Deep Dive into FTX's Balance Sheet: A Textbook Case of Bank Run

TechFlow Selected TechFlow Selected

Deep Dive into FTX's Balance Sheet: A Textbook Case of Bank Run

Do not underestimate the liquidity pressure of a bank run.

Written by: Degg_GlobalMacroFin, published with author's permission

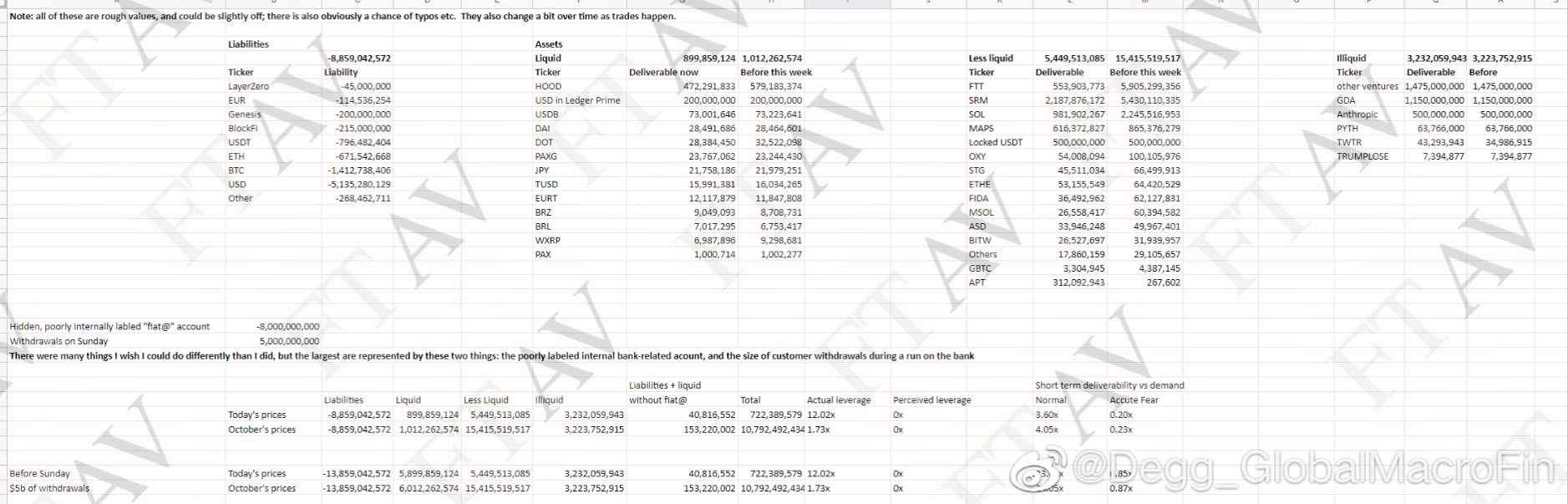

1. The Financial Times has just released a balance sheet reportedly from FTX’s final moments, appearing to be SBF presenting FTX’s financial condition to potential investors (Figure 1).

This balance sheet not only shows what FTX looked like in the last second before its Chapter 11 bankruptcy, but also reveals how it suddenly plunged into irreversible collapse since last weekend.

One could say this balance sheet is a perfect textbook case of a "banking crisis."

2. Let's first examine FTX’s balance sheet condition before the run began (last Saturday).

At that time, FTX had approximately $24 billion in total assets at market value.

-

About $6 billion consisted of liquid assets, including various stablecoins, fiat currency deposits, and Robinhood shares.

-

Additionally, about $15 billion in various crypto assets, labeled by SBF as “less liquid,” including $6 billion in its own issued FTT, $2.2 billion in SOL, and $5.4 billion in SRM.

-

Finally, $3.2 billion in illiquid assets, primarily venture investments. Some speculate that FTX held so many SBF-related assets (SOL, FTT, SRM) because SBF used customer funds deposited on FTX to support his personal holdings. Others suggest FTX used tokens such as FTT, SOL, and SRM as collateral to lend to Alameda, and these tokens on the balance sheet actually represent a consolidated statement between FTX and Alameda (SBF indicated on this balance sheet that FTX provided approximately $8 billion in loans to Alameda).

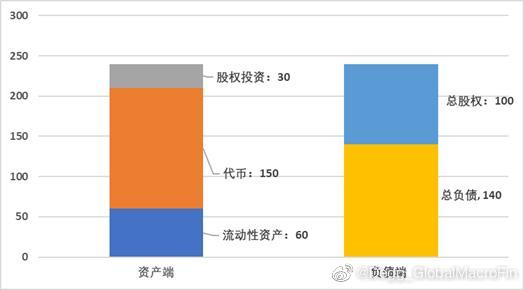

On the liability side, FTX had about $14 billion in liabilities last Saturday, including at least $5 billion in USD or USD-pegged stablecoin obligations, along with significant BTC and ETH liabilities. At this point, FTX’s net equity (total assets minus liabilities) was approximately $10 billion.

In other words, prior to last Saturday, FTX’s leverage ratio was only 1.4x—SBF was indeed still a billionaire at that moment (Figure 2).

3. Now let’s look at FTX’s liquidity situation last Saturday.

SBF estimated that FTX typically experienced average daily withdrawals of around $250 million. Therefore, even without new inflows, SBF expected the $6 billion in liquid assets would cover roughly 24 days of withdrawal demands (similar to the traditional banking concept of “liquidity coverage ratio”), giving FTX ample time to liquidate token holdings or secure funding elsewhere.

4. However, the bank run that started on Sunday far exceeded SBF’s expectations.

In this document, SBF stated that on Sunday (November 6), FTX faced withdrawal demand 25 times higher than normal. Within just a few days, net outflows reached $5 billion, including at least 20,000 BTC and large amounts of stablecoins.

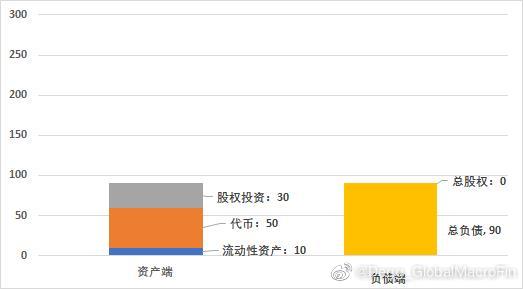

The result of the run: FTX’s total liquid assets dropped from $6 billion to just $1 billion (it is unclear whether the $5 billion outflow occurred entirely on Sunday or accumulated between Sunday and Wednesday).

At this point, FTX’s $1 billion in liquidity reserves faced a daily outflow pressure of $5 billion (though unsustainable long-term). The coverage ratio thus collapsed from 24x (60/2.5) to just 0.2x (10/50). In other words, if withdrawals were not suspended, FTX could survive only for a few hours.

5. Alongside the evaporation of liquidity came a sharp plunge in prices of FTX-related assets.

It is unclear how much FTX itself sold on secondary markets, but FTT, SRM, and SOL prices fell approximately 90%, 60%, and 60% respectively since last week. This caused the market value of FTX’s less liquid assets to shrink by two-thirds—from $15 billion down to $5 billion.

SBF did not record any impairment on its illiquid holdings, but most of these are tied to crypto venture investments whose market values are hard to assess and likely significantly diminished.

Therefore, after experiencing the run and asset write-downs, FTX’s pre-bankruptcy balance sheet looked like this: On the asset side, only $1 billion in liquid assets remained, $5 billion in tokens, and $3 billion in illiquid assets carried at book value but likely worth far less. On the liability side, approximately $9 billion in liabilities remained, $5 billion of which were denominated in USD.

In short, at this stage FTX was no longer merely facing a liquidity crisis—it had become a full-blown solvency crisis.

It was insolvent (Figure 3).

6. FTX’s collapse within just a few days is a textbook example of a bank run, exhibiting nearly all the classic characteristics of a run on a bank—especially a dealer bank (investment bank):

(1) Engages heavily in risk transformation and liquidity transformation, using customer funds for high-risk, low-liquidity investments.

(2) Grossly underestimated vulnerability to runs, causing seemingly sufficient liquidity buffers to deplete within one or two days.

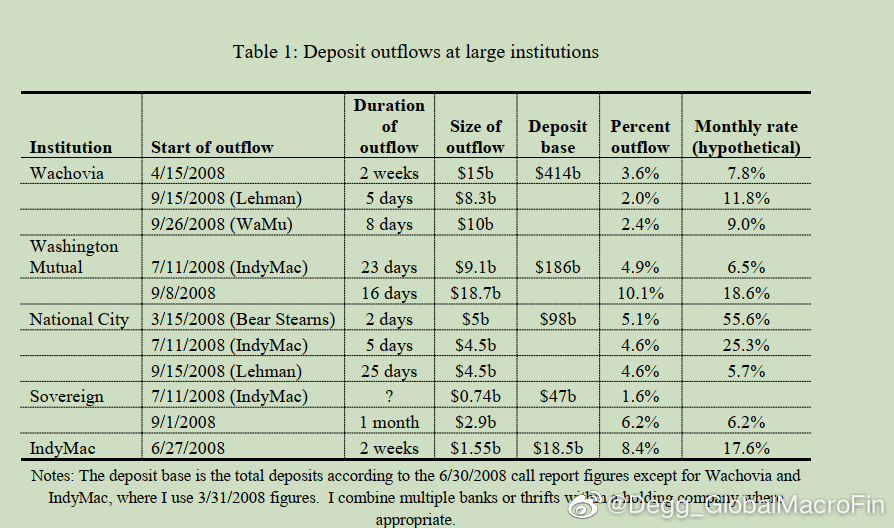

It should be noted that runs in the crypto space occur entirely on-chain, making them far more intense than in traditional banking systems.

In traditional commercial banking, a 10% net deposit outflow over a month already constitutes a severe crisis (Figure 4).

For investment banks, Lehman Brothers saw its liquidity reserves drop by $40 billion in one week before collapse—about 8% of total assets.

In contrast, FTX’s case shows that a single day’s net outflow at a crypto exchange can reach as high as one-third of total liabilities.

This represents an extremely severe liquidity stress—such that virtually any financial institution operating with fractional liquidity reserves would be doomed, let alone an aggressively managed entity like FTX potentially involved in Ponzi-like schemes.

(3) Assets marked-to-market easily fall into a death spiral of run → fire sales → falling prices → declining equity → intensified run. What made FTX even more reckless was holding massive quantities of its own tokens—akin to a bank buying its own stock and self-capitalizing.

(4) Information spreads extremely fast, combined with fragile market sentiment, accelerating the giant’s sudden collapse.

7. SBF wrote a rather insightful summary in this document.

There were many things I wish I could do differently than I did but the largest are presented by these two things: the poorly labeled internal bank-related account, and the size of customer withdrawals during a run on the bank.

In translation: The two things I regret most are: improperly managing credit dealings with Alameda, and underestimating the liquidity pressure during a bank run.

8. FTX’s $20 billion bank run case deserves a place in every monetary and banking economics textbook.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News