The End of the 60:40 Portfolio? How Inflation Is Reshaping Asset Allocation Logic

TechFlow Selected TechFlow Selected

The End of the 60:40 Portfolio? How Inflation Is Reshaping Asset Allocation Logic

The key to understanding wealth management and asset valuation lies in inflation.

Author: Michael Howell

Translator: Block unicorn

Asset allocation is typically conducted in a vacuum, with little consideration given to the monetary policy environment investors will face. The standard approach builds a portfolio split 60:40 between equities (risky assets) and high-quality bonds (safe assets). The rationale is that these two asset classes are often negatively correlated—especially during economic recessions.

While this thinking forms the bedrock of modern wealth management, it has only been valid during specific periods and under unique circumstances—specifically from the early 1980s through the 2008/09 Global Financial Crisis (GFC). It did not hold in the 1970s, and arguably does not apply today.

The key to understanding wealth management and asset valuation lies in inflation. Simply put, while we all clearly want to grow wealthier, our primary concern should at least be maintaining real wealth levels. Assets should not be compared against each other (such as bonds versus stocks), but rather against inflation.

Inflation may be a difficult concept to measure precisely, but for illustration, assume it represents the loss of purchasing power in paper currency. Inflation can stem from monetary inflation—that is, “money printing”—or from cost-driven inflation, such as rising oil prices or declining productivity.

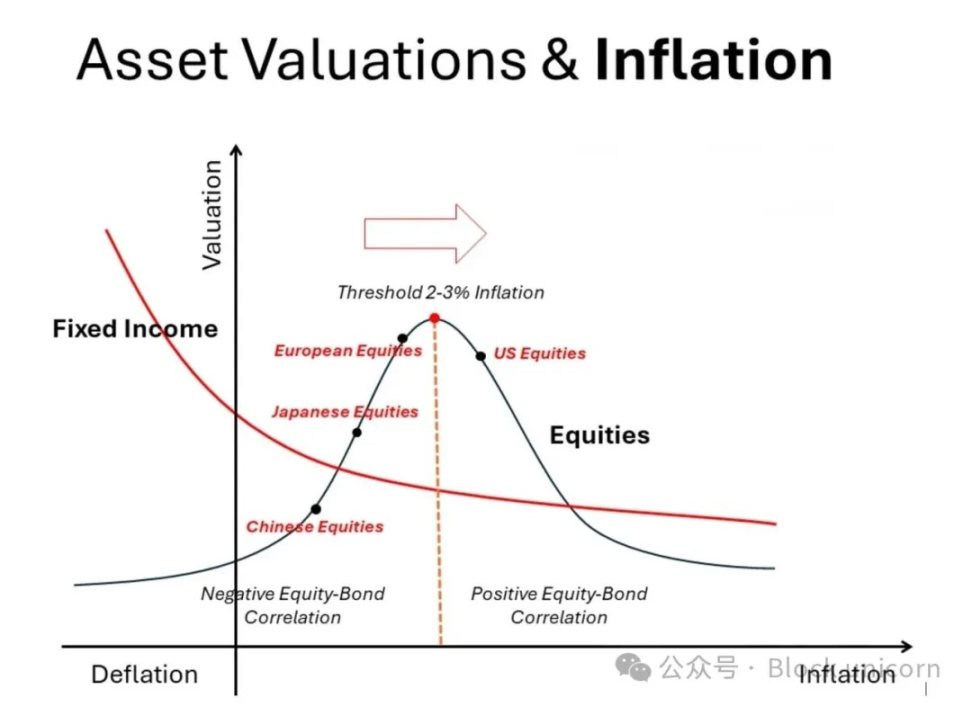

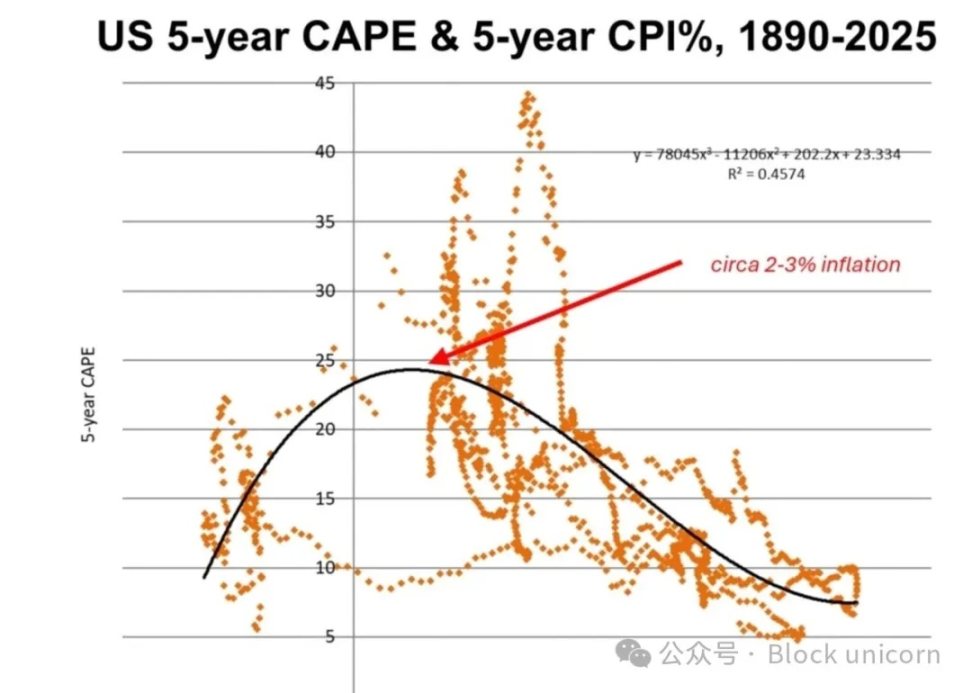

The chart below illustrates how inflation affects the valuation of different asset classes. While schematic in nature, this chart can be empirically constructed using long-term data published by academic Robert Shiller on his website. We use data from 1880 onward to present our version below. Curves are fitted using polynomial regression.

High-quality bonds (such as U.S. Treasuries) exhibit a monotonic relationship: as inflation accelerates, their valuations fall (yields rise); as deflation approaches, valuations rise (yields fall). This trade-off is acknowledged in textbooks. Real assets (not shown in the chart)—such as residential real estate, land, gold, and perhaps Bitcoin—follow the opposite path entirely. As inflation rises sharply, their valuations and prices increase accordingly.

In contrast, the relationship between equities and inflation is more complex and nonlinear—a fact not covered in finance textbooks. On either side of a 2–3% inflation "sweet spot" (where price-to-earnings valuations peak), both rising and falling inflation lead to lower valuations. In other words, to the left of this valuation peak, stocks and bonds are negatively correlated (“risk parity” zone), while to the right, they become positively correlated. This shift in correlation patterns demands significant adjustments in portfolio construction.

Since the 1980s, most of our investment experience has occurred in the “low” inflation region—centered around and mostly to the left of this valuation peak. This strongly supported heavy allocations to equities, and even small changes in inflation justified holding bonds due to their negative correlation with stocks. [Note the divergence between stock and bond valuation lines.] This was especially evident during periods of economic weakness or when deflationary pressures emerged. Japan’s history demonstrates what happens to stock and bond valuations within an “ultra-low” inflation regime.

But this was not characteristic of the inflationary 1970s. Back then, real assets were favored, while financial assets performed poorly. The same chart reveals why. To the right of the valuation peak—at inflation rates around 2–3% and above—both stock and bond valuations decline. And they do so simultaneously. This correlation undermines the rationale for holding both assets in a portfolio. Conversely, the inverse and positive performance of real assets relative to inflation strengthens the case for including them.

Rising Monetary Inflation

Our recent research has focused on the accumulation of monetary inflation risk—namely, governments deliberately devaluing paper currencies. [We remain neutral on cost-driven inflation.] A rightward arrow in the chart serves as a reminder. In short, the 60:40 asset allocation (or “risk parity” approach) faces a serious threat. Going forward, investors should now consider reducing bond holdings and increasing exposure to real assets.

To be sure, our chart shows the right tail of the equity valuation bell curve dipping below the bond valuation line. Of course, this isn't always the case. Unlike fixed bond coupons, corporate earnings and dividends can rise with inflation. Different stocks will behave differently, as some are better inflation hedges than others and thus may maintain relatively higher valuations. On the other hand, many companies struggle to maintain profitability in high-inflation environments. However, here we discuss general trends, not granular details.

Global bond yields are gradually rising. This move is driven more by increasing term premiums than by higher policy rates. This suggests rising yields may reflect growing inflation uncertainty and concerns over greater issuance of government debt due to high fiscal spending.

Looking across markets, we believe the U.S. currently faces greater inflation uncertainty—due both to its large fiscal deficits and rising expectations of “sales taxes” from tariffs. More importantly, the deficit is increasingly financed via short-term securities, which raises the risk of monetary inflation.

Japan has recently experienced rising inflation, primarily driven by wage growth—but this follows decades of deflation and intermittent disinflation. In other words, placing Japan on the chart above, its equity valuations could potentially rise toward the 2–3% inflation “sweet spot.” Clearly, at current low levels, a 1.5% yield on Japanese Government Bonds (JGBs) looks unattractive in real terms.

China is currently in a deflationary phase following tariff shocks, possibly at an earlier stage than Japan. Chinese equities are cheaply valued, but further monetary stimulus and stronger economic fundamentals could easily shift investor sentiment back toward stocks.

Meanwhile, European equities, by inflation standards, are close to the ideal “sweet spot,” positioning them between U.S. and Asian markets. In other words, if inflation continues to rise (which we believe will lead the world into stagflation), European equity valuations are more likely to follow the U.S. path—gradually being marked down.

Asset Allocation Implications

The 60:40 or “risk parity” model, long beloved by wealth managers, faces severe challenges in a monetary inflation environment. We lean toward reducing bond allocations, or at minimum shifting part of the bond portfolio into inflation-linked bonds (TIPS).

Portfolios should be tailored to individual investors, but taking the 60:40 financial asset benchmark as an example, we prefer a strategic shift toward 60:10:10:10:10. Here, 10% might go to TIPS; 10% held in cash; 10% added to gold and precious metals; and 10% allocated to Bitcoin. We exclude dedicated real assets such as prime residential real estate and land—not because they lack appeal, but because of their low liquidity and the fact they are often permanent, non-tradable components of an investor’s wealth.

Moderate inflation increases could benefit overall equity markets. Our chart above depicts nominal positioning across markets. Arguably, Wall Street has already passed its peak due to inflationary pressures in the U.S. economy. European inflation remains mild, while China and Japan are emerging from deflation/low-inflation environments—conditions favorable to bonds rather than stocks. Investment in these Asian markets may be worthwhile, though investors must remain cautious of heightened geopolitical risks.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News