Opinion: This bull market stems from capital overflow in the AI sector, and the momentum will continue

TechFlow Selected TechFlow Selected

Opinion: This bull market stems from capital overflow in the AI sector, and the momentum will continue

AI giants' capital spending generates liquidity, crypto companies emerge as new buyers, bull market still has momentum.

Author: arndxt

Translation: TechFlow

This is a bull market driven by liquidity, yet lacking support from traditional sources of liquidity.

The Federal Reserve maintains a tight monetary policy, and fiscal stimulus is gradually fading, yet risk assets continue to rise. Why? Because capital gains fueled by artificial intelligence (AI) and capital expenditures (Capex) within the top tier of the economy are cascading downward, while crypto treasury companies (Crypto Treasury Companies,简称 TCos) have designed a new transmission mechanism that converts stock market euphoria into on-chain bidding.

This "flywheel effect" can withstand seasonal weakness and macro noise until hyperscaler Capex declines or ETF demand stalls.

Image source:

https://x.com/lanamour69/status/1957087662105415896

Three Key Insights

-

Shift in Liquidity Source: Liquidity no longer comes from the Fed or the Treasury, but from equity gains and capital expenditures by AI hyperscalers. The wealth effect generated by companies like NVIDIA and Microsoft, combined with a wave of over $100 billion in capital spending, is gradually flowing into labor markets, suppliers, and especially retail portfolios, pulling the risk asset curve toward the crypto space.

-

New Major Buyers in Crypto: Treasury companies (e.g., MicroStrategy's investment in BTC; Bitmine and others investing in ETH) act as bridges between public equity capital and spot tokens. These structural buyers represent a critical factor missing in previous cycles.

-

Macro Crosscurrents Remain Contained—For Now: Despite sticky inflation risks (tariffs, wages, dollar) and signs of labor market softening, productivity optionality from AI and favorable crypto regulation continue to compress risk premiums.

1) AI at the Top of the Pyramid

-

Capital Gains → Risk Rotation: As S&P 500 valuations run high (elevated forward P/E), retail investors rotate into loss-making tech stocks, short-squeeze baskets, and crypto assets.

-

Capex as Liquidity Source: Record-level spending by hyperscalers acts like a private-sector liquidity pump, channeling funds to suppliers, employees, and shareholders, which then recycle back into markets.

-

Side Effect: AI infrastructure buildout (data centers, chips, power) shows up immediately as investment growth, while productivity gains lag. Lag → Wealth effect is immediate.

2) Crypto Treasury Companies (TCos) = Digital Asset Treasuries (DATs)

-

From "Generation Zero" to Price-Seeking TCos: Early TCos (like Michael Saylor’s strategy) acted as price-insensitive floor support. The new generation focused on ETH are more price-sensitive, capable of defending key price levels and driving breakouts while accelerating upstream equity value.

-

Reflexive Loop: Equity financing → Buying reserve assets (BTC/ETH) → Token prices rise → TCo equity value increases → Lower cost of capital → Repeat. This is the so-called "flywheel effect".

-

Achilles’ Heel: Gaps between key levels. If ETF treasuries or retail capital fail to fill these gaps, failed breakout attempts force TCos to conserve cash, leading to rapid price drawdowns.

3) Tailwinds from Policy and Market Positioning

-

Favorable Crypto Policy: Deregulation and friendlier regulatory stances in crypto have opened channels for traditional financial capital inflows.

-

Tariff "Resolutions" Are Illusory: Firms still lack clarity on exemptions and court rulings related to China, Mexico, Canada, and USMCA. This uncertainty pushes corporates toward financialization over Capex—more money flows into asset markets.

Ethereum’s Current State (and Why It’s Bouncing Back)

-

Treasury Demand + ETF Inflows: Combined treasury demand and ETF inflows provide ETH with a new narrative turning point, enabling a comeback after years of underperformance relative to L2s.

-

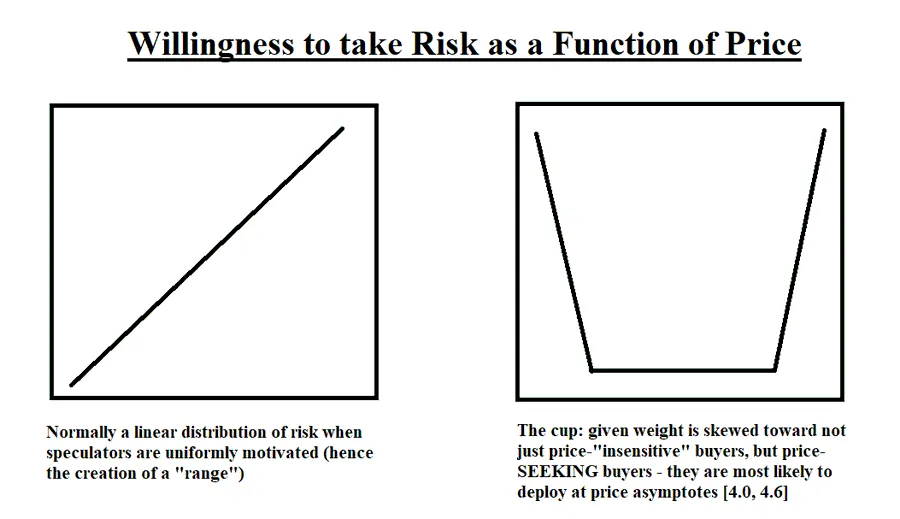

Through the "Cup Theory" Lens: Price-seeking ETH treasury firms defend the $3,000 level and push prices toward $3,300–$3,500 → $4,000; ETF flows fill the gaps. If ~$27B in pending demand materializes in stages, the current uptrend may persist; if not, gap vulnerability becomes critical.

-

Interpretation: ETH now has a fundamentally different buyer base than past cycles. It's no longer "retail vs miners", but "ETF + TCos vs liquidity gaps".

Image source:

https://x.com/lazyvillager1/status/1956414334558478348

Macro: The Wall of Worry (and Why Markets Climb It)

Inflation

-

Channel Pressure via Surveys: Sales price indexes have risen for three consecutive months (highest since August 2022), indicating goods-driven price pressures consistent with tariff pass-through, a weaker dollar, and sticky wages.

-

Interpretation: Implied inflation near ~4% isn’t crisis-level, but complicates rate cuts. The Fed can only tolerate growth-friendly inflation if the labor market shows no clear cracks.

Labor Market

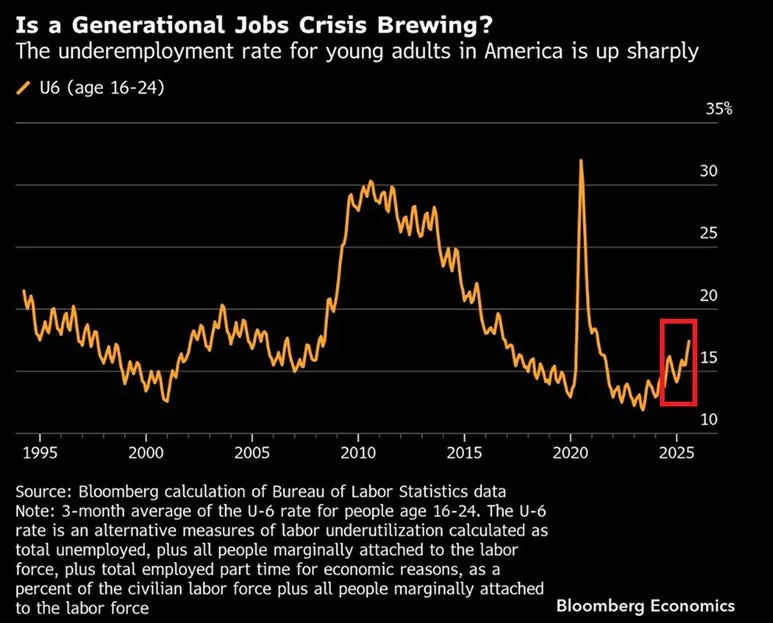

-

Youth Underemployment Rate surges (~17% 3-month average), an early-cycle warning sign. Young workers feel economic shifts first; if this spreads to core employment, risk assets will suffer.

Growth, Debt, and AI

-

AI as Fiscal Offset: If AI boosts total factor productivity (TFP) by 50 bps annually long-term, public debt-to-GDP could fall to ~113% by 2055 versus a baseline of 156%, with real per capita GDP ~17% higher. In short, AI is the only credible growth lever strong enough to bend the debt curve.

-

But Timing Is Critical: Just as computer Capex in the 1980s didn’t lift productivity until the late 1990s, AI’s broad efficiency gains will take time. Markets are pricing in future gains today.

Tariffs and Uncertainty

-

Policy Fog = Valuation Risk: Undetermined tariff rates, ambiguous trade deals (e.g., EU/Japan), shifting exemptions, and legal disputes create uncertainty around future cost curves. This pushes CFOs toward financial assets over long-term physical investments—supporting markets short-term while increasing medium-term inflation risk.

Bearish vs Bullish: My Assessment Factors

Bearish Factors

-

Declining Treasury General Account (TGA) balance + Quantitative Tightening (QT) remains restrictive.

-

Seasonal weakness persists through September.

-

Early signs of labor market loosening; inflationary pressures (tariffs/wages).

Bullish Factors (Weighted More Heavily)

-

AI Capex + wealth effect serve as current liquidity sources.

-

Pro-crypto policy shift opens the floodgates for TradFi capital flows.

-

Crypto treasury companies / ETF structures act as sustained mechanical buyers.

-

2026 Fed composition leaning dovish is a credible long-term catalyst.

Summary: I remain constructive as long as the chain from AI → retail → crypto treasuries → spot markets remains intact.

What Could Change My View:

-

Decline in Hyperscaler Capex: Clear drop in AI infrastructure orders.

-

Stalled ETF Demand: Persistent outflows or failure in secondary issuance.

-

Closure of Crypto Treasury Company Equity Markets: Down rounds, failed ATM offerings, or collapse of NAV premium.

-

Labor Market Cracks: Youth employment weakness spreads to prime-age workers.

-

Tariff Shock → CPI: Goods inflation forces the Fed to tighten again instead of cutting.

Positioning Within the Cycle (Not Financial Advice)

-

Core Strategy: Focus on high-quality AI growth companies; selectively invest in "tools and infrastructure" (compute, energy, networking).

-

Crypto Assets: Bitcoin as systemic risk exposure for risk assets; Ethereum as a self-reinforcing reflexive flywheel. Watch key defense levels and anticipate potential inter-market gaps.

-

Risk Management: Adjust positions based on ETF flow data, TCo issuance schedules, and hyperscaler guidance. Add at key support; trim on euphoric breakouts lacking follow-through.

Core Summary

This cycle is fundamentally different from 2021.

It is powered by private-sector liquidity from AI equity gains and Capex, channeled into crypto via new corporate structures and validated and amplified by ETFs.

The growth flywheel is real: It will keep spinning until the hyperscalers at the top of the pyramid falter.

Until then, the path of least resistance remains upward and climbing

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News