Deep Dive into Synthetix: Current Ecosystem Status and V3 Outlook

TechFlow Selected TechFlow Selected

Deep Dive into Synthetix: Current Ecosystem Status and V3 Outlook

Synthetix will ultimately serve as a liquidity-as-a-service platform that can be easily integrated into new products.

Author: THOR HARTVIGSEN

Translation: TechFlow

Synthetix has recently seen significant growth. This article aims to explain what makes Synthetix unique today, its recent performance, and why V3 represents a major innovation in DeFi.

Current State of Synthetix

Synthetix was launched in 2017 by Kain Warwick and Justin Moses. Originally known as Havven, the project offered a stablecoin (nUSD) backed by over-collateralized crypto assets. Since then, the protocol has evolved significantly, now offering synthetic versions of various assets on Ethereum mainnet and Optimism.

Today, Synthetix serves as a liquidity layer for many DeFi protocols. On Synthetix, users stake the native SNX token to mint sUSD (synthetic USD). Thus, sUSD is Synthetix’s native stablecoin, over-collateralized by SNX, representing users’ debt within the protocol.

Therefore, the total available liquidity usable by protocols built on Synthetix depends on the amount of collateral (i.e., SNX) deposited into the protocol. Why would users stake SNX to provide this synthetic liquidity? Because stakers earn rewards in native SNX tokens and also receive fees generated from using this synthetic debt (currently yielding around 40% annually). If the amount of staked SNX falls below a certain threshold, additional SNX issuance is triggered to attract more users to stake and increase liquidity.

The liquidity on Synthetix supports two types of assets: spot and perps (perpetuals). Synthetic spot assets track various underlying assets such as cryptocurrencies, commodities, forex, etc. This allows users exposure to these assets without actually holding them. Synthetic perps allow users to trade leveraged futures contracts on various assets. The liquidity on Synthetix acts as the counterparty to these trades. As a result, SNX stakers assume counterparty risk. This means that if traders on protocols leveraging Synthetix's liquidity (e.g., Kwenta) make large profits, the stakers' debt increases—and vice versa. However, mechanisms exist to mitigate this risk, including arbitrage opportunities (funding rates) provided when trading activity becomes skewed. These are designed to make liquidity providers (SNX stakers) hedged-neutral, while V3 will introduce isolated risk pools.

Kwenta

As of now, Synthetix’s total value locked (TVL) stands at $375 million, meaning $375 million worth of SNX has been staked. One example of a protocol built atop Synthetix and utilizing its liquidity is Kwenta. Kwenta is a perpetual futures trading protocol on Optimism that lacks native liquidity and instead inherits it from Synthetix. All trading pairs on Kwenta are priced in sUSD, so to trade these synthetic assets, users must either stake SNX or purchase sUSD on the open market.

All trading fees generated on Kwenta are paid out to SNX stakers. On average, Kwenta accounts for approximately 60–70% of all fees generated by protocols leveraging Synthetix’s liquidity. Other protocols/front-ends built on Synthetix include:

-

Lyra;

-

Thales;

-

Kwenta;

-

dHedge;

-

Polynomial.

Infinex

Infinex is an on-chain perpetual exchange designed to simulate the centralized exchange trading experience in a decentralized manner. Since user interface and experience are central to the protocol, both “simple” and “professional” modes will be offered to make onboarding new traders easier.

The protocol will not have a new native token but will instead be governed by SNX. Furthermore, all revenue will be used to deepen liquidity on Synthetix by purchasing and staking SNX. Higher trading volume leads to greater buying pressure on SNX and deeper liquidity—potentially creating a positive feedback loop.

Synthetix V2 Metrics

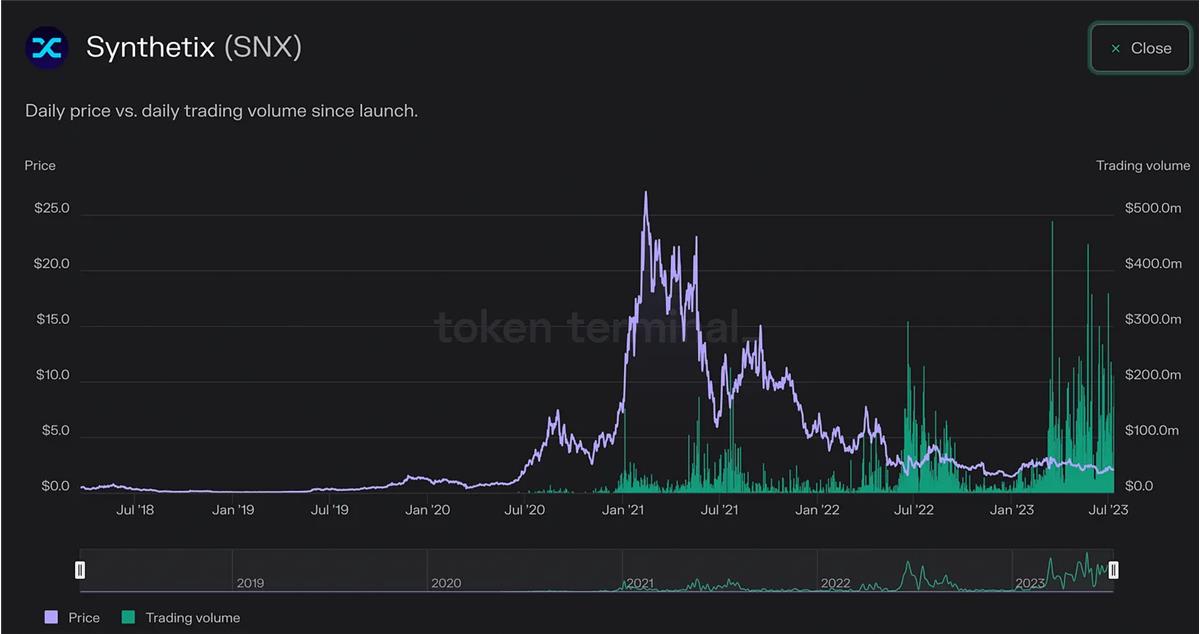

Below is a chart from Token Terminal showing the price of SNX alongside trading volume generated by protocols using Synthetix’s liquidity. As shown, there is currently a significant divergence between recent on-chain activity and the current price of SNX.

Recently, Synthetix has launched several products, with the Perps V2 upgrade playing a key role in driving increased activity. This upgrade introduced various synthetic assets usable on protocols like Kwenta. Notably, Synthetix received substantial OP tokens from Optimism, which were used to incentivize usage on platforms like Kwenta. Additionally, Kwenta issued its own KWENTA tokens to further boost incentives.

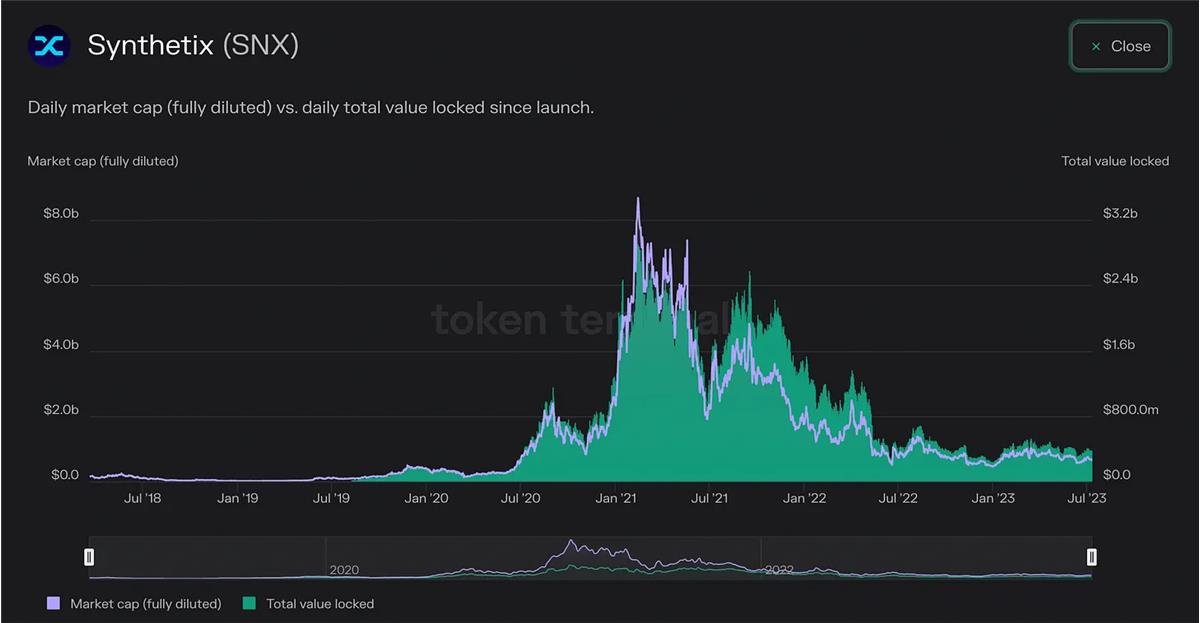

Below is a chart of TVL, which in Synthetix’s case is directly tied to the price of SNX, as illustrated. This is because, as previously mentioned, SNX is the only asset that can currently be staked on the protocol.

Synthetix is core infrastructure in DeFi, with its liquidity being used by multiple protocols, as noted above. Currently, the limitation on liquidity—or TVL—is that only SNX can be staked on Synthetix. This will change with V3.

Synthetix V3

Synthetix V3 includes a suite of upgrades that elevate Synthetix to a new level: becoming a cross-chain liquidity layer for DeFi. V3 is currently in alpha, with different features rolling out gradually.

TLDR

-

Multi-collateral, not just SNX;

-

Permissionless liquidity layer;

-

Developer-friendly ecosystem;

-

Seamless cross-chain functionality.

Multi-Collateral Staking

Multi-collateral staking is one of the core principles of the Synthetix V3 vision. Currently, only SNX can be staked to provide liquidity for synthetic spot and perpetual markets. V3 introduces a vault-based design, where each vault represents one type of collateral (token). One vault could hold ETH, another SNX, and a third wBTC. The types of collateral accepted into these vaults are added via governance. Additionally, vaults can be pooled together for use by protocols seeking specific liquidity. For instance, a pool might consist of an ETH vault and a DAI vault, which could then be used by an on-chain derivatives market like Kwenta. Key benefits include:

-

As a liquidity provider, you can choose which asset to deposit as collateral and earn yield, enjoying greater flexibility.

-

Since pools are linked to specific markets, stakers can avoid unwanted risks. Risk-averse investors may only provide liquidity to pools used by BTC and ETH markets, avoiding exposure to higher-risk assets.

-

Better hedging becomes possible since pools are associated with specific markets, reducing counterparty risk.

Permissionless Liquidity Layer

With V3, developers can create new markets on Synthetix that leverage liquidity pools in a permissionless manner. A major hurdle in DeFi is bootstrapping liquidity early on, often requiring large token emissions.

Beyond selecting which liquidity pools their market should integrate, market creators can also choose their preferred oracle and define custom reward structures for liquidity providers. Listing new synthetic assets no longer requires governance approval and can be done seamlessly. These assets could range from spot OP to ETH options.

Ultimately, Synthetix will function as a "liquidity-as-a-service" platform, easily integrable by new products.

Seamless Cross-Chain Functionality

The ultimate goal of Synthetix V3 is availability across any EVM-compatible chain. "Teleporters" will enable liquidity supplied on one chain to be used on others. For example, if a user provides liquidity to a pool on Optimism, a market on Arbitrum can utilize that same liquidity to support its platform.

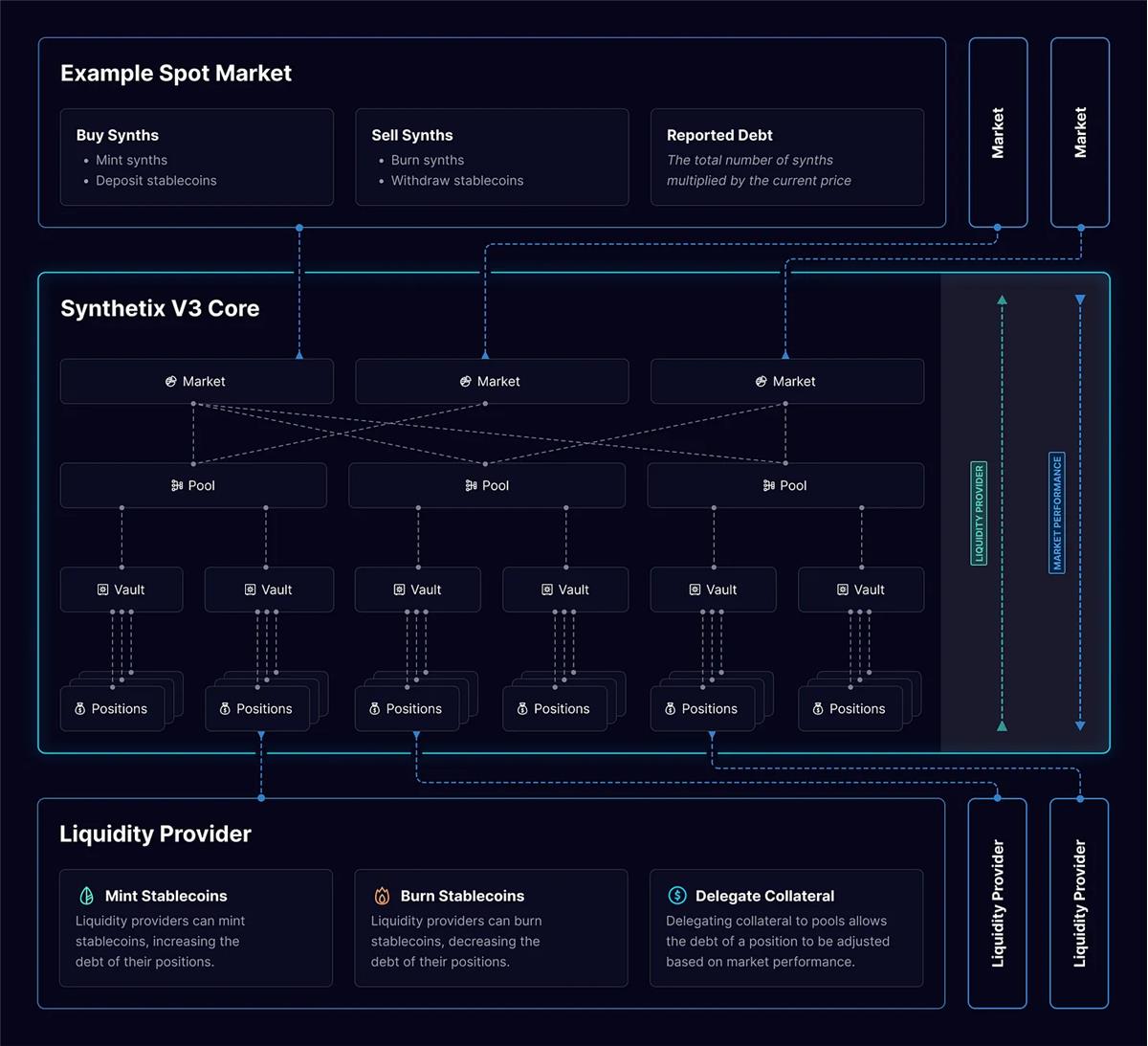

Below is an overview of the structure of Synthetix V3 spot markets: Users deposit assets into vaults, which are added to specific pools. These pools can then be used by protocols to build markets atop Synthetix’s liquidity layer. These markets are what users interact with through dApps built on Synthetix, such as Kwenta.

Path to V3

A brief outline of the roadmap leading up to the full release of Synthetix V3:

Stablecoin Migration — V3 introduces a new synthetic stablecoin to replace the current V2 sUSD. The name has not yet been finalized, though one proposal is to keep the new stablecoin as “sUSD” and rename the current V2 version to “oldUSD” or “legacyUSD.” Over time, as the new V3 stablecoin and synthetic assets gain liquidity and utility, users will need to migrate their assets from V2 to V3 (via Curve pools).

Perps V3 — Perps V3 will introduce the multi-collateral functionality described earlier. Most importantly for traders on protocols like Kwenta and Polynomial, all synthetic assets (not just sUSD) will be usable as margin for trading. The UI/UX will also become simpler and more intuitive. Most core code is complete and nearing audit. Testnet launch is expected in late July.

Upgrade V2 SNX Stakers to V3 LPs — This feature allows current SNX stakers to migrate to V3 without needing to repay debt or close positions. (SIP-306).

Teleporters — Teleporters are a critical component of V3’s cross-chain capabilities. To enable cross-chain liquidity usage, they burn sUSD on one chain and mint it on another, eliminating slippage and reliance on traditional cross-chain bridges. Teleporters are currently under development and running on several testnets. (SIP-311).

Cross-Chain Pool Synthesis — Another core component required to achieve fully interconnected liquidity. It enables markets and pools to recognize the state of collateral on other chains. With this capability, a new perpetual market can launch on one chain and leverage liquidity from another. This is currently being tested on testnets (SIP-312).

Conclusion

Synthetix’s endgame is highly ambitious and exciting, but success hinges on generating demand and attracting developers to build solutions using Synthetix as a liquidity layer. The more protocols (like Kwenta) that build on Synthetix, the higher the yields earned by liquidity providers (stakers on Synthetix). As yields rise, more liquidity is supplied, and deeper liquidity attracts even more protocols to build on top. This creates a self-reinforcing positive cycle.

As noted earlier, 60–70% of fees earned by SNX stakers come solely from traders on Kwenta. Trading on Kwenta is heavily incentivized by large emissions of OP and KWENTA tokens, making it difficult to accurately assess the true extent of recent user growth.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News