OKX Children's Day Special: Unveiling the "Crypto Kids" Development Plans of Ten Crypto Influencers

TechFlow Selected TechFlow Selected

OKX Children's Day Special: Unveiling the "Crypto Kids" Development Plans of Ten Crypto Influencers

Bitcoin is not just an asset, but also the greater optionality we leave for the next generation.

Ten years ago, Bitcoin was a tech novelty; ten years later, it has become a global value consensus.

If buying Bitcoin was important ten years ago, today "leaving your child some Bitcoin" might be the most forward-thinking decision.

A property may face purchase restrictions, depreciation, or even obsolescence over time; but one Bitcoin is a free asset that transcends borders and resists risks.

It's not just an asset—it’s giving our next generation greater choices: more possibilities and lives not defined by any system in the future world.

As Children's Day approaches, let’s explore from the real-life perspectives of industry practitioners, together with OKX, a bold yet realistic question:

How do top crypto dads pass down their Bitcoin—and how can “crypto kids” get ahead from day one?

1. @Cobie (Co-founder & CEO of Cobo)

Q: For you, is “leaving your child some Bitcoin” more of a belief or a hedge? Many worry it’s too late to enter now—what’s your view on the right timing for ordinary people to get involved?

A: I used to think this way—planning to leave some BTC for my child. But this year, my view has shifted: excessive crypto wealth could weaken his curiosity and sense of responsibility. I’ll only use a small amount of Bitcoin as a safety net, while treating curiosity and values as my true family legacy.

For ordinary people, entering the crypto world isn’t about being “early or late,” but whether you’re willing to grow alongside the industry cycle. Today’s market infrastructure, regulations, and application ecosystems are far stronger than before, increasing survival odds while shrinking space for windfall profits. Latecomers should: first assess their risk tolerance and cash flow to determine a sustainable long-term position; use dollar-cost averaging instead of lump-sum investments to turn timing risk into time-based gains; treat buying crypto as acquiring a learning ticket—follow technological progress and experience real applications so that knowledge and assets grow together. In this way, missing the early stage doesn’t mean losing opportunity; participating with clearer insight gives you a steadier compounding curve rather than volatile spikes and crashes.

2. @Nisen (Top-tier KOL)

Q: How do you see more and more people who once called Bitcoin a scam now quietly starting dollar-cost averaging? Some say “trading gold preserves value, trading Bitcoin is about the future”—do you agree? If a parent unfamiliar with crypto asked you: “Can I really leave Bitcoin for my child? Is that reliable?”—how would you respond?

A: As a long-term BTC investor using dollar-cost averaging, I deeply believe in BTC’s future. Compared to gold, BTC’s safe-haven feature isn’t strong yet due to its high price volatility. However, as BTC moves further into regulated spaces and more high-net-worth traders adopt it in their strategies, I believe BTC’s future will be brighter.

One thing I’d add: data already shows that over long periods, BTC consistently flows into the hands of long-term, high-net-worth investors. 13F filings and spot ETF data both indicate that U.S. high-net-worth individuals and institutions are holding more BTC. This fuels a herd effect around DCA. Since my first BTC purchase in 2018, I’ve kept increasing my position, investing monthly via DCA. These BTC holdings are the best gift I can leave for Hualishu (my son). I believe BTC will deliver greater financial value in the future.

3. @UNICORN (Top-tier KOL)

Q: “Leaving your child a house is less valuable than leaving them one Bitcoin”—do you find this claim credible? Or how would you interpret the anxiety and hope behind it? Do you think Bitcoin will take on a formal, stable role in household portfolios in the coming years?

A: In terms of upside potential, Bitcoin has shown enormous growth and near-limitless potential. For example, reaching $1 million per coin—but this will take time, possibly many years. A house worth $1 million today may have limited appreciation compared to Bitcoin, but it holds value now. So perhaps we should rephrase it: “Leave 10 Bitcoins instead,” which sounds more reasonable.

It depends on the family. The world rewards those who embrace new things first. For me, Bitcoin is already part of my household assets. But if one day billions of families treat Bitcoin as a standard, stable component of their portfolio, then its massive growth potential may end—turning it into an asset like gold, appreciating less than 30% annually. At that point, I’d probably start looking for the next high-growth asset.

4. @Mandy (Founder of Odaily Planet Daily)

Q: From a media perspective, how do you view Bitcoin’s “reputation reversal” over the past decade? Is it now time to seriously discuss including Bitcoin as part of household assets?

A: Bitcoin’s “reversal” reflects mainstream society’s evolving recognition of its value. Ten years ago, it was seen as a fringe technology challenging regulation. Now, exchanges are going compliant, multiple countries have established clear regulatory frameworks, and the U.S. Bitcoin ETF has achieved hundreds of billions in trading volume. This represents institutional acceptance of Bitcoin’s underlying logic and its formal inclusion in the global asset allocation system. When Wall Street enters and policymakers begin regulating, Bitcoin transforms from a “rebel” into part of the “establishment.” It hasn’t changed—rather, the world is making peace with it on its own terms.

Yes, especially from a global perspective, this is no longer a niche topic but a real consideration. With soaring inflation, frequent wars, and currency devaluations across many countries, the “cross-system security” of household assets is becoming increasingly vital. As a decentralized asset independent of any single sovereignty, Bitcoin offers a logically sound alternative. More importantly, its fixed supply, growing institutional adoption, and expanding global consensus continue to support its scarcity-driven value over the long term. It’s not a panacea, but within diversified portfolios, it deserves a rational, long-term place.

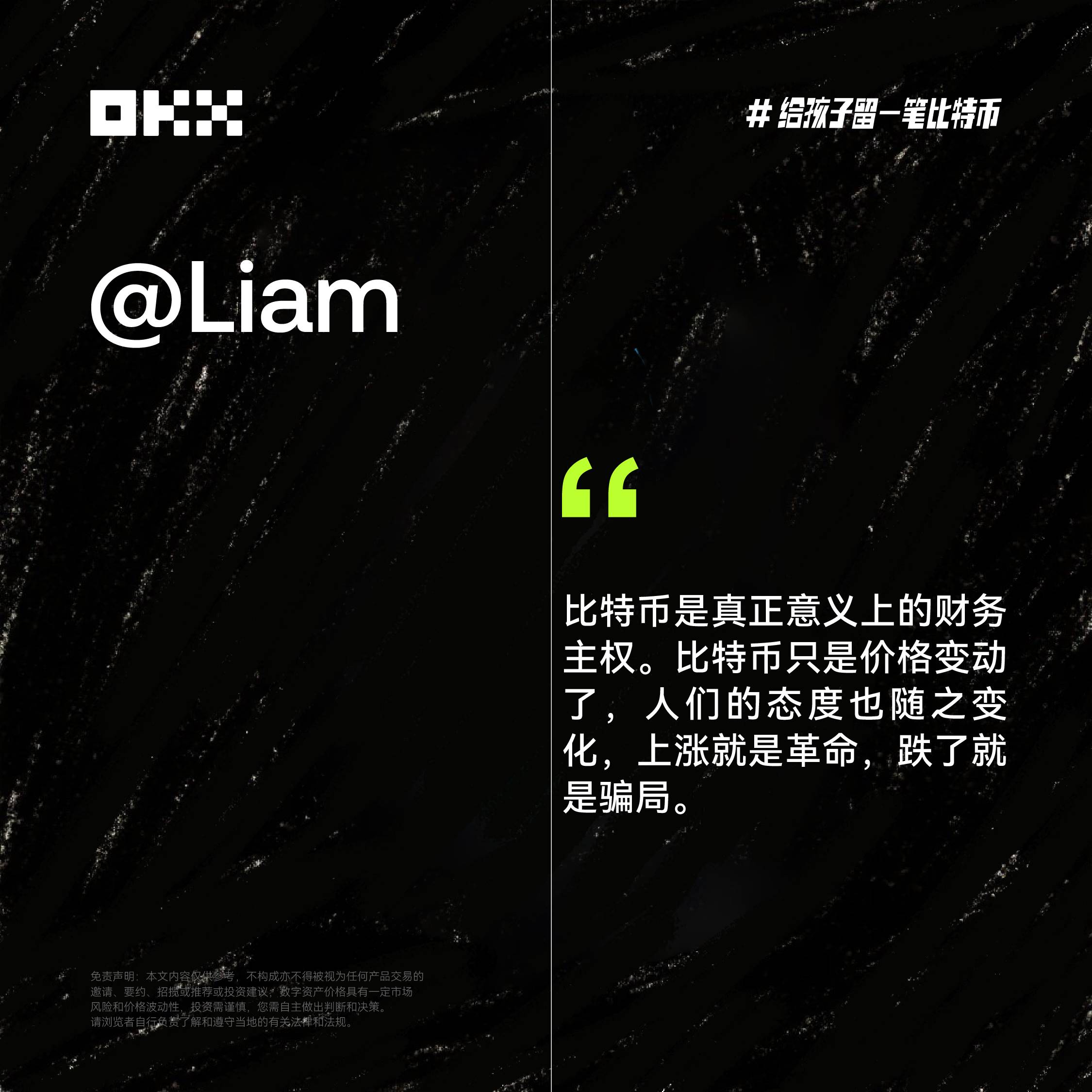

5. @Liam (Founder of TechFlow)

Q: As a seasoned media professional, what has Bitcoin “changed” over the past decade, and what has remained “unchanged”? What does Bitcoin truly mean to you? What’s your personal trading logic and allocation strategy?

A: What changed is mainly the external environment. Ten years ago, Bitcoin was a geek toy; today, it’s part of global public companies’ investment portfolios—evolving from a niche experimental project to a mainstream asset, with prices rising from a few dollars to over $100,000. Meanwhile, the ecosystem around Bitcoin has matured significantly—from trading infrastructure to derivative applications—spawning an entirely new digital economy.

What remains unchanged is the core. Bitcoin’s fundamental principles—like the 21 million cap and PoW mechanism—have never changed. More importantly, its narrative around fighting inflation and protecting financial sovereignty has not weakened over the past decade; rather, it’s been repeatedly validated and strengthened during global financial turmoil. See, Bitcoin is still Bitcoin—the price changes, and so do people’s attitudes. When it rises, it’s revolutionary; when it falls, it’s a scam. Life is similar: when your life chart goes up, you hear praise and cheers; when it drops, you face accusations of fraud. Stay strong, and everything strengthens. Be like Bitcoin.

When I first learned about Bitcoin, Li Xiaolai’s words struck me deeply: Bitcoin is the first time in human history that technology has made private property sacred and inviolable. To me, that’s Bitcoin’s value—true financial sovereignty. So for me, Bitcoin is essentially emergency money. And I also embrace the idea of “saving enough Bitcoin for the next generation,” treating it as a legacy—provided there *is* a next generation. I’ve suffered too much: once lost a large amount of BTC when an exchange vanished; another time, before a bull run, I listened to a “friend’s tip” and sold BTC to buy a shitcoin, losing 70%. So now, my approach is simple: just hold. Don’t try to trade short-term swings—you’ll eventually swing yourself out of your coins. Knowing your own limitations is crucial.

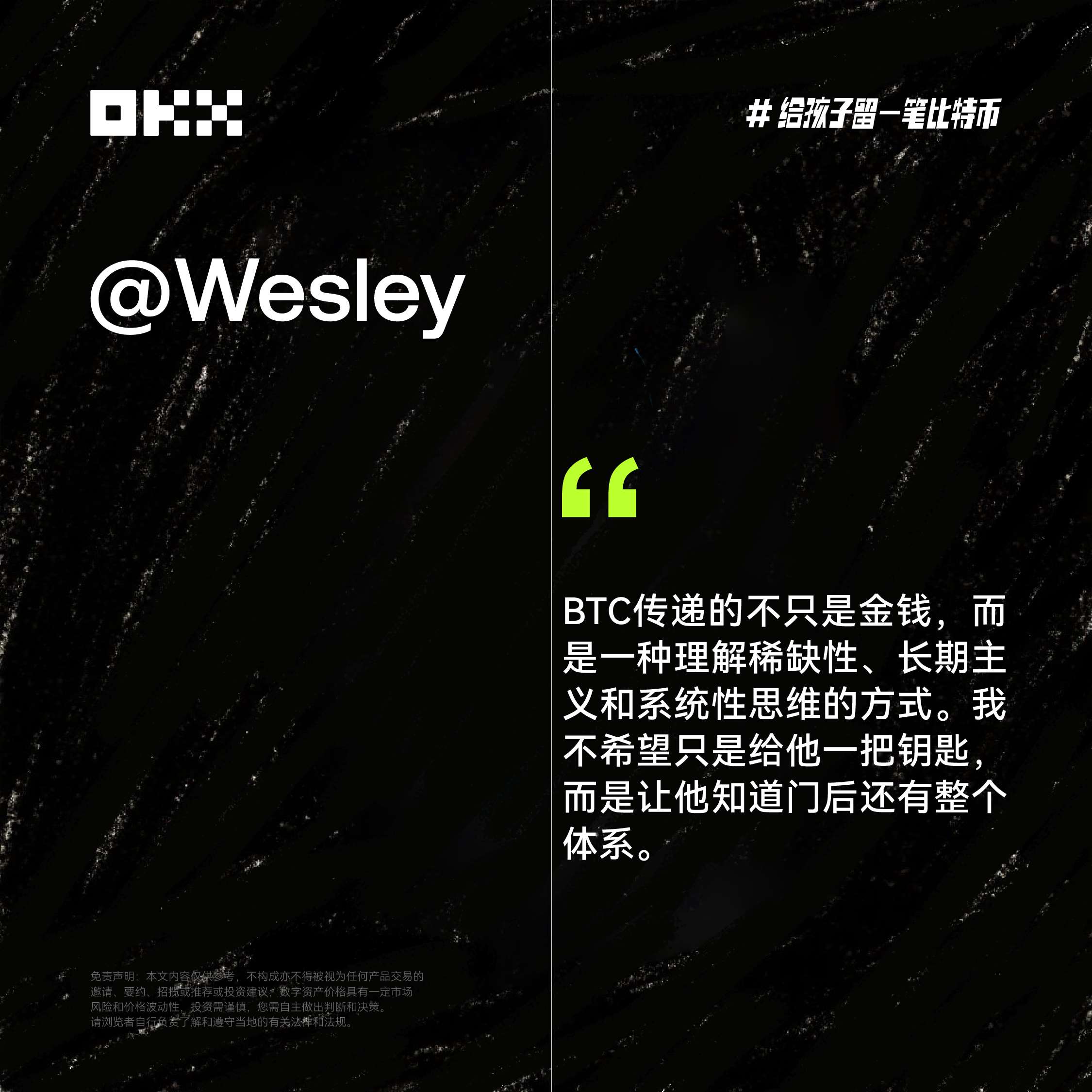

6. @Wesley (Serial Web3 Entrepreneur in Silicon Valley)

Q: What do you think is the biggest misconception people have about Bitcoin? From an asset allocation perspective, is adding Bitcoin to a child’s “starting line” bold or reasonable? If you were to leave Bitcoin for your child, when would you tell them? What message would you want this asset to convey?

A: From an asset allocation standpoint, I don’t see this as “bold”—it’s “forward-looking.” Leaving Bitcoin isn’t just giving money; it’s providing a key to participate in the future reconstruction of global value. If I really decided to leave Bitcoin for my child, I probably wouldn’t tell them too early—I’d wait until they’re 18, when they’ve developed their own understanding of “value,” then open this “time capsule.” Let Bitcoin grow with them. This asset conveys not just money, but a mindset rooted in scarcity, long-term thinking, and systemic reasoning. I don’t want to just hand them a key—I want them to understand there’s an entire system behind the door.

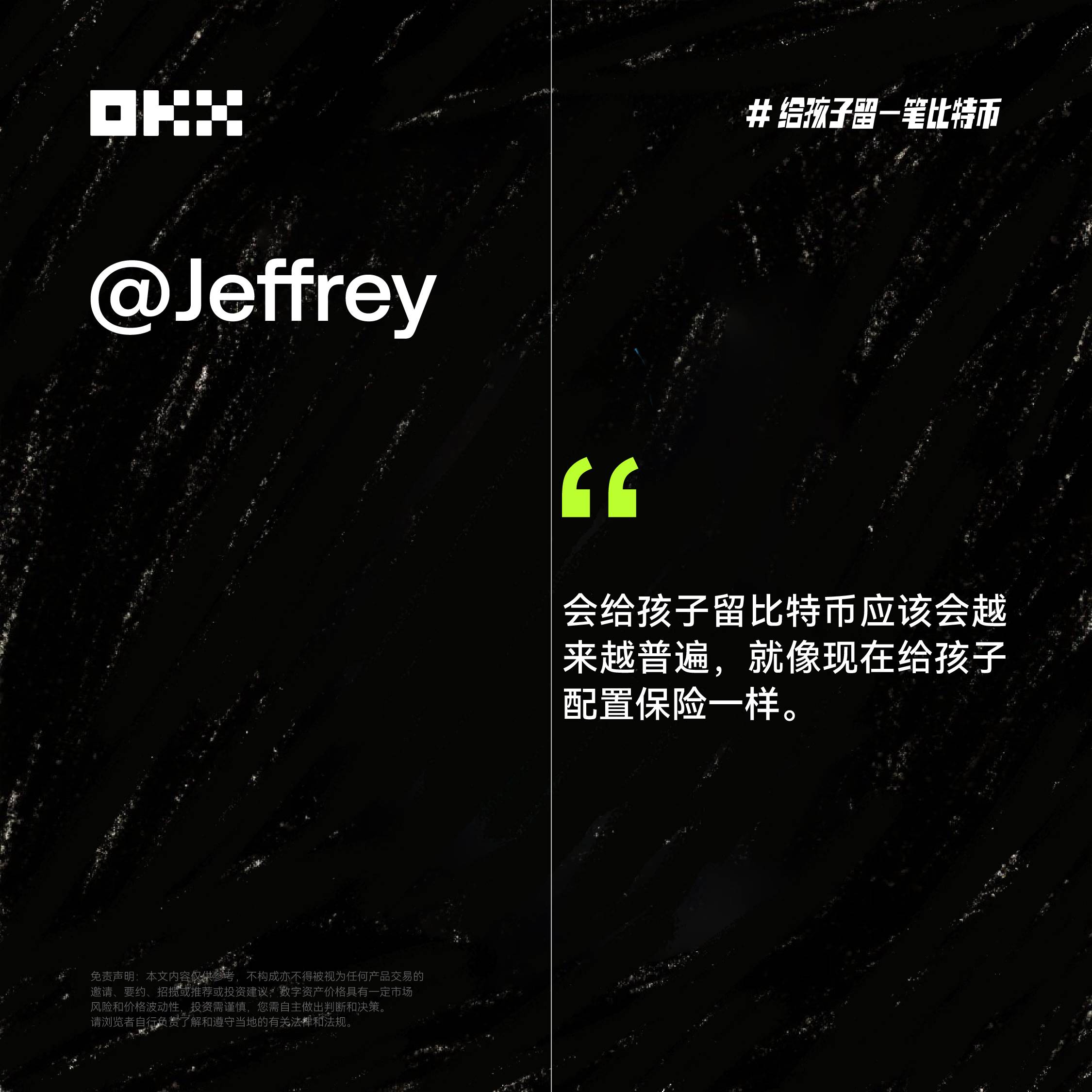

7. @Jeffrey (Operations Director at PANews)

Q: Would you personally leave Bitcoin for your child? Is this driven by emotion or informed judgment? As a parent, what do you think of the idea of “leaving Bitcoin for your child”? And how would you explain the meaning of Bitcoin to them?

A: Absolutely yes—and I’m already doing it. I believe many crypto parents feel the same. It’s a mix of cognition and emotion. Cognition determines *how* I do it; emotion decides *how much*. Each generation has its own form of gold—just as older generations bought gold for heirs, I buy Bitcoin on key occasions like my child’s birth, Chinese New Year, or during market dips, transferring it to a wallet set aside for him. By the way, I’ve also saved a bit of Ethereum for my kid.

I think this idea will become increasingly common, just like setting up insurance for children today. Right now, I won’t explain Bitcoin’s meaning to him. This generation was born or raised in an era of information explosion and the dawn of mass crypto adoption—they’ll naturally accumulate understanding of crypto assets through learning, socializing, and daily usage. Of course, during their development, we need to help them build proper values and worldview. Once they develop a basic grasp of money and consumption, I’ll allow them to manage part of their Bitcoin.

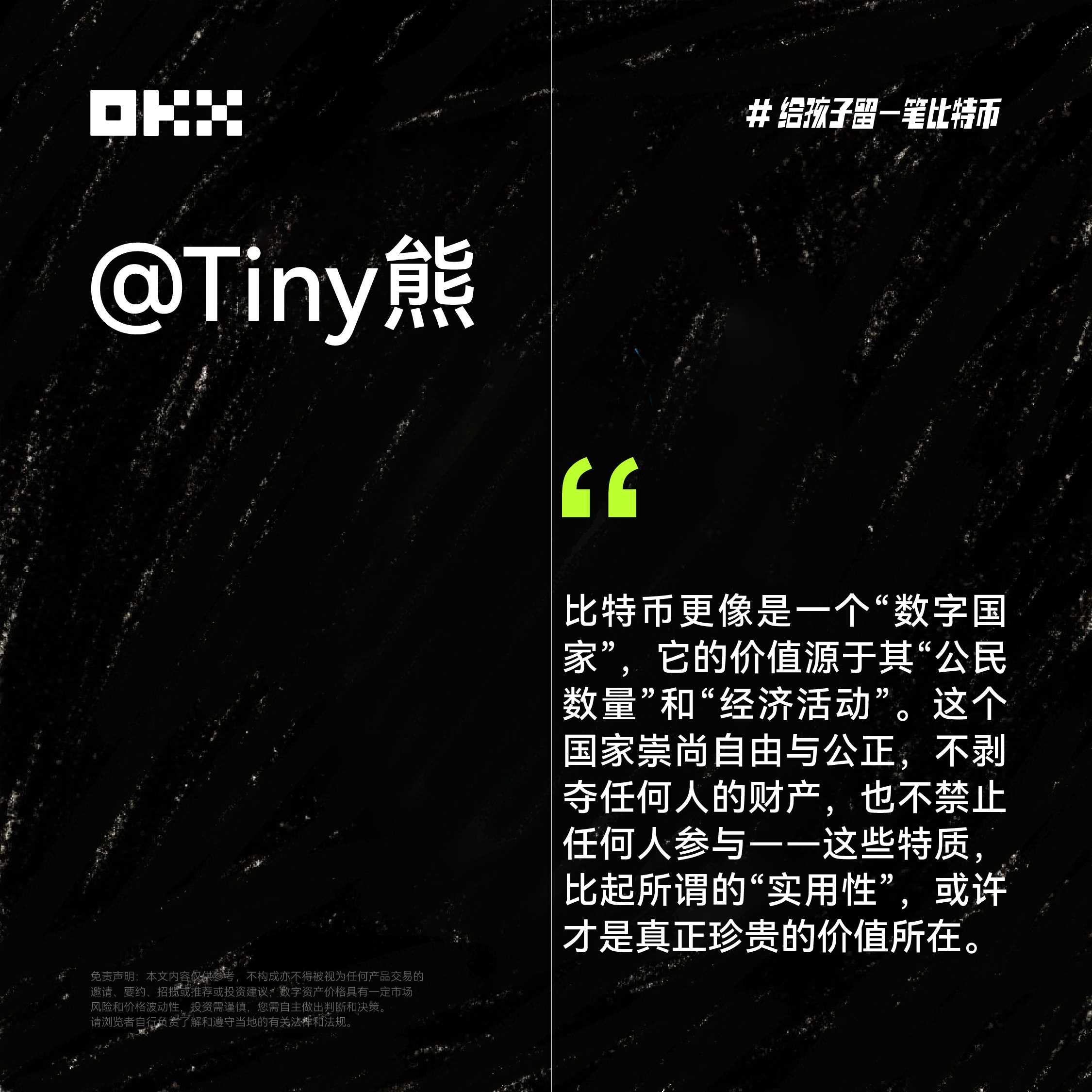

8. @Tiny Bear (Founder of DenChain Community)

Q: How do you view Bitcoin? From a parent’s perspective, what’s the value of letting children own Bitcoin?

A: Many people tend to evaluate Bitcoin using company valuation logic, arguing that since Bitcoin lacks tangible “products” from a “practicality” standpoint, it shouldn’t be valuable. But to me, Bitcoin is more like a “digital nation,” whose value stems from its “citizen count” and “economic activity.” This nation champions freedom and fairness—never seizing anyone’s property or barring participation. These traits may be far more precious than mere “utility.”

Letting children own Bitcoin helps them understand “long-termism.” Life is similar: in the short term, we may hit lows or brief highs. But we want our children to focus less on immediate wins or losses and learn to stay focused and resilient. Like Bitcoin, life’s greatest returns come from the compounding power of time.

9. @Tony Li (Portfolio Growth Lead at Dragonfly)

Q: Compared to traditional assets like real estate and gold, what does Bitcoin represent? Has Bitcoin become part of your household asset allocation? Why?

A: After nearly a decade in the industry, Bitcoin is a deep faith for me. It represents a new paradigm of assets—more efficient, freer, and more resilient. Compared to traditional assets like property and gold, Bitcoin’s core advantages lie in three areas: superior efficiency and liquidity, greater long-term value storage potential, and stronger resilience against global uncertainties.

Yes, Bitcoin is now a significant part of my household portfolio. I believe it’s the asset that will benefit our next generation the most. If I had to choose one asset to leave my child, it would undoubtedly be Bitcoin—and the belief in Bitcoin.

10. @Onchain Expert (Top-tier KOL)

Q: More and more parents are seriously considering allocating Bitcoin for their children—what does this indicate? How has your view on Bitcoin evolved? What caused this change?

A: Bitcoin has become a mainstream asset, standing equal to traditional financial instruments. Its consensus continues to expand, and many parents now see Bitcoin as a long-term investment tool—akin to setting up education funds. Traditional finance has many instability issues, which Bitcoin effectively addresses. Allocating Bitcoin for children is now the most advanced form of wealth inheritance.

The biggest shift is in my understanding of return potential. I used to think Bitcoin was too large to grow fast, believing smaller altcoins or meme coins offered better chances for life-changing gains. So I accumulated many altcoins, memes, and NFTs—only to find most failed to outperform Bitcoin, crashing harder instead. The reason? As more institutions and outsiders enter, Bitcoin becomes the default choice. Retail investors can still chase small opportunities via airdrops or speculative plays, but the smartest move after earning gains is to convert them into Bitcoin.

Disclaimer:

This article is for informational purposes only. The views expressed are those of the author and do not necessarily reflect the positions of OKX. This article does not constitute (i) investment advice or recommendations; (ii) an offer or solicitation to buy, sell, or hold digital assets; or (iii) financial, accounting, legal, or tax advice. We make no guarantees regarding the accuracy, completeness, or usefulness of the information provided. Holding digital assets (including stablecoins and NFTs) involves high risk and may result in significant volatility. You should carefully consider whether trading or holding digital assets is suitable for you based on your financial situation. For specific advice, please consult your legal/tax/investment professionals. You are solely responsible for understanding and complying with applicable local laws and regulations.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News