How to Make American Stocks Great Again?

TechFlow Selected TechFlow Selected

How to Make American Stocks Great Again?

The stock market no longer waits for the bell to ring, and investing no longer requires broker permission.

By: 1912212.eth, Foresight News

Buying U.S. stocks is a bet on America's national fortune. If you had invested $10,000 in the S&P 500 index in 2002, it would now be worth $85,900. If that same $10,000 had been invested in the Nasdaq index, you might have received a return of $114,900.

As the world’s largest securities market, U.S. equities have rarely disappointed investors. Yet, investors in many countries and regions around the globe still lack access to such assets, missing out on wealth opportunities.

What if buying these assets no longer required an account and was not limited by geography or trading hours? Imagine being able to purchase "shares" of major U.S. stock giants anytime, anywhere, using just a smartphone and a crypto wallet balance. This is no longer a fictional scenario—it’s the real transformation brought by “tokenized U.S. stocks.”

In the next era, stock markets won’t wait for opening bells, and investing will no longer require placing orders through brokers.

Tokenization, simply put, is the process of converting real-world assets into programmable, tradable digital tokens. These tokens are built on blockchain technology and typically comply with standards like ERC-20, ensuring transparency and security. Tokenized U.S. Stocks refers to mapping or anchoring shares of U.S.-listed companies (such as Apple, Tesla, etc.) onto a blockchain, enabling them to be traded, transferred, and held on-chain just like cryptocurrencies.

In short, replicating traditional stocks within the blockchain world, turning equities into “on-chain assets.” For example, a single share worth tens of thousands of dollars can be fractionalized into thousands of smaller units, allowing ordinary investors to participate with low barriers. Benefits of tokenization include 24/7 trading, reduced intermediary costs, and enhanced liquidity, though challenges remain around regulatory uncertainty and technical risks.

For investors, tokenized U.S. stocks lower investment thresholds. For companies, motivations to explore tokenization stem from multiple factors. Liquidity bottlenecks in traditional financial markets are increasingly evident, especially during non-trading hours. Additionally, institutional investors like BlackRock and JPMorgan view tokenization as a tool to reduce financing costs. Improving regulatory environments provide policy support for this trend.

So why is the wave of tokenization sweeping into U.S. equities?

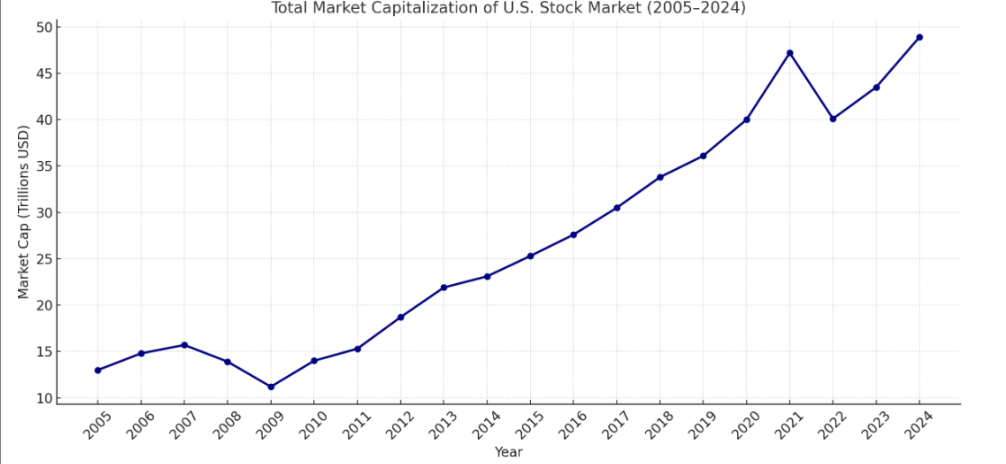

U.S. stocks possess unique advantages unmatched by other asset classes. First, as the world’s largest stock market, the total market capitalization of U.S. equities reached between $52 trillion and $59 trillion in 2025—far exceeding that of any other country or region. In 2025, global stock market capitalization stood at approximately $124 trillion, with U.S. equities accounting for over 40%.

High returns are another key factor. The S&P index recently hit a record high of 6,336 points. Since 1957, the S&P 500 has delivered an average annual return of about 10.4% (approximately 6.5% after inflation adjustment), with average annual returns of 10.364% over the past 20 years and 9% over the past 30 years. For non-U.S. investors, the barrier to investing in U.S. stocks remains high. Traditional investment requires opening a brokerage account, meeting minimum investment thresholds, adhering to trading hours (only 9:30–16:00 ET on weekdays), and navigating complex cross-border regulations and tax requirements—especially burdensome for overseas investors due to cumbersome account setup processes and high fees.

The Surge Begins

Retail investors are bypassing traditional barriers and flocking to tokenized U.S. stocks for wealth gains—but what about institutional moves? Crypto exchanges, on-chain protocols, and online brokerages are all preparing to enter the space.

On May 22, cryptocurrency exchange Kraken partnered with Backed Finance to launch a tokenized stocks and ETF trading service called “xStocks,” initially covering over 50 U.S.-listed stocks and ETFs including Apple, Tesla, and NVIDIA.

Another crypto exchange, Bybit, chose to enter the U.S. stock market by partnering with Swarm. Notably, neither Kraken nor Bybit issues stock tokens themselves; instead, they enter via third-party collaborations. Entities actually issuing stock tokens include Backed Finance and Securitize. The former collaborates with protocols like Uniswap under MiFiD and Swiss DLT regulations to offer freely transferable tokenized stocks tradable on-chain. Securitize partners with major institutions such as BlackRock and VanEck to provide end-to-end tokenization services.

However, the most talked-about and closely watched projects in the crypto space are institutional platform Ondo Finance and well-known U.S. brokerage Robinhood.

Ondo Finance is an institutional-grade platform focused on tokenizing traditional financial assets and bringing them onto blockchains. It is currently the most recognized and product-comprehensive project among launched RWA initiatives. Ondo’s flagship product, USDY, represents tokenized U.S. Treasuries, with total TVL reaching $1.39 billion. However, market response has been lukewarm, and its token price has steadily declined from $2 to hover around $0.7.

With the surge in interest in tokenized U.S. stocks, Ondo has become more active: in early July, it first partnered with Pantera Capital to invest $250 million toward advancing RWA tokenization, then acquired Oasis Pro—a SEC-regulated broker—on July 4 to obtain a series of U.S. securities licenses. Ondo also announced plans to launch tokenized stock trading within the coming months.

In just one month, Ondo has become notably aggressive in its push into tokenized U.S. equities.

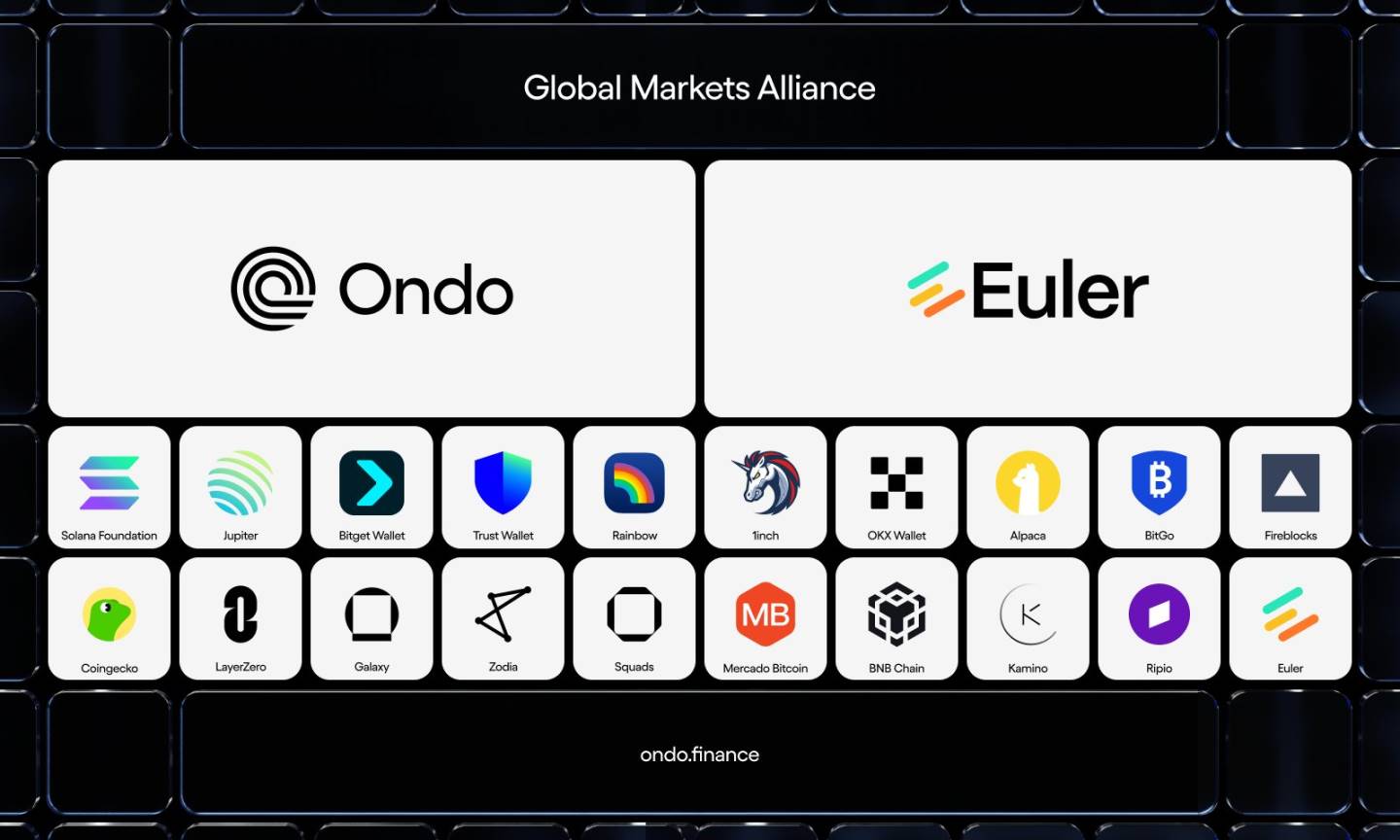

On July 10, Ondo acquired Strangelove to accelerate development of a full-stack RWA platform and recently launched a Global Market Alliance, collaborating with public chains, DEXs, wallets, data providers, cross-chain protocols, and DeFi products to unify industry standards.

It’s foreseeable that once Ondo launches tokenized U.S. stocks, its strong resource integration capabilities will spread these offerings across every corner of the crypto market, allowing crypto users to easily buy tokenized U.S. equities.

Robinhood has also entered the arena directly, becoming the first U.S. publicly traded brokerage to embrace stock tokenization.

This player, which disrupted the traditional brokerage industry with its zero-commission model, attracted a large number of young investors—especially millennials—with its low barriers and user-friendly interface. Its average user age is 35, managing 25.8 million funded accounts and $221 billion in assets.

In June this year, Robinhood launched over 200 on-chain stock tokens, even introducing tokenized equity for OpenAI and SpaceX, gifting eligible users $5 worth of OpenAI tokens each.

Robinhood co-founder Tenev stated bluntly that the fundamental problem in private markets is that top-tier companies have too many options and don’t naturally consider retail investors, leading to “adverse selection.” The key innovation of tokenization lies in functioning “without requiring the company itself to opt in”—a breakthrough that Robinhood is pushing forward.

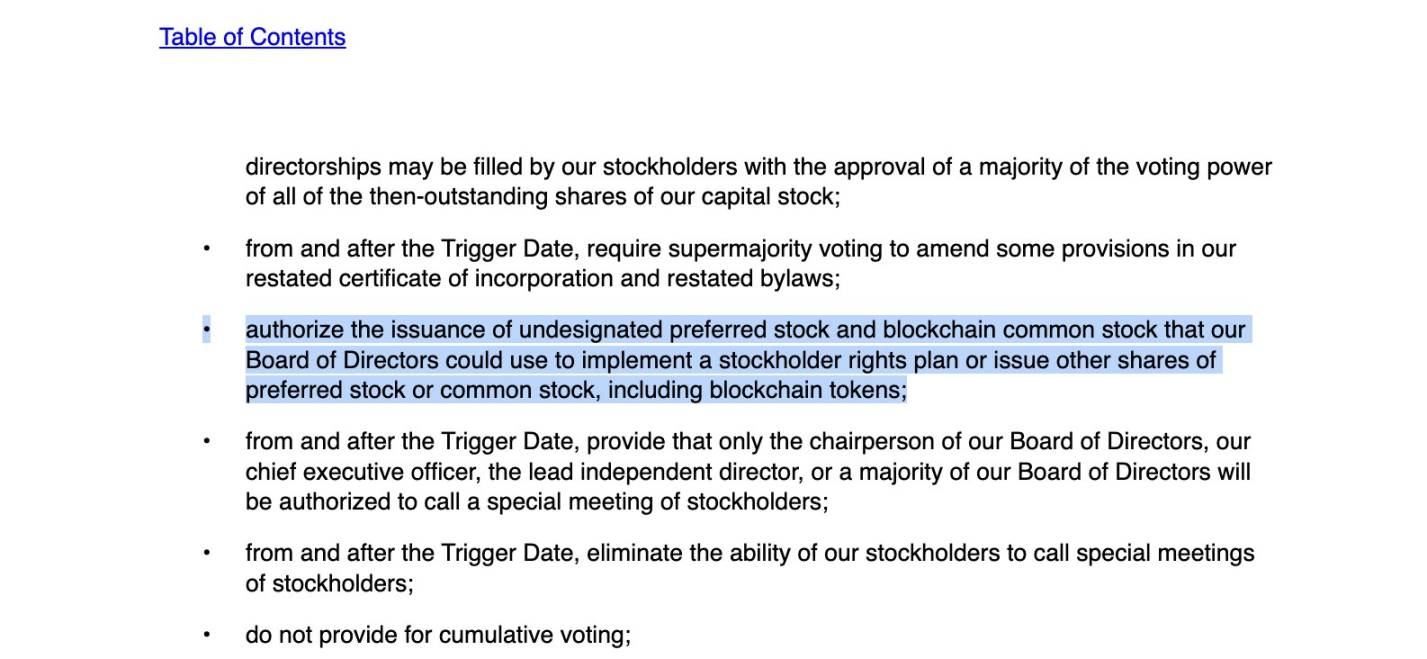

On July 21, design software giant Figma filed a revised S-1 form for its IPO. Beyond confirming the IPO price range, the updated filing notably specified that the company has formally authorized a new class of “blockchain common stock,” granting its board the power to issue shares as blockchain tokens in the future. In a sense, this allows institutions to reach global potential investors through borderless blockchain platforms, expanding their pool of potential buyers.

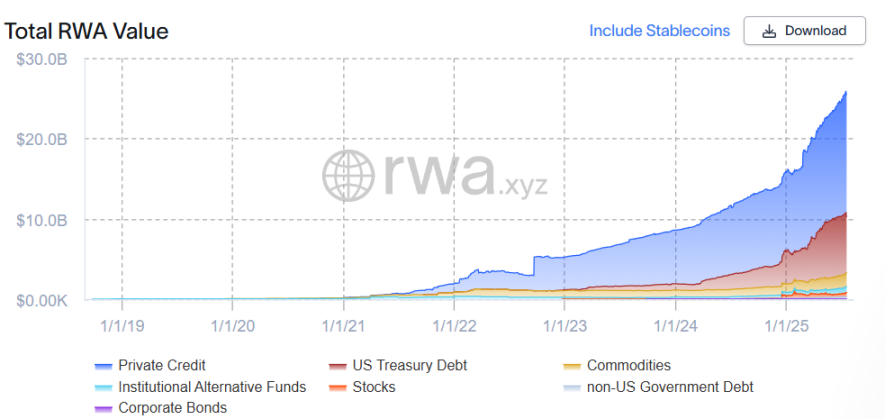

In the first half of 2025, tokenized U.S. stocks on-chain moved from concept to reality. According to data from rwa.xyz, total TVL rose to $530 million, while monthly active addresses surged to 70,000.

The penetration of tokenization from pure crypto into traditional finance: no longer just a speculative tool, but a bridge to greater efficiency.

Leaving the Wild West Behind

The current booming wave of tokenized U.S. stocks isn’t new—it’s the result of past innovations paying their dues.

Early attempts at tokenizing U.S. stocks trace back to decentralized protocol experiments in the previous cycle. Synthetix was one of the earliest platforms supporting synthetic stock assets, allowing users to hold tokens like sTSLA and sAAPL on-chain to mirror U.S. stock price movements. However, these assets lacked backing by actual shares, relying solely on collateral mechanisms and oracle price feeds, resulting in fragile liquidity and de-pegging risks. Statistics show that sTSLA on Synthetix accumulated fewer than 800 trades before most such projects pivoted due to regulatory pressure and unsustainable business models.

Despite lacking shareholder rights, this model opened the door for crypto assets to represent real-world assets. Using oracles for pricing and bypassing traditional custodianship, it provided a reference framework for later entrants.

Meanwhile, centralized exchanges became early drivers of U.S. stock tokenization. In 2020, FTX partnered with German licensed broker CM-Equity to launch tokenized stocks for Tesla and Apple, allowing non-U.S. users to trade 24/7, with underlying real stocks held in custody. In 2021, Binance followed suit by launching “stock tokens,” enabling users to trade Tesla and other assets commission-free using USDT.

However, these models were essentially derivatives within CEXs, lacking on-chain transparency and regulatory compliance, quickly drawing warnings from regulators in multiple countries. FTX saw $94 million in quarterly trading volume for tokenized stocks in Q4 2021, but the service abruptly ended with the platform’s 2022 collapse. Binance discontinued its product after only three months under regulatory pressure.

While the vision was attractive, reality proved harsh. The 2022 FTX collapse became a turning point for tokenized U.S. stocks, shifting the market from “unregulated growth” to “compliance-driven restructuring.”

These cases exposed the core conflict of early tokenized U.S. stocks: a misalignment between technical feasibility, compliance costs, and market demand. Nonetheless, these efforts laid the foundation for today’s more compliant and structured tokenization attempts, helping the market recognize the potential of moving assets on-chain.

Genuine on-chain U.S. stock assets re-emerged on the agenda after 2022 as the RWA concept gained traction. This wave includes projects like Backed Finance, which operate in relatively favorable jurisdictions such as Switzerland and Liechtenstein, using a “1:1 custody + verifiable reserves + on-chain issuance” model to map real holdings of U.S. equities into ERC-20 or similar standard tokens, offering stronger compliance and traceability.

In 2024, Exodus Movement became the first U.S. public company to tokenize its common stock, issuing EXOD tokens on the Algorand blockchain, allowing users to convert between on-chain tokens and NYSE-listed shares at a 1:1 ratio. This marked a shift in the SEC’s stance toward on-chain stocks, although the tokens only support price tracking and do not include voting rights or other shareholder benefits.

Challenges and Risks

An opportunity-rich field always comes with accompanying risks. Liquidity for on-chain U.S. stocks remains a major challenge.

On July 3, the Apple-tracking token AAPLX briefly surged to $236.72, a 12% premium over the stock’s actual trading price. Similarly, a token tracking Amazon spiked to $891.58 on July 5—four times the stock’s previous closing price. An even more extreme case occurred on the peer-to-peer crypto platform Jupiter. Blockchain data showed that on July 3, an unidentified user attempted to buy about $500 worth of the Amazon token AMZNX, briefly pushing its price to $23,781.22—over 100 times Amazon’s prior day closing price.

“xStocks,” issued through partnerships between Backed Finance and Kraken, primarily enables tracking of multiple stock-linked tokens. However, due to thin trading volumes across multiple crypto exchanges, xStocks are prone to sharp price swings when trades exceed market depth. These fluctuations may intensify during nights and weekends when traditional markets are closed.

Market liquidity, oracle reliability, and potential manipulation concerns have deterred many would-be participants in on-chain U.S. stocks.

Additionally, user rights protection has drawn market attention. After Robinhood announced its OpenAI equity tokens, OpenAI quickly responded on X: “These ‘OpenAI tokens’ are not OpenAI equity. We are not partnering with Robinhood, nor are we involved or endorsing it. Any equity transfer requires our approval—we haven’t approved any. Please proceed with caution.”

Elon Musk joined in mocking: “Your ‘equity’ is fake.” Regulators such as Lithuania’s central bank launched investigations, the SEC warned of potential violations, and Robinhood’s stock price reversed into decline. Bernstein analysts noted the company is betting on SEC policy support and the passage of the CLARITY Act to open up the tokenized asset market.

Facing intense controversy, Robinhood CEO Vlad Tenev recently said in an interview that reactions from OpenAI and SpaceX, while understandable, are unfair. He used a vivid analogy: this is like “digital NIMBYism”—in principle, everyone supports tokenization, but when it happens to them, the appeal fades. What people truly want isn’t complex financial tools, but “capital as a service”—press a button, and money flows into your account, he said.

Whether underlying market demand can sustain a major on-chain stock sector remains questionable. A seasoned investor told Foresight News: “Doing U.S. stocks on-chain means finding U.S. stock investors within the crypto community. But crypto users, accustomed to 24/7 global trading and frequent high volatility, may not have a significant overlap with those interested in U.S. equities.”

He added: “For non-crypto users, learning about on-chain wallets just to trade U.S. stocks is also a barrier.”

Another challenge stems from regulation—finance being a heavily regulated domain.

Recently, SEC Chair Paul Atkins indicated the agency is considering a “crypto innovation exemption” policy to incentivize progress in tokenization.

But this is far from a foolproof shield.

When Apple stock is “copied” onto a blockchain, who ensures it genuinely represents shareholder rights? Who handles disclosure, compliant trading, and anti-money laundering? Under U.S. securities law, any issuance or transfer of securities must be registered or qualify for exemption, yet the decentralized nature of on-chain assets fundamentally clashes with traditional compliance logic.

In a recent statement on tokenized securities, the U.S. SEC said: “Tokenization has the potential to facilitate capital formation and enhance investors’ ability to use their assets as collateral. However, despite the great promise of blockchain technology, it does not possess ‘magic’ to change the fundamental nature of the underlying asset. Tokenized securities are still securities. Therefore, market participants must carefully consider and comply with applicable federal securities laws when dealing with such instruments.”

Once involving cross-border custody, lack of KYC, or directing liquidity to unregistered platforms, tokenized U.S. stocks could easily be deemed illegal securities offerings by the SEC. This presents a test for innovators and a blind spot for regulators—one that cannot ignore the space, yet struggles to govern new paradigms with old rules.

Hence, how future tokenization firms and protocols navigate this gray regulatory zone—“dancing in shackles”—has become an unavoidable critical issue.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News