The Biggest Hidden Winner in the Liquid Staking Bonanza: Lending Protocols

TechFlow Selected TechFlow Selected

The Biggest Hidden Winner in the Liquid Staking Bonanza: Lending Protocols

Could lending protocols potentially earn more profits from LSDs than the LSD protocols themselves?

Author: capitalismlab

Could lending protocols potentially earn more profits from LSDs than the LSD protocols themselves?

Yes, you heard it right. After Ethereum's Shanghai upgrade, this potential could be fully realized. This isn't just about investment or arbitrage opportunities—it also includes clear-cut airdrop prospects. Let’s break it down.

First, let's look at current data.

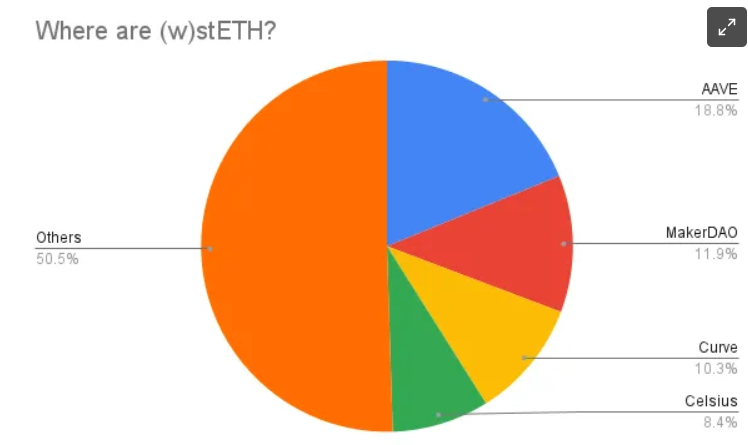

For stETH—which hasn't yet enabled unstaking and still experiences significant price volatility—31% is currently deposited in two major lending protocols, Aave and MakerDAO, with smaller amounts on Compound and Euler. Even though this potential hasn't been fully tapped, it already firmly establishes stETH’s largest use case to date, surpassing Curve which holds only 10%.

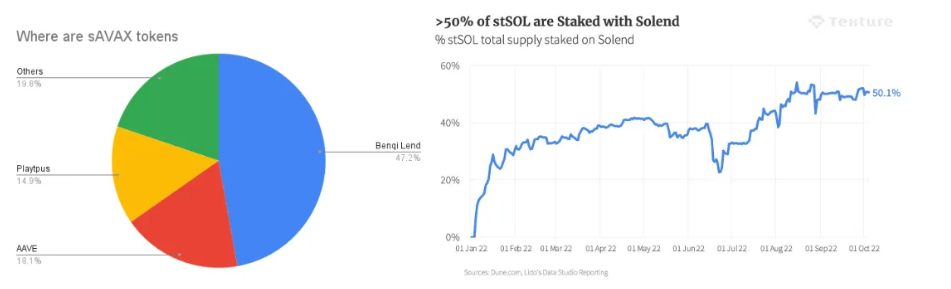

What might happen after unstaking goes live? Let’s take Avalanche (Avax), an alternative Layer-1 with a relatively mature DeFi ecosystem. There, Benqi and Aave together hold as much as 65% of all sAVAX (Avalanche’s LSD). Back when Solana was thriving, over half of all stSOL was deposited on Solend, Solana’s largest lending platform; adding other protocols like Larix brings the total close to or above 60%.

Why is this happening?

Two main reasons:

LSDs are inherently high-quality collateral—and they keep earning yield while pledged. They’re popular across the board, from 3AC to hackers exploiting Wormhole.

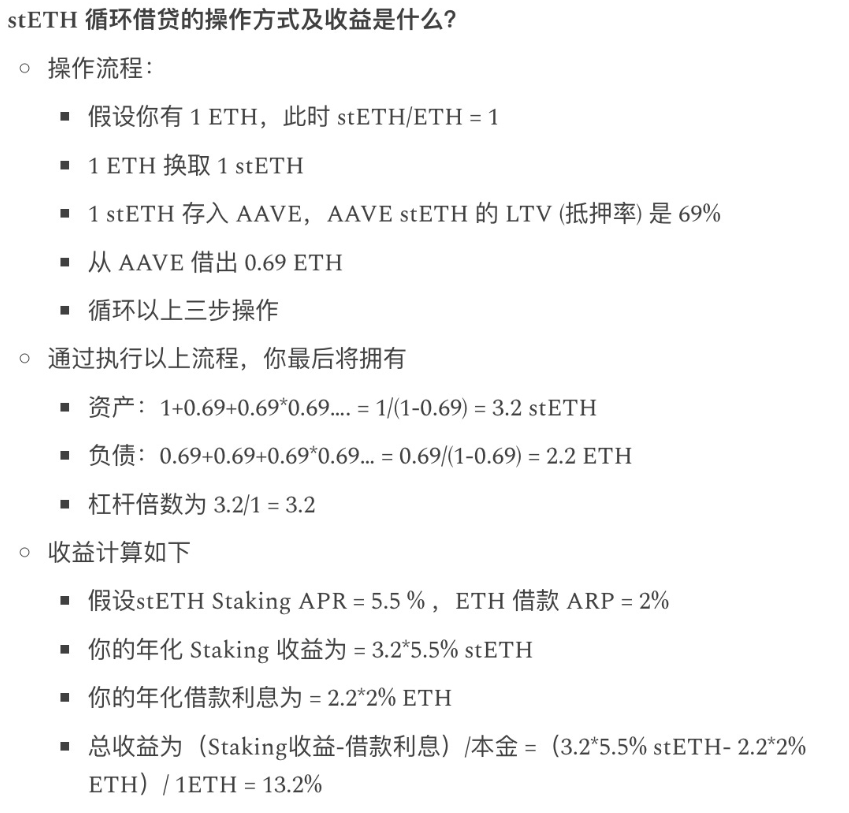

Leveraged staking is the primary engine driving LSD growth. The correlation between collateral and borrowed assets allows for higher returns with relatively low liquidation risk. See the chart below for details.

At its core, lending protocols act as conduits that transmit staking yields back to native assets. For example, circular borrowing of stETH significantly boosts Aave’s ETH interest rates and volume, which then propagates through the broader DeFi ecosystem integrated with Aave and influences other platforms, thereby raising ETH’s base interest rate.

Given how lucrative LSDs have become, lending protocols have introduced optimized policies for them. Take Aave V3’s eMode: if you're only borrowing ETH, stETH can be used as collateral with a Loan-to-Value (LTV) ratio as high as 90%. Similarly, Compound V3 offers comparable terms for stETH and cbETH. Under such conditions, 1 ETH can effectively become 10 stETH, rapidly expanding stETH’s scale. Arbitrageurs who buy stETH at a discount can leverage this mechanism to amplify their gains tenfold.

Based on the above data, we can estimate lending protocol revenues. Assume total LSD staking rewards amount to X, with 60% of LSDs held in lending protocols, average LTV = 75%, borrowing rate equals 75% of staking yield, and protocol fee share is 15% (as with Aave on ETH). Then, income earned by lending protocols would be: X × 60% × 75% × 75% × 15% = X × 5.1%. Compare this to Lido’s protocol revenue split, which stands at just 5%.

This stems from the fact that lending protocols face higher entry barriers and place greater emphasis on historical credibility (for instance, Aave continues to pull ahead of Compound despite lacking liquidity mining incentives). With competition now largely plateauing, these protocols can afford higher fee margins.

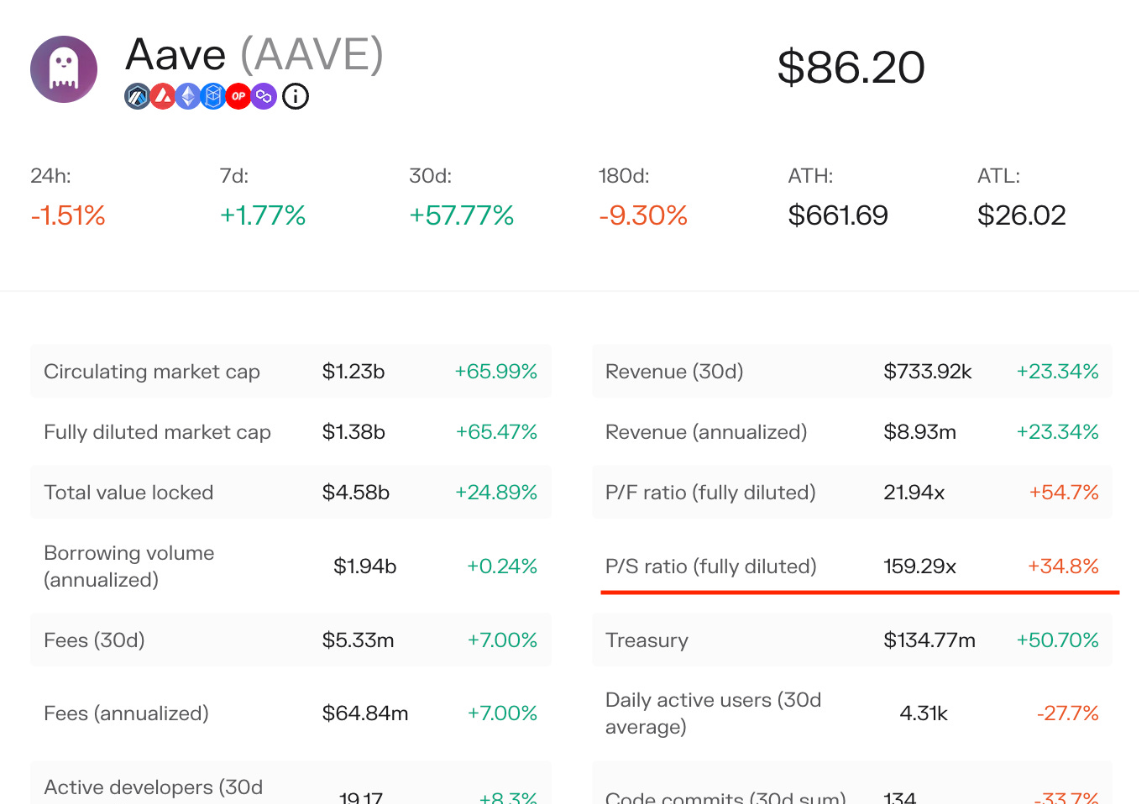

As outlined above, with the upcoming Shanghai upgrade set to boost LSD adoption and reduce price volatility, lending protocols stand to quietly generate massive profits. However, it’s important to note that valuations based on Fully Diluted Market Cap / Protocol Revenue remain high across the board—for example, AAVE trades at around 160x. Even with this favorable catalyst, valuations won’t appear cheap. Thus, this opportunity hinges on shifts in market narrative.

Catching a rising narrative isn't easy, but there are several airdrop opportunities worth watching here.

LSD collateralization naturally creates new demands:

To avoid liquidation under leveraged positions, users need proper leverage management tools.

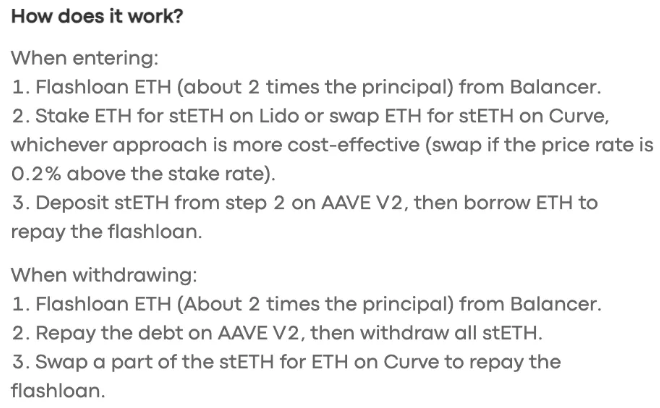

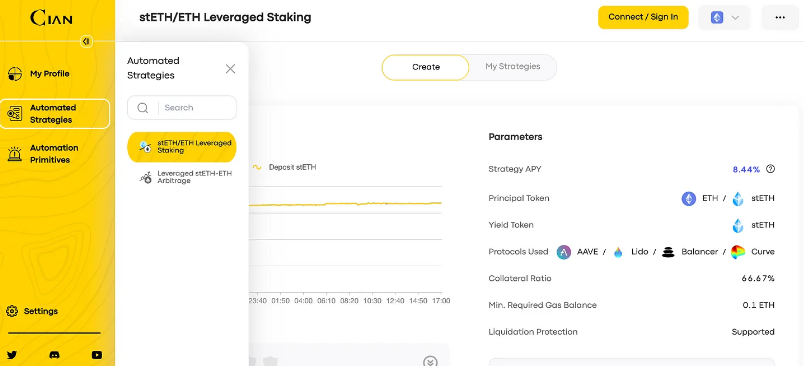

Leveraged staking operations are cumbersome and gas-intensive. Using flash loans simplifies the process, especially when combined with automated strategies (see example strategy at cian.app).

One notable project is DeFiSaver, a well-established player in DeFi position management that hasn’t yet launched a token. Its core offering focuses on leverage management and provides numerous one-click automation strategies tailored for LSDs. Despite operating for over three years and profiting handsomely during the last bull run, its intentions regarding token issuance remain unclear. That said, since DeFiSaver has expanded to Arbitrum and Optimism, trying it out costs little in gas fees.

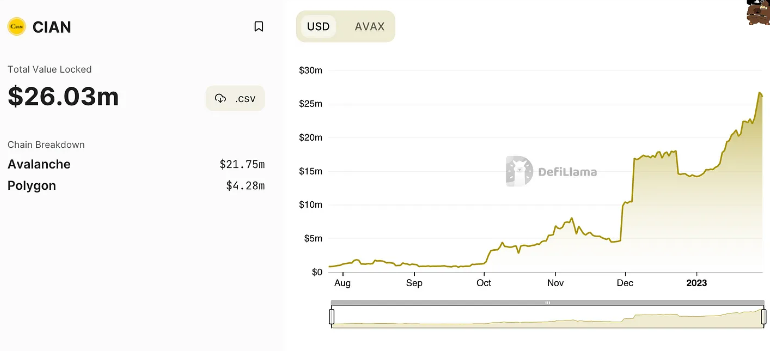

The other key player is cian.app, which currently specializes in LSD-focused automated strategies. This project appears to be conducting a transparent airdrop campaign, frequently launching NFTs and hinting in AMAs that a token launch is expected in 2023. Judging by its TVL growth, traction looks promising.

Cian supports Ethereum, Polygon, and Avalanche. A quick visit to its homepage reveals mostly LSD leveraged staking strategies. Their plan to launch a token in 2023 seems clearly aimed at capitalizing on the momentum from the Shanghai upgrade.

In summary, lending protocols may ultimately earn income from LSDs rivaling that of LSD protocols themselves. However, given their current high valuations, further price appreciation will likely depend on evolving narratives.

Leveraged staking genuinely amplifies staking returns and presents tangible airdrop opportunities today. But because leverage introduces higher risk, thorough research is essential.

Further reading: Ethereum Shanghai Upgrade Approaches: How to Scientifically Maximize ETH Staking Returns?

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News