The USDH minting rights spark a fierce competition, but does HyperLiquid really need a new stablecoin?

TechFlow Selected TechFlow Selected

The USDH minting rights spark a fierce competition, but does HyperLiquid really need a new stablecoin?

Setting aside returns, "market share anxiety" might be the biggest motivation behind HyperLiquid issuing a stablecoin.

By Eric, Foresight News

Just as large-scale projects two or three years ago began launching their own blockchains or L2s en masse, the stablecoin market is also being increasingly carved up by major ecosystem players.

Last week, HyperLiquid—the rising star among derivative DEXs—announced it would release the USDH ticker, previously tightly held by the protocol, prioritizing service to the HyperLiquid ecosystem and compliance standards, allowing participants to compete for the right to issue this native stablecoin.

At the time of writing, five institutions or projects are competing for the minting rights of USDH: Paxos, Frax, Agora, Ethena Labs, and Native Markets, a protocol within the HyperLiquid ecosystem. Aside from Ethena Labs, which has not yet formally submitted a proposal, the other four are actively competing on how best to maximize user benefits.

Due to compliance requirements, USDH will be a dollar-pegged stablecoin similar to USDC. The market has interpreted HyperLiquid's move in various ways—some believe Hyper aims to reduce reliance on USDC, while others think it seeks to leverage its platform influence to capture a share of the stablecoin market. Many community members have praised the approach as an innovative model for launching a project-native stablecoin.

While some view Hyper’s move as more "offensive," I see the launch of a stablecoin at this peak moment as fundamentally a "defensive" strategy. Letting the community decide who issues the stablecoin delegates expertise to specialists and allows users collectively to choose what serves them best. At the same time, Hyper did not seek input on *whether* minting rights should be relinquished, indirectly suggesting that the stablecoin itself is not central to its core strategy.

The strongest contender, Paxos, emphasized its extensive experience in compliance and integrating stablecoins into banking operations. Key strengths include partnerships across industries, compliance across multiple global jurisdictions, integration with diverse payment channels, and direct convertibility with USDC, PYUSD, and USDG. As a seasoned stablecoin provider, Paxos can rapidly connect USDH to numerous channels, reinforcing its parity with the U.S. dollar.

In the relatively weaker Web3 domain, Paxos has countermeasures. It pledged to allocate 95% of interest earned from USDH reserves toward buying back HYPE tokens, redistributing them to ecosystem programs, partners, and users. A portion of these buybacks will incentivize platforms contributing to USDH growth, measured by USDH volume and transaction activity on each platform.

Additionally, Paxos established Paxos Labs to accelerate stablecoin adoption in decentralized ecosystems and acquired Molecular Labs, an infrastructure provider for HyperLiquid ecosystem projects, aiming to promote USDH more widely within the ecosystem.

Frax has gradually transitioned its original algorithmic stablecoin FRAX into an over-collateralized stablecoin frxUSD since late last year. Its proposal states that USDH will be backed 1:1 by frxUSD and support minting and redemption via USDT, USDC, and fiat. Frax explained that its entire protocol is now built around frxUSD, with mature infrastructure, so USDH will inherit all existing frxUSD functionalities.

frxUSD is currently supported by BlackRock’s on-chain fund BUIDL. Unlike Paxos, which offers 95% of yield, Frax plans to pass all underlying yield directly to Hyper users through FraxNet. This includes boosting HYPE staking rewards, buying back HYPE for community funds, and rewarding active traders or USDH holders.

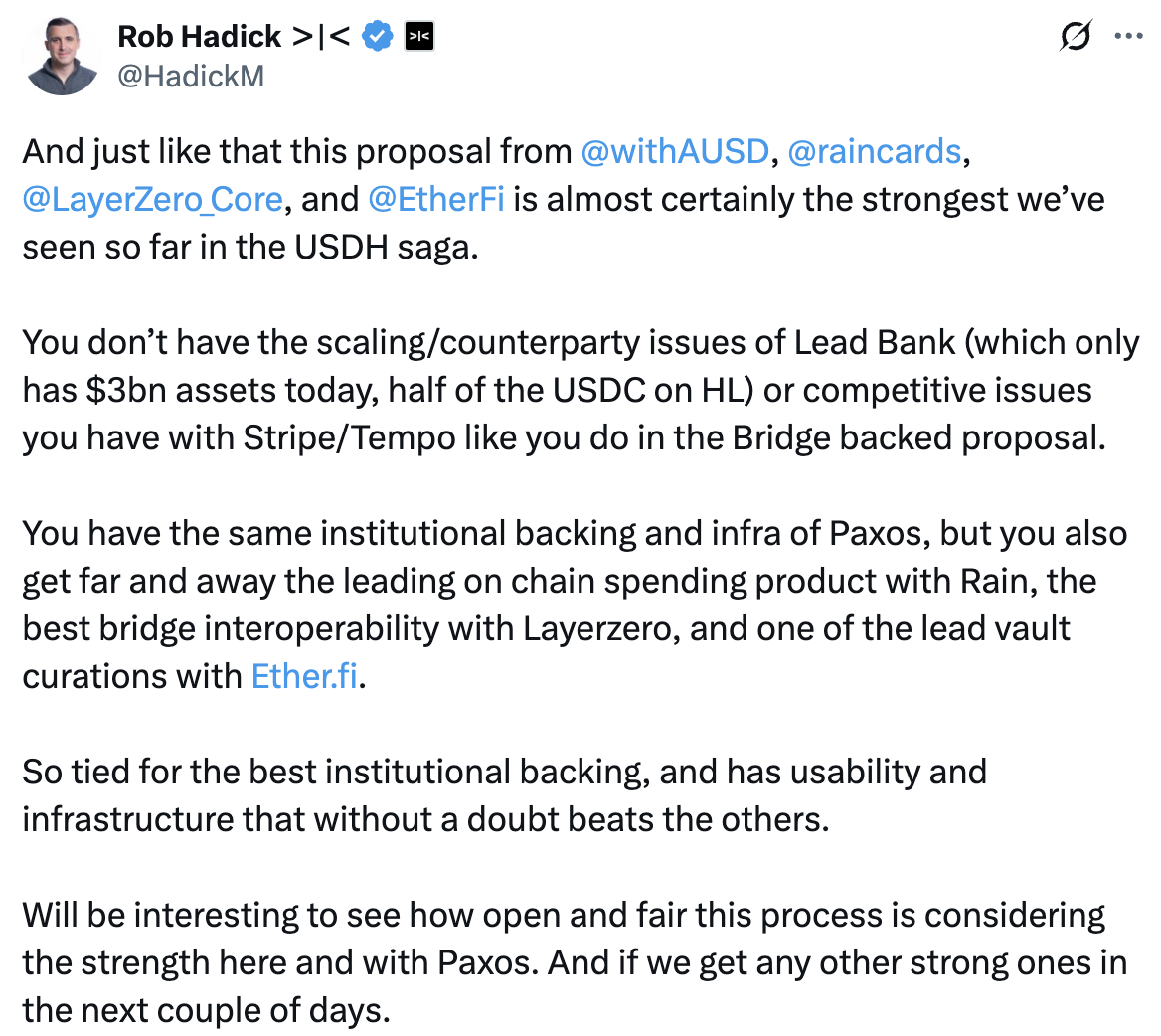

Agora, which announced a $50 million Series A round in July, is another competitor. Unlike the first two operating independently, Agora formed a "coalition": Agora provides institutional-grade stablecoin infrastructure, Rain offers consumer cards and on/off-ramps, and LayerZero delivers interoperability support. Agora also plans to collaborate with Etherfi to bring USDH into consumer applications. Like others, Agora commits to channeling all reserve asset yields into community funds or HYPE buybacks.

Agora particularly highlights that its white-label architecture enables solution delivery while preserving USDH’s brand independence from HyperLiquid, leaving operational control to Hyper and providing only backend support. Dragonfly Managing Partner Rob Hadick appeared to favor Agora, calling it the “strongest proposal” he’s seen so far.

Native Markets appears weaker among competitors and lacks distinctive features in its proposal. While it matches the others in fully returning reserve yields, its partnership with Bridge for compliance and fiat on/off-ramp solutions raised concerns about conflicts of interest. Bridge was previously acquired by Stripe, which recently announced plans to develop its own stablecoin chain, Tempo.

Native Markets’ sole advantage may lie in its deep integration with the Hyper ecosystem. Its proposal explicitly states that USDH will be minted directly on HyperEVM and will support transfers to HyperCore from day one.

Ethena Labs, a breakout new player in stablecoins this cycle, has not formally submitted a proposal. It tweeted that it had submitted two USDH-related proposals but received no response.

In an interview with Altlayer, I once asked why they believed projects would inevitably be motivated to launch their own blockchain or L2.

They explained that Web3 users lack psychological loyalty to any single project; decisions often hinge on which project offers greater benefits. If most projects continue building atop existing chains or L2s, they risk being replaced overnight by a newer alternative. By building their own chain and placing core assets in a controllable environment, projects gain more room to distribute value and lock users onto their chain. To some extent, the friction and complexity of asset migration lead users to let their positions dictate their choices, keeping them within the project’s ecosystem.

This stems from anxiety over user retention and traffic. In the fast-evolving Web3 market, HyperLiquid—which captured nearly $400 billion in contract trading volume last month, securing 70% of the on-chain market—is now facing the classic challenge: “conquering is easy, holding onto power is hard.”

The on-chain derivatives market has long been winner-takes-all. dYdX brought order books on-chain using L2’s high speed and low cost, once seen as a potential exchange disruptor, only to be overtaken by GMX on Arbitrum, which uses vaults to bet against traders. Now the baton has passed to HyperLiquid. Despite its current dominance, it too could be dethroned overnight by a new challenger.

This pattern isn’t limited to on-chain derivatives. Circle, Tether, and Stripe (mentioned earlier) are all exploring stablecoin blockchains. One day, a “new Hyper” might emerge on such a chain, enabling stablecoin holders to trade without complex cross-chain steps. Circle or Tether could even enter directly, eliminating trading fees altogether just to boost stablecoin issuance and profit from U.S. Treasury yields.

Facing such potential threats, Hyper must find a way to retain users within its protocol. Issuing a stablecoin is indeed the best method available—one that preserves fee revenue while strengthening user stickiness.

If Hyper merely wanted to add a stablecoin to its ecosystem, it wouldn’t need to publicly select a provider. It could quietly partner with a service provider and return 50% of Treasury yield to users—achieving both popularity and increased protocol revenue. The real motive lies in fostering competition among providers to maximize user returns, even operating at a loss temporarily, thereby locking users into the protocol. From this perspective, Hyper’s decision to ignore Ethena’s overture is understandable—Ethena excels at productizing stablecoins, but that’s not Hyper’s goal.

According to Qianji Investment Bank’s “2024 Third-Party Payment Industry Research Report,” Analysys data on China’s third-party payment transaction volumes in 2023 shows Alipay, WeChat Pay, and UnionPay Merchant Services ranked top three with 34.5%, 29%, and 10.2% market share respectively, while JD Pay held only 5.8%. In the same year, JD’s e-commerce market share was 14%.

Using these figures, my point is that Hyper cannot撼动 Circle’s fundamental position. Circle’s supply chain and ecosystem built over years for USDC are difficult to surpass overnight. Hyper issuing a stablecoin is something Circle will eventually have to face—just as Tencent must eventually confront JD’s self-developed third-party payment solution.

Even if it loses HyperLiquid, Circle can still support other protocols or sacrifice some revenue for distribution channels, much like its collaboration with Coinbase. While USDH’s emergence may cause short-term pain for Circle, in the long run, it remains uncertain whether Circle’s ecosystem reach and influence or full yield redistribution will prove more attractive.

Unveiling the long-held USDH ticker may not signal HyperLiquid’s ambition to dominate stablecoins, but rather reflects how the genius yield法案 mandates stablecoin reserves to invest in Treasuries, generating natural interest—a perfect tool for retaining users.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News