Mantra Co-Founder Reveals: Did the 5 Billion Dollar OM Token Collapse Truly Become "Luna 2.0"?

TechFlow Selected TechFlow Selected

Mantra Co-Founder Reveals: Did the 5 Billion Dollar OM Token Collapse Truly Become "Luna 2.0"?

JP has committed to providing full transparency and launched a buyback and burn program to support investors.

Guest: JP Mullin, Co-founder of Mantra

Translation: zhouzhou, BlockBeats

Editor's Note: The podcast discusses JP Mullin, co-founder of Mantra, explaining the OM token crash. He expressed a sense of responsibility for losses suffered by investors and the community, despite no malicious conduct. JP committed to full transparency and announced a buyback and burn program to support investors. He emphasized the importance of transparency and ongoing communication, stating his determination to repair the current situation and restore the project’s health. He thanked supporters and pledged to strengthen engagement with the community going forward, ensuring better development and responsiveness to investor needs.

Below is the original content (slightly edited for clarity):

JP Mullin: Setting aside market cap, I’m not happy about this at all. This is an unprecedented event—many people have lost money and been hurt. I’m personally hurt too. I feel our community has been hurt, holders have been hurt, and investors have been hurt. Even if I didn’t do anything wrong or act negligently or maliciously, I still feel responsible.

Host: I'm curious—you said investors were hurt, but if the current trading price is 70 cents, are they really in loss?

JP Mullin: I don't think they've actually lost yet. And precisely because of that, investors holding liquid tokens haven't sold any so far.

Host: I'm Akuzhman. A lot has happened in crypto recently, and this past weekend, the entire space was focused on the sharp drop in a real-world asset (RWA) blockchain project’s token.

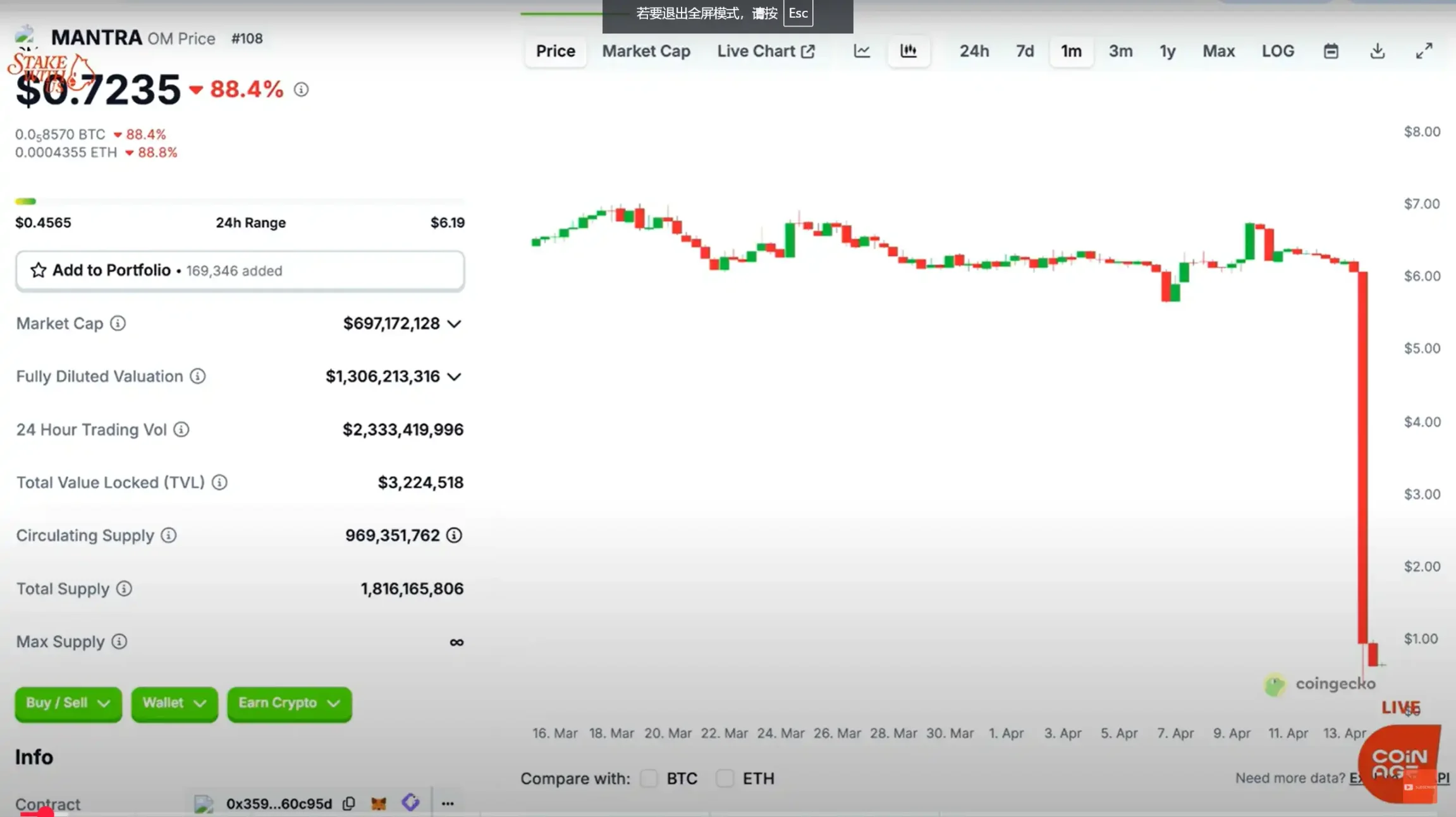

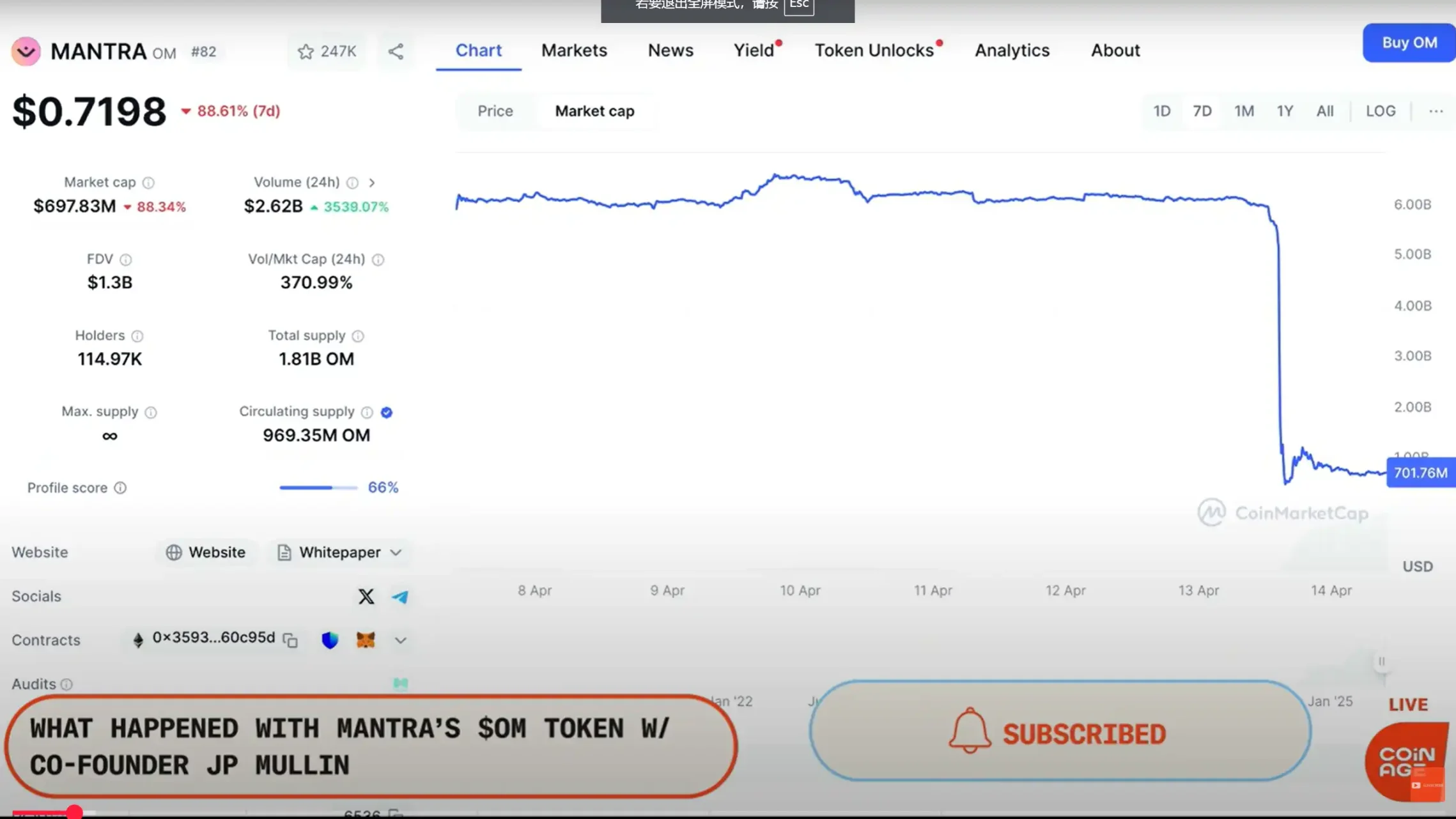

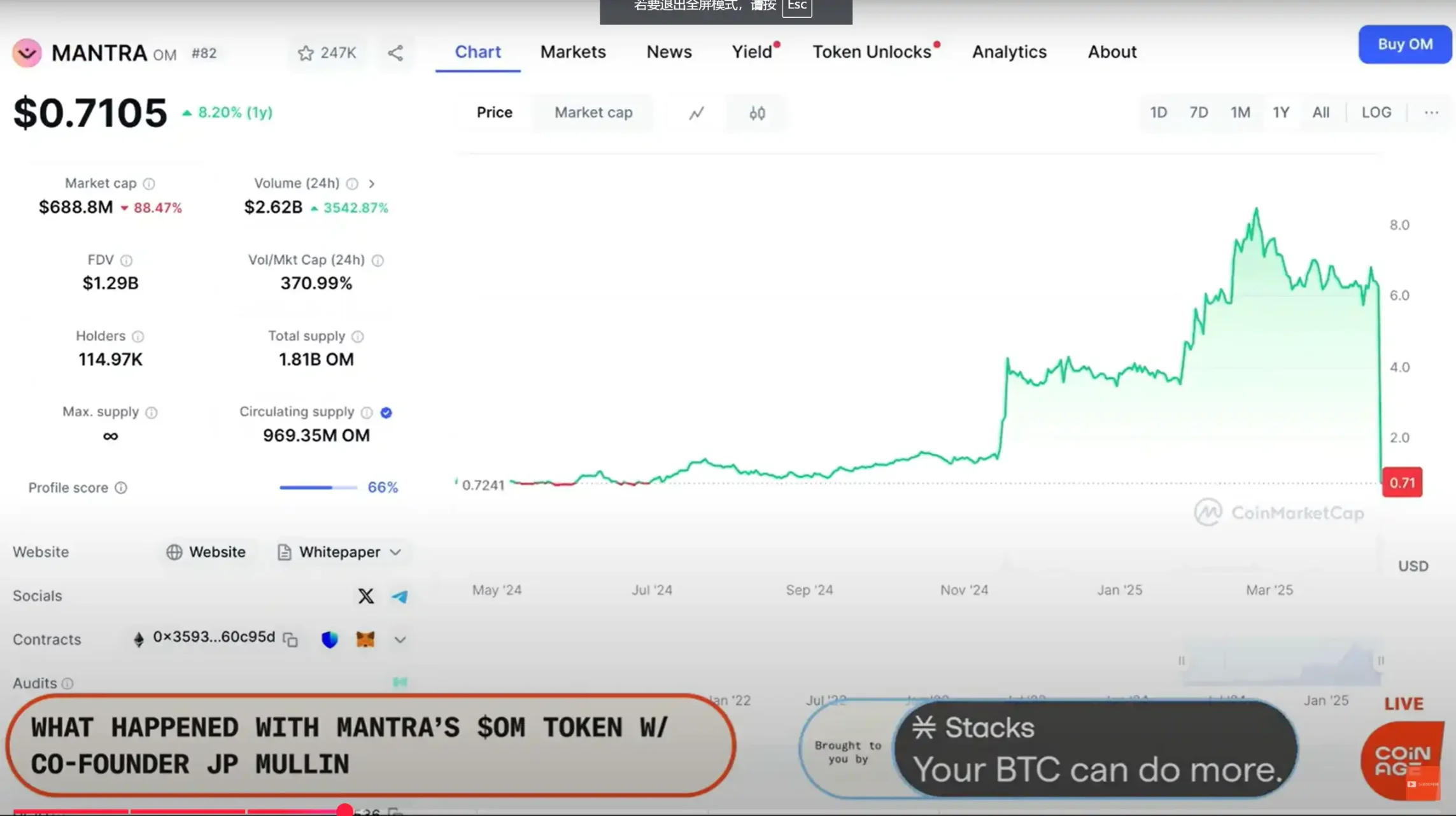

The chart we're looking at now shows the OM token plunging over 80% in a single day, wiping out around $5 billion in market value—at least on paper.

Many are asking what exactly happened, and hopefully today we can find some answers. We also want to thank Mantra’s co-founder for joining us to address these questions—welcome John Patrick Mullin, aka JP.

JP Mullin: Thank you for giving me the opportunity to talk about this incident and how we plan to respond moving forward.

Host: What’s happened in the last 24 hours since you became aware of this? How has this time been for you?

JP Mullin Responds to the OM Crash

JP Mullin: This past day has been extremely difficult—for me, for the team, and especially for the community. Let me walk through how this unfolded, break it down step by step, and explain where we stand now.

Last week I attended Paris Blockchain Week. On Saturday local time, I boarded a flight from Paris to Seoul, South Korea. Right now, I’m staying at a hotel here in Seoul. We hosted an artist-focused summit today, which I attended—I’ll tell you more about that later. I went to sleep around midnight local time. I posted a tweet saying I was on the plane without Wi-Fi, so people assumed I was mid-flight.

But in reality, I had just fallen asleep—it was late at night. Then around 5 a.m., I was woken up by a call from the hotel front desk. The team couldn’t reach me directly, so they called the hotel. As soon as I woke up, I was bombarded with messages—token crashing, something’s wrong, etc. We immediately started checking whether there was a chain exploit, stolen tokens, or anything similar.

Was a Mass Liquidation Behind the Token Crash?

After communicating with key partners, investors, and exchanges, we quickly identified the issue: large-scale liquidations on centralized exchanges. Someone had used OM tokens as collateral for leveraged positions, along with significant long positions in OM itself. These positions were forcibly liquidated within a short period, coinciding with Sunday night in Asia—a time of very low liquidity.

I was asleep during all this, and the rapid cascade of liquidations triggered a price collapse, which in turn triggered even more liquidations and sell-offs, resulting in this massive downturn.

That’s how I woke up—to this chaos. We immediately issued a statement saying we were investigating and committed to communication and transparency. We’ve reached out to all investors, partners, exchanges, and community members to clearly explain what happened, what actions we’re taking, and answer any questions, as the situation is indeed complex.

Host: For context—we didn’t talk much before this show, just basic coordination. So like everyone else, I’m learning about this in real time.

But I’m a bit surprised—you and your project Mantra have existed for quite some time. Maybe we should start before the crash? Because many may not know what you're doing. You're building a Layer 1 protocol tied to real-world assets, headquartered in Dubai—the place you spend most of your time, in the UAE.

Your core mission is tokenizing real-world assets. But even before launching your mainnet last year, the OM token had already existed for years as an ERC-20 token on Ethereum, right? Could we go back to the beginning and trace how the project evolved? I see your token circulates across multiple chains. I’m also curious—who was selling on that exchange you mentioned earlier? If it wasn’t your investors, and you didn’t dump tokens, who caused this sell-off? Do you have further insights?

Mantra’s Founding, Token Design, and Bridging

JP Mullin: Let me start from the founding of Mantra, so you can better understand the relationship between the two tokens: the early ERC-20 version and the later mainnet token.

Mantra was founded in early 2020 during the pandemic. We launched the OM ERC-20 version on August 18, 2020—so the project has been around nearly five years. In March 2021, we listed on Bybit. We began as a DeFi protocol and built some early products. We caught the first wave of DeFi Summer and initially saw strong growth, but then declined along with the broader market.

By 2023, our situation was tough—our token dropped as low as $0.017 in October 2023. From late 2023 into early 2024, I began meeting with key partners including Shorooq, a UAE-based fund, and Laser Digital, the crypto arm of Nomura Securities. They helped bring institutional capital and advanced our vision of a “regulated DeFi protocol.”

We were also working with VARA, Dubai’s regulator, on licensing. Earlier this year, we secured the world’s first official license for a DeFi protocol. Our new Layer 1 chain is designed specifically for real-world asset tokenization, with built-in compliance frameworks, permission layers, identity systems, and more.

Around that time (late 2023 to early 2024), we started thinking about integrating our token model. Initially, we planned to run two separate token systems: the Ethereum-based Mantra ERC token and the AUM token on our upcoming Omega chain.

But we put it to a community vote, and the community wanted us to focus resources on one token instead of two. So we merged the paths based on that result, shifting focus to building an institutional-grade RWA business in the UAE.

In the past month alone, we’ve announced major partnerships, such as with Mag and Damac Group in real estate. We officially received our VARA compliance license and launched our own chain at the end of last year.

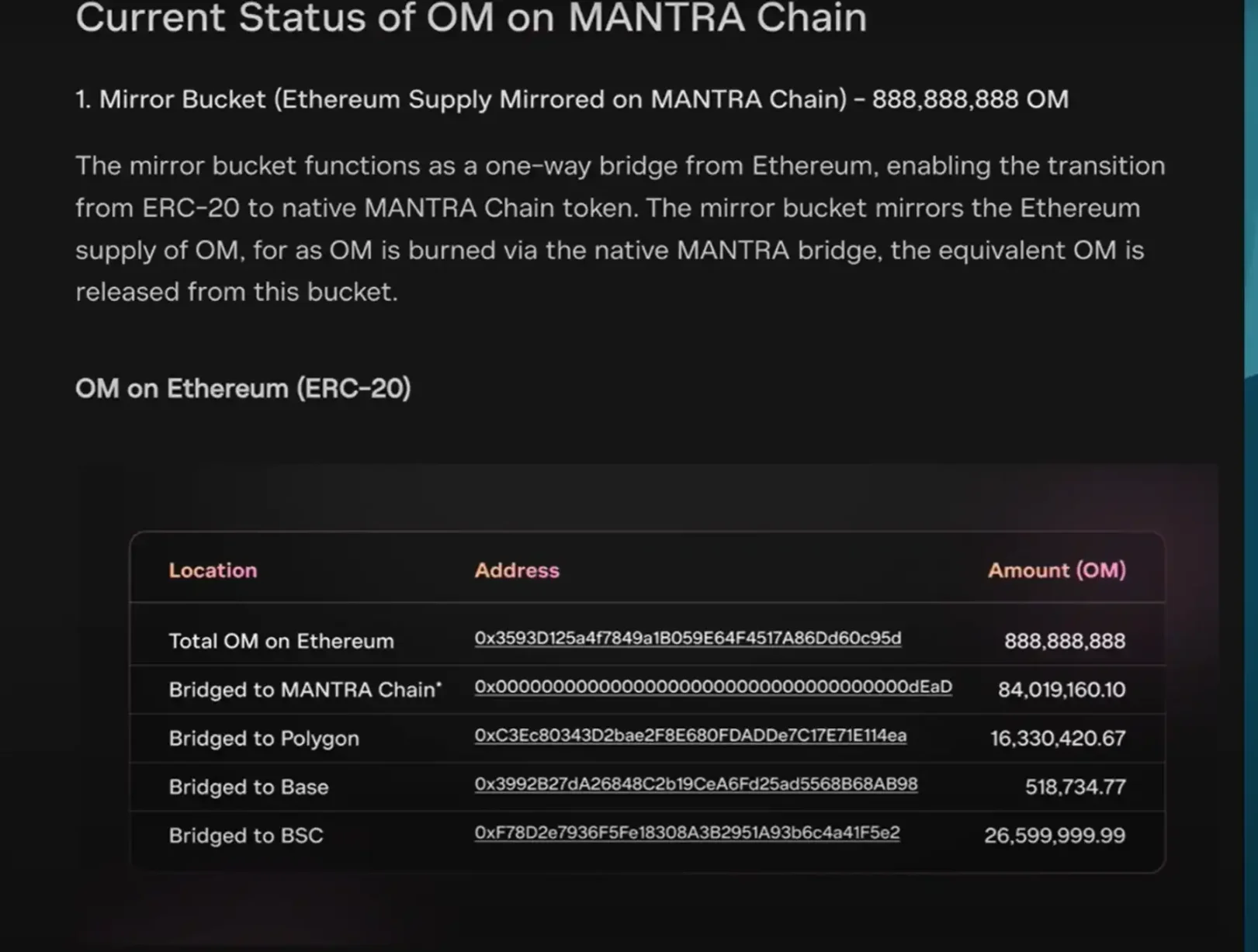

With the mainnet launch came the cross-chain bridge process. At launch, about 95–96% of the ERC tokens were already circulating; now it’s around 98%. The ERC token has a hard cap of 8 million, all verifiable on Etherscan—wallet addresses, distribution—all clear, with many in exchange wallets and tagged wallets.

Most of the mainnet tokens remain locked and are held in custody by third-party institutions like Anchorage, under strict vesting schedules.

Last week we released a transparency report addressing concerns about token details. We’ll continue sharing more granular wallet and distribution data going forward.

The ERC token has also been bridged to multiple chains—Polygon (via Polygon POS Bridge), Binance Smart Chain (BSC version of OM), and even Base.

But all of these remain within the original 8 million ERC supply—no new issuance—just bridged to other chains for circulation.

Host: This part is interesting—you “mirrored” old-chain tokens onto the new chain. So if someone wants to move their old tokens to the new chain, they must first burn the old ones and receive new ones, correct?

This kind of decision is crucial for established projects evolving over time. Now that we understand Mantra’s background and how its tokens are spread across chains,

let’s return to the core of this incident. Yesterday you mentioned someone may have opened a large leveraged position using OM on an exchange, which later got liquidated. That led to a flood of tokens hitting the market, causing the crash.

So I have a few questions: First, do you know who did this? Second, which exchange was involved? Third, did you receive any warning before the liquidation?

JP Mullin: We’ve actually been in regular contact with several exchanges for months—not just in the past 24 hours—asking things like: “When did these tokens list?” “Do you know who owns these wallets?” “Are these team wallets? Market maker wallets?”

For this incident, we’d already been discussing such issues with exchanges for months. We monitor which tokens flow into exchanges and whether they arrive as collateral. But these incoming tokens came from clean wallets—meaning wallets transferred from other exchanges, with no prior activity and no links to wallets we recognize.

I personally tag every wallet I know on Etherscan so I can track them. But the wallets involved here were all clean, untagged, and entirely new—no direct link to the team or known entities.

We do know certain exchanges played a role, but I can’t name them publicly right now. We’re currently evaluating potential legal options with institutional investors and partners to protect our community and investors, as we believe they’ve been harmed and treated unfairly.

Clearly, this was a large forced liquidation during a low-liquidity window—Sunday night. We haven’t contacted the liquidated investors yet, but we maintain communication with institutional partners like Cheroke and Laser.

Host: To clarify, both Cheroke and Laser have publicly stated they weren’t behind this sell-off. You mentioned this occurred during low liquidity, a typical “off-peak” weekend period—exactly when projects usually rely on market makers to stabilize prices. Can you disclose who your market makers are? And how did they respond during the event? After all, this is precisely when market makers should step in.

JP Mullin: We do have multiple market makers, and they’re also our investors. We work with major trading firms who are both investors and OM holders, and some have loan agreements with us.

But frankly, I don’t believe their positions were large enough to counteract this extreme scenario. Based on what we know, the forced sell-off volume could have reached hundreds of millions of dollars—we don’t have exact figures yet, and that’s part of our ongoing investigation. We’ll disclose more as we learn.

Host: You mentioned a position size around $100 million—is that the ballpark?

JP Mullin: Yes, we believe it was in that range—an extremely large position. OM is a multi-billion dollar market cap token, with many long-term, large holders using their tokens as collateral or for leverage.

And it happened incredibly fast—I fell asleep around midnight, woke up at 5 a.m., and it had already been unfolding for one or two hours. We were completely unaware and reacted passively.

That’s why we emphasize this was an unprecedented, sudden, and rapid event. We’re still gathering details and will share as transparently as possible.

Host: I agree this is highly unusual, especially happening during a weekend low-liquidity window. The price chart makes it clear. I’m curious—now the community is discussing on-chain transparency. People are asking: if it wasn’t your core investors, then who could build a $100M+ position? Such massive liquidations likely involve off-chain operations beyond pure on-chain visibility.

As a founder, I know these decisions are complex—you need to get listed on centralized exchanges, work with market makers, and worry about them turning against you.

So let’s rewind to 2024: what decisions did you make during the project rollout? Were there OTC agreements? What did those structures look like? How did we get to this point? We all know many tokens were already circulating before the official launch—did that plant the seeds for today’s crisis?

What Was the Situation Before Official Launch?

JP Mullin: We conducted two rounds of mainnet token fundraising, detailed in our previously mentioned transparency report. These tokens remain custodied on Anchorage and are locked.

The first round started in October last year, with a 12-month lock plus 24-month vesting. The second round’s unlock is approaching, with a 12-month lock.

Besides that, some investors acquired the ERC version via OTC deals—long-term backers like Shorooq and Laser. Their wallet addresses are public and verifiable. They’ve never sold a single token. Those tokens have an 18-month vesting schedule and are still gradually releasing.

Our first funding round closed around February or March last year—those tokens have been circulating for a long time. Yet on-chain data confirms no sell-offs. We have a group of deeply aligned, long-term investors, and I’m truly grateful they’ve stood by us. We’ll continue supporting them.

So we fully reject accusations that anyone secretly dumped tokens.

Host: Let’s clarify what we mean by “accusations.” I haven’t seen anyone openly blaming you, and as a journalist, I must be precise.

I don’t believe every crypto incident is a “rug pull”—even Terra’s collapse wasn’t, in my view. Often, problems arise without malicious intent. We’re not talking about meme coins here.

We’re discussing your team building a real-world asset Layer 1 blockchain, collaborating with major institutions—like your integrations in Dubai.

So it’s worth asking: where do you think things went wrong? If you’re serious about building a real, useful project, what missteps occurred? Your tone suggests you suspect a particular exchange.

Also numerically speaking, a $100M position equals roughly a full day’s trading volume on many days. Such a liquidation is extremely violent.

Where Exactly Did Things Go Wrong?

JP Mullin: I’m not implying it was a single individual. Honestly, we believe it was a coordinated group action. We do believe the core incident occurred on one specific exchange, but we’re cooperating with all exchanges to investigate and gather as much information as possible.

This was truly unprecedented and deeply painful for our community. We’ll do everything we can to resolve it. I’ve participated in numerous AMAs and Spaces lately to show we’re not shirking responsibility.

We’re five years into this project, and we’ll keep going—not just five more years, possibly much longer.

Preview of Buyback and Burn Plan

Next, we need to rebuild confidence among our community and holders. We’re actively considering launching a buyback program. We’re also evaluating whether to burn portions of future token supplies. If we combine both measures, we aim to announce a concrete plan soon.

Beyond the buyback, we’ll provide as much detailed, transparent on-chain data as possible—facts and evidence proving our claims, allowing the community to verify for themselves that we’re handling this responsibly.

Host: A practical question: post-event, the number of token holders has actually increased—many bought after the drop. Now you’re planning a buyback, so people naturally wonder: how much capital do you have for this? Can you share your current financial status?

JP Mullin: Let me emphasize: our operations are fully healthy, we have ample funds, and the business is solvent. Beyond existing investors, many new ones have proactively offered support—providing capital, joining buybacks, engaging in long-term OTC trades.

We’re actively assessing these options and will roll out a comprehensive solution soon. Business will continue as usual, and we’ll keep updating everyone. Financially, we’re in good shape—we’ll keep moving forward.

Transparency, Investors, and Market Makers

Host: You mentioned “long-term OTC trades”—that’s worth highlighting. OTC is common but often lacks transparency.

You noted Laser Digital and Shroooq’s tokens are locked and they’ve confirmed no sales. But OTC involves private sales of tokens, possibly below market rate. If those tokens later enter the market, it might appear as if the team is dumping.

So, how extensive have your OTC transactions been to date? How large were they?

JP Mullin: We’ve done OTC deals with institutional investors, high-net-worth individuals, and family offices. But all come with long-term locks—none have unlocked yet.

These agreements include restrictions like bans on secondary market resale or transfer. We work hard to ensure investors align with us—no hedging, no short-term plays—but rather long-term bullish holders. We don’t want unnecessary selling pressure in spot or perpetual markets.

We also care deeply about secondary market health, so we manage all such transactions through official channels. We work with brokers who inform us when institutions want to buy or sell, and we coordinate to ensure these trades happen under our awareness and supervision, maintaining market stability.

Host: I understand you have control mechanisms, but circling back: this situation has already escalated. I’ve seen your token allocation table—the early ERC-20 tokens are substantial and can be mapped to mainnet. In that case, isn’t it still hard to control circulating supply? No wonder someone could build a seemingly valuable but illiquid position on-chain, right?

JP Mullin: It’s not that hard, actually. Just this morning, over 100 million OM tokens had already been bridged from Ethereum to the mainnet. Yes, a large amount has entered the market.

But let’s be clear: we did not sell these “liquid” tokens ourselves. We sold only long-locked, non-tradable portions.

Host: I understand your official stance—you don’t sell liquid tokens. But existing holders of older tokens could use them to build positions. So when an exchange sees someone using these tokens as collateral for a massive position, they might worry: “This looks valuable on paper, but there’s little real demand or liquidity.” So they force-liquidate. Is that the core issue?

JP Mullin: Why do these tokens look valuable on paper but aren’t worth that much in practice? Is it due to liquidity? This isn’t about locked tokens as collateral—it’s about freely tradable tokens deposited on exchanges.

I believe exchanges have their own risk controls. We’ve communicated with some, but such liquidations should be between the exchange and the investor.

Typically, this doesn’t happen overnight—it involves ongoing dialogue. I wasn’t part of this specific conversation, so I can’t comment on details. But from what we observed, the liquidation was extremely aggressive and swift, which is why we’re paying close attention and exploring all possible legal remedies.

We’re working with investors to evaluate all viable options.

Host: I also want to discuss your previously announced token plans, since this incident followed shortly after your first airdrop round, which included efforts to prevent Sybil attacks—people creating fake wallets to claim multiple airdrops.

As a founder, what’s your take on the timing between the airdrop and the liquidation? Did this expose early risk signals—e.g., tokens wrongly distributed to ineligible recipients?

JP Mullin: Honestly, I think it was just an unfortunate coincidence. We completed our first 10% airdrop a few weeks ago—it was delayed.

Let me briefly explain our overall tokenomics: in February 2024, we announced the first airdrop of 50 million tokens, valued at $5–10 million at the time. Later, the valuation rose to $400–500 million.

This meant some received zero-cost tokens, which understandably concerned long-term buyers. So we adjusted vesting rules to balance interests. Still, we proceeded with the first airdrop round.

We also filtered airdrop addresses for Sybil attacks—and found massive abuse. Hundreds of thousands of addresses tried gaming the system, which we clearly don’t want. We’re committed to protecting genuine community members who supported us financially.

We made filtering decisions in March, and the 10% initial airdrop was distributed one to two weeks ago.

Host: So let me clarify: why protect the cost basis of users who paid for tokens? Logically, it’s to prevent those who got free tokens from harming those who invested real money, right?

JP Mullin: Exactly. I think it’s important—if someone uses their hard-earned money to support your project and token, I genuinely feel responsible.

As a founder, it’s not just a fiduciary duty—it’s a personal commitment I deeply believe in.

When we discover people exploiting loopholes to grab airdrop tokens and dump them onto loyal holders, it harms our project. I won’t allow that.

Of course, we welcome participation. After the airdrop, over 200,000 wallet addresses remained active on the mainnet.

These are real users who passed our anti-Sybil checks, no fake identities. They’ve transacted and continue holding—we must protect them.

And it’s not just mainnet addresses—we also have over 100,000 original ETH holders, excluding exchange wallets. So this affects a vast user base, and I take it very seriously.

Host: Since you take this responsibility seriously, as a founder you have two key duties: first, ensure vesting mechanisms are clear and enforced—some projects don’t even implement locks.

Second, regarding the token’s price surge you mentioned—sometimes, when liquidity is low, market makers use minimal capital to pump prices artificially.

Your case is unique: an existing token, a new L1 mainnet, and a two-way swap mechanism between tokens.

As the founder, did you ever feel uneasy watching this? You said you didn’t want anyone buying at the top. But if there’s insufficient real trading volume or activity to support rising prices, it creates artificial inflation.

Across crypto, many founders and market makers gamble—betting that the team will eventually drive demand higher than current and future token supply, especially in projects with built-in airdrop + unlock mechanics.

How do you view this game? In this incident, how much responsibility lies with the founder?

JP Mullin: Let me explain some adjustments we made to our tokenomics—that’ll give you better context.

When revising the vesting schedule for the airdrop, we also restructured the team’s token release. Team tokens remain locked at Anchorage, wallet addresses are public, and documented in our transparency report.

As part of the new airdrop rules, we extended the team and advisor vesting to one of the longest in the industry: 30-month cliff (zero release) + 30-month linear unlock.

I originally held early ERC tokens, but I returned them and reset the vesting. My personal tokens are now locked for another six years—on top of the four and a half years I’ve already spent building Mantra. We’re in this for the long haul.

I’ll stay with this project through highs and lows. This isn’t our first storm. I accept responsibility for this incident. This situation was unprecedented. I do believe there was malicious behavior involved, and we’re investigating exactly what happened.

The reason I’m sitting here doing this interview, why I flew to Korea for the summit, why I’m being as transparent as possible—is because this project matters deeply to me, and the community means everything.

We’ll keep doing what’s right, supporting the community forward. Through good times and bad, I’ll carry this burden. This is one of our toughest moments, but we’ll push forward, building on our solid foundation alongside strong partners.

Host: You mentioning “malicious behavior” is new info—can you elaborate? To me, it sounds more like someone held a large position and got liquidated. Isn’t that just market behavior, not necessarily “malicious”?

JP Mullin: The timing was highly suspicious, and the entire sequence felt too “clean,” not random at all. You don’t typically see such a waterfall-style liquidation erupt overnight.

This is why we’re investigating thoroughly to uncover what really happened.

Situations like this rarely happen instantly. If you’ve experienced margin calls or loan liquidations, you know—if you communicate with the exchange or lender, offer additional collateral or negotiate solutions—they won’t just wipe out your entire position, especially not a $100M+ one all at once.

Such a massive position requires careful management. Our impression is that this wasn’t handled properly, which is why we’re digging deep—because so many people were hurt.

Host: I agree, but this is exactly what observers are focusing on—the relationships between market makers and your communication gaps. From our outside perspective, we can only speculate. As the project lead, you’re best positioned to know the truth. So the core question remains: how did this happen?

Many argue the logic is simple: if a token’s price isn’t driven by organic supply-demand but artificially inflated by participants, then during a correction, exchanges may deem the price “unrealistic,” seeing weak real demand. Once no one buys, it collapses rapidly.

From that angle, triggering liquidation seems “reasonable.” As the founder, I assume you’ve been part of discussions around tokens, circulation, exchange listings, volume distribution—surely you understand how these relationships work?

JP Mullin: To some extent, yes. Some exchanges proactively contacted us: “What’s going on with these tokens? Where did they come from? Why are they being used as collateral?”

They’d send me a wallet address—one newly created and funded from another exchange, appearing completely unfamiliar.

I couldn’t determine where these tokens originated, especially if they came from a centralized exchange. Obviously, we work with several market makers who are also investors. I’m happy to name them: Laser, Amber, and Manifold Trading. These are our investment partners.

I can clearly state: we have never collaborated with market makers to manipulate or pump the token price. We simply don’t have the capital for that. The funds Mantra raised over the past 12–16 months are limited. This isn’t something we’d do—I publicly declare that.

As for token value, you can judge fairness however you like—that’s for the market to decide. I hope we ultimately achieve a fair market valuation for what we’re building.

Over the past 12–15 months, we’ve gained significant traction and executed strongly. We’ve made major announcements and earned broad support—from institutional investors, real estate developers, and Web2 partners like Google.

From a due diligence standpoint, we’ve passed every review. We’re a regulated project—we’ve shown regulators and partners all compliance documentation, maintained transparency, and engaged in open dialogue.

Host: If this is a VARA-approved project, did you discuss the incident with them?

JP Mullin: We reached out to them immediately. We’re in constant contact. Everyone wants to understand what happened. We’re committed to transparency—showing every fact and piece of information.

Beyond recovery plans, next comes a detailed post-mortem—publicly disclosing all facts, wallet data, etc. We’ll share everything we know to rebuild community trust and clearly demonstrate our side of the story on-chain.

Shorooq has published their wallet, Laser has too, and we’ve shared ours. We’ll keep releasing more—maximizing transparency. We’re not hiding—we’re right here.

How Will the OM Token Evolve?

Host: Let’s continue on transparency. As I said earlier, Shorooq released their report denying involvement in the sell-off. Regarding transparency, where do we go from here? What’s the path forward for Mantra? How will the OM token develop? Because as you said, many questions remain.

Before this happened, while preparing for our chat, I saw a Twitter discussion where someone raised transparency concerns. You responded: “We’re not pumping anything, nor am I saying it’s a bad or good investment. We’ve always been transparent from day one, and recently released another report for the community.” I wanted to clarify which report you meant.

I’m not sure if you meant the feedback loop issue, but the main concern is supply dynamics. Even Binance recently flagged warnings about OM listing due to concerns over increasing supply. Could that be what you were referring to?

I’m referring to the transparency report we previously shared, listing different categories. I’m happy to provide the link—it was published about a week ago.

As mentioned, throughout Mantra’s history, we’ve consistently updated the community on OM token issuance and supply. This began last year when we merged the ERC and new chain tokens, following governance votes and approval from the ERC20Mantra community—all verifiable. Over recent months, we’ve continued issuing updates (though I don’t have links now, I’m happy to share).

You can see the evolution. We work closely with Binance and other exchanges—whenever tokenomics change, we notify them immediately. Any economic changes are proposed via verified governance, media articles, etc., and we directly share them with Binance and others.

I know Binance was aware of this change—precisely why many exchanges chose to support it, including Binance. We communicated this change to them; they knew about the supply shift. This isn’t new—it happened back in October.

It strikes me as odd, especially your proposal for a “one-to-one mirrored burn.” Was there ever discussion about converting some tokens if supply is too high? As we discussed, OM’s supply is already substantial.

I’m reviewing the proposal now—many refer to it as that type. I recall it had 91 votes. I remember you saying many thought we were finished when we did this. As Mantra’s leader, can you walk us through that decision-making process? Would you do anything differently in hindsight?

JP Mullin: I wouldn’t change it. In fact, if that proposal hadn’t passed, we wouldn’t even have a Mantra Layer 1 chain.

Originally, we planned to use the Mantra ERC token and build a fully independent L1 chain, distributing a new token called Omega AUM via airdrop to OM holders.

We discussed this with investors and core team members in late 2023 and early 2024—when almost no one had heard of Mantra.

Back then, our token had dropped 95%, and many believed we were done. Then came an improbable recovery, fueled by OM’s repricing, the launch of Mantra’s chain for RWAs. These narratives combined with our efforts brought us to where we are today.

About the “mirror bucket”—when we created the new supply for the chain, everything was public. Every supporter knew the details. From the moment the proposal was published, we communicated openly.

The mirror bucket acts as a bridge between ERC and mainnet tokens. We effectively mirrored the existing ERC supply—one-to-one—and it’s fully verifiable on-chain. When users send ERC tokens, they’re sent to a burn address—about 100 million tokens burned so far.

The process allows one-to-one redemption of fungible tokens. You can even see it on Bybit—they list both ERC OM and Mantra-chain OM. You can deposit ERC OM and withdraw Mantra-chain OM, and vice versa.

We set a 30,000-token threshold. Below that, deposits are auto-filled within minutes—once verified as sent to burn, new tokens are released. Above 30,000, a manual process kicks in requiring multi-sig approval to release tokens, taking up to 24 hours to ensure security given the large sums involved.

Even at launch—I forget OM’s price then—but hundreds of millions, even billions in value sat in that bridge wallet. We wanted to prevent it from becoming a target. We also wanted to ensure users correctly bridge tokens to the mainnet—the hub of all new activity and our future direction.

Host: Looking back at that 90% drawdown, considering those who entered at much higher prices, current levels are far below their cost basis. If so, as you said, they may have lost hard-earned money. Do you think you and your team were transparent enough? Did you adequately warn people this could happen?

JP Mullin: I truly believe we’ve done our best to stay transparent. I don’t think the issue lies in transparency. I do intend to keep being as open as possible, showing everyone that we didn’t sell, and neither did our investors.

Host: I don’t think people are necessarily angry about you selling tokens. Interestingly, I know you’re not in the U.S., but the SEC recently clarified their stance on transparency. Specifically, they said if you’re involved in crypto trading, you must disclose who your market makers are, reveal your agreements, identify potential token holders, and explain supply changes—that’s essentially their requirement.

So if we were to start over today, with OM trading at 70 cents versus its near-$7 peak—down to 1/10th—what would you do differently? If discussing protocol transparency, especially regarding large market makers or investors’ cost bases—which could pressure supply—what would you disclose to new stakeholders?

JP Mullin: I think the best thing we can do now is publish as much on-chain data as possible—showing where tokens are, what happened.

Host: But that’s on-chain. I meant off-chain aspects—agreements, OTC deals, etc. That’s what I’m asking about.

JP Mullin: I believe the off-chain parts are relatively public—especially our vesting schedule, which we’ve disclosed from the start.

We’re clearly willing to provide all information related to any monetary association agreements. We’re fully committed. I’ll support this, we’ll publish—but we can’t do everything.

Now, investors want to know what happened. I appreciate you raising both on-chain and off-chain aspects. We’re fully committed to providing as much information as possible—I give you my word.

Mantra’s Future Roadmap

Host: What comes next is undoubtedly the big question—and likely why so many are tuning into this conversation.

I’d like to give you space to share your next steps and roadmap. Frankly, I hadn’t heard of Mantra before this—possibly due to geography, differences between your location and New York/global crypto users. At least, I hadn’t heard much.

But now, given the real-world assets on this chain, you said funding isn’t abundant. When you mention buybacks and recovery plans, I’d say—even you might agree—it’s nearly impossible to return to previous levels. But how do you view the path back, and what assets can you realistically operate with now?

JP Mullin: Of course, we’ve been here before. We once dropped over 95%, everyone thought we were done, but we came back. We know we can do it again.

From a founder’s perspective, I’ll do whatever it takes to ensure the community is cared for. That matters more than anything. We need to act now in this difficult moment, restore normalcy, and support our community.

We have strong long-term institutional partners. I mentioned our company is well-funded, business remains healthy, and we’ll keep executing our plans. Post-event, institutional interest has surged—we’re thrilled to see that.

We’re committed to doing everything we can for the buyback plan—starting with my personal founder tokens, which I’ve re-locked. Financial gain isn’t my focus now—truthfully, it never was. My priority is ensuring we restart and move forward.

We’ll work with partners like Shorooq, Laser, and others to design a reasonable buyback plan, coupled with a burn mechanism to visibly reduce unnecessary supply. I’ve already spoken with investors—they’ve committed to supporting this initiative.

Host: Clarifying what you just said about normal procedures and liquidations—if there’s institutional demand or investor interest, could they step in during such moments? Are you saying those conversations haven’t happened?

I mean, until now, regarding demand—your comments about institutional and investor support—are they reflecting the post-90%-drop reality?

JP Mullin: It happened very fast—almost overnight. A Sunday night surprise, sudden and with little time to react. I was asleep.

We’re clearly working with token-holding partners who’ll continue supporting us, with financial backing. We’ve also attracted new investors interested in the project, ready to support and participate.

Seeing new investors join feels encouraging. They understand our track record and that we’ve faced challenges before. We’re ready to rise again.

Host: On a personal level, I’d like to ask—how has this affected you? You’ve worked on this project for a while. I’ve seen your past interviews, from Home to pre-mainnet launch last year.

Personally, having gone through this, how do you reflect on the journey? I’ve interviewed many founders—Do Kwon after Terra’s collapse, SBF after FTX, and others.

After experiencing such volatility, do you feel any sense of relief? I know today you clearly don’t sound relieved. But given the token’s price drop, maybe now at lower levels—like you said, you’ve survived similar crashes before—do you think “maybe we needed this reset”?

JP Mullin: Not at all. Setting aside market value, this isn’t something I’d feel relieved about. An unprecedented event occurred—many lost money and were hurt. I feel absolutely no comfort from that.

I feel frustrated. Today has been extremely tough. I’m heartbroken for our community, for those who lost money, for our team, for international investors—it’s truly awful. Honestly, I feel terrible.

This isn’t something I’d ever feel relieved about. I feel awful, but I’m committed to doing everything I can—spending every waking hour to fix this, do the right thing. I stand by these words. I believe those who’ve seen our journey over the past five years will support me on this. I’ll keep my promises and do everything possible to support this project, take responsibility, and not run away.

Host: You said you feel awful—I want to understand which part weighs on you. Clearly, the price drop is one thing, but you said it wasn’t your fault. So besides price, what specifically troubles you?

Because you said you didn’t sell, and your investors didn’t. So from an outsider’s view, especially those outside the Mantra ecosystem—what do you think you did wrong?

JP Mullin: I’m pained that people who believed in this project and token lost money—people uninvolved in the event, waking up to find their tokens down 80%, 90%. It’s devastating. I feel for those who supported us.

Host: Part of that responsibility lies with you, doesn’t it? To clarify finally—where exactly do you feel this pain? Is it about something you did?

JP Mullin: They believed in me, believed in this project, and ended up losing money. As I said, as a responsible founder, I feel accountable to token holders and supporters. I can’t avoid it—I feel for them, honestly, I don’t know how else to put it.

I feel sad. I feel our community was hurt, our holders were hurt, our foundation was hurt. I feel responsible—even if I didn’t act negligently or maliciously, I still bear great responsibility.

Host: Curious—if your investors were hurt, are they really in loss if the token now trades at $0.70?

JP Mullin: I don’t think they’re in loss—that’s exactly why investors holding liquid tokens haven’t sold any.

Host: So perhaps they weren’t impacted much, while later entrants bore the brunt. As you said, that’s why we’re having these conversations, why we’re talking to you. Maybe if we’d spoken earlier, more people would understand your project and its RWA connection—a clearly hot sector.

Seems you’ve endured a long journey, handling what comes next. One final message—what would you say to those holding this token?

JP Mullin: First, thank you for giving us the chance to share our side. Again, we’ll create a plan ensuring full transparency—disclosing what happened and where things went wrong.

Follow my personal Twitter and our company account—this information will be shared there. We’ll roll out our buyback and burn plan in the coming days, doing everything possible to support investors. We’ll maintain ongoing communication with the community. I promise, community—we’ll do everything we can to fix this.

Thank you to those who’ve supported us and reached out—your support means the world. To those doubting us now, we’ll keep working tirelessly and emerge stronger than ever.

Host: I’m very grateful. Sometimes people avoid transparency and updates. This situation is relatively unique, especially with the weekend timing. I believe sharing everything you know is exactly the kind of transparency this space expects.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News