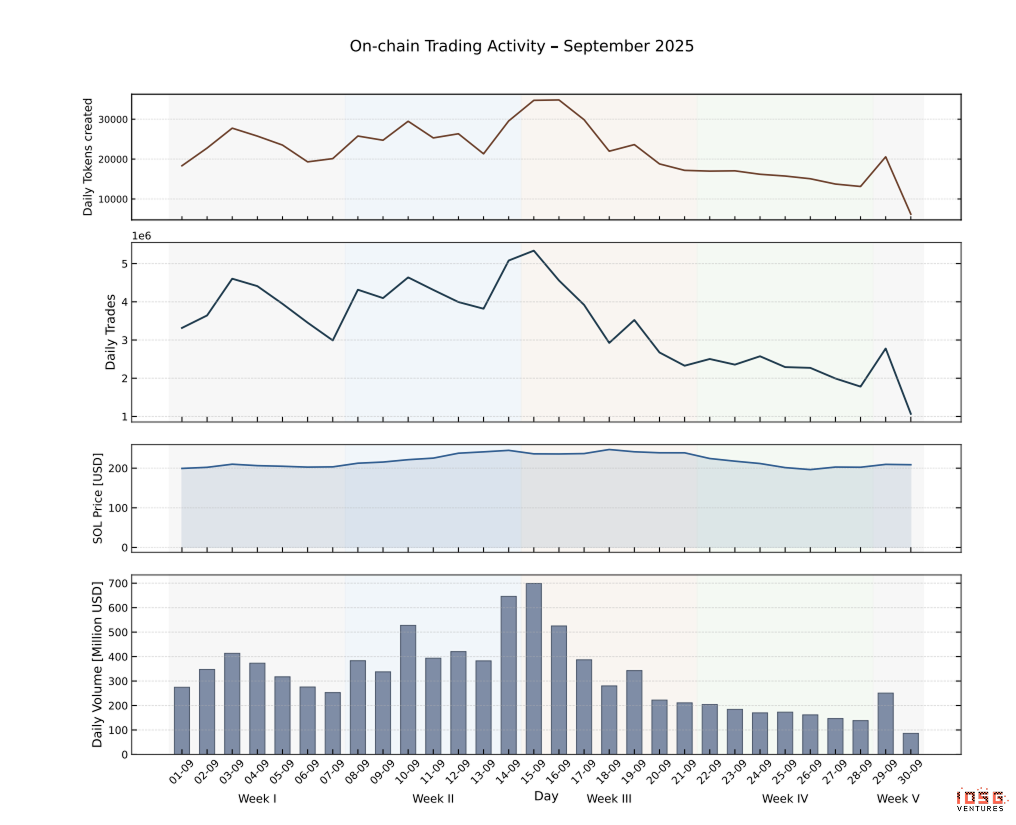

Researchers from the University of Pisa conducted a comprehensive onchain analysis of the Pump.fun Launchpad, covering all transactions across 655,770 tokens launched between September–October 2025. They used Solana transaction log metadata to distinguish bot-driven from human-initiated trades.

Four findings directly address the issue of fake trading.

Large human buys are the strongest predictor of graduation

The strongest predictor of graduation is rapid accumulation of SOL via a few large trades. Median graduation requires only ~457 trades—and occurs ~4.4 minutes after token creation. This pattern—large, infrequent inflows from diverse wallets—is consistent with coordinated human speculation (Telegram group calls, KOL hype) or pump-and-dump schemes—not high-frequency bot wash trading. Conversely, bot-dominated tokens tend to accumulate many small trades before stalling pre-graduation.

Bot activity actually suppresses graduation

Post-early-curve-phase, tokens exhibiting bot activity show systematically lower graduation probabilities. At the time, graduation required accumulating ~85 SOL in the curve. If bots were wash-trading to hit graduation thresholds, bot-active tokens should graduate more frequently—but the data shows the opposite.

The reason is structural: Upon graduation, the bonding curve transitions from virtual to real AMM reserves—causing effective liquidity depth to drop discretely. Selling before graduation (under virtual-reserve-supported depth) is more profitable than selling afterward.

The study also found that the top 10 token issuers in September 2025 each launched over 2,000 tokens monthly—and for each, statistically anomalous sell sequences were observed across wallet clusters just before hitting graduation thresholds. Bundlers and snipers front-run, building positions early and dumping on retail demand attracted by curve price rises.

Conclusion: Most bots on the platform are front-runners who extract value from human counterparties during entry and exit—not wash traders aiming to game graduation thresholds. They hoard supply and dump on retail near graduation. This is fundamentally distinct from wash trading.

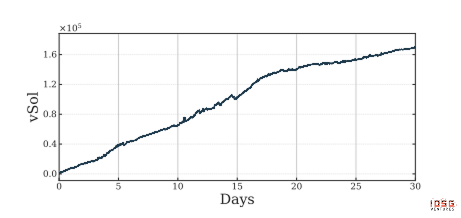

SOL net flow remains persistently positive—structurally incompatible with wash trading

The paper computed net SOL flow across the full dataset (total SOL deposited into curves minus total SOL withdrawn via sales). Over the one-month observation window, the ecosystem accumulated ~160,000 SOL in net retention (worth ~$32 million at September 2025 prices).

This serves as a hard test for wash trading: circular trades among linked wallets would produce near-zero net capital flow, as buys and sells cancel out. A $32 million net retention is structurally incompatible with large-scale circular trading—indicating sustained inflow of real external retail capital into the Launchpad. Each trade incurs a 1.25% fee, generating frictional revenue for the protocol.

The paper’s findings align with our volume correlation analysis: Much of Launchpad volume stems from bundlers and snipers executing pump-and-dumps—establishing a volume floor—but not wash trading. The distinction is critical: Wash trading generates zero net protocol revenue (fees offset across linked wallets), whereas pump-and-dumps generate real fees from genuine retail counterparties paying platform fees. An ARR of ~$390 million confirms Pump.fun monetizes real retail volume through a pump-and-dump ecosystem—not fabricated metrics.

Tokenomics

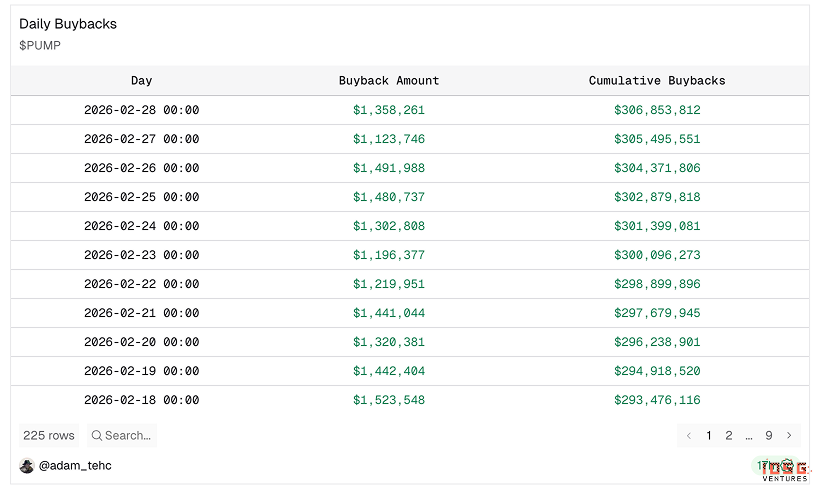

Buybacks

Pump Foundation currently allocates 100% of revenue from all product lines toward open-market $PUMP buybacks. Since announcing full-revenue buybacks on July 15, 2025, over eight months:

It has bought back 27% of circulating supply—removing 9.6% of total supply.

For comparison: Hyperliquid, since launching buybacks in November 2024, has burned only 4.1% of total supply (~12.3% of circulating supply).

At current price and revenue levels, annualized circulation reduction approaches 45%.

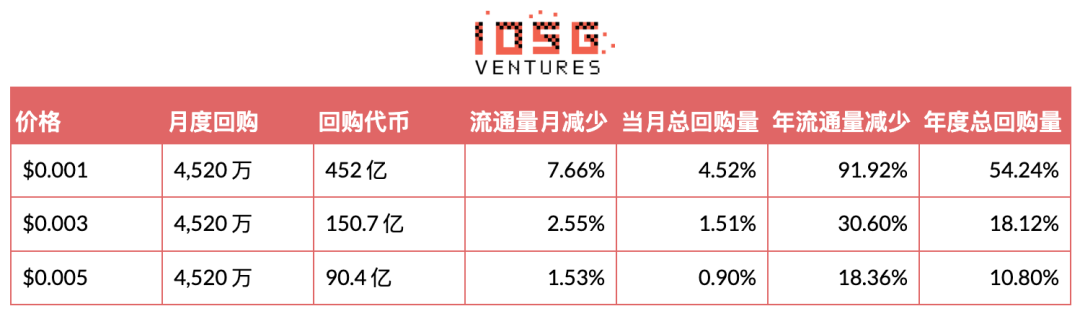

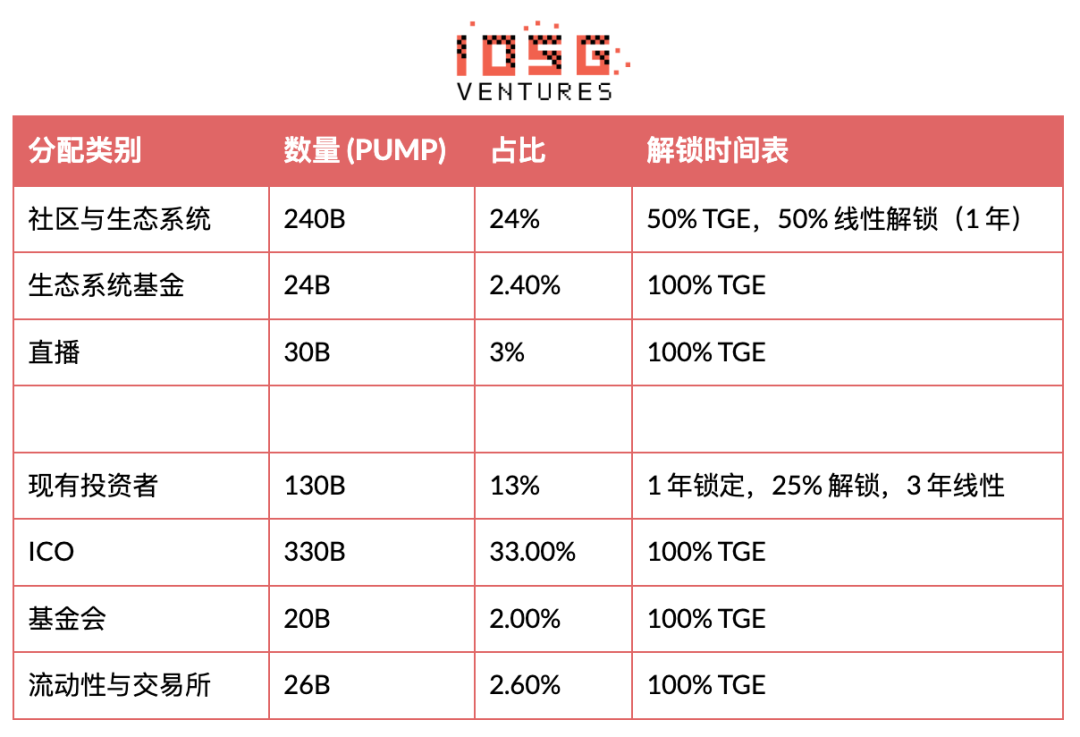

Supply Structure & Unlock Schedule

Total Supply: 1,000,000,000,000 PUMP

Circulating Supply: 430,000,000,000 (43%)

Remaining Locked: ~58% of total supply

Key unlock milestones: Ongoing—12% (as of July, released at 2% monthly for community & incentives); July 2026—8.25% unlock, followed by 36 months of 0.68% monthly unlocks.

Valuation Analysis

If the wash-trading analysis holds, $PUMP is undervalued—with asymmetric upside potential.

The discount stems from three factors:

# Market skepticism about revenue sustainability

The market views Pump.fun’s platform-wide volume as speculative and cyclical—tied closely to short-term meme activity. Investors treat current profitability as transient. At today’s P/E ratio, buybacks deliver tangible financial accretion—but valuation models exclude them, because the underlying assumption is that revenue will contract sharply. The debate isn’t whether Pump.fun profits now—it’s whether it will still profit 24 months from now.

# Absence of institutional coverage

We interviewed 15 Tier-1 secondary funds and VCs to gauge sentiment on $PUMP. Only one actively tracks $PUMP using bottom-up analysis. Most institutions haven’t modeled the new product suite, segmented revenue by product line, or stress-tested volume sustainability.

This coverage gap creates a narrative vacuum—pricing driven more by market perception than financial analysis. By contrast, $HYPE benefits from deeper institutional support, broader research coverage, and clearer product positioning—supporting a higher, more stable valuation multiple.

A self-reinforcing dynamic also exists: Assets tied to meme infrastructure are default-classified as speculative and ephemeral—leading to trading behavior that reinforces that classification. It takes time—and data across multiple cycles—for the market to update this mental model. Until Pump’s revenue withstands broader crypto market corrections and institutional coverage expands, valuation compression may persist—regardless of current cash flow.

# Management trust not yet established

Investor concerns center on: long-term vision beyond memes, capital allocation discipline, execution against the product roadmap, and transition from viral growth to a sustainable platform economy.

Markets typically assign lower valuation multiples to founder-led, high-growth platforms—until they demonstrate resilience through market volatility and prove growth converts into durable platform economics. Until Pump demonstrates sustained revenue diversification and disciplined execution via products like PumpSwap and Pump Terminal, this discount is likely to remain.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News