Will application-specific chains rise, making L1s a commodity?

TechFlow Selected TechFlow Selected

Will application-specific chains rise, making L1s a commodity?

Block space prices will trend toward zero, and the future winners will be those applications that best align with demand.

Author: Arcana, Crypto Research Institute

Translation: deep from TechFlow

Editor's note: The "fat app thesis" argues that as block space costs approach zero, L1 blockchains shift from monopolies to commoditized utilities, and value migrates from base protocol layers (such as Ethereum, Solana) to the application layer. Successful applications vertically integrate, control order flow, and capture MEV to become sovereign app chains. Markets are repricing L1s/L2s—future winners will be apps close to demand and focused on utility, not chains chasing high TPS.

The following is the original content (slightly edited for readability):

The crypto infrastructure era is entering a post-marginal-cost world. Just like bandwidth and computing power, the price of block space will rapidly trend toward zero. The only chains that will survive are those that can:

-

Achieve growth today through subsidies

-

Capture non-inflationary revenue tomorrow

-

Provide infrastructure that apps cannot easily replicate or outsource

But in this new environment, L1s are no longer monopolists defined by early advantages or native ecosystems. Instead, they have become commodities—interchangeable tools competing economically based on performance, interoperability, and cost efficiency.

Their value now depends on how well they integrate into application workflows and deliver indispensable or non-outsourcable services. The “protocol premium” that once drove high valuations is fading, replaced by demand for real utility and performance. The ongoing market repricing of many L1s/L2s reflects this shift.

Chart includes: BERA, MOVE, SCR, STRK

Was the Fat Protocol Thesis Wrong?

In 2016, Joel Monegro introduced the fat protocol thesis, arguing that in crypto networks, most value concentrates at the base protocol layer (Ethereum, Solana, etc.), rather than the application layer. This contrasts sharply with Web2, where applications like Facebook, Google, and Amazon capture most of the value, while protocols like HTTP and TCP/IP become commoditized.

The fat protocol thesis was indeed correct over the past eight years. This is evident in the stark differences in valuation and revenue multiples between infrastructure and applications. On average, applications trade at significantly lower revenue multiples compared to infrastructure.

Under this model, crypto infrastructure attracted massive funding and venture capital. So much so that founders and developers were almost incentivized to launch yet another alternative L1 or general-purpose rollup, knowing venture capital would readily support them.

In a recent report, I noted that data availability (DA) is becoming commoditized and inevitably trending toward zero. By the same logic, we can assume all parts of the infrastructure stack will eventually be commoditized and stripped of value. Why?

1. The fat app thesis: Applications realize they can capture more value by becoming sovereign “app chains” and vertically integrating the entire stack.

2. Application-specific sequencing: Apps can control their own transaction ordering and inclusion process. This serves as an alternative path for apps unwilling to build an app chain from scratch.

The Fat App Thesis

The fat app thesis holds that successful crypto applications will capture more value than the underlying blockchain protocols. The simple reason: applications are business entities, and business entities prioritize maximizing revenue.

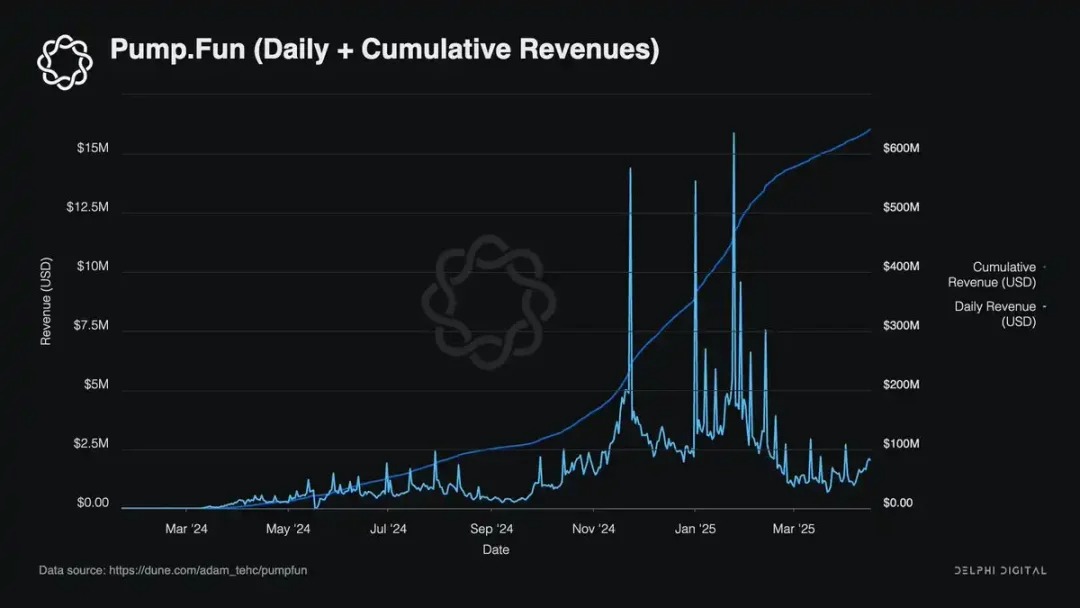

The most successful players in the space are those consistently generating revenue—examples include pumpfun, Hyperliquid, Jupiter, and Uniswap. What do they have in common? Fee income. These business entities have strong incentives to control their own order flow and MEV capture—or in many cases, become sovereign app chains—which is entirely rational.

Vertical integration appears to be the most economically efficient direction for apps to plug value leaks. As apps scale, the opportunity cost of not doing so only increases. This is good for apps but less so for underlying infrastructure like Ethereum. We’re already seeing clear signs of this trend in Unichain and JupNet.

What’s Left for the Protocol Layer?

There are two prevailing views on how value might accumulate at the base protocol layer in the future:

1. Base and transaction fees will trend toward zero over time. With MEV as the last remaining revenue source, it will be abstracted away by applications seeking to internalize all value. Protocol layers (e.g., Ethereum, Solana) will provide value as settlement layers but won’t capture any value themselves—similar to HTTP and TCP/IP.

2. Cheap block space will drive increased demand and a surge in applications. Transaction volume will rise enough to offset low base fees, funneling value back to the protocol layer.

Let’s unpack the first scenario:

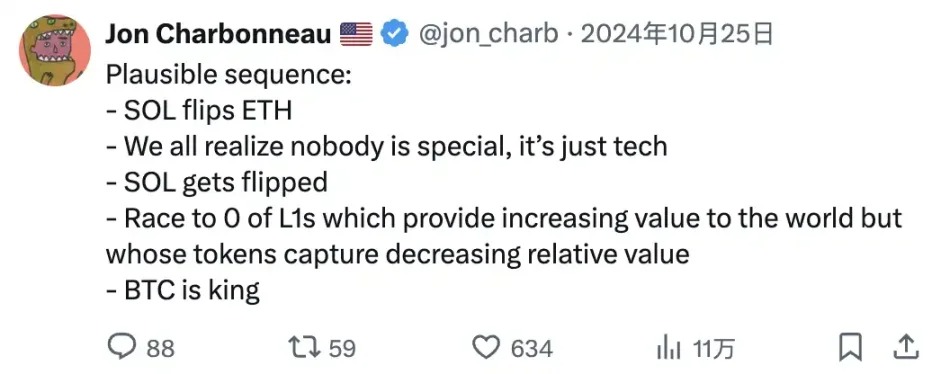

Possible sequence of events: · SOL surpasses ETH · We all realize no one is special—it’s just tech · SOL gets surpassed · L1s deliver more and more to the world, yet their tokens capture relatively less value · BTC reigns supreme

This view assumes full commoditization of infrastructure. Regardless of data availability, fees, or compute costs, all parts of the stack will trend toward zero over time. Cheap and abundant block space from rollups and DA layers is eroding Ethereum’s transaction monopoly.

Data blob inclusion (EIP-4844) decouples execution from settlement. L2s adopting alternative DA solutions further reduce the residual value of sequencing and data storage, a trend accelerating over the past year.

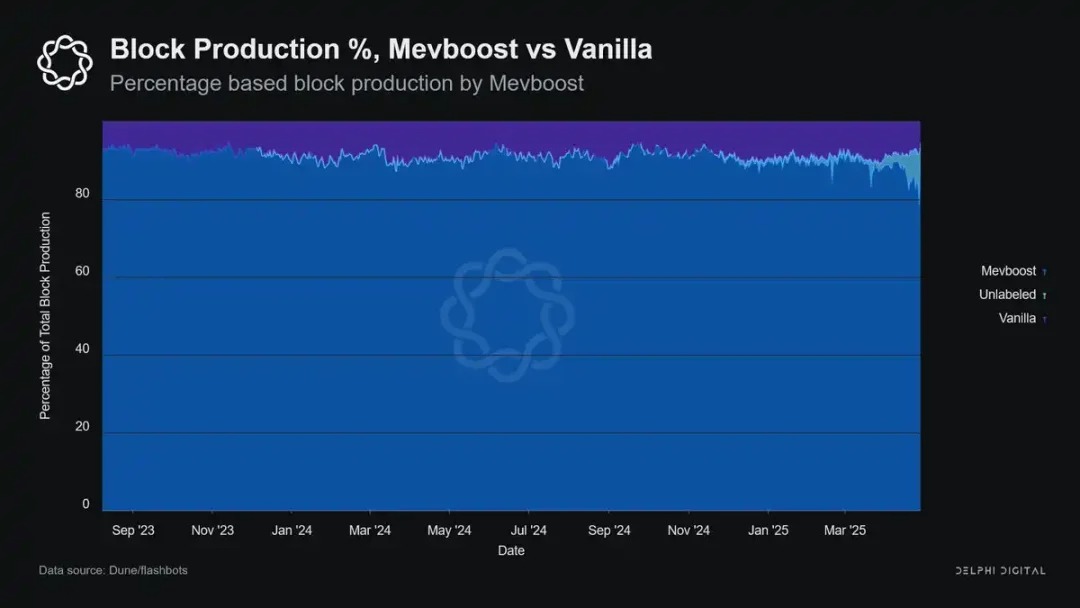

But the strongest evidence lies in the declining share of MEV captured by L1 block proposers. In 2024, most MEV is captured by searchers and relays via systems like Flashbots—not by Ethereum validators. Currently, 90% of Ethereum blocks are proposed via MEV-Boost, with a significant portion routed through Flashbots-affiliated relays.

This doesn’t even account for apps like CoW Swap, which use solver networks to handle matching and execution off-chain, completely bypassing the public mempool and its associated MEV.

The second scenario heavily relies on surging demand and transaction volume driven by near-zero fees. It assumes abundant cheap block space leads to increased consumption, not deflationary effects.

Just as falling computing costs fueled the internet boom, lower transaction fees will unlock new application categories and use cases. The key analogy here is that general computation and coordination layers resemble AWS or Linux, not HTTP. Ethereum and Solana aren’t merely “settling” transactions—they enable large-scale, trustless state coordination.

As usage grows and cost barriers fall, this trustless computational capacity becomes more valuable, not less. Low fees don’t push value to zero—they expand the addressable market for block space.

-

Low fees > Increased network demand

-

Increased network demand > Higher total fee revenue

Token Valuation—What Does This Mean for My Investments?

If there’s one takeaway, it’s this: capital allocation is shifting in ways unfamiliar to many since 2016/17.

The fat protocol thesis unfortunately created an illusion of L1 premium, subsidized by hundreds of millions in venture capital. Yet we are now at an inflection point in the value distribution curve, where application revenue growth relative to the protocol layer is clearly visible.

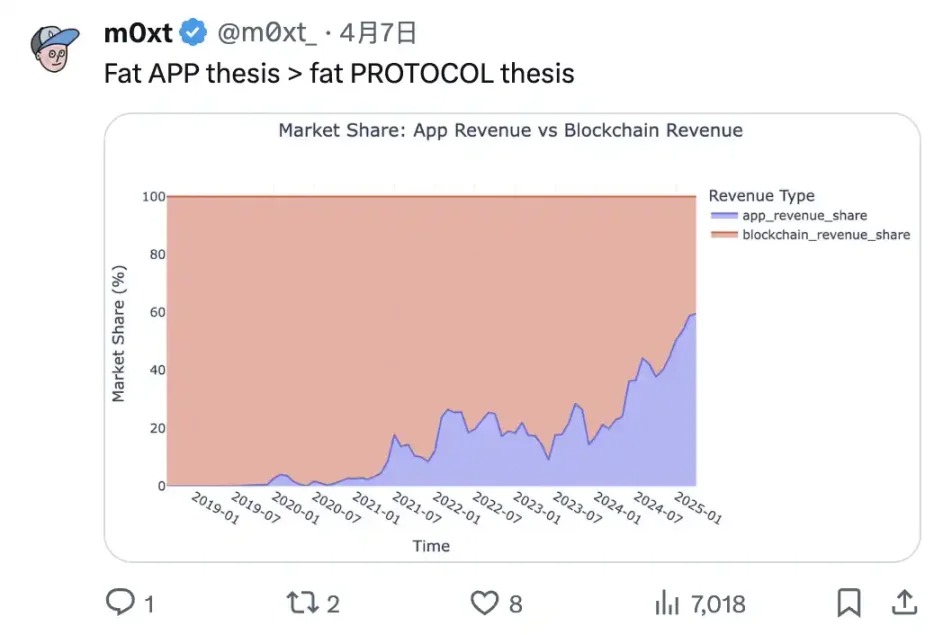

Fat App Thesis > Fat Protocol Thesis

Regarding L1 valuations, we’ve overused narratives to such an extent that these tokens can no longer sustain prices after TGE. Fundraises of hundreds of millions and pre-mainnet billion-dollar valuations have become standard for L1s/L2s. A common pattern among most new protocols is: prices only go down, never up.

This isn’t to say infrastructure will become irrelevant—the signs of market maturation are obvious. However, trading in L1s/L2s has saturated. Low liquidity and high FDV sentiment reflect this. Newly launched L1s now have FDVs orders of magnitude higher than in previous cycles. Monad, Bera, and Story Protocol each raised nine-figure sums before launch, while Solana raised only $45 million (including public token sales).

The next cycle won’t be led by chains racing to reach 100k TPS. It will be driven by focused, composable applications that prioritize usage over architecture, sustainability over speculation. Winners will be the apps closest to the source of demand.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News