380 million USD at stake? Interpreting Chinese creditors' legal basis and pathways to claim recovery from the FTX motion

TechFlow Selected TechFlow Selected

380 million USD at stake? Interpreting Chinese creditors' legal basis and pathways to claim recovery from the FTX motion

This article aims to conduct an in-depth analysis of the issues related to this motion and the current state of rights protection for Chinese creditors from three perspectives: the motion system, legal application, and case comparison.

Author: Guo Ruofei Lucius

"The judicial experiences from the Mt.Gox and Celsius cases have provided favorable references and practical support for Chinese creditors seeking claim rights in the FTX case. Although the current FTX motion path shows tendencies of closure and exclusivity, there remains discretion within the bankruptcy court. As long as Chinese creditors act appropriately, there is still hope to achieve recognition of their rights and actual compensation."

On July 2, 2025, the FTX Recovery Trust submitted a "Motion to Implement Restricted Procedures in Potentially Restricted Jurisdictions" to the U.S. Bankruptcy Court in Delaware, requesting the establishment of differentiated payout mechanisms for creditors in 49 jurisdictions—including China. The core content of this motion can be summarized as follows: if local counsel hired by the trust determines that making payments to a particular jurisdiction would violate local cryptocurrency regulatory laws, creditors from that region will have their claims reclassified as "disputed claims," potentially resulting in them being entirely deprived of repayment rights, with such claims taken over by the FTX Recovery Trust.

According to relevant statistics, Chinese creditors hold $380 million in claims, accounting for approximately 82% of total claims from restricted regions. This motion has also triggered widespread attention across the Web3 space and legal practice circles in the crypto industry—not only because it affects the claim rights of hundreds of thousands of Chinese investors, but also due to its potential long-term impact on the future application of law, user protection boundaries, and compliance pathways for global crypto enterprises facing cross-border bankruptcies.

This article aims to analyze the issues raised by this motion and the current status of rights protection for Chinese creditors from three dimensions: motions procedure, legal applicability, and comparative case analysis.

1. Introduction to Motion Practice and Preliminary Analysis of the Current Motion

Before analyzing disputes surrounding this motion, it is necessary to first introduce the basic mechanism of "motion practice" in U.S. bankruptcy proceedings. A motion under U.S. bankruptcy law refers to a formal application filed by debtors, creditors, or other interested parties to the bankruptcy court regarding specific procedural matters or substantive requests. Its legal basis typically comes from the Federal Rules of Bankruptcy Procedure, supplemented and enforced by specific local court rules.

Under Chapter 11 of the Federal Bankruptcy Code, motions may cover an extremely broad range—from asset disposition, claim verification, priority repayment order, to denial of creditor eligibility as seen in this case—all of which can be initiated through the motion process. Motions usually require submission of formal written documents (Motion Briefs), stating legal grounds and factual assertions, along with supporting evidence. For motions involving significant procedural rights, the bankruptcy court often schedules hearings to hear opinions from relevant parties before reviewing whether procedures are compliant and whether the motion's arguments are valid, then issuing a ruling. In other words, the motion system constitutes a critical component of U.S. bankruptcy proceedings and serves as an essential tool for participants to advance their interests.

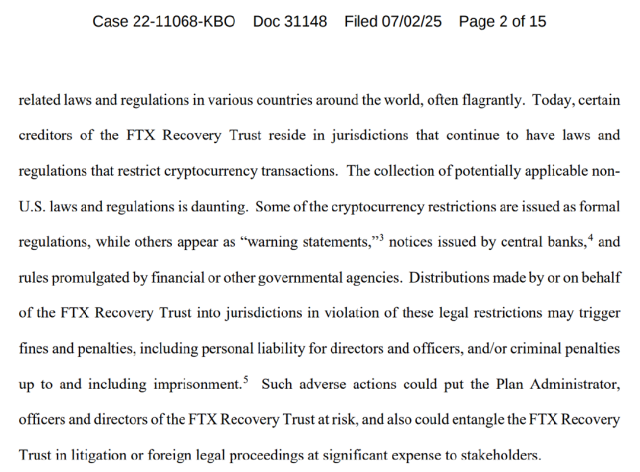

In this case, the FTX Recovery Trust invokes Section 105(a) of the U.S. Bankruptcy Code (granting courts power to issue necessary orders), Section 1142(b) (authorization for plan execution), and Rule 3020(d) of the Federal Rules of Bankruptcy Procedure, requesting the court authorize the trust to implement "Restricted Jurisdiction Procedures." The motion seeks to deny payouts to claimants from 49 "potentially restricted jurisdictions" listed in Attachment B, including China, Russia, Egypt, Nigeria, and others. The FTX Recovery Trust argues that cryptocurrency regulations in these jurisdictions could lead to fines or penalties (Fines and Penalties), undermining the legality of debtor repayments and exposing responsible personnel to criminal liability (Criminal Penalties).

(The image above shows part of the original text from the motion filed by the FTX Recovery Trust, explaining the primary reasons behind the motion)

The substantive issues raised by this motion go beyond whether U.S. law permits exclusion of certain creditors' repayment rights; more fundamentally, they concern whether a court can deny claim eligibility based solely on a creditor’s origin from a "restricted country," touching upon complex controversies at multiple levels. The following sections will conduct detailed analysis from both substantive and procedural law perspectives.

2. Scope of Legal Application and Key Controversies: Procedural vs. Substantive

From a substantive law perspective, the central defense cited by the FTX Recovery Trust is that "making payouts to users in restricted jurisdictions may violate local cryptocurrency asset and foreign exchange control regulations." While this argument appears on the surface to fall within the scope of bankruptcy administrators’ “compliance risk management,” it contains at least two clear flaws in terms of legal application and interpretation:

First, the logic underlying the motion confuses the nature of payment instruments versus settlement assets. The assets FTX intends to use for payouts are not cryptocurrencies per se, but U.S. dollars or court-approved stablecoins (such as USDC, USDP), which are not directly restricted within international payment systems. Precedents exist in both the Celsius and Mt.Gox bankruptcy liquidation cases—bankruptcy administrators in those cases successfully made settlements via SWIFT international wire transfers or stablecoin transactions to individual creditors located in restricted jurisdictions (including China and Russia) under court supervision, without triggering compliance exemption requirements or regulatory disputes from local authorities.

Second, the motion misapplies Chinese laws and administrative regulations. Under China's current legal framework, there is no comprehensive prohibition on individuals holding cryptocurrency assets or receiving overseas cryptocurrency payments. The September 4, 2017 joint announcement by the People's Bank of China and six other ministries titled "Notice on Preventing Risks Associated with Token Issuance Financing" primarily targeted financial institutions and ICO platforms participating in token issuance and trading. Similarly, the September 2021 notice issued by the PBOC and nine other ministries, "Further Notice on Preventing and Addressing Risks of Virtual Currency Trading Speculation," further strengthened crackdowns on trading platforms but did not invalidate the legality of individuals passively receiving or holding cryptocurrency assets. More importantly, civil courts in various regions have already recognized in certain judicial practices that digital assets such as BTC and USDT qualify as "virtual network property," falling under the protection of Article 127 of the Civil Code and eligible for enforcement in debt recovery. The same applies in criminal contexts. Therefore, the motion’s interpretation of Chinese regulatory policy lacks general binding force and contradicts prevailing judicial trends.

From a procedural law standpoint, the procedural arrangements proposed in the FTX Recovery Trust’s motion raise several concerns.

While formally adhering to U.S. bankruptcy court procedural rules, the motion effectively introduces a largely closed, trustee-controlled "compliance review mechanism" in operational terms. Specifically, the FTX Recovery Trust unilaterally hires lawyers to issue legal opinions (Legal Opinion) on whether payouts are permissible in specific jurisdictions, requiring these opinions to be unconditional and exception-free (Unqualified Legal Opinion) to be acceptable. If local counsel identifies any potential legal barrier or fails to provide an absolute unqualified opinion, all claims from that jurisdiction will automatically be classified as "disputed claims" (Disputed Claims), suspending payouts or even fully disqualifying claim eligibility. Such a review mechanism is especially prone to causing substantive injustice in areas with ambiguous regulation or opaque policies—like China. For example, given that China currently has no explicit law prohibiting individuals from receiving USD settlement payments or holding stablecoins, local lawyers may still hesitate to issue definitively positive legal opinions due to uncertainty about risks. In practice, even when lawyers believe compliance risks are minimal, professional prudence often leads them to include reservations in their opinions, making "unacceptable opinions" (Unacceptable Opinion) the default procedural outcome.

A more serious issue lies in the fact that this compliance review mechanism is not established or administered neutrally by the court, but rather fully controlled by the FTX Recovery Trust itself. From lawyer selection and instruction issuance to drafting, interpreting, and applying legal opinions, every step is managed unilaterally by the debtor. This kind of review process—where conclusions are predetermined and legal opinions merely serve to justify them—bears a strong resemblance to 'shooting the arrow first and drawing the target afterward.' Furthermore, this procedure has not undergone substantive judicial scrutiny. If the court accepts the motion solely based on legal opinions submitted by the debtor, it effectively delegates decision-making power over repayment rights of entire national creditor groups to legal advisors controlled by the debtor. Such a design runs counter to the fundamental principle emphasized in U.S. bankruptcy law of fair treatment of similarly situated creditors and systematically disadvantages creditors from specific jurisdictions like China.

Beyond this, jurisdictional issues in the case remain controversial. As a territorial court, the U.S. Bankruptcy Court generally exercises jurisdiction only over U.S.-based debtors and their assets. However, FTX’s customer base is highly globalized, and its platform liabilities involve complex transnational contractual relationships beyond purely domestic U.S. law. Most Chinese creditors opened accounts through FTX’s international platform without explicitly agreeing to U.S. law or exclusive jurisdiction of U.S. courts. Thus, whether a single-jurisdiction court can universally exclude claim eligibility of users from certain countries based on policy considerations remains legally debatable. According to general principles of private international law, while insolvency proceedings have centralized liquidation effects, they must not arbitrarily deprive foreign creditors of legitimate claim rights, otherwise violating the spirit of international instruments such as the Hague Convention on Choice of Court Agreements and UNCITRAL Model Law on Cross-Border Insolvency. Should U.S. courts adopt "compliance risk" as a general basis for motions, this precedent might be replicated by other debtors in future cross-border bankruptcy cases, further weakening the legal standing of foreign creditors.

3. Comparative Case Study

The FTX case is not the first time a major crypto platform’s bankruptcy has triggered cross-border claims disputes. Past precedents show that Japan’s Mt.Gox case and the U.S.’s Celsius case offer typical comparisons for this situation. Though arising under different legal systems with varying regulatory stances, both share key characteristics: large-scale cross-border creditors, massive crypto asset liquidations, and tangible impacts on Chinese users’ rights. Judicial approaches, trustee roles, and payout principles in these cases form important reference points for analogical analysis in the FTX case.

(1) Mt.Gox Case

Mt.Gox is one of the most iconic exchange bankruptcy cases in Bitcoin history. In 2014, Mt.Gox declared bankruptcy due to system vulnerabilities and massive BTC theft, with over 20,000 creditors spread worldwide, including a significant number from China. The case fell under the jurisdiction of Tokyo District Court and applied Japanese bankruptcy law and later the Civil Rehabilitation Act. In procedural design, the court imposed no restrictive thresholds based on user nationality or regulatory risk, instead implementing a unified "creditor portal system" to collect global claims, offering multilingual interfaces including Chinese and English, thereby lowering procedural barriers.

More crucially, the Japanese court required the trustee to propose a "pro-rata payout + residual BTC physical return" plan, without distinguishing between creditors based on their home country’s stance toward virtual currency regulation. For instance, despite China having issued the "Notice on Preventing Risks Associated with Token Issuance Financing" at the time, this did not affect the progress of claim verification or payouts for Chinese users. Throughout the process, the Tokyo District Court maintained high levels of judicial neutrality and transparency. Trustees regularly published multilingual updates and responded to collective objections. Ultimately, most creditors received compensation via JPY, wire transfer, or BTC. The Mt.Gox case demonstrates that even in complex cross-border scenarios, as long as judicial procedures are fair and uniform compensation standards are applied, the regulatory complexity of crypto assets does not constitute sufficient grounds to prohibit or restrict external creditor repayments.

(2) Celsius Case

Celsius Network, one of the largest U.S. crypto lending platforms, filed for Chapter 11 reorganization in 2022 and was handled by the U.S. Bankruptcy Court for the Southern District of New York. Like FTX, Celsius faced a large number of cross-border creditors, particularly across Asia and Europe.

In terms of procedural arrangements, the bankruptcy court and creditor recovery corporation established a global creditor portal open for claim submissions, supporting multiple languages and allowing creditors to choose preferred payout methods—U.S. dollar stablecoins or equivalent BTC/ETH. Notably, the Celsius case did not attempt to exclude creditors from any specific country via motion nor establish a list of "restricted jurisdictions." Regarding Chinese users in the Celsius case, although China maintains strict cryptocurrency regulations, the Southern District of New York did not accept "potential compliance obstacles" or "foreign exchange controls" as grounds to exclude or freeze repayment rights for Chinese creditors.

More importantly, the court upheld the fundamental principle of equal creditor repayment under bankruptcy law, clearly stating that unless there is an explicit legal prohibition or a request for assistance from a foreign court, foreign creditors’ rights cannot be unilaterally denied due to regulatory ambiguity. Indeed, a large number of mainland Chinese creditors in the Celsius case completed initial payouts by early 2024, mostly verifying identities through third-party KYC platforms and receiving USDC transfers or corresponding BTC allocations—demonstrating the court’s dual-track approach emphasizing both substantive review and procedural safeguards.

Taken together, the precedents of Mt.Gox and Celsius show that in judicially led, transparent bankruptcy frameworks, even when creditors reside in countries with unclear crypto regulations or foreign exchange restrictions, courts tend to uphold basic civil rights and advocate the principle of 'non-discriminatory participation,' offering valuable guidance for Chinese creditors pursuing remedies in the FTX case.

First, from a judicial philosophy standpoint, whether it is the Japanese court opening claim channels to Chinese creditors and offering local currency payout options in the Mt.Gox case, or the U.S. Southern District of New York explicitly rejecting the use of "regulatory uncertainty" to disqualify Chinese claim eligibility in the Celsius case, modern courts handling cross-border crypto bankruptcies increasingly emphasize substantive review and equal participation rights. Particularly in the Celsius case, U.S. courts refrained from invoking any nation’s regulations to block payouts to users from mainland China, instead achieving a balance between risk control and compliance through procedural tools like KYC and identity verification.

Second, regarding the bankruptcy court’s discretionary mechanisms, while U.S. bankruptcy procedures grant debtors certain motion rights and procedural design flexibility, final decisions still require substantive judicial review. Considering the current trajectory of the FTX case—including submitted opposition statements from representatives of Chinese creditors and widespread protests from the global creditor community—it is reasonable to expect that the court may not unconditionally accept the FTX Recovery Trust’s argument to exclude creditors from restricted jurisdictions, possibly favoring a more nuanced, region-by-region adjudication approach. Under such circumstances, if Chinese creditors organize collective legal action through attorneys, formally file oppositions to the motion, and actively participate in hearings, their claims still stand a chance of being recognized and compensated by the court.

Of course, the ultimate outcome of rights protection efforts will depend on how the court ultimately balances conflicts between 'compliance barriers' and 'procedural equality,' as well as between 'some creditors' and 'all creditors.' If the court adopts the reasoning in FTX’s motion, Chinese creditors may need to pursue appeals or seek diplomatic channels to correct the procedure.

In conclusion, the judicial experiences from the Mt.Gox and Celsius cases have provided favorable references and practical support for Chinese creditors seeking claim rights in the FTX case. Although the current FTX motion path shows tendencies of closure and exclusivity, the bankruptcy court still retains discretionary space. As long as Chinese creditors take appropriate actions, there remains hope to achieve recognition of their rights and actual compensation.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News