IOSG: How Can X-to-Earn Challenge the Death Spiral?

TechFlow Selected TechFlow Selected

IOSG: How Can X-to-Earn Challenge the Death Spiral?

Expectations for the future story of X2E.

Author: Andy, IOSG Ventures

Editor: Elaine, IOSG Ventures

This article is for industry learning and discussion only and does not constitute any investment advice.

Preface

Since the rise of Axie Infinity, Play-to-Earn (P2E) games inspired by Axie have sprung up like mushrooms after rain. However, after Axie delivered a dramatic performance of a death spiral rollercoaster to both the crypto and gaming communities, no P2E game has yet emerged that can rival Axie’s compelling story: insufficient market cap, insufficient hype, insufficient innovation—or simply not ready.

As a result, Axie's P2E model not only taught other blockchain games a lesson but also gave equally clever non-blockchain markets an idea: If Play-to-Earn can become this popular, could other forms of X-to-Earn (X2E) find opportunities too? Thus, in the past two months, the market has finally seen another exciting X2E product following Axie: STEPN.

I’ll briefly summarize what many research reports have already covered: STEPN is a Move-to-Earn game where users purchase NFT running shoes to earn tokens—currently boasting 1 million users, 300K DAUs, with its governance token market cap rising from an $8 million IEO valuation to $2 billion in under two months.

Given that this article is published while STEPN remains in its growth phase, those who have already joined or are watching from the sidelines—including founders of other X2E projects—are closely asking one question: When will STEPN reach its peak and enter the death spiral? It’s understandable that under Ponzinomics, the death spiral is an unavoidable topic. Yet as market enthusiasm for X2E continues to surge, we must not shy away from discussing the death spiral. Instead, we should proactively understand what it truly means, explore how projects can endure despite its shadow, and examine what kind of operations and philosophies allow users, teams, and investors alike to maximize long-term value. At this moment when STEPN is gaining immense attention—and before more X2E products emerge—I’d like to use Axie and STEPN as case studies to offer several perspectives on the death spiral that I hope will benefit the broader market.

Enough preamble—here are the key takeaways:

While the death spiral may be inevitable under Ponzinomics, this article aims to illustrate the following points:

First, the outcome of a death spiral isn't necessarily death, nor does it mean product failure—it's the process of returning from the frenzy of X2E back to the product’s fair value. The latency period before this occurs varies in length, the speed of decline differs, and the eventual fair value level reached afterward can vary significantly.

Axie, as the first breakout X2E project, went through many trials and errors, revealing the possibilities, limitations, and long-term operational challenges of X2E—enabling successors like STEPN to learn, refine, and innovate. X2E is evolving.

What we hope for in X2E evolution is a more restrained boom phase, a slower cooldown period, and a higher fair-value baseline—something I believe STEPN has the potential to achieve.

Even more importantly, we aim to shift the mainstream user base toward those who recognize the project’s intrinsic fair value, allowing utility-driven investors—not speculators—to capture most of the gains. (We want participants to understand that joining such a project isn’t merely about investing $10 to earn $20, but rather investing $10 that inherently covers the utility value provided by the project, plus an additional $3 returned—and for persistent users, even the possibility of returning $10 or $20.)

Looking ahead, non-Ponzinomic economic inflows represent one of the most promising aspects of X2E, offering far greater narrative depth and room for expansion than current blockchain-based P2E models. For example, I recently discussed an early-stage Bike-to-Earn project (MOTE by Sweetgum Labs—interested investors are welcome to connect) that explores carbon credit monetization and reinjection into the economy. To illustrate: someone who previously drove 10km daily for work switches to cycling, saving 4 tons of CO₂ emissions annually. With carbon priced at €80 per ton in Europe today, this translates to over €300 in theoretical annual revenue flowing back into the system. Future increases in carbon pricing would further amplify this mechanism’s potential. While significant feasibility hurdles remain (e.g., whether carbon exchanges recognize these credits), I’m highly encouraged by X2E projects striving to integrate with external economies.

Sunk Costs and Unexpected Returns

1. Tolerance for Sunk Cost Losses in Investment

Let’s start with an example familiar to most: gym memberships. Most people know the pattern—going three times a week in the first month, then once every three weeks by the tenth month. And if your membership expires and later you reignite motivation only to repeat the cycle—you’re not alone. Why do we repeatedly invest substantial sums, only to surrender repeatedly to low self-discipline, letting this loop persist? Do those who fail again forget their lessons and vow “next time will be different,” only to re-enter the same path?

A key mindset here is tolerance for sunk costs: purchasing a gym membership is an investment in your physique and health (utility). When the initial excitement fades and dust gathers on your card, it signifies a mental acceptance that the investment has failed—a reconciliation with sunk cost.

This might not resonate immediately, so let’s quantify it roughly: a $500+ annual gym membership was bought to motivate you to run 3 times a week, 5km each time. If you only stuck with it for the first two months, the original expected ROI of $5000 translating to 13kg weight loss ends up delivering just 2.3kg—only 15% of intended ROI. Most people’s reaction would still be “Sorry, I’ll try again,” and sign up anew. But imagine this were your ROI in stocks or blockchain investments—would you still say “I’ll try again”? In financial investments, people show low tolerance for sunk costs, whereas for utility investments (body, health, happiness), tolerance is vastly higher.

2. STEPN: Is It Your Financial Investment App or Your Utility (Fitness) App?

An unexpected return for STEPN investors: Consider a friend who experienced Axie and entered STEPN about a month ago. His initial goal, like with Axie, was to make money—plus, running required less mental effort than gaming, eliminating the guilt of “wasting time playing games.” Given equal time investment, he chose STEPN. But after running daily to earn GST, he realized his experience diverged from expectations: initially focused on breakeven timelines and daily earnings (financial return), he became unexpectedly moved by non-financial benefits: improved mental state from 40 minutes of daily exercise, breaking post-work inertia, starting outdoor activities with family, losing two pounds in a month despite years of failed diets, and growing concern for personal health.

For him, STEPN started as a run-and-earn project—users naturally expect returns on both fronts upon entry. But during participation, a crucial mindset shift occurred: arriving primarily for financial gain, sustained engagement led to appreciation and gratitude for non-financial returns—utility gains. This is precisely what Axie Infinity lacked. We often say Ponzi-games end in death spirals and dispersal, but this added psychological transformation in STEPN might become a critical factor rewriting that outcome.

Inevitable Death Spiral Doesn't Mean Death

1. First, define three types of players:

Lucky Type A players, anxious Type B players, and观望 Type C players: The friend mentioned earlier joined a month ago and is nearing breakeven—we can call those who have broken even (or are close) lucky Type A players. Since the game doesn’t impose a lifespan on shoes, Type A players who keep going will profit indefinitely. Now, considering Type A’s success, two core questions arise for any Ponzinomics-based product:

1) Can those who recently bought shoes but haven’t broken even still recover their costs—and how long will it take? Let’s call these anxious Type B players.

2) Can those who haven’t bought shoes yet but are watching still enter profitably? Let’s call them观望 Type C players.

Clarification: A, B, and C aren’t fixed user identities—they’re classifications based on timing. Individuals can transition: B becomes A after breaking even; C becomes B upon entry.

2. How Will STEPN’s Death Spiral Differ From Axie Infinity?

One undeniable truth is that Ponzinomics cannot avoid the death spiral. However, I believe STEPN’s experience and outcome will differ meaningfully from Axie in three ways (again, not investment advice): 1) STEPN’s death spiral may have a longer latency period; 2) Its chain reaction may unfold more slowly; 3) Its post-spiral plateau could hold greater promise. Let’s discuss each.

1) STEPN’s Death Spiral May Have a Longer Latency Period (Warning! Theoretical Analysis, Not Investment Advice):

Axie:

a. Axie’s adoption of guilds led to explosive, unnatural growth—only 15% of players were individual users; 85% were guild members who could generate SLP without owning Axies. Guilds offered step-by-step tutorials, enabling quick onboarding and immediate income generation, with optimized yield strategies managed centrally, maximizing SLP output from rapidly scaling guild players.

b. Large-scale guilds and mercenaries extracted value far more efficiently than organic players:These guild players weren’t Type A/B/C as defined earlier—they were pure mercenaries focused solely on maximizing extraction from Axie Infinity’s ecosystem. Their efficiency vastly exceeded that of equivalent numbers of organically grown solo players. This rapid extraction brought short-term rewards, encouraging further expansion. Sky Mavis, enjoying fast growth, didn’t intervene much—or couldn’t, given the momentum. High-efficiency extraction combined with unnatural growth meant a shorter Ponzi lifecycle. AXS peaked in early November, just four months after its July surge, officially entering the death spiral.

c. Guilds and mercenaries may have been Axie’s necessary slow poison:What if there had been no guilds? Could Axie have stretched those four months to six or ten via organic growth? Or without guilds, would Axie have grown too slowly to attract new blood, dying even earlier? I don’t have a definitive answer, but I lean toward believing Axie couldn’t rely on organic growth alone—it had to swallow the life-saving poison of guilds. Traditional gamers wouldn’t willingly pay high prices to grind through such a dry game. In developing countries like the Philippines, without guild support, the complexity barrier of crypto tokens would deter users with lower learning or financial capacity. Guilds were thus almost inevitable for Axie—even if they carried known economic risks.

STEPN:

a. Firm commitment to organic growth—cracking down on cheating, rejecting guilds, no rentals:At the time of writing, official figures report 300K DAU—a stark contrast to Axie in that nearly all are real “one person, one device, one account” users. No guilds, no rentals, no easy loopholes. Entry requires self-learning crypto usage and personal payment. Thanks to strict monitoring and enforcement, unnatural growth is extremely difficult. Founders Jerry and Yawn have repeatedly emphasized their commitment to organic growth. Even the rental feature mentioned in the whitepaper—which relates to unnatural growth—Jerry confirmed in response to my direct question won’t launch for at least six months.

b. Project team exercises great restraint in tokenomics:The referral code system helps moderate onboarding speed. Features like gems and mystery boxes actively burn GST. Recent demand drivers added for governance token GMT indirectly relieve pressure on GST, with more utilities planned. The team, with gaming backgrounds, draws from both traditional games and P2E cases to innovate methods stabilizing token economics—aiming to extend the lifecycle Axie cut short.

c. Wealthy, eager-to-learn real users and high-quality crossover newcomers:This discipline results in a user base filtered twice: financially capable (entry fees are steep and self-funded), and knowledgeable (STEPN offers no lengthy beginner guides—users must learn wallet mechanics themselves—Jerry noted surveys show 30% of users are using decentralized wallets for the first time).

d. If desired, the team could open valves for unnatural growth to delay the spiral (though unlikely short-term):Despite visible rapid user growth, this data reflects genuine users under deliberate constraint. Value extraction efficiency pales compared to Axie’s guilds. Even if growth slows later, STEPN could theoretically reopen unnatural growth channels—lowering barriers—to further delay the onset of the death spiral.

2) STEPN’s Death Spiral May Unfold More Slowly:

Axie:

a. Though the death spiral involves chain reactions, Axie’s decline wasn’t cliff-like:Looking at AXS’s market cap post-spiral onset, the drop wasn’t vertical. Breakeven timelines extended, but dedicated grinders could still slowly recoup costs—though painfully. Gameplay enjoyment is limited; late-stage grinding purely for financial recovery becomes torture.

b. With little utility beyond financial returns, selling becomes the obvious choice:For most users, aside from earning, the game holds little appeal. If you personally invested real money into Axie, beyond break-even goals, the utility/enjoyment derived is too low. During the spiral, you're left only with frustration over diminishing financial returns. The rational move is to exit early—and most will do exactly that. With many thinking similarly, the collapse accelerates—not instantly, but not gradually either.

STEPN:

a. Users increasingly recognize utility returns beyond financial gains:Recall my friend’s story—the primary motivation was financial, but he gradually recognized utility returns (fitness, health, joy). Returning to an earlier point: people show low tolerance for sunk costs in financial investments, but much higher tolerance for utility investments. How does this extra tolerance manifest in STEPN? Let’s analyze:

b. Unlike Axie, STEPN gives utility-focused users a reason not to sell:So here’s the key question: Suppose you invested $1,000 at the peak, ran daily for a month, and saw your 50-day breakeven target stretch to a year or more—but suddenly realized huge non-financial benefits. What would you do?

Sell everything immediately, reverting to a sedentary lifestyle?

Acknowledge your progress and utility gains, realizing the breakeven goal has transformed from an investment expectation into a commitment to persistence—deciding to hold or reduce holdings minimally, extending your breakeven horizon to a year or more, gradually recovering costs?

If you choose to persist, you grow healthier and eventually recover costs and begin net profits. Selling means immediate financial loss and losing external motivation, likely abandoning a beneficial habit. If you’re already weighing these options instead of rushing to sell like Axie users, then STEPN’s downturn could indeed be slower.

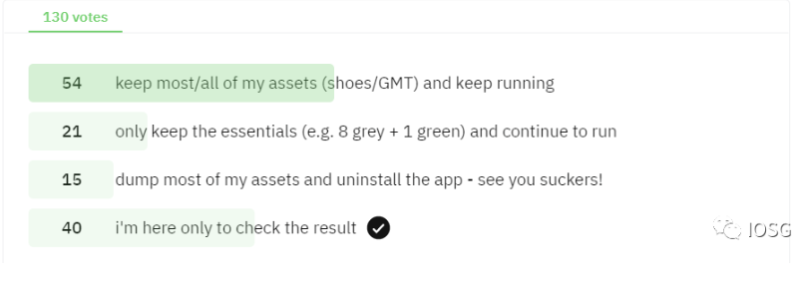

c. Survey shows 83% of users intend to stay during the spiral:Consider a Reddit poll I conducted in the STEPN community (see image below): “When STEPN enters a death spiral like Axie, what will you do with your assets?” I expected most to choose full exit. Surprisingly, 60% said they wouldn’t sell GMT or shoes and plan to keep running; 23% would retain key shoes (e.g., 1 gray or 1 green + 8 gray); only 17% chose full liquidation:

Of course, this survey carries no legal weight—those saying they’ll hold may still sell when prices fall. But I believe such results would be unimaginable in the Axie community. Therefore, I expect selling pressure during STEPN’s spiral to be significantly lower, the decline gentler, and negative impacts on breakeven periods smaller than typical blockchain games—because some users shift focus toward utility, reducing sensitivity to financial returns.

3) STEPN’s Post-Spiral Plateau May Hold Greater Potential:

Axie:

a. The spiral’s outcome isn’t death, but revealing the product’s fair market value:After the sharp spiral decline, AXS has stabilized around a $3 billion market cap for nearly three months. Axie prices dropped to around $50—accessible to more people. Entry barriers are now low, though breakeven remains long. But since utility returns (gameplay fun) are limited, players aiming to profit still suffer. Meanwhile, 85% of players were mercenary guild members whose yields now fall below real-world wages, lowering participation. Ironically, genuine players who previously wanted to try Axie but found entry too expensive—the “watching Type C players”—now get their chance. The death spiral ended Axie’s hyper-hype phase, finally opening doors to authentic users. Guilds and mercenaries are unhappy with lower yields, but the spiral created opportunities for true players seeking enjoyment. My colleague Alex and I believe P2E isn’t the end goal, but a user acquisition (UA) strategy—Axie indirectly validated this: P2E mania skipped cold-start marketing costs, enabling rapid capital, user, and product development. After the spiral, entry aligns with intrinsic fair value, welcoming players motivated by gameplay—not speculation.

STEPN:

a. STEPN will stabilize at a higher plateau value than Axie, with more users and a larger market:When the cheapest gray shoe drops from $1,000 to say $100, breakeven may take a year. Those unable to persist turn their investment into sunk cost, subsidizing those who continue. As initial investment drops, users become more tolerant of sunk costs, increasing abandonment and thus collected sunk funds—creating a stable equilibrium similar to AXS’s current price floor. At this stage, STEPN transforms from a money-making scheme into a commitment contract: paying $100 to enforce your own running habit. Stick with it, and you not only recover your $100 but potentially earn steadily beyond. How does that sound?

b. Clones may survive temporarily but won’t last—won’t affect STEPN’s long-term value:Smart readers might ask: why not switch to a clone later and earn more? Consider Axie: no project has more clones. What happened to them? Some made money, but their cycles were shorter, caps smaller, and demands on profitable players unusually high: deep knowledge of high-yield schemes, market manipulation awareness, perfect timing. Yes, financially sensitive STEPN users may flock to clones for extra gains, but eventually, clones fade, leaving users bruised but with established habits, returning to proven, lower-yield but stable STEPN. And that’s just the financially driven cohort. Utility-focused users won’t risk clones requiring heavy effort. This is a fundamental difference between STEPN and Axie users—Axie’s guild players relied on this income to live. How could they not maximize returns? Coupled with STEPN’s social features, stronger narratives, ability to develop non-Ponzi revenue streams (e-commerce, carbon credits, brand partnerships), founder storytelling skills, and user authenticity and quality—I believe STEPN has the potential to become a brand outlasting Axie.

While the death spiral is unavoidable under Ponzinomics, my purpose in writing this is to emphasize the following:

First, the death spiral doesn’t mean death or product failure—it’s the process of returning from X2E mania to intrinsic fair value. The pre-spiral latency varies, the descent speed differs, and the eventual fair value level ranges widely.

Axie, as the first breakout X2E project, underwent extensive trial and error, revealing X2E’s possibilities, limits, and long-term challenges—enabling successors like STEPN to learn, extract best practices, and innovate. X2E is evolving.

What we hope for in X2E evolution is a more restrained boom, a slower cooldown, and a higher fair-value baseline—precisely what I believe STEPN has the potential to achieve.

More importantly, we must ultimately shift toward a mainstream user base that recognizes the project’s intrinsic value, ensuring utility-driven investors—not speculators—capture most gains. (Participants should see it not as investing $10 to earn $20, but investing $10 that inherently matches the utility value delivered, plus an extra $3 returned—with persistent users possibly getting $10 or even $20 back.)

Beyond Ponzinomics, future external economic inflows represent my greatest hope for X2E—offering richer narratives and broader potential than current blockchain P2E. For instance, I recently discussed a Bike-to-Earn project (MOTE by Sweetgum Labs—interested investors welcome to connect) involving carbon credit monetization. Example: someone switching from a 10km daily commute by car to bike saves 4 tons of CO₂ annually. At €80 per ton in Europe, that’s over €300 in annual revenue reinjected into the system. Rising carbon prices will further boost this mechanism’s potential. Despite operational and pricing challenges, I’m highly encouraged by X2E projects striving to connect with external economies.

Closing Thoughts

Having highlighted areas where I believe STEPN holds advantages over Axie, let me reiterate: this is not investment advice. Project outcomes depend heavily on leadership and major stakeholders beyond fundamentals—STEPN’s swift collaboration with top exchanges and whales’ generous pumping reveal strengths beyond basic metrics. Ultimately, STEPN’s trajectory hinges on balancing internal dynamics amid volatile markets. The above analysis speculates on potential future milestones and potentials based on current information. Only time will tell how it unfolds.

Join TechFlow official community to stay tuned

Telegram:https://t.me/TechFlowDaily

X (Twitter):https://x.com/TechFlowPost

X (Twitter) EN:https://x.com/BlockFlow_News