After $20 billion in liquidations, crypto investors must master these risk management strategies

TechFlow Selected TechFlow Selected

After $20 billion in liquidations, crypto investors must master these risk management strategies

There are many important things to manage, but nothing is more important than risk.

Author: Spicy

Translation: Luffy, Foresight News

There are many important aspects in trading, but nothing is more critical than risk management.

I was a professional trader and have been trading cryptocurrencies for 8 years. Thank you for taking the time to read this article. In return, I will share with you everything I know about risk management without reservation.

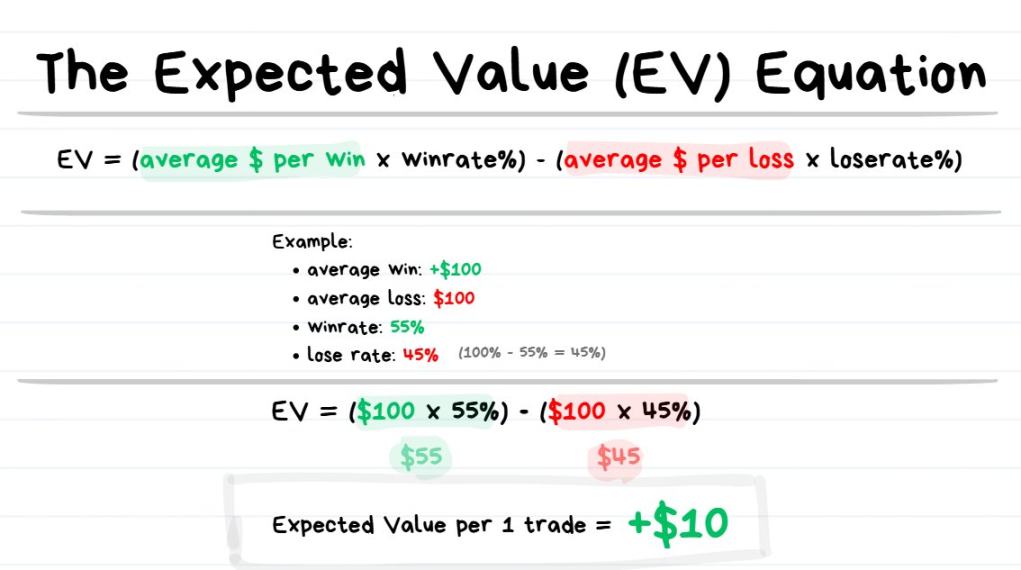

Expected Value (EV) Formula

Expected value formula: EV = (average profit × win rate) − (average loss × loss rate)

Tip: Expected value refers to "the average outcome you can expect when repeatedly making the same decision."

Every trader must understand the concept and calculation of expected value. Why is expected value so important? A trading strategy’s expected value helps us estimate "the profit we can expect after conducting N future trades."

For example, if each trade has an expected value of +$10, after executing 1,000 identical trades, your expected profit would be approximately $10 × 1,000 = $10,000.

-

If you have a positive expected value (+EV), you will be profitable in the long run;

-

If you have a negative expected value (-EV), you will eventually lose money over time.

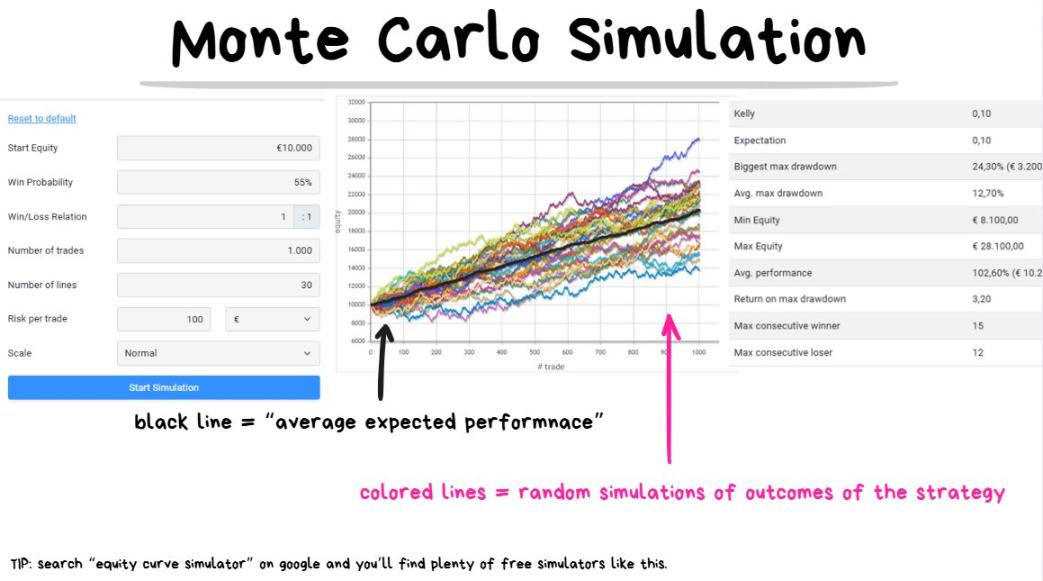

Next, I’ll introduce the "Monte Carlo simulation," which visually demonstrates how expected value works in practice.

Monte Carlo Simulation

First, a quick overview of Monte Carlo simulation

Assume a trading strategy has a 55% win rate and a 1:1 risk-reward ratio. Simulating 30 possible outcomes for the next 1,000 trades shows this is a profitable strategy with positive expected value (+EV).

Tip: Monte Carlo simulation predicts all potential results after N trades by running numerous random hypothetical scenarios.

Monte Carlo simulation helps manage expectations and gives a rough idea of a strategy’s profit potential.

By inputting initial capital, win rate, average profit/loss ratio, and number of trades, the simulation generates random combinations of possible trading performance.

The thick black line in the chart represents the average expected result: If each trade has an expected value of +$10, after 100 trades, total profit is around +$1,000; after 1,000 trades, around +$10,000.

Note the word "around"—results aren't guaranteed due to variance.

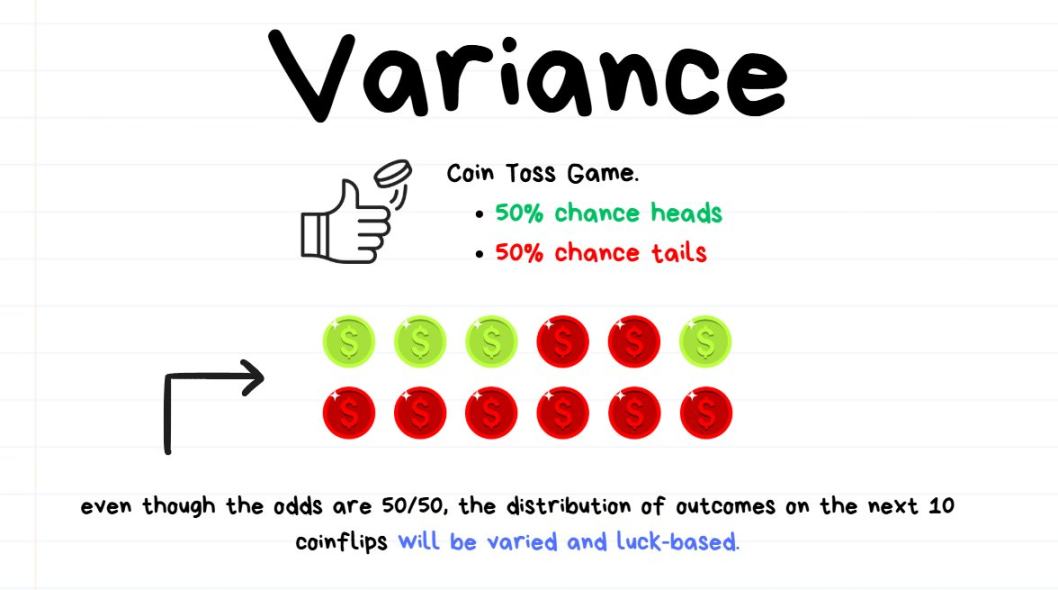

Then, a quick look at variance

Whether you like it or not, randomness affects trading performance.

Using a coin toss analogy: Suppose you play a coin-tossing game where heads and tails each have a 50% probability.

If you toss the coin 10 times, you might get 8 heads and 2 tails—even though the expected probability is 50%, the actual result shows 80%.

This doesn’t mean the coin is rigged or that heads actually have an 80% chance—it simply means the sample size is too small for probabilities to reflect their true distribution.

The difference between the actual result (80%) and theoretical probability (50%) is called variance (80% - 50% = 30%).

If you toss the coin 10,000 times, you might get 5,050 heads and 4,950 tails. Although heads occurred 50 times more than expected, the percentage variance is only 0.5% (50 ÷ 10,000).

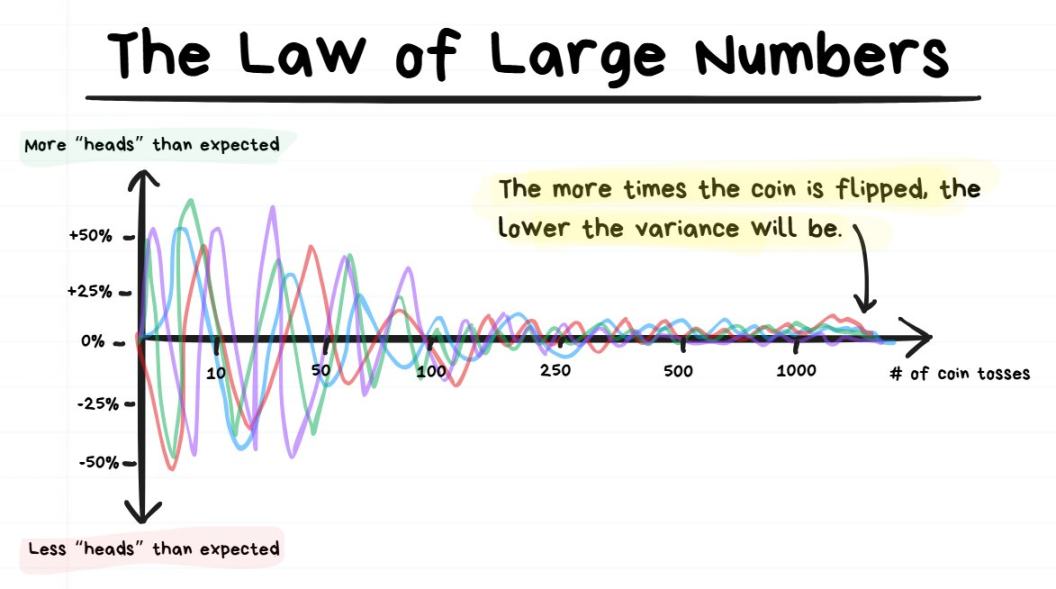

Finally, a quick look at the Law of Large Numbers

The more times you toss the coin, the closer variance gets to zero.

Tip: The Law of Large Numbers states that as a random event is repeated more times, its results converge toward the true average.

With only 10 tosses, the variance in heads probability could be large; with over 10,000 tosses, the variance becomes very small.

In simple terms, the more events occur, the closer the results get to the true probability.

How do Monte Carlo simulation, variance, and the Law of Large Numbers relate to trading?

Monte Carlo simulation helps us manage expectations based on variance and predict how N future trades might perform—the more trades, the smaller the expected variance.

It also answers key questions:

-

After N trades, what should the expected profit be?

-

What's the maximum possible streak of consecutive wins?

-

What's the maximum possible streak of consecutive losses?

-

Given current win rate and risk-reward ratio, what percentage drawdown after N trades is considered normal?

At the same time, it delivers a reality check:

-

Even highly profitable strategies may experience long drawdowns (drawdown refers to the percentage loss in account value);

-

Even high-win-rate strategies may suffer extended losing streaks;

-

Even low-win-rate strategies may have long winning streaks;

-

The outcome of the next trade doesn’t matter—what matters is the overall result across the next 100+ trades.

Core takeaways from this section:

-

Sometimes you make a good trade and still lose;

-

Sometimes you make a bad trade and still profit.

These situations arise due to variance (or luck). Judging the quality of a trade based solely on its outcome is flawed.

Two extreme examples:

-

You follow a trading strategy with a 90% win rate and 1:1 risk-reward ratio. Even if this trade loses, it’s still the correct decision. Because if you repeat this trade 1,000+ times and let the Law of Large Numbers work, you will inevitably profit.

-

You play a slot machine at a casino. Even if you win once, it doesn’t mean it was a smart bet—just lucky variance. If you keep betting 1,000+ times and let the Law of Large Numbers work, you will inevitably lose all your money.

Key conclusion:

Don’t judge trade quality by whether the next trade wins or loses—judge it by its expected value. You need patience and must endure some variance before profits gradually emerge.

Leverage and Liquidation

Leverage may be one of the most misunderstood concepts among traders.

Before reading further, remember: you don’t need to memorize every detail—no pressure. Just grasping the basics of leverage is enough for trading.

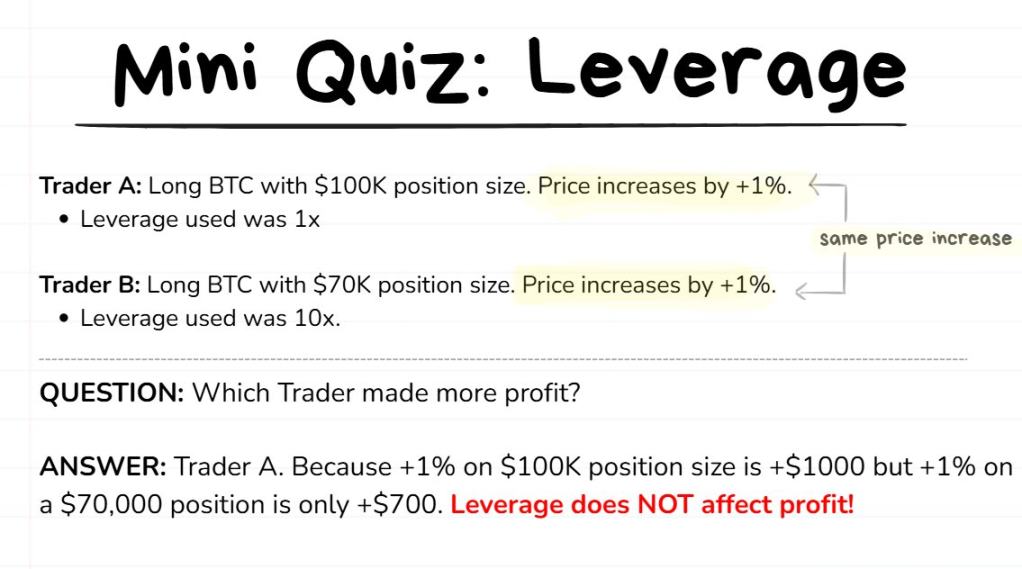

Quick test: See if you understand the fundamentals of leverage (assuming two traders enter at the same price):

Most people have a major misconception (completely wrong): Leverage is a profit multiplier—crank up leverage, magically increase trading profits.

I can say with certainty: leverage is absolutely not this.

The real purpose of leverage (correct): Leverage is a tool to reduce counterparty risk and improve capital efficiency.

Counterparty risk: The risk of holding funds on an exchange, which could potentially disappear, commit fraud, or get hacked (e.g., the FTX incident)—so your funds aren’t completely safe.

Capital efficiency: How effectively you use your capital to generate more profit. For example: earning $1,000 per month with $1,000 principal is 100x more efficient than earning $1,000 per month with $100,000 principal.

Before diving deeper, let’s define a few terms, then return to leverage.

-

Trading account balance: Total capital you’re willing to allocate for trading;

-

Exchange account balance: Funds deposited on the exchange, usually only a small portion of your trading account balance. It’s not recommended to deposit all trading funds on an exchange;

-

Margin: Deposit required to open a position;

-

Leverage: The multiple of borrowed funds from the exchange;

-

Position size: The total amount of tokens (or their dollar value) you actually buy/sell in a trade.

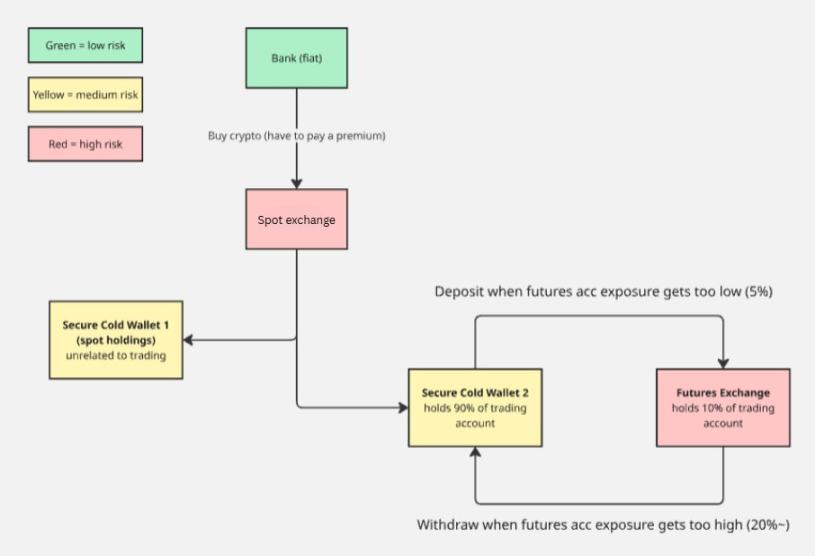

Additional note: The diagram below shows my process for managing deposits and withdrawals from exchanges. The core principle is "don’t concentrate all funds on a single exchange to avoid excessive exposure."

Understanding these concepts through an example

Suppose you have $10,000 available for trading—this is your trading account balance.

You don’t want to deposit the full $10,000 on an exchange (due to concerns about freezing, fraud, or hacking), so you deposit only 10%, or $1,000. Your exchange account balance is now $1,000.

You spot a good opportunity to go long on Bitcoin and want to open a $10,000 BTC position. When you click buy, the system says insufficient funds because your exchange balance is only $1,000. To open the position, you need to borrow funds via leverage.

Set leverage to 10x, then click buy again to successfully open the position:

-

The trade’s position size (actual value of BTC bought) is $10,000;

-

The margin (your deposit) is $1,000;

-

The leverage is 10x.

Tip: Regardless of whether you use 1x or 100x leverage, the profit from a $10,000 position remains the same—the nature of a $10,000 position doesn’t change with leverage. Even adjusting leverage during the trade won’t affect final profit.

Purpose of liquidation

When you open a leveraged position, you’re essentially borrowing money from the exchange—these funds don’t appear out of nowhere.

If you open a $10,000 position with 10x leverage and your exchange balance is only $1,000, then $9,000 is borrowed from the exchange and can only be used to open the position.

To ensure the exchange can recover the lent funds, a liquidation mechanism exists.

Liquidation: If the price hits a specific level (liquidation price), the exchange forcibly closes your position and seizes your margin. After that, the position is taken over by the exchange—any further gains or losses are no longer yours.

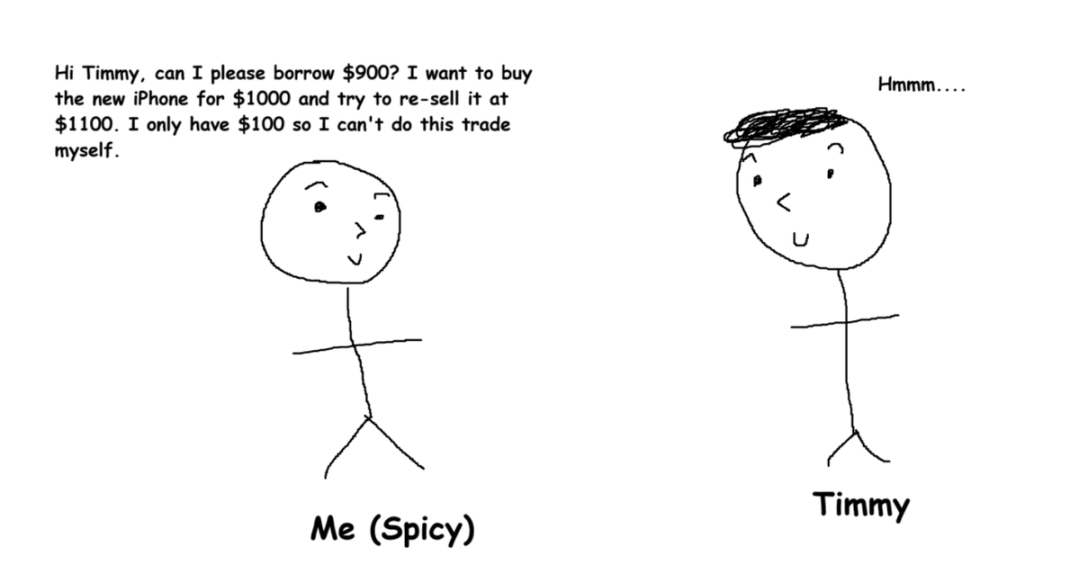

Simple analogy to clarify understanding

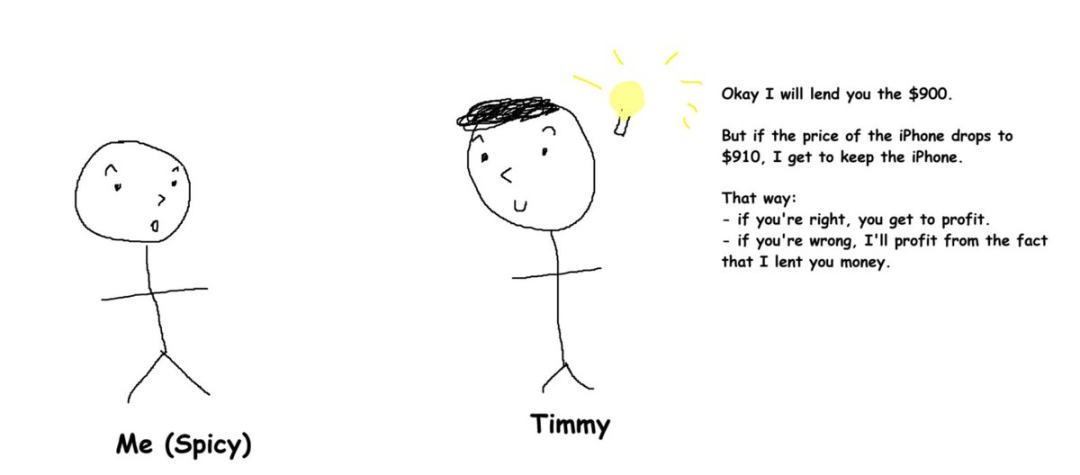

Suppose you’re bullish on a new iPhone currently priced at $1,000. You expect it to rise to $1,100 (a 10% gain), plan to buy at $1,000 and sell at $1,100, profiting $100.

But here’s the problem: you only have $100 in your bank account.

So you approach a wealthy friend, Timmy, and borrow $900 to execute this iPhone trade.

Potential Risk

If after lending you $900, the iPhone price drops below $900, even if you sell the iPhone, you can’t fully repay Timmy—you’d default, causing Timmy to lose money, which he wants to avoid.

Solution

You and Timmy sign a mutually beneficial agreement (a perpetual contract is essentially such an agreement between a trader and an exchange):

You agree with Timmy: if the iPhone price falls below $910, you must hand over the iPhone to Timmy—this is equivalent to your position being liquidated.

At this point, you lose your initial $100 deposit (margin); Timmy then tries to sell the iPhone himself. If the price doesn’t fluctuate much and he sells above $900, he makes a profit.

Timmy requires takeover at $910 instead of $900 because "lending you money" should give him a reasonable return, providing enough buffer for him to "sell the iPhone and recover his principal."

Core takeaway from this section

You don’t need to memorize all term definitions. The key is understanding that leverage is merely a tool to achieve your desired position size.

Additionally, never expose yourself to liquidation risk—liquidation costs and fees are extremely high.

Tip: Always set a stop-loss for every trade. Trading without a stop-loss is highly risky.

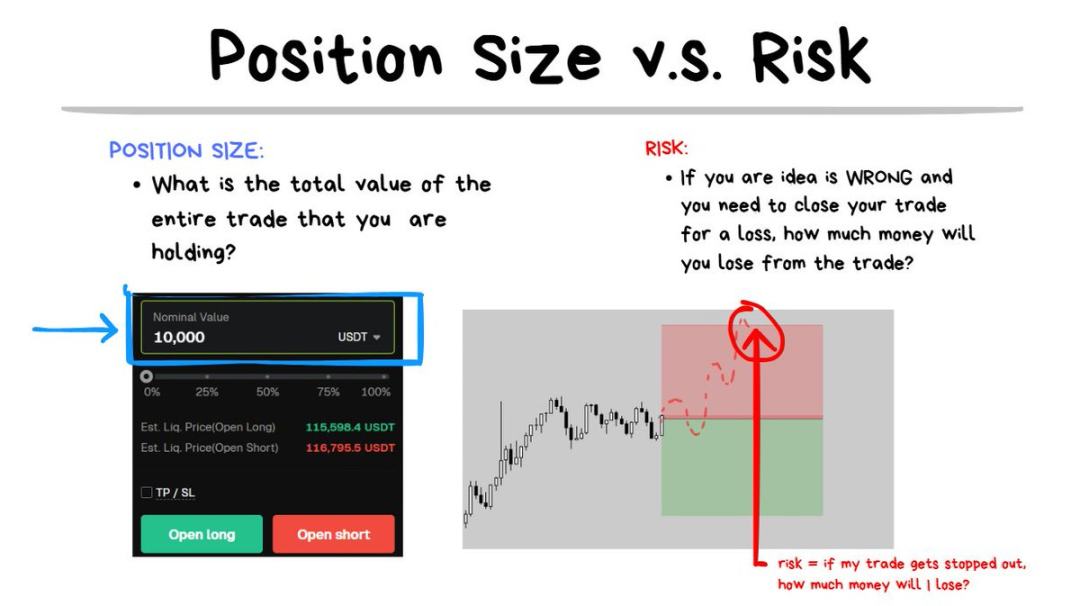

Difference Between Position Size and Risk

Another commonly misunderstood concept among traders is the difference between position size and risk.

Position size refers to the total amount of tokens involved in a trade (or their dollar value). For example: I bought $10,000 worth of BTC, so my position size is $10,000.

Risk refers to the amount of money you stand to lose if your trade is wrong and you need to exit via stop-loss. For example: if the price hits my stop-loss, I’ll lose $100—so my risk is $100.

Before any trade, I first ask myself: "If I’m wrong and must exit via stop-loss, how much loss can I accept?"

This is a crucial question, yet many traders completely ignore it. They firmly believe their trading idea is absolutely correct and cannot fail, compounded by FOMO, often leading them into trouble.

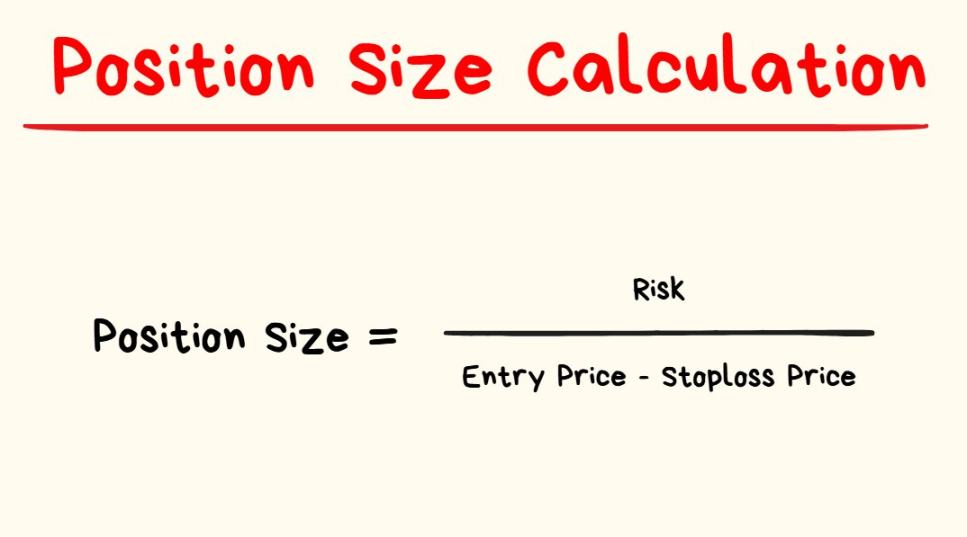

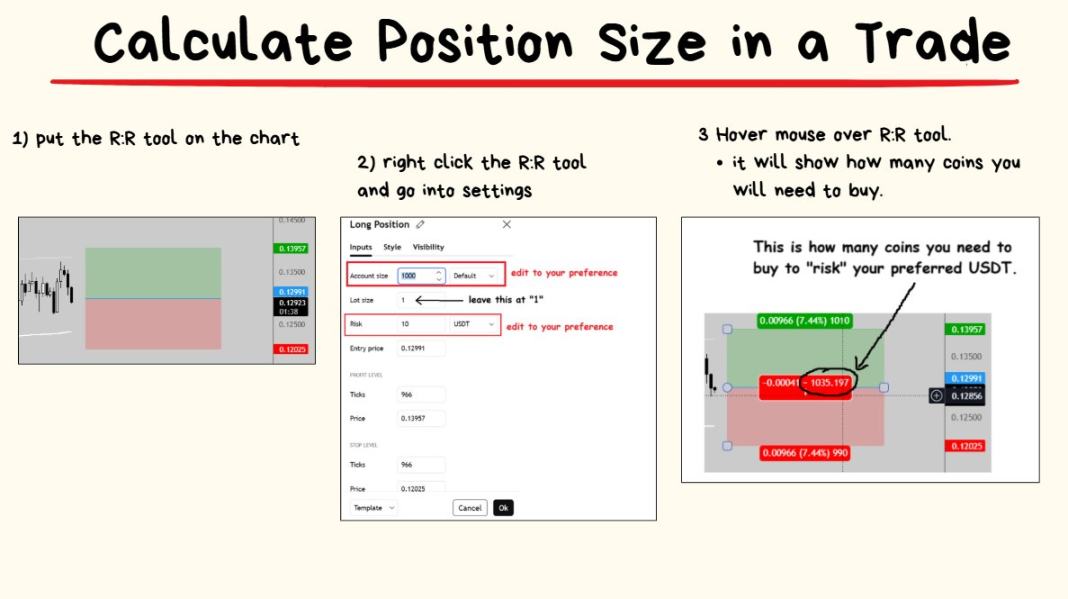

Once you determine the acceptable loss amount for your next trade, the next step is calculating the required position size.

You don’t need to worry about doing math before every trade—there’s a simpler way.

TradingView’s risk-reward tool already includes built-in calculations:

It’s very easy to use. Now let’s move to the final concept 🤓

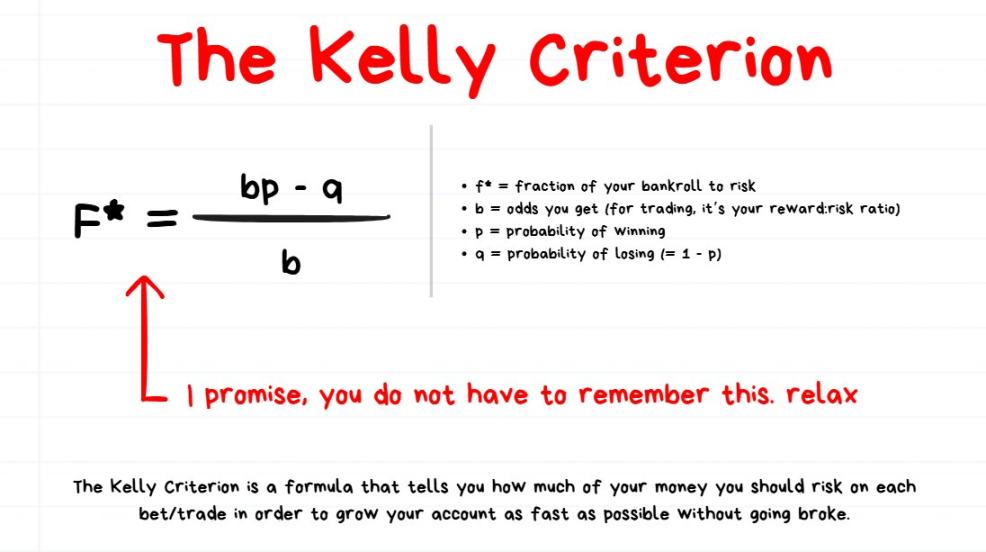

Risk of Ruin and Optimal Bet Sizing

All traders eventually face the same question: What’s the optimal risk per trade?

Answer: It depends.

Common answer: The widely accepted advice is to risk no more than 1% of capital per trade. For example, if you have $10,000 capital, your expected loss on the next trade if stopped out is $100.

My personal answer: Higher-quality trades = larger bets; lower-quality trades = smaller bets.

This section covers risk of ruin and the Kelly Criterion.

First, understand risk of ruin

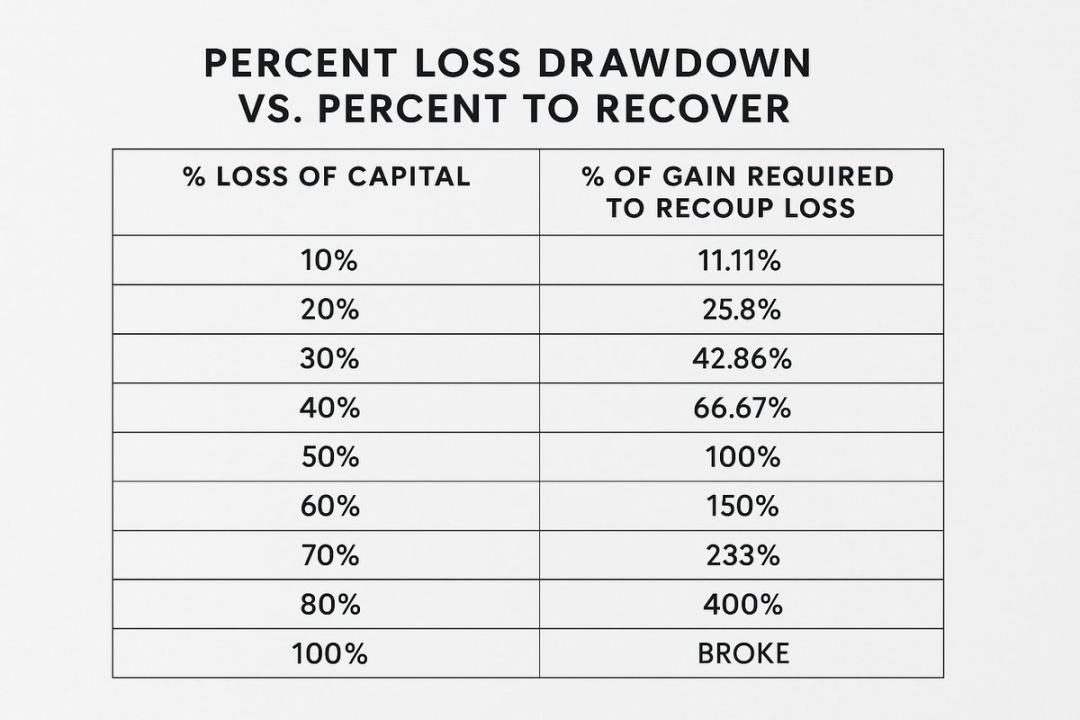

Even if you have a trading edge (a profitable strategy with positive expected value), it doesn’t mean you can’t blow up your account.

Tip: The first rule of trading is never blow up. Once you’re ruined, you can’t continue trading. The essence of trading is staying in the market long-term.

In fact, if you risk too much per trade, even with a profitable strategy, you will eventually lose everything.

Extreme example:

Suppose you commit 100% of your capital on every trade, with a strategy that has a 90% win rate and a 10:1 risk-reward ratio—an excellent strategy. But the problem is that going all-in every time will eventually lead to ruin.

Once ruined, the game is over. Even nearing ruin makes recovery extremely difficult.

This is why growing an account feels hard, while blowing up feels easy.

Clearly, there’s a hard limit to excessive risk—even with great strategies, betting too big will eventually cause ruin.

On the flip side, if risk is too low (e.g., risking only 0.0000001% of capital per trade), your account will never grow effectively.

So where is the balance point for optimal risk?

Then, the Kelly Criterion attempts to solve this "balance point" problem

You don’t need to memorize the exact Kelly formula—I include it only for curious readers.

Some traders believe the Kelly Criterion is the best method for calculating optimal bet size; others think it’s too conservative and slow-growing, so they multiply the Kelly result (e.g., bet size = Kelly × 2); still others think it’s too aggressive and doesn’t account for unexpected errors, so they divide the Kelly result (e.g., bet size = Kelly ÷ 2).

My core view on the Kelly Criterion and optimal bet sizing

I believe there’s no perfect method for calculating bet size.

Even if you use the Kelly Criterion or other complex formulas, there’s no absolutely perfect solution in trading.

As I mentioned earlier, I prefer dynamically adjusting bet size:

-

Low-quality trades: Skip entirely;

-

Standard-quality trades: Risk 1% of capital;

-

High-quality trades: Risk 2% of capital;

-

Exceptional-quality trades: Risk up to 4% of capital.

Additional note: Is this the optimal betting method? I’m not sure! But I like simplicity, and this approach works well for me.

I judge trade quality based on the strategy used and the market variables present before entry.

Summary

-

Understanding the numbers behind your trading edge is crucial. In probabilistic activities like trading, expected value is the core concept;

-

Focus on the overall outcome of the next 100 trades, not the profit or loss of the next single trade—let the Law of Large Numbers work;

-

Leverage isn’t a profit multiplier—it’s a tool to improve capital efficiency. Remember: never expose yourself to liquidation risk;

-

Position size is the value of tokens you buy/sell, while risk is the amount you’ll lose if your analysis is wrong;

-

Drawdowns are easy to fall into but hard to recover from—control your bet size wisely. If you're new, simplify: risk less than 1% per trade, and only adjust after gaining familiarity with high-quality A+ trade setups.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News