From "Paradigm Shift" to "Attention Shift": Narrative vs First Principles

TechFlow Selected TechFlow Selected

From "Paradigm Shift" to "Attention Shift": Narrative vs First Principles

Fish care about water quality; we must have a clear understanding of everything happening around us.

By: Xiao Xiaopao

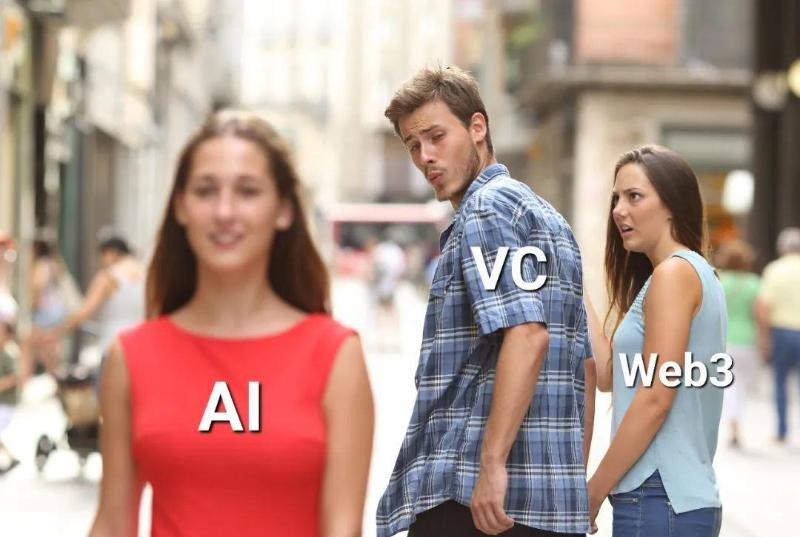

Yesterday I was flooded with "AIGC" (AI Generated Content) all day. Late at night, feeling inspired, I made a little image and shared some thoughts.

I didn’t expect this casual meme to go viral so quickly—much faster than those big buckets of "first principles" from the "Liberal Arts & Sciences" series. I can't help but marvel at how fast VC's "sector rotation" spins—faster than a windmill, with no real "tracks" or "paradigm shifts," just an “attention shift.”

This brought back my old theory—the “narrative machine” and my “four narrative formulas”:

-

Low attention + positive sentiment = potential opportunity

-

High but scattered attention + positive sentiment = cautiously bullish

-

High but scattered attention + negative sentiment = cautiously bearish

-

High and focused attention + negative sentiment = collapse

-

High and focused attention + high excitement = bubble

This was originally a game in the secondary market, but now seems fully applicable—and deeply internalized—in the primary market.

Replacing "financial markets" in the text with "VC," "venture capital," or "primary market" feels completely natural.

Three years later, the only upgraded insight is the importance of “first principles” and “underlying logic”—which is exactly where I and “Liberal Arts & Sciences” are heading today.

Sharing the article again today:

One day, a caterpillar struggled to climb up a leaf stem. It reached the tip, fell, climbed again, rolled down, then tried once more…

What comes to mind?

To me, it’s Sisyphus—the Greek mythological figure condemned to eternally push a boulder uphill, only for it to roll back down. Ah, even a lowly caterpillar embodies relentless perseverance.

But here’s the reality: that caterpillar is most likely infected by Ophiocordyceps unilateralis—the zombie fungus. The fungus invades its brain and nervous system, takes over its body, forces it out of its nest, climbs to the top of a plant, and makes it repeat Sisyphean motions—just like a zombie.

That same fungus lives in my head too. Because I interpreted what I saw through my own worldview, assigning grand meaning to the caterpillar. I see what I want to see, understand what I want to understand. This fungus is everywhere—in every human brain, influencing everyone’s actions, creating this kaleidoscopic world.

In finance, this Ophiocordyceps fungus is called “narratives.”

Every “idea” in financial markets is wrapped in a story. Stories emerge, evolve, and eventually die. But if an “idea” is strong enough, it survives beyond any single story’s lifespan, jumps into a new narrative, and gets reborn.

That’s why in finance, we constantly see the cycle: “starts with innovation, collapses due to abuse.” New ideas emerge, change the world, then time moves on—“when Pompeii became my fiefdom, Pompeii was already ruins.” That’s the fate of narratives.

Of course, finance isn’t just about storytelling, and macro analysis isn’t something anyone with a license can do. Compared to this mountain, I’m neither hardcore nor an expert. But I love literature, history, and philosophy—older I get, the clearer it becomes that these disciplines explain finance better.

The most common thing in finance? Absurdity. As Camus taught us: absurdity arises because humans still have expectations. We’re emotional, full of desires, while the world is cold and indifferent—utterly unconcerned with fulfilling our wants. This mismatch creates disharmony, opposition, absurdity.

When you turn to humanities for answers, you often find them. Here, you see “people”: their emotions, their absurdities, their grand and subtle actions. This is where the world’s most fundamental laws reside. Using humanities to interpret financial narratives breaks down as follows: “literature” tells the story; “philosophy” checks whether the story is logical, reasonable, and convincing; “history” judges how long the story will last.

Unfortunately, the world’s noise is growing louder. In an infinite sea of information, cutting through complexity to grasp essence is incredibly hard. As ordinary mortals without leverage or superpowers, in environments where we control nothing, using only our bare senses to distinguish truth from falsehood, the probability of getting wiped out keeps rising.

Thankfully, technology gives us tools. Game theory, sentiment analysis powered by NLP—turning ourselves into cyborgs, using their weapons against them—might be the right path forward.

Taking the chance of a Live session, I organized my work and, with humble understanding, tried to discuss from a more practical angle the role of “narratives and game theory” in macro analysis, investing, and trading. Below is the transcribed recording, shared for your reference.

1. Narratives: The Third Presence in Markets

1. What are financial market narratives?

There’s a unique presence in financial markets: Narratives.You can translate it as “market narrative” or simply “story.”It’s intangible—a subjective interpretation. Whether trading or investing, people often say: “watch the market narrative,” meaning listen to the stories the market is telling.

Narratives are hard to perceive directly, but you frequently encounter them in news and commentary. For example:

They appear on mainstream media sites, in economists’ or commentators’ columns. If you pay attention, you’ll often spot the word and sense its presence.

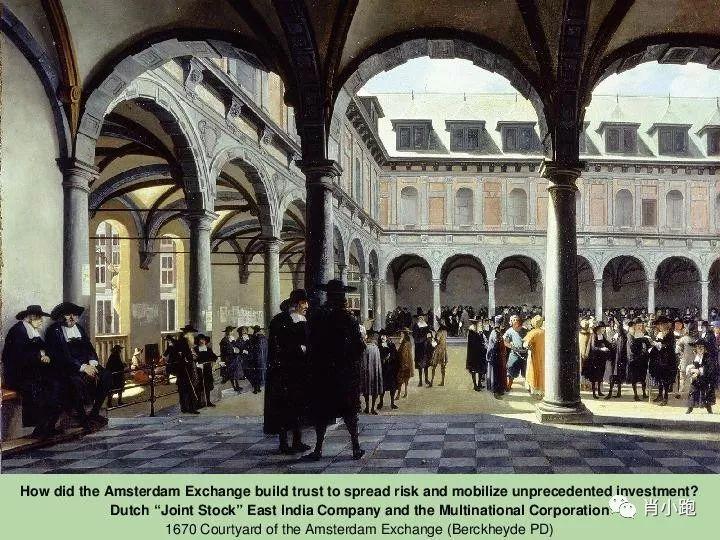

2. “Narrative” has existed since the birth of “markets.”

You’ve probably heard the English phrase “corner the market”: meaning to corner the market, force a short squeeze, blow up longs/shorts.

Where does this term come from?

Ever since the Dutch established the world’s first stock exchange (the Amsterdam Stock Exchange) over 400 years ago—or even earlier, 2,000 years back at Rome’s Temple of Castor, where government and private firms traded “public services”—with the emergence of such exchanges, each company got its own “corner,” its designated spot to trade shares. Like selling cabbages or pork, they now had a billboard in the public market, a “speaker’s corner,” a place to tell stories.

In other words, narratives, market stories, sentiment—they’re essentially marketing. Not purely objective, but infused with human subjectivity.

Listening to market stories is not only the main (if not only) way we understand a company’s or asset’s “value,” but also a tool companies and assets use to “self-fulfill prophecies,” guiding the market to view value—and even the world—in ways favorable to their interests.

3. Why are Narratives important?

To answer this, ask another question first: Why does the market move? Why is it dynamic? Why do prices rise and fall? And why can’t this motion be as direct as a machine—“on when switched, off when stopped”—or like a thermometer, changing instantly with temperature?

Because markets don’t run on numbers—they run on stories, narratives. Or rather, interpretations of numbers, translated into narratives. Raw data is cold, complex, meaningless. Humans need to turn it into understandable stories. Only then do we gain agency—only then do we act. These actions ultimately impact reality. In markets, that means price volatility.

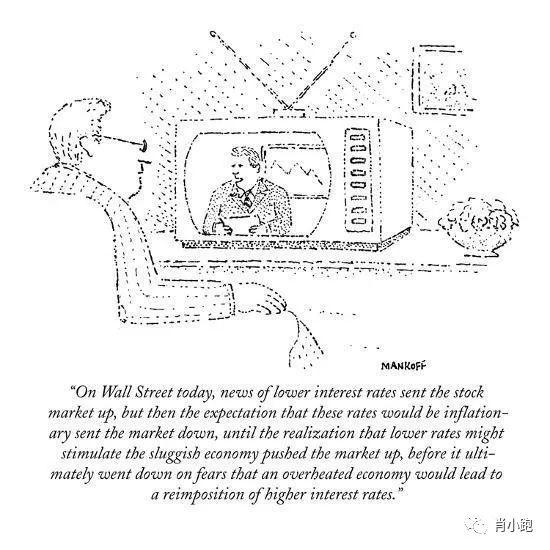

A famous cartoon perfectly illustrates the power of narratives:

"Today on Wall Street: Rate cut news boosted stocks, but fears of inflation from rate cuts soon pulled markets down; then markets reconsidered—low rates could revive a weak economy—so stocks rose again; finally, fear of overheating leading to rate hikes dragged markets back down."

More and more economists and hedge fund legends recognize this—the critical influence of narratives on markets.

Take Nobel laureate Robert Shiller. He even developed a formal discipline: Narrative Economics. The core idea: words and language easily influence mass behavior, thus shaping markets. Stories don’t just inspire—they embed in values, connect actions, and spread virally across regions or even globally.

This may sound obvious, yet it’s often overlooked by scholars, experts, and investors alike—until recently.

What is Narrative Economics? “Stories motivate and connect activities to deeply felt values and needs. Narratives ‘go viral’ and spread far, even worldwide, with economic impact.” Dr. Shiller, 2017.

4. Narratives matter—but are hard to grasp because they keep changing

As markets mature, stories grow more complex. The narratives that drive markets never stop evolving.

Take the narrative of “value investing.” Once near-biblical, it dominated nearly a century starting in the 1930s. After the 2008 crisis, with global liquidity surges and deeper “financialization,” the “central bank” narrative suddenly surged in influence, now almost entirely overshadowing “fundamentals” in investment decisions.

That’s why lately, the gap between asset “value” and “fundamentals” has grown like the distance between a middle-aged man’s eyebrows and hairline.

Too abstract? Let me give real examples:

Story One: The famous “whatever it takes”

Strictly speaking, U.S. equities began rising from May 2009. 2011 was brutal for hedge funds still believing in “Active Portfolio Management” and chasing alpha—dragged down by subprime and European debt crises. By year-end, hedge fund performance was dismal, many legendary names dethroned. Yet until then, the “Quality” narrative still held; active management strategies still worked; alpha still existed.

Then came the turning point—in summer 2012.

The first week of August, at the ECB conference in London, two historic narratives emerged: Mario Draghi’s “whatever it takes” (“不惜一切代价” to save the euro), and “OMT” (Outright Monetary Transactions). These two phrases changed everything.

At the time, many investors held heavy short positions on European financial stocks. Right after the meeting, European markets did drop—shorts made big money. But within two days, a total reversal. That morning, media headlines screamed “Draghi’s major blunder”; by afternoon, it was “Draghi’s bold move.” The narrative flipped instantly.

Spain and Italy—then dubbed the “PIIGS” among PIIGS—were the epicenter of global investor anxiety. But the day after “whatever it takes,” that panic vanished from their stock markets. No trace remained of how bad fundamentals were. From July 26 onward, Spain’s IBEX 35 rose 17%, Italy’s index jumped 13%. The entire European market celebrated—shorts were obliterated.

Many hedge funds disappeared forever in summer 2012.

The surreal twist? Draghi became FT’s Person of the Year. A fool turned hero—“Super Mario.” The nickname stuck.

Morning

Afternoon

Forward Guidance

Everyone knows the term. But what is forward guidance?

Japan pioneered it in 1999. But excessive intervention turned it into “the boy who cried wolf.” Today, Japan’s verbal signals are largely ignored. So they intervene directly—acting, not talking—buying bonds and stocks outright.

Then in 2008, Bernanke adopted it, later perfected by Yellen.

Before Bernanke, the Fed communicated very differently. Greenspan mastered vagueness—his ambiguity was unmatched. Under Bernanke, after several market boosts, he realized: market momentum is marginal. Anything “moves” due to the margin—the final straw.

Where does marginal momentum come from? Expectations, not reality. What drives expectations? Narratives.

So wipe away all ambiguity. Use a megaphone: tell the market exactly your goal. Tell them what to think.

Thus began Bernanke’s post-QE “forward guidance,” locking in market expectations of future central bank policy. By 2013, it wasn’t just the Fed—major global central banks coordinated frequent “guidance.” Starting with Bernanke, joined by Draghi, then Mark Carney at the Bank of England, leaders moved in perfect sync.

Forward guidance has two styles: Odyssean and Delphic. Odyssean is explicit—publicly stating forecasts and targets. Delphic is implicit—hinting through speeches, indirectly signaling policy intent. Earlier, everyone was subtle, mostly Delphic. Over time, less restraint. Today’s “guidance” is blunt, crude, unapologetic.

This central bank narrative game has big side effects. Simple reason: revealing intent makes it easy for markets to exploit—like “die trying.”

2. A Sociological View of Humans and Narratives

1. Why do humans listen to stories?

Human cognition is like a QR code scanner—constantly scanning the world for scannable codes. An unordered, chaotic image becomes “meaningful” through cognitive decoding. This process—telling and hearing stories—is how narratives operate in consciousness.

For thousands of years, “interpreting stories” has been a survival skill. In an uncertain world, we need algorithms or models to turn strange, shocking novelties into understandable stories. Only then can we analyze, respond, survive. That’s why we need stories.

But humans have a serious built-in bug.

A profound influence on me—Edward O. Wilson, an evolutionary biologist, author of three masterpieces: *The Insect Societies*, *Sociobiology*, and *On Human Nature*. He argued Earth has only three truly remarkable species: termites, bees, and humans. These share a key trait: they’re monumental achievements of biological evolution, solving ecological challenges through social organization—unlike most organisms that face problems alone. These are called “eusocial animals.”

As “eusocial animals,” humans must constantly communicate with peers, spreading information collectively, relying on communities to “remember.” Like a giant termite colony. This trait made us the most successful multicellular species on Earth—but also caused many disasters, like destruction by rumors and conspiracy theories—we’re defenseless against powerful, simple, contagious stories.

Once humans form groups, they become nearly identical to sheep. Sheep are animals whose “peripheral vision never leaves companions.” A single sheep is shockingly sensitive to others’ emotions and actions—its own mood and behavior entirely dependent on others. Sociology calls this “other-regarding behavior”—exactly like sheep.

For instance, if one sheep is happy, it must have found good food—the only thing that makes sheep happy. Another sees it, feels “I want that too,” and spreads the emotion until the whole flock converges on the “good thing.” If one sheep panics, others panic too—regardless of why. Result: chaos, gasping, stampede. That’s why sheep pens can’t have narrow doors—no predators needed, sheep trample themselves.

We think sheep are gentle and obedient. But they’re actually the least obedient—each lives in a self-centered universe, “zero altruism” and “overwhelming selfishness” make them the least controllable. They cluster not to “cooperate,” but because being apart, not watching others’ emotions, causes anxiety.

Humans are the same—doing things because others do. Stampedes happen because everyone is fleeing.

This human trait makes us extremely vulnerable to stories—especially those told by people around us. In financial markets, this bug often triggers massive booms and busts.

The classic example: the 1929 U.S. crash. Ten years of “Coolidge Prosperity,” strong indices, beautiful numbers. Suddenly—pitch black, no warning—it hit, plunging into a decade-long depression.

Economists long puzzled over this—no clear cause.

Aliens?

No. Perhaps it happened because of a market narrative—one told by any economist dissenting from mainstream media. Before the market decides which story to believe, it’s like a tug-of-war—volatile, directionless. Until one side adds extra force, tipping the balance.

Then, unnoticed, it becomes real—the elephant in the room.

Next, it turns infectious—starting from a mutation, maybe weather changes, maybe people gathering accelerated bacterial spread. At some unpredictable moment, the overwhelming “moment” arrives.

3. How to coexist peacefully with Narratives in an age of information explosion and omnipresent manipulation?

1. First, become aware. Fish should care about water quality.

Like Bian Zhilin’s poem: I watch you from the bridge—you are the scenery. But you can also be the audience, watching a flock of sheep.

In this era, we need the ability to distinguish when we’re the scenery and when we’re the spectator.

In financial markets, investing and trading are games—but group games, not one-on-one duels. Everyone’s opponent is the herd.

Keynes said “finance is like beauty contests”: guess the winner among many beauties to win a prize. How should you guess? Not whom you find prettiest, but whom others will pick. Even if ugly, if everyone picks her, you should too.

Back to markets: don’t bet on what you think will profit, but on what others think will profit—even if it contradicts your fundamental analysis. Popularity wins. Beauty contest logic applies.

But how do you know what others think?

Here enters a concept from game theory: common knowledge. A related idea is mutual knowledge.

Mutual knowledge is “everyone knows.” Common knowledge is “everyone knows, and everyone knows that everyone knows.” Simplest example: “The Emperor’s New Clothes.” The emperor is naked—that’s mutual knowledge, but not common knowledge. Before the child speaks, everyone knows he’s naked, but no one knows whether others see it too. The lie persists.

Only when the child shouts “the emperor has no clothes!” does it become common knowledge: everyone knows others know.

Like in a bar: if you know there’s a fire but aren’t sure others do, you might still grab a few drinks before the stampede. But if you know everyone else knows—then what? Whoever reaches the door first survives. That’s why news you think isn’t news crashes markets once it hits headlines.

Financial markets are the largest application field of game theory and common knowledge. Why care about mainstream financial media—Bloomberg, Reuters, CNBC, all those apps? Not because their reporting is most reliable, but because market players know others are watching too. When a headline appears, everyone assumes others have seen it.

Headlines themselves don’t immediately impact reality. Seeing “key data released” or “major policy announced” is just seeing “the emperor is naked.” The following “analysis and interpretation” confirm that everyone sees it, and establish a “consensus” on what it means. Your task: how to use that consensus.

2. Then, observe narrative shifts—especially speed and connectivity. Use tech to fight fire with fire.

So here’s the question: Is there a way to symbolize and visualize the “stories” and “sentiments” in news—their evolution—like medical images showing cancer cell spread? Tag emerging stories as “stained cells” and watch them metastasize like cancer?

Ever since Chomsky defined the four types of grammar, turning each language into mathematical expressions, human languages—including high-level programming languages—can follow grammatical rules. This made “machines understanding human language” possible.

Thus emerged NLP (Natural Language Processing)—now a mature technology. Tech giants use it in voice bots or automated recognition systems. Many investment banks apply it to financial fields, like sentiment analysis in forex markets. JP Morgan even created Volfefe Index (I FFF Index) based on Trump’s tweets. Human language—words, phrases, stories, emotions, emotional evolution—can all become measurable vectors. NLP lets machines train in vast text oceans, build large n-gram comparison sets mapped to every story. Visualizing this mapping creates an “emotional cancer spread map” or a “story detector.”

/// What is N-gram? A sequence of N consecutive words.

For example, in the sentence “Xiaopao has a smart brain,” a bigram (2-gram) representation would be:

“Xiaopao, has

has, a

a, smart

smart, brain”In trigram (3-gram):

“Xiaopao, has, a

a, smart, brain”Assuming the probability of the Nth word depends only on the previous N-1 words, the overall sentence probability is the product of individual word probabilities.

This structure helps predict the likelihood of the next sentence. ///

If we can tag N-grams in news articles with sentiment labels, compare them across all articles, and track sentiment diffusion over time, we build a story detector. We can visualize market narratives and monitor their evolution.

Now that we have a story detector—what next?

All this only matters when linked to “money flow.” After all, I’m not a linguist—I want to make money. The link isn’t hard—it works like advertising: “story + understanding buyer sentiment + capturing attention = roughly predicting when people will start buying.”

Every story has a lifecycle: birth, growth, reproduction, death. “Attention” is the story’s life meter. Market stories, their sentiments, sentiment spread—only gain momentum when combined with “attention.” Different combinations of “sentiment” and “attention level” drive capital flows in different directions.

When a story is born, market reaction is like new parents’ heartbeat. A newborn only grabs parents’ attention—not much else. The market must test various angles to label and define the new story.

But eventually, a label emerges. The sign? Investor attention—awareness of the sector or concept, hearing more market discussion, seeing more media keywords. Hear the drumbeat today, enter tomorrow. Capital flows in.

But every story ends—just differently. If a viral story drains all attention and fades, capital flees overnight. Or if a story becomes outdated but still has residual attention, it slowly dies. Or if a story remains captivating but suddenly twists—good cop was a bad mole—capital runs, leaving wreckage.

Summarized simply:

-

Low attention + positive sentiment = potential opportunity

-

High but scattered attention + positive sentiment = cautiously bullish

-

High but scattered attention + negative sentiment = cautiously bearish

-

High and focused attention + negative sentiment = collapse

-

High and focused attention + high excitement = bubble

Another example:

If you recall, the Fed “rate hike” narrative first appeared in 2009. Yet it took nearly ten years for markets to react. What was happening during those years?

Listening to stories. It started with some “talk”—not necessarily from Bernanke, Yellen, or Powell (they say nothing anyway). Instead, stories grew from Ray Dalio’s “70-year debt cycle” or former PBOC governor Zhou Xiaochuan’s “Minsky Moment.” Which exact phrase? Unknown. All you feel is the elephant in the room slowly growing. One day it roars—and you see the bloody Christmas 2018 global stock crash. (High and focused attention + negative sentiment = flee)

What next? Two competing stories—market still unsure which to believe:

One story: “liquidity injection.” Everyone knows this. The other: “consequences of liquidity injection.” This hasn’t converged. The consequences are too terrifying, beyond imagination. Yet it remains the elephant in the room (high but scattered attention + negative sentiment = cautiously bearish).

Practice this regularly when reading news.

Again: fish care about water quality. We must stay清醒ly aware of everything around us.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News